NOC - Northrop Grumman Overvalued Stock Crashed: What's Next?

2023-05-06 06:00:00 ET

Summary

- War premiums drove stock prices high, too high.

- Northrop Grumman was overvalued at previous prices.

- Its business is attractive for the long term, but the extremely high stock prices included an unjustifiable premium.

(This report was issued to members of The Aerospace Forum on May 3rd, including a valuation model. All data herein is from that date or prior).

Northrop Grumman (NOC) stock lost 15% since the last time I covered the stock. In this report, I will be looking at the reasons for the stock prices plunging and provide an analysis of the first quarter results accompanied with a price target.

Reason #1 For The Stock Crash: Politics, Politics, Politics

Northrop Grumman stock is currently trading 18% off its highs with geopolitical tension with China as well as the war in Europe. It almost seems like a no-brainer that defense budgets and equipment sales have to expand. That is not so much to actually use the equipment in war fighting situations but more so for power projection to back up your words. Compare it to having a fancy car in your garage that you don't drive but do show to everyone. Advanced weapon systems are similar to that.

While the need for higher defense budget seems to be clear, it became a political playball as Kevin McCarthy considered cutting the Defense budget by $75 billion in an attempt to gather votes to become the Speaker of the House of Representatives. Looking at the geopolitical landscape, one can only conclude that politics and decision making don't go well together when votes need to be won.

Reason #2: Everything Becomes A Reason To Sell

From January 2022 through December 2022, on the back of the war in Ukraine, Northrop Grumman stock gained 41% and I think the reality is that once a stock has such a strong run up, it becomes harder to make investors extremely confident about further upside and everything becomes a reason to sell as the focus shifts from further upside identification to profit taking and even though Northrop Grumman CFO David Keffer mentioned that a loss is possible but not probable for the low-rate initial production phase of the B-21 program it still triggered a downgrade from Cowen.

A Look At The Q1 2023 Results: Space Growth

{kind=link}

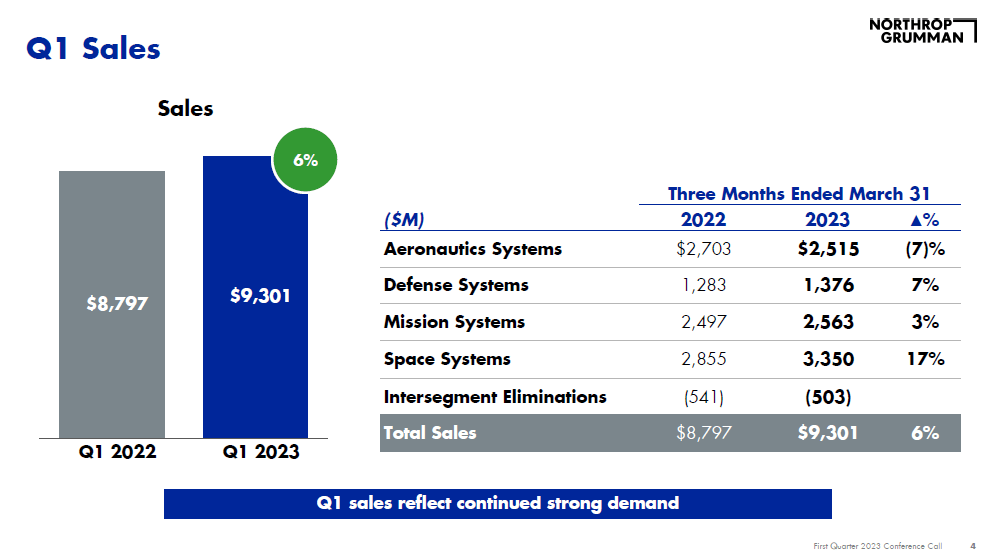

The first quarter results showed that overall sales were up 6 but with variance in year-over-year changes between the segments. Aeronautics Systems sales were down 7% driven by timing. Defense Systems sales grew by 7% reflecting strong interest in Missile systems while the growth in Mission Systems was more modest at 3%, reflecting higher sales in all its business segments partially offset by lower radar and airborne radar programs. Space was the big grower with a 17%. With the acquisition of Orbital ATK years ago and the demand for space-based global security solutions, commercial satellites and space travel increasing Northrop Grumman is positioned well to benefit. During the quarter, the Ground Based Strategic Deterrent accounted for a third of the revenue growth, while the program also benefited from higher interceptor volumes.

