NOC - Northrop Grumman: My Favorite High-Tech Investment

2023-09-10 03:48:11 ET

Summary

- Northrop Grumman is a highly advanced defense contractor with a focus on next-gen areas like hypersonics and space.

- NOC has tremendous growth potential in space and related industries, with its Space Systems segment generating over $12 billion in revenues.

- The company is well-positioned in the fast-growing space industry, with a high-tech portfolio and a strong domestic customer base.

Introduction

Earlier this month, I wrote an article covering the Schwab U.S. Large-Cap Growth ETF ( SCHG ). In that article, I mentioned that I own no technology stocks.

However, I would make the case that I may own one of the most high-tech companies in the world: the Northrop Grumman Corporation ( NOC ) .

Technically speaking, the company is a player in the industrial sector. However, it may be one of the most advanced defense contractors in the world, focusing on next-gen areas like hypersonics and space, the fastest-growing segment in this area.

On July 28, I wrote an article titled Northrop Grumman: Strong Buy As It Sees A Path To Double Free Cash Flow . Since then, shares have lost roughly 6% as the market continues to flee from sectors that may be negatively impacted if inflation remains sticky.

While I cannot disagree with that thesis, in general, the market is throwing the baby out with the bathwater.

In this article, I'll reiterate why I remain an aggressive buyer of NOC stock. However, unlike in my prior article, I will focus on one of the most undercovered aspects of the NOC investment: its tremendous growth potential in space and related industries.

While NOC appears to be more expensive than some of its peers, its future free cash flow growth potential is stunning, making it a strong buy for dividend growth investors.

So, let's get to it!

NOC Is Where It's At

On a side note, another stock I really like in this area is L3Harris Technologies ( LHX ). The other day, I updated my bull case, stating that LHX shares are up to 50% undervalued . Like NOC, LHX is also well-diversified with space exposure.

The difference is that NOC is bigger, with more exposure in high-growth areas.

With a market cap of more than $60 billion, Northrop Grumman ((NOC)) is one of the largest defense contractors in the world.

The company is the result of the merger between Northrop and Grumman. Both companies started before the Second World War. They built aircraft that were essential in winning the war and later focused on ballistic missiles, radars, and so much more.

Pictured below is the Grumman F6F Hellcat, a plane that was designed to combat the advanced planes of the Japanese during the Second World War.

Wikipedia (Grumman F6F Hellcat)

In 2018, the company bought Orbital ATK, a company with significant space and missile/ammunition exposure, further increasing NOC's highly diversified footing in the defense industry.

