NOC - Northrop Grumman: Near-Term Risks But Long-Term Growth

2023-11-14 06:39:17 ET

Summary

- Northrop Grumman's shares have lost 13% in the past year due to concerns about defense spending and budget outlook.

- The company reported strong Q3 results with increased revenue and orders, raising its revenue guidance for the year.

- However, uncertainties in defense spending and political risks may impact future growth, but the company is focused on returning capital to shareholders.

Shares of Northrop Grumman (NOC) have lost about 13% over the past year, despite a world that sees an abundancy of threats, from the war in Ukraine, ongoing tensions with China, and the recent Israeli-Gaza war. These forces have confronted an increased austerity drive out of Washington, restraining the outlook for defense spending. Since recommending investors buy shares last October , NOC has essentially tread water, losing about 3%, as the budget outlook has undershot my expectations. NOC is operating well, and I view it as a long-term buy, but near-terms risks are clouding the outlook.

{kind=link}

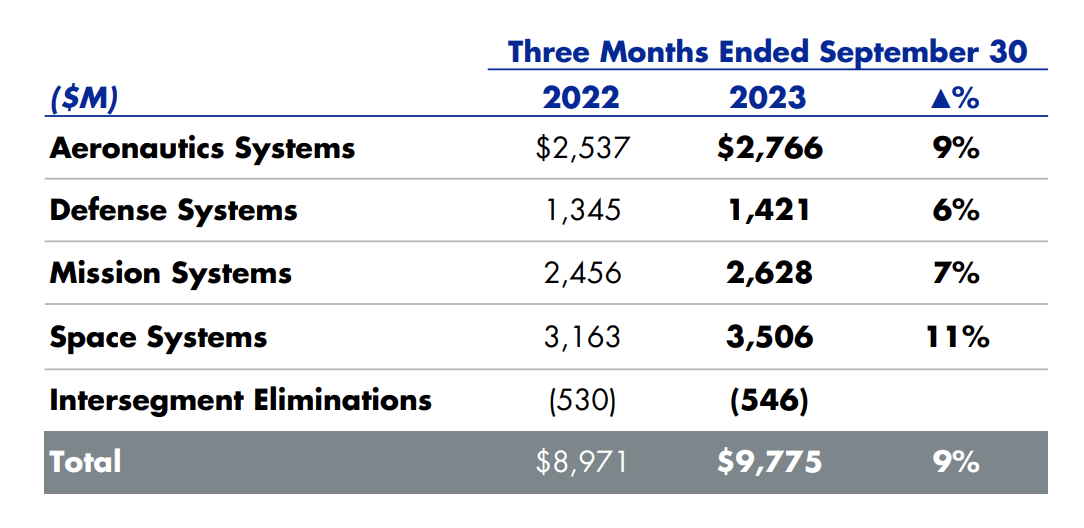

Looking first at reported results before turning to the outlook; in the company's third quarter , Northrop Grumman earned $6.18, which was up from 5% from last year, despite pension accounting headwinds. This beat consensus by $0.40, and revenue rose by 9% to $9.8 billion, a really solid outcome as NOC benefitted from stronger defense spending and improved supply chains.

Critically, this revenue growth is strong across the board with each of its four business units reporting year over year growth. In particular, aeronautics was boosted by higher deliveries of aircrafts with margins down a slight 10bp to 10.2%. Defense systems manufactures ammunition. As the US has supplied Ukraine with significant amounts, there has been strong demand to restock our own inventories. This is boosting sales, and margins rose 110bp as investments over the past year in scaling up facilities to boost capacity is paying off. Space margins declined 30bp due to lower net adjustments for project costs.

{kind=link}

Given this strong third quarter, Northrop now sees aeronautics and defense systems outperforming previous expectations, allowing it to raise revenue guidance to $39 billion from $38.4-$38.8 billion previously. Due to slightly lower mission margins, free cash flow is still expected to fall in the $1.85-$2.15 billion range with $22.45-$22.85 in EPS, though I view both likely to come in at the higher end of what are fairly wide ranges.

Importantly, because of strong demand, the company received $15 billion in orders during the quarter, for a book to bill ratio of 1.5x. It is essential to see this ratio stay above 1x to maintain revenue levels over time. Ideally, I like to see 1.1x to allow for upwards of 10% revenue growth. NOC blew past this level, providing meaningful future revenue opportunities. Its backlog now stands at $84 billion. Per its financial filings, 40% of the backlog is expected to be delivered on within the next year, 25% in the following year, and 35% thereafter.

As you can see below, the company has added about $5 billion in backlog this year. It is also important to note that about $36.5 billion of the backlog is "funded" vs $47 billion being "unfunded." The Pentagon awards long-term contracts for projects, but these can be dependent on annual appropriation and authorization by Congress via spending bills. If funding levels come in lower, some projects will see cuts, and not all of this backlog will actually be realized. Conversely, backlog that has already been funded is largely immune from spending drama in DC.