{kind=link}

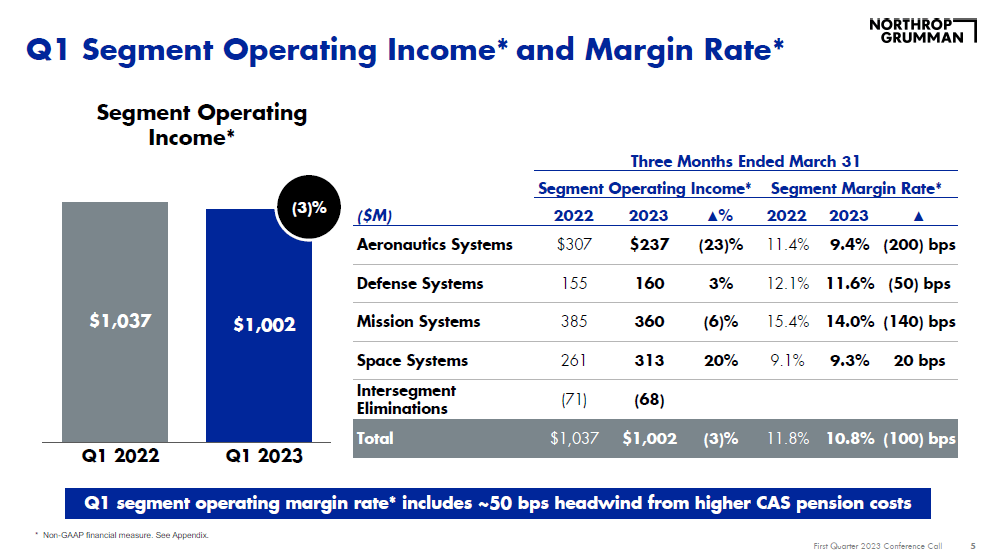

Aeronautics operating income declined by 23% or $70 million, which was a rather big drop, but it should be noted that last year there was a positive catch up adjustment to the B-21 program in the amount of $67 million. Excluding that adjustment, we would have seen the business generating similar profits on lower revenues. Similarly, Defense System margins dropped due to lower catch-up adjustments in Battle Management & Missile Systems.

Mission Systems income declined by 6%, driven by a joint-venture loss recognition and less favorable contract mix while Space Systems income increased 20%, driven by volume and a high margin license sale.

Overall, the first quarter results exceeded analyst expectations by $115.64 million and by $0.41 per share on earnings level. It was, however, pointed out that $0.30 in earnings per share tailwind was more timing-related meaning that it will even out over the remainder of the year. Nevertheless, we saw some solid performance partially diluted by lower catch-up adjustments and the only soft performer during the quarter was Aeronautics.