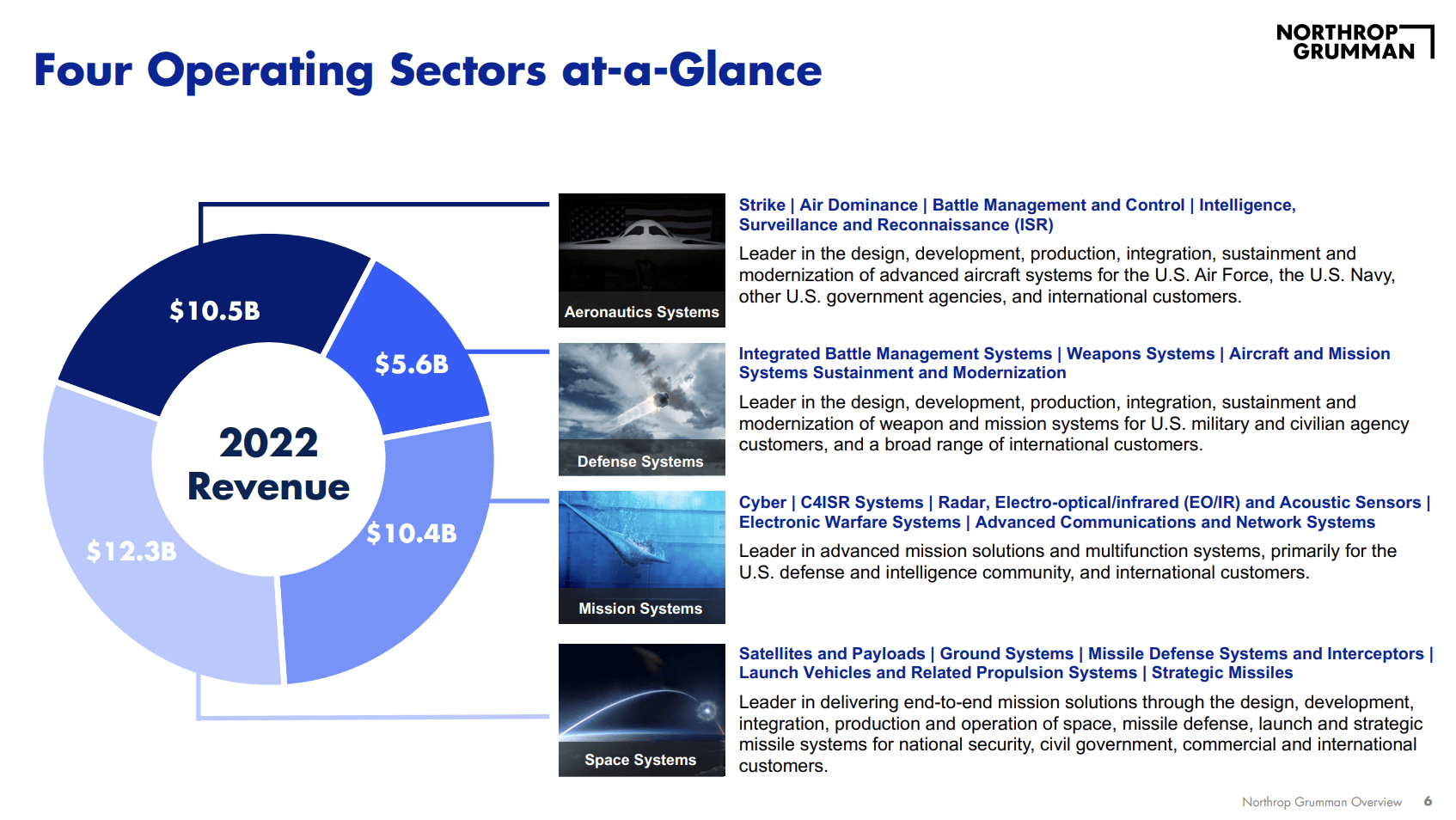

Fast forward to 2022, the company operated four major business segments, each generating more than $5 billion in revenues.

{kind=link}

These segments include air dominance like the B-21 Raider stealth bomber, a range of full-spectrum cyber solutions, modernization services for land infrastructure and vehicles, sonar for the Navy, Multi-Domain warfare solutions, and a wide range of advanced weapons, including hypersonics, intercontinental ballistic missiles, and air-to-ground missiles for modern jets.

It also builds fuselages for Lockheed Martin's ( LMT ) F-35.

On top of that, the company also engages in high-tech innovations like disruptive quantum computing , which is one of many reasons why the company is an innovation powerhouse, which is often overlooked as people think it's an industrial stock that only makes money when nations start firing missiles at each other.

Based on that context, I have close to 20% defense exposure. I never decided to go big into defense to benefit from wars. On the contrary, I believe that advanced defense technologies prevent wars. As far as history books go back, warfare has been among the biggest sources of innovation. Innovation is what keeps wars from happening.

While Russia has advanced into Ukraine, I believe that NATO nations are safe. Mainly thanks to advanced weapons and systems that would make any attempt to invade NATO nations too bloody .

The US has an overwhelming advantage over Russian troops . This month, Joe Biden said he would request an additional $24 billion from Congress for Ukraine, “and other international needs related to the war”, said Al Jazeera.

Biden and his team have said the US will help Ukraine “as long as it takes” to remove Russia.

For all his threats, said Tisdall, “ Putin fears Russia-Nato conflict ”. For him, it would be “political and military suicide”.

