NOC - Northrop Grumman: Increase In Defense Budget And Favorably Valued

2023-03-06 23:20:26 ET

Summary

- Northrop Grumman’s James Webb Space Telescope is an amazing piece of engineering. The telescope can observe and determine the chemical components of exoplanets' atmospheres.

- Order backlog was also very strong and is 2x the size of sales in 2022.

- Management is shareholder friendly, paying dividends and buying back as many shares as it generates in free cash flow.

- Although Northrop Grumman expects a decline in operating margins for 2023 due to increased inflationary pressures, many analysts expect earnings per share to rise sharply after 2023.

Introduction

Northrop Grumman ( NOC ) is one of the largest defense companies in the world with well-known defense vehicles, aircraft, ships and space systems such as the James Webb Space Telescope and others.

About 80% of its revenues come from government contracts, and revenues have increased sharply by 41% over the past 5 years. Looking at the stock price, we see excellent returns averaging 24% per year, compared to 12.4% for the S&P 500. Investors must wonder if NOC stock price is overvalued, but it is not. Northrop Grumman offers strong earnings growth, a shareholder-friendly management and a favorable stock valuation.

Strong 2023 Outlook

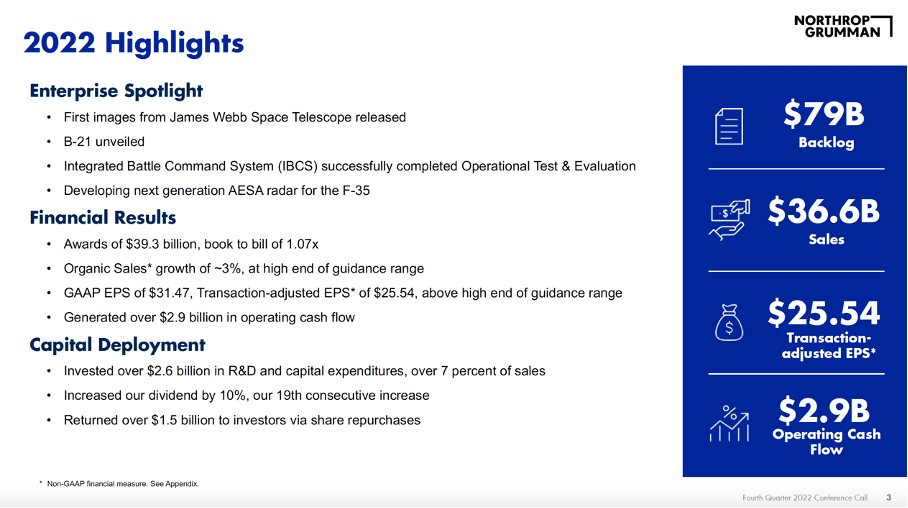

Northrop Grumman delivered strong fourth quarter and full year 2022 results with revenue growth of 15.7% year over year and non-GAAP EPS growth of 25% year over year which were above expectations. Order backlog has grown to an astounding amount of more than 2x times 2022 revenue due to the rising U.S. defense budget.

One project worth mentioning is the James Webb Space Telescope which is now the world's most powerful space telescope and has been operational since 2022. It provides stunning images and observes the four most distant galaxies known. It can gain insight into the atmospheres of exoplanets by analyzing the transmission spectrum. The James Webb Space Telescope is an outstanding piece of technology engineered by scientists at Northrop Grumman.

2022 Highlights (Northrop Grumman's 4Q22 Investor Presentation)

{kind=link}

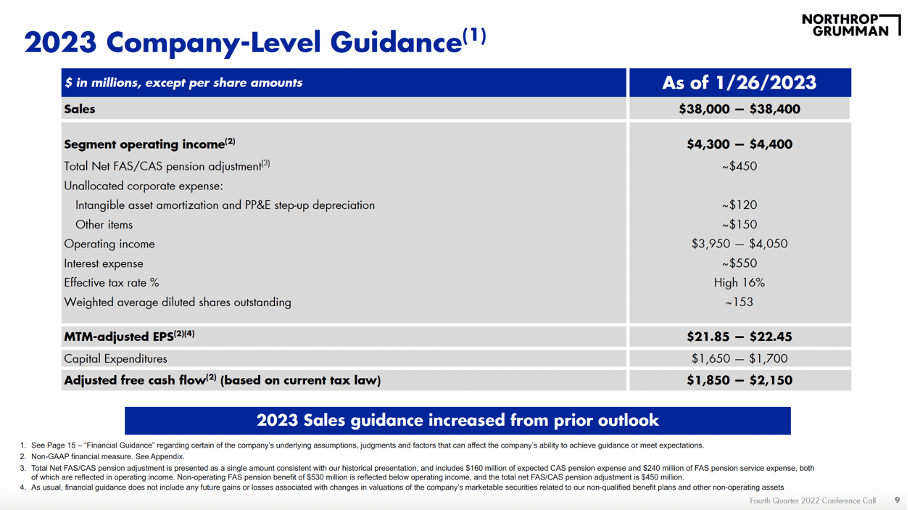

Defense budgets were increased 10% year over year to $858 billion for National Defense. Global threats are increasing rapidly, and Northrop Grumman offers defense products that provide increased security through air and missile defense, radar capabilities, munitions and armaments, and global surveillance systems.