{kind=link}

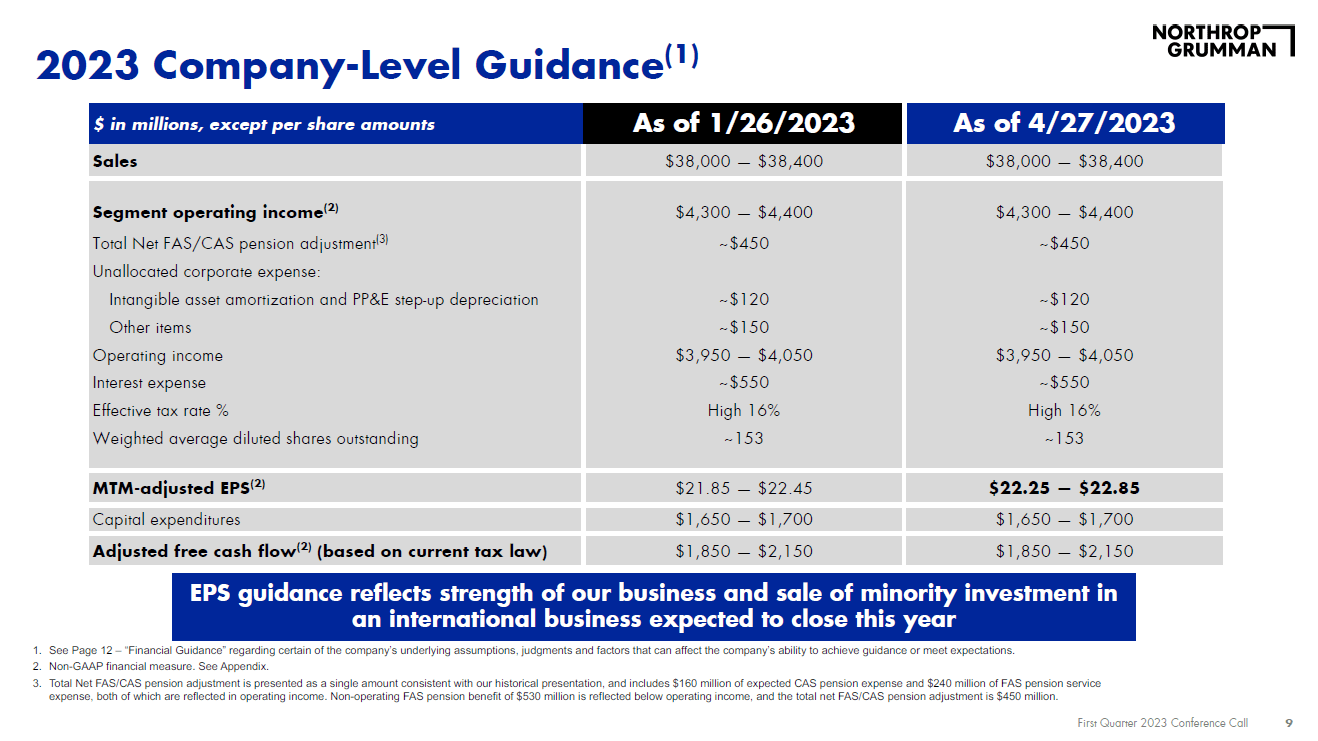

For the full year, Northrop Grumman continues to expect $38 billion in sales up around 4% year-over-year and slightly lower growth on its segment profits. The free cash flow is expected to be $2 billion at the midpoint reflecting higher capital expenditures and R&D cash taxes paid due to new regulations requiring R&D expenses that could previously be deducted when incurred are now given five-year deduction period. The only thing that has changed in the company's outlook is a $0.40 increase in adjusted EPS reflecting the sale of a company.

Conclusion: Northrop Grumman Is A Solid Hold And Opportunistic Buy

Northrop Grumman has a lot going that could improve results going forward. The positive defense budget environment is the driving power but beyond that Northrop Grumman is positioned well with hypersonics and interceptor expansion and global space-based security solutions. For the longer term, that is an attractive part of the business. While I remain bullish on the prospects, from valuation perspective, with 2023 earnings in mind, the company is fairly valued compared to peers and has less than 10% upside with 2024 earnings in mind.

Does this mean, I am rating the stock a Hold? Yes. While the stock offers little to no upside, meaning there is no reason to buy for its current year results, I do think that the company is positioned so well that unless there are big shocks to the market there won't be any major undervaluation to capitalize on. Northrop Grumman is undervalued compared to its peers on TTM metrics and as odd as that may sound, I don't want to use that as a reason to put a buy tag for the simple reason that the previous prices of $545 per share would only have been justified for profit figures that we won't be seeing until after 2025.

Still, in case geopolitical tension intensifies… you are likely going to see defense stocks heading up. One should just be aware that this is not driven by earnings but by applying at a higher premium to the stocks in the sphere. So, I am currently putting a Hold rating on the stock as I believe that with the projected earnings previously seen, share prices are not realistic, unless there is a big sentiment change as we saw in 2022.

For further details see:

Northrop Grumman Overvalued Stock Crashed: What's Next?