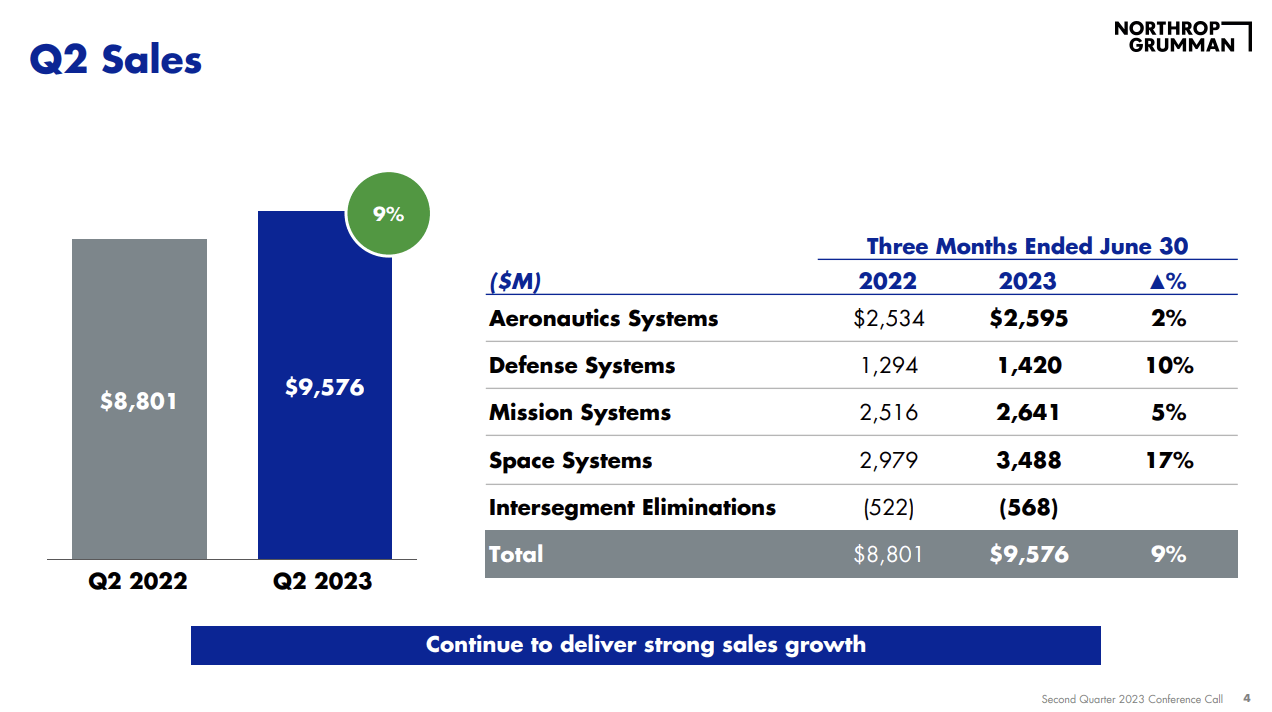

Furthermore, NOC isn't just highly diversified, but it has very high exposure to fast-growing areas. Looking at the overview above, the Space Systems segment alone generated more than $12 billion in 2022 revenues. This makes space the company's largest segment, with 32% of total revenues!