Therefore, Northrop Grumman expects a strong outlook for 2023, and management expects revenue to grow 4.4% at the halfway point. However, adjusted earnings per share are expected to decline to a range of $21.85 to $22.45 due to cost inflation.

2023 Company-level guidance (Northrop Grumman's 4Q22 Investor Presentation)

{kind=link}

Northrop Grumman Is Shareholder Friendly

Northrop Grumman has been paying a steadily growing dividend for years. The dividend has grown from $2.15 in 2012 to $6.76 in 2022; an average growth rate of 12.1% per year. The expected dividend stands at $6.92, representing a dividend yield of 1.48%.

Dividend growth history (NOC ticker page on Seeking Alpha)

{kind=link}

The dividend payout has increased annually and, in addition, Northrop Grumman also repurchases shares, increasing the dividend per share as the number of shares outstanding decreases. Share repurchases also create additional demand when purchased on the open market. Companies buy back shares when they believe their stock is undervalued; this increases earnings per share. Let's see if shares are indeed undervalued.

Northrop Grumman's Cash Flow Highlights (SEC and author's own calculations)

{kind=link}

Temporary Headwinds But Favorably Valued

As with Lockheed Martin ( LMT ), I compare Northrop Grumman's EV to EBIT ratio and P/E ratio to historical figures. And I also try to gain insight into its forward valuation.

Currently, the EV to EBIT is 12.9, which I think is quite low compared to the general market. Lockheed Martin's EV to EBIT is at 18.3, so Northrop Grumman seems undervalued compared to a peer in the defense sector. The 3-year median notes 11.8, but that is due to a strong undervaluation at the 2022 start.

The PE ratio provides another view of the stock's valuation. It currently stands at 14.9, which is undervalued compared to the S&P's PE ratio of 21.6. At the beginning of my article, you saw that Northrop Grumman's 10-year total return was 764%, compared to the S&P500's return of 222%. The funny thing is that Northrop Grumman's P/E ratio almost never exceeded that of the S&P 500 over the past 10 years, and yet the company outperformed the S&P 500 thanks to strong earnings growth.

In the chart below, we can also see that the PE ratio is a bit overvalued relative to its 3-year average. But not to worry, even in this climate of high interest rates, I find a P/E ratio of 13.9 very attractive.

Looking ahead, many analysts expect non-GAAP earnings per share to rise in the coming years. But for 2023, they expect a low double-digit decline, making the P/E ratio quite expensive compared to historical figures. From then on, however, growth is expected to return with a forward P/E ratio of 17.

Compared to industry peer Lockheed Martin, we see that here too, earnings per share are expected to decline slightly in 2023 but is expected to increase from then on. The projected 2025 P/E ratio of both companies is about 17, but Northrop Grumman's earnings growth is much stronger than Lockheed Martin's.

Thus, we can conclude that both companies expect temporary headwinds in 2023, but growth should return in the period thereafter. Northrop Grumman's earnings per share are expected to grow faster, and the forward valuation is about the same for both companies. In this comparison, I would rather invest in Northrop Grumman than Lockheed Martin.

Earnings estimates for NOC and LMT (Seeking Alpha and author's own visualization)

{kind=link}

Conclusion

The James Webb Space Telescope is a great engineering piece by Northrop Grumman. This telescope can determine the chemical components of exoplanets' atmospheres. Northrop Grumman is one of the world's largest defense companies, providing air and missile systems, radar systems, munitions and weapons, global surveillance systems and many more. The United States' defense budget has been increased by 10% a year due to the increase in global threats. This will benefit Northrop Grumman greatly and could be seen as a strong catalyst. Its fourth quarter results were strong as revenue was up 15.7% year-over-year. Order backlog was also very strong and is 2x the size of revenue in 2022. Its management is shareholder friendly, paying dividends and buying back as many shares as it generates in free cash flow. Furthermore, looking at the valuation of the stock, we see a strong undervaluation based on the EV/EBIT ratio, but also on the P/E ratio. Although Northrop Grumman expects a decline in operating margins for 2023 due to increased inflationary pressures, many analysts expect earnings per share to rise sharply after 2023. The stock's valuation looks healthy and the stock is worth buying.

For further details see:

Northrop Grumman: Increase In Defense Budget And Favorably Valued