{kind=link}

NOC has a mix of "short cycle" and "long cycle" businesses and products. Short cycle are items like ammunition, which tend to be delivered within a year or two. Conversely, its bomber program or rockets for space initiatives can have project lives that exceed a decade. It follows then that aeronautics and space, which house these longer cycle projects, have much more of their budget unfunded than defense and mission systems.

That does make their backlogs somewhat less certain, but with space in particular being a key long-term strategic priority, I would expect over time for this backlog to move from unfunded to funded and be realized. Space has been NOC's high-growth business, growing about 17% annually over the past five years. Just given its higher revenue base, we are likely to see future growth rates slow, though they should stay faster than overall company revenue growth.

This takes me to the outlook, as well as my concerns. Northrop reaffirmed its 2024 outlook for $2.25-$2.65 billion in free cash flow alongside " rapid " free cash flow growth the next five years as sales rise 4-5%. Free cash flow is aided by the fact that cap-ex begins to decline in 2025. Additionally, free cash flow was negatively impacted in 2022 and 2023 by the fact that the 2017 tax cuts allowed for the expensing for R&D spending for five years. When this expired and congress failed to extend it, companies had to start capitalizing R&D. This ended up costing NOC $700 million in 2022.

R&D is now capitalized over five years for taxes. Because all R&D before 2022 was expensed, it essentially only deducted 20% of its R&D for taxes last year. In 2023, it will deduct 20% of 2022 as well as 20% of 2023 R&D, essentially giving 40% coverage of its R&D spending. As such, the tax bite is just $550 million this year. Essentially after five years, the net impact of the tax change will be under $100 million. This continued annual improvement provides about 6-7% free cash flow growth by itself, which is a reason NOC becomes much more cash flow generative.

With that cash, NOC is aggressively returning capital to shareholders. It is on target for $1.5 billion in buybacks this year, and it pays a 1.6% dividend. Thanks to its buyback, its share count is down about 2.3% from last year. Management expects to return at least 100% of free cash flow to investors in 2024, as recently discussed at a conference .

My concern is that this 2024 guidance assumes a defense budget is passed with budget growth similar to President Biden's proposal. Now, this year's debt ceiling deal capped Pentagon spending at up 3.3% or $886 billion for fiscal 2024. That is fairly consistent with NOC's expectations. Unfortunately, defense spending bill has not been passed yet; instead, we continue to operate under a continuing resolution, which expires week. Moreover, if congress cannot pass spending bills, there will be an automatic 1% cut next year.

We have learned that House Speaker Mike Johnson is proposing a " laddered " continuing resolution that would fund the government at current levels with some agencies facing a January 19 deadline while the Defense Department and others face a Feb 2 deadline. While better than a 1% cut, this is below the 3% growth hoped for. Now, if congress can pass this and then pass a defense spending bill early next year, there should be enough time to catch-up lost spending and deliver on its revenue growth targets.

As we have seen though, Congress does not always act predictably, and with the US government accounting for 85% of Northrop's business, it is ultimately subject to political risk. Essentially, NOC is expecting its revenue growth to run faster than its assumed Pentagon budget by 1-2%. Now given its funded backlog, if Pentagon spending undershoots targets because a CR remains in place for longer, and worse case for an entire year, its revenue should hold in better but also come in below that 4-5% target.

This is partly because the CR as proposed provides no funding for Ukraine or Israel. It is extremely uncertain how much aid Congress will provide to either country. Particularly for Ukraine, it seems appetite to provide funding as past levels has declined among Republicans. As such, supplemental spending beyond the Pentagon's regular budget is likely to fall, which may reduce growth in NOC's defense systems business. Ultimately, it does seem that some spending is likely to get passed, in my view given there is still bipartisan support, but it is proving to be more difficult than I expected last year.

In a full-year CR with only aid for Israel scenario, I would expect NOC revenue growth to be halved to about 2%. This would bring free cash flow down to $2.1-$2.5 billion, still higher than this year by about 15%, aided in part by the tax tailwind discussed earlier.

We have seen shares retrace some of their rally after the Israeli-Gaza conflict began in part because I think investors are recognizing that it is more difficult to add defense spending than anticipated. In the medium term, I do think a more dangerous world supports ongoing defense spending growth, but the near-term trajectory is less favorable than anticipated. Of course if spending deals are passed that include supplemental spending, some of these headwinds would moderate. Assuming results come in toward the lower end of guidance, to reflect the risk of CRs, NOC has a ~21x forward multiple and a 3.4% free cash flow yield. Further multiple expansion seems unlikely given the more muted backdrop in my view. Still over the next year, as it reduces its share count by ~2%, pays 1.6% in dividends, and as its space programs become increasingly funded, I think there is modest upside, particularly as free cash flow growth will outpace earnings growth. With about 5-8% medium term free cash flow alongside a starting a free cash flow yield of 3.4%, NOC can generate returns over time of around 10%. As such, I would stay long shares while recognizing near-term risk likely limit upside to about $480.

For further details see:

Northrop Grumman: Near-Term Risks But Long-Term Growth