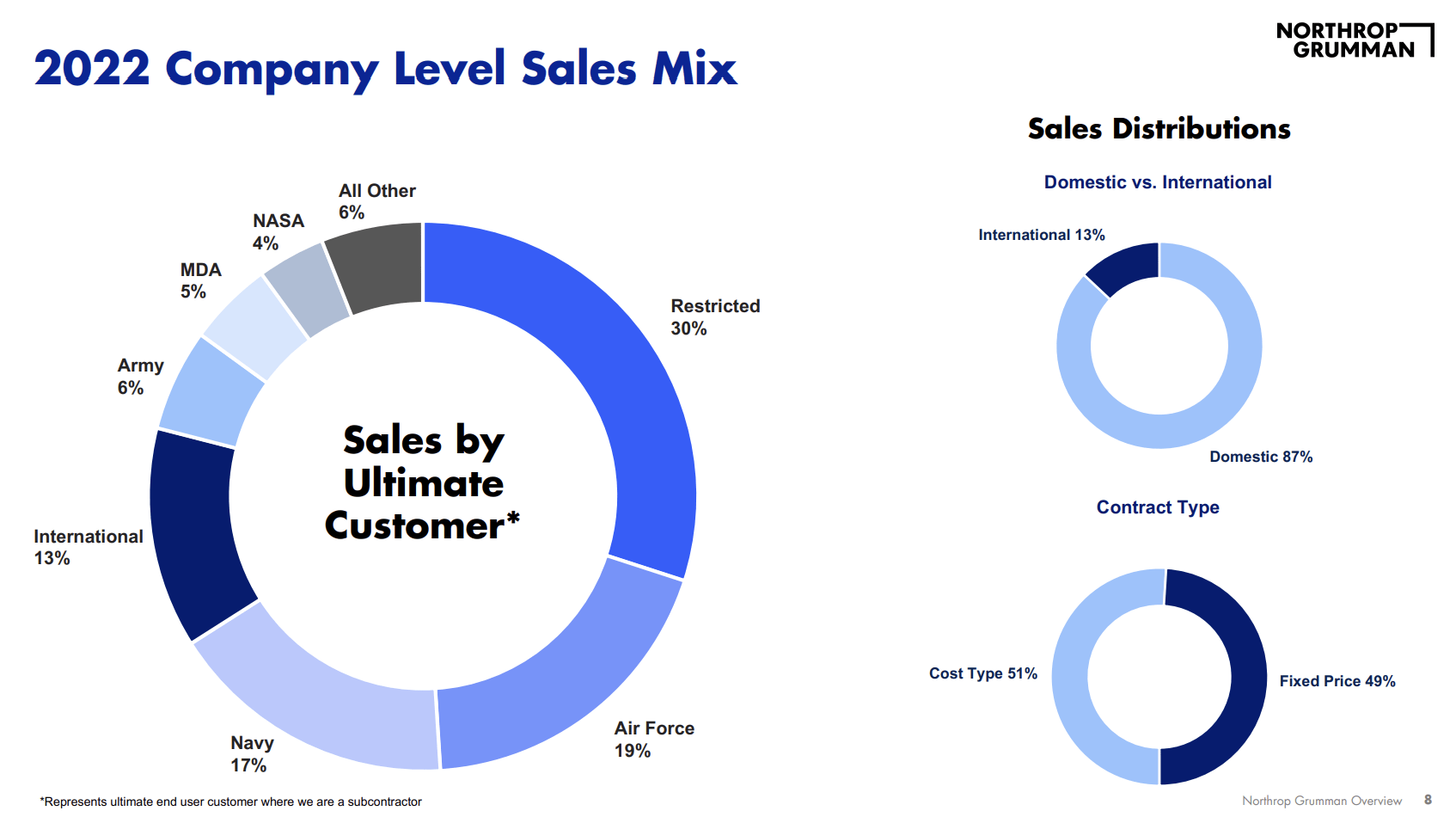

The company is so high-tech that almost all of its sales are domestic. Roughly a third of its sales are for restricted customers. It also has the benefit of having close to 50% cost-type contractors, which means half of its contracts automatically adjust for inflation.

However, Northrop Grumman anticipates a shift in its business mix towards more fixed-price revenue, rising to approximately 60% of sales by 2027.

This shift is driven by programs transitioning from development to production, which typically yield higher margins. During its 2Q23 earnings call, the company cited progress in moving programs into production, such as the AARGM ER program and the B-21 program.

International business growth is also expected, contributing to improved margin opportunities.

{kind=link}

Going back to its Space Systems sector, there's a lot to unpack.

Fast Space Growth

Space has always been a fascinating subject since the race for the first moon landing after the Second World War.

Now, it's becoming an even more important subject, as space isn't just the place where we put satellites for crucial communications, but it's also a way to build new defense capabilities.

Northrop may be the go-to player in this space without having to buy smaller, high-risk startups.

In addition to securing our world, we've always pioneered exploration and discovery . Our teams designed the iconic Apollo Lunar lander and were instrumental in returning the Apollo 13 crew safely home . This passion for deep space continues today with cutting-edge exploration programs such as the James Webb Space Telescope ("JWST"), safety initiatives such as the Launch Abort System ("LAS") and purpose-built spacecraft designed to change the way we view space exploration. - Northrop Grumman

In its Space Systems segment, the company sells 97% to domestic customers. More than 70% of all contracts are cost-type (inflation-protected) contracts. 35% of its customers are restricted. NASA accounts for 11% of revenues.

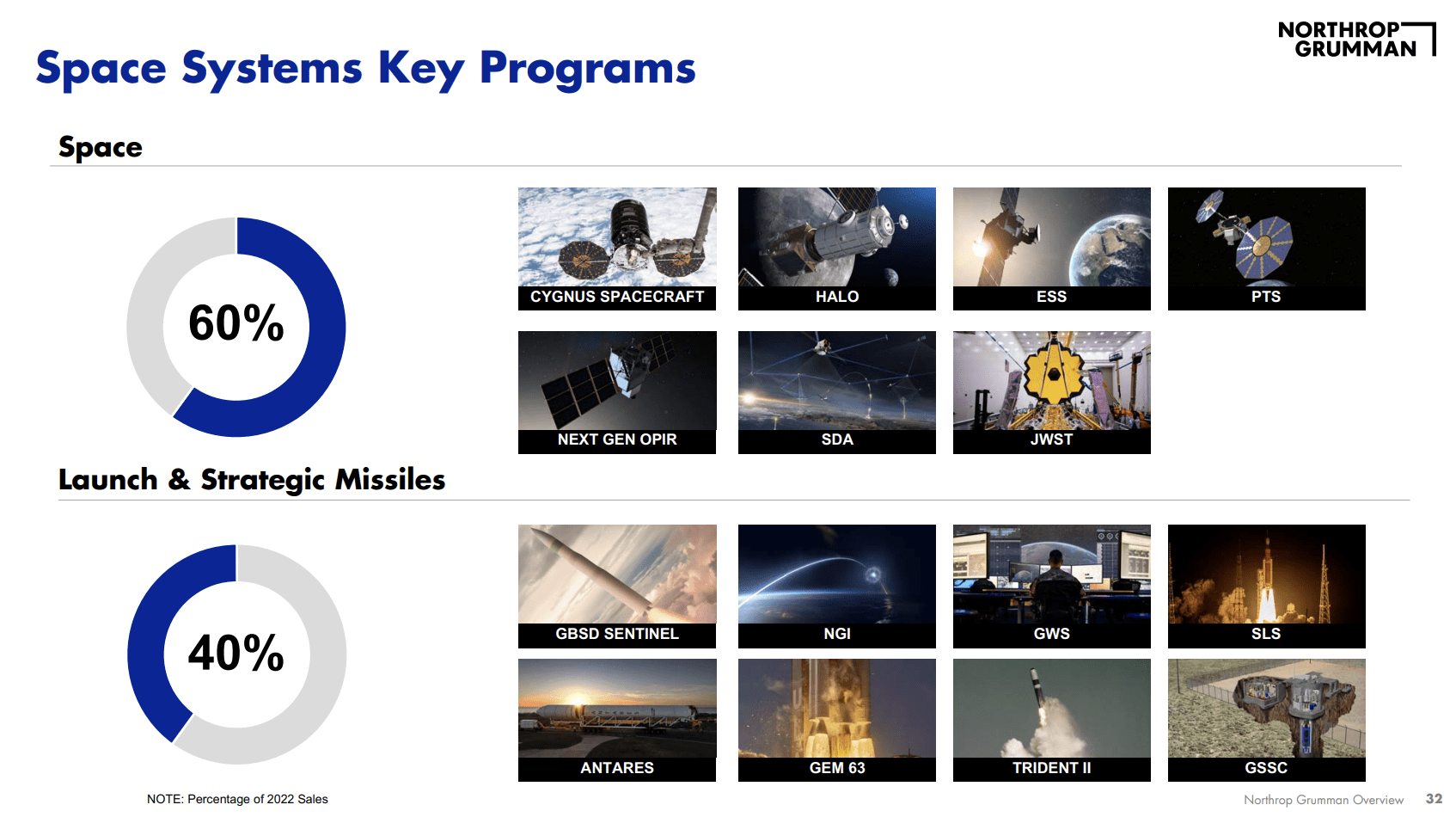

In this segment, the company focuses on 60% space (mixed-use) and 40% defense purposes. After all, space is becoming the next focus for militaries. It's also why the U.S. launched its Space Force.

The company not only builds supplies for payload support, launch vehicles and propulsion systems, and commercial communication satellites, but it also builds the GBSD Sentinel, a future land-based intercontinental ballistic missile system.

{kind=link}

Space doesn't just sound like a fast-growing business, but it's proven to be the best place to be.

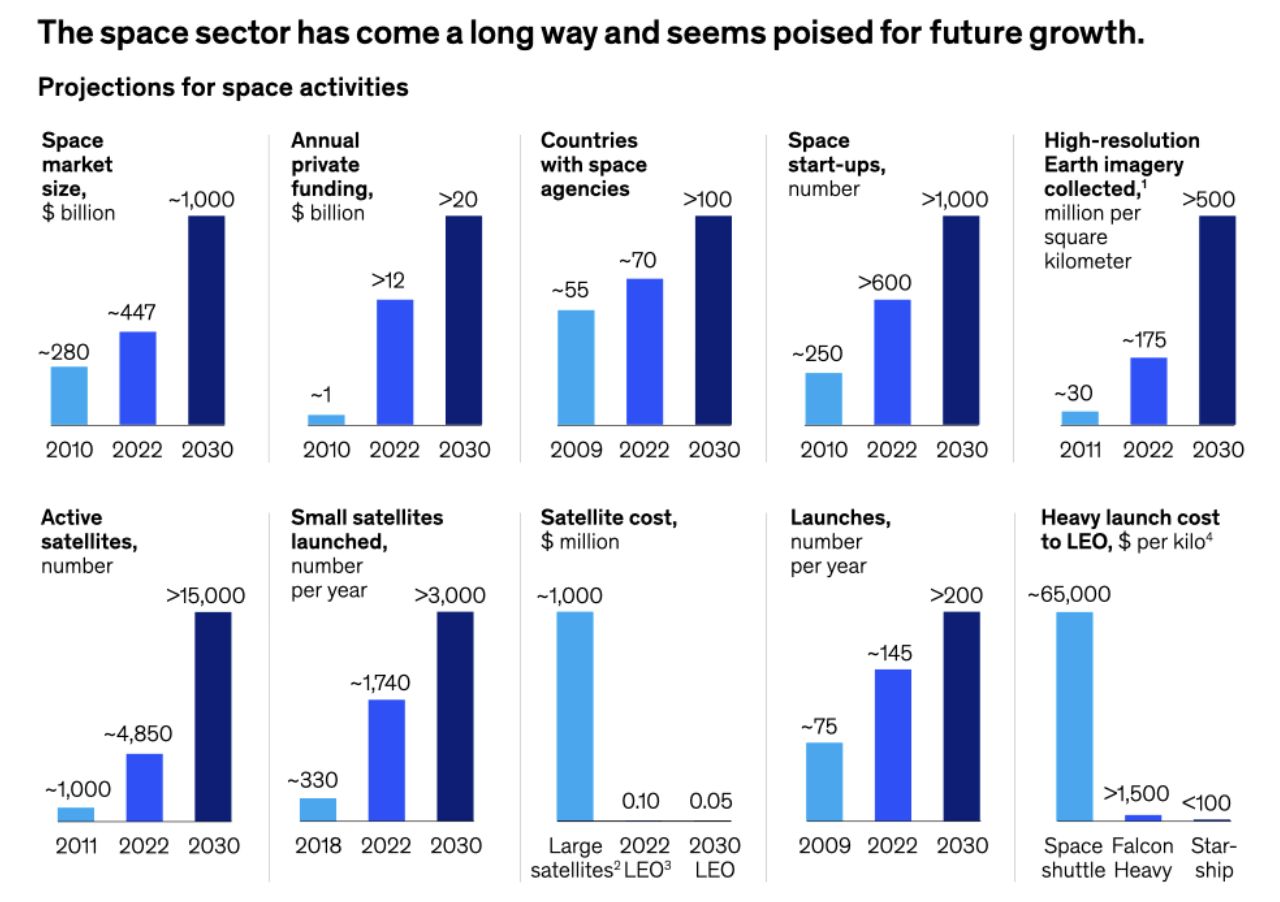

For example, in March, Deloitte focused on the exponential growth in space.

The company wrote that the year 2022 marked a historic milestone in the space industry, with a record-breaking 186 successful rocket launches, 41 more than the previous year.

This surge underscores the rapid transformation of the space sector, setting the stage for an era of unprecedented growth.

Despite lingering uncertainties and challenges, a collaborative approach, backed by public and private investment, holds the potential to establish a self-sustaining industrial base in the space ecosystem.

This is also becoming clear to U.S. military leaders.

{kind=link}

As reported by the Wall Street Journal , the United States is extending its efforts to promote closer military integration among its allies to the realm of space. Gen. Chance Saltzman, the Chief of Space Operations, has outlined plans to encourage allies to collaborate in training and planning for space operations, paralleling the existing cooperation seen in ground, air, and naval combat.

This initiative arises from growing concerns over China and Russia's capacity to disrupt Western satellites and employ advanced space technology, including satellites capable of intercepting others. Notably, Russia has engaged in operations to disrupt Ukraine's space-enabled communications, emphasizing the critical role of space in modern warfare.

Russia and China have developed significant capabilities in space. Russia has been deploying satellites in close proximity to those of other nations, with some capable of releasing objects for potential attacks in space.

China, on the other hand, has tested robotic arms for capturing other satellites and demonstrated missiles capable of destroying orbiting satellites.

On top of these increasing defense-related threads, McKinsey sees exponential growth until at least 2030 (and likely beyond!). In 2022, the space market had a $447 billion size. That number is set to more than double by 2030. The number of active satellites could break 15,000 - up from less than 4,900 in 2022.

{kind=link}

As a result, we're seeing these expectations tuning into strong growth for NOC.

In the second quarter, Space Systems saw 17% revenue growth. The company's total revenue growth was 9%.

{kind=link}

According to the company:

[...] our space business continues to deliver outstanding sales growth and bookings, demonstrating the strength of its diverse portfolio capabilities. As a result, we're increasing sales guidance for space to the high $13 billion range.

[...]

With respect to margin rates. We're maintaining our expectations for as AS, DS and MS and we're projecting a lower operating margin rate at space to reflect the rapid increase in new program winds and their first half results. - NOC 2Q23 Earnings Call

Furthermore, because of its diversification in high-tech areas, the company benefits from targeted growth in defense spending, which offsets some of the ongoing budget risks.

In its 2Q23 earnings call, the company mentioned that the FY24 budget and recent congressional committee bill prioritize modernization in areas where Northrop Grumman excels, such as the triad, space domain, information superiority, and advanced weapons.

The company also anticipates continued support for Ukraine and related emergency spending, which could increase demand further.

Shareholder Distributions & Outperformance

Another reason why I like Northrop is its dedication to shareholder distributions. Northrop Grumman recently increased its dividend for the 20th consecutive year by 8% and has returned $1.5 billion to shareholders in the first half of this year.

The company remains confident in its growth trajectory, driven by the global defense budget outlook and alignment with customer priorities, and is focused on margin expansion and free cash flow growth for the benefit of customers and shareholders, which should continue the impressive streak of buybacks and dividend growth.

Not only has the company hiked its dividend for 20 consecutive years, but it has also bought back 30% of its shares between 2013 and 2022!

The average dividend growth rate between 2013 and 2022 was 12%.

{kind=link}

The current yield is 1.8%, protected by a sub-30% payout ratio.

Dividends are also protected by a healthy balance sheet. The company has a sub-2x net leverage ratio and a BBB+ credit rating.

Thanks to anti-cyclical demand, innovative power, and the ability to maintain consistent dividend growth and buybacks, NOC shares have returned 437% over the past ten years, beating the S&P 500 by a considerable margin.

Although the industry is currently dealing with supply chain and inflation-related headwinds, I expect NOC to keep outperforming the market on a long-term basis.

Valuation

Northrop Grumman shares are down 23% year-to-date, making it one of the worst performances since the Great Financial Crisis. This is due to budget uncertainty and sticky inflation, and it applies to a wide range of high-quality companies across multiple sectors.

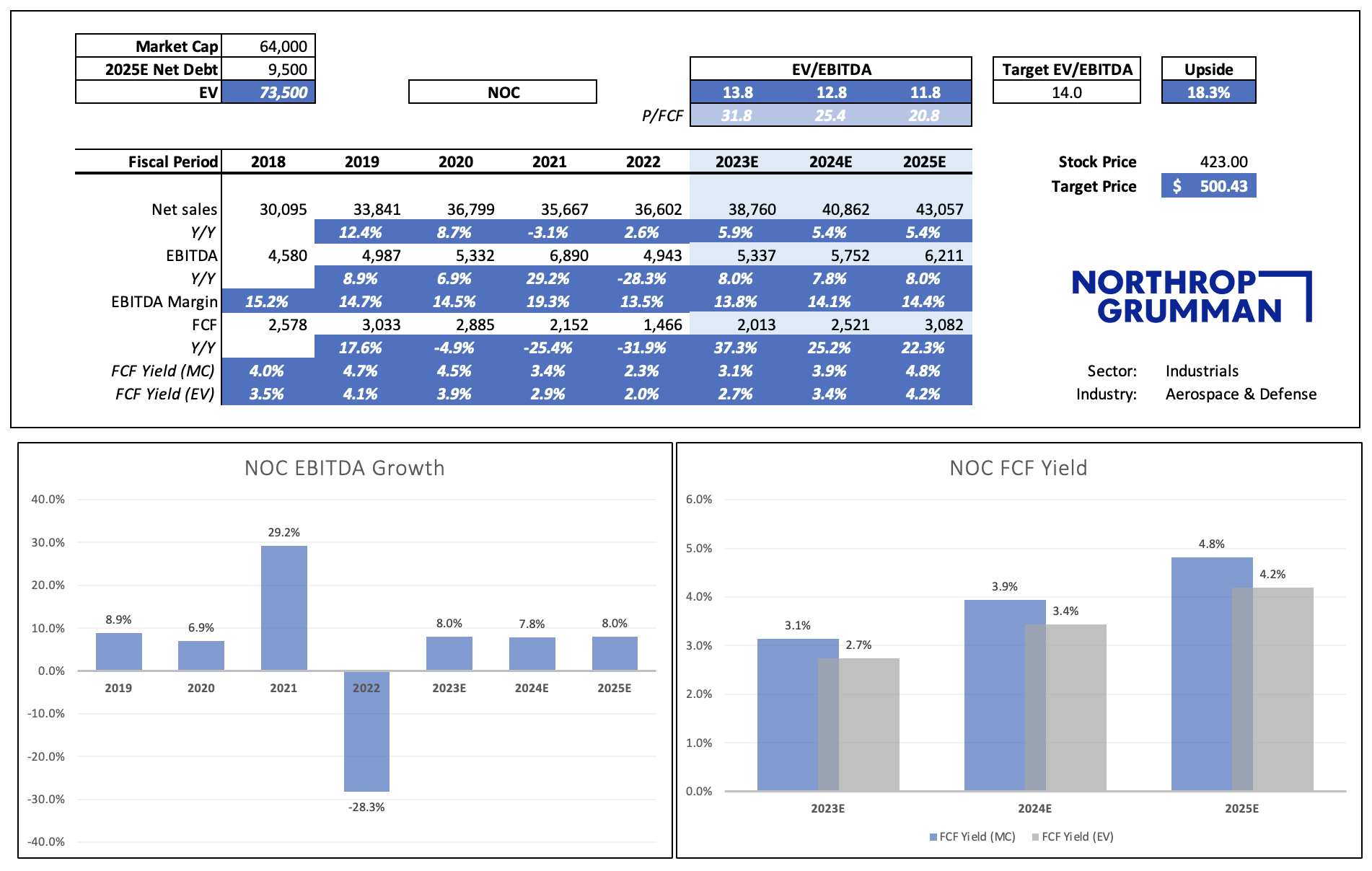

The company is currently trading at 13.8x EBITDA. That number drops to 11.8x using 2025E numbers. As the data below shows, the company is expected to maintain annual EBITDA growth rates close to 8%.

Leo Nelissen (Based on analyst estimates)

{kind=link}

Even more impressive than EBITDA growth is free cash flow growth. Free cash flow growth is expected to average more than 22% in the next two years.

By 2028, NOC might be able to double its free cash flow!

[...] over the next five years, we see an opportunity to approximately double our current level of free cash flow. - NOC 2Q23 Earnings Presentation

If we apply a 14x EV/EBITDA multiple, we get a fair price target of $500, which implies close to 20% upside.

The current consensus price target is $504.

As I said in my prior article, I believe that NOC is in a great position to beat the market and deliver double-digit returns on a prolonged basis.

Strong defense tailwinds, its focus on next-gen and high-tech products, and the path to much higher margins make it a highly attractive investment for me.

Takeaway

Northrop Grumman Corporation might not be your typical high-tech stock, but it's undoubtedly one of the most advanced players in the defense industry, especially when it comes to the exciting world of space technology.

With a market cap exceeding $60 billion, NOC boasts an impressive portfolio, including cutting-edge innovations like quantum computing.

Space is no longer just about satellites; it's the future of defense capabilities, and NOC is leading the way.

Despite market fluctuations and budget concerns, NOC stands out with its commitment to shareholder distributions, boasting 20 consecutive years of dividend increases and a history of buybacks. The company's growth trajectory, combined with its financial stability, makes it an attractive long-term investment opportunity.

So, while NOC may not fit the traditional high-tech mold, its high-tech future in space and defense positions it as a strong buy for those seeking both innovation and growth in their investment portfolio.

Reasons To Be Bullish

- Innovation : Northrop Grumman is an innovation leader in the defense industry with a history of groundbreaking technologies.

- Space Growth : NOC's significant exposure in the high-growth space sector positions it for substantial growth.

- Dividend Stability : NOC's 20-year streak of dividend increases showcases its commitment to shareholders.

- Defense Strength : NOC benefits from strong defense trends, ensuring long-term viability.

- Cash Flow Potential : Expectations of doubling free cash flow by 2028 underscore NOC's financial strength.

- Value Opportunity : With an attractive valuation, NOC presents a compelling investment prospect for the future.

For further details see:

Northrop Grumman: My Favorite High-Tech Investment