NOC - Northrop Grumman: Strong Buy As It Sees A Path To Double Free Cash Flow

2023-07-28 11:40:59 ET

Summary

- Northrop Grumman faced post-earnings weakness, leading to a stock price drop, presenting a buying opportunity for long-term dividend growth investors.

- 2Q23 saw strong revenue growth and a positive outlook, driven by robust new orders, a favorable demand environment, and international expansion.

- The company is actively working on improving margins with a clear game plan, cost management programs, and a shift towards international contracts, promising long-term growth and cash flow potential.

Introduction

As most readers know, I have significant defense exposure. Roughly a fifth of my dividend growth portfolio is invested in four defense giants. One of them is Northrop Grumman ( NOC ) .

Unfortunately, this earnings season hasn't been kind to investors in this industry. While quarterly numbers were often good, most defense giants sold off after earnings, as the market disliked certain developments in profitability or, in the case of RTX Corporation ( RTX ), the news regarding material engine issues.

Northrop Grumman is one of these victims. The stock briefly sold off more than 5% after its just-released earnings. The stock price is now hovering close to the lowest levels since early 2022.

That's bad news for everyone relying on quick capital gains. It's good news for long-term dividend growth investors.

The company is doing well. Sales are improving, new orders are extremely strong, and further fueled by a very supportive demand environment.

As a result, the company was able to increase full-year guidance and explain that it sees a path to double its free cash flow over the next five years.

The problem is that operating income guidance wasn't hiked as ongoing cost and operating headwinds keep a lid on margins.

As annoying as that may be (it annoys me), the company is actively working on improving margins, as it has a clear game plan and macroeconomic tailwinds that could fuel mid-term results.

Hence, in this article, I'll explain why I just used post-earnings weakness to add to my NOC position.

I'll also explain why I'm even more bullish than I was when I wrote my most recent article roughly two months ago. Especially with regard to the demand and margin picture, we're dealing with new opportunities and important developments that deserve some attention.

So, let's get to it!

2Q23 Was A More-Than-Decent Quarter

As usual, let's start with the numbers that hit the wires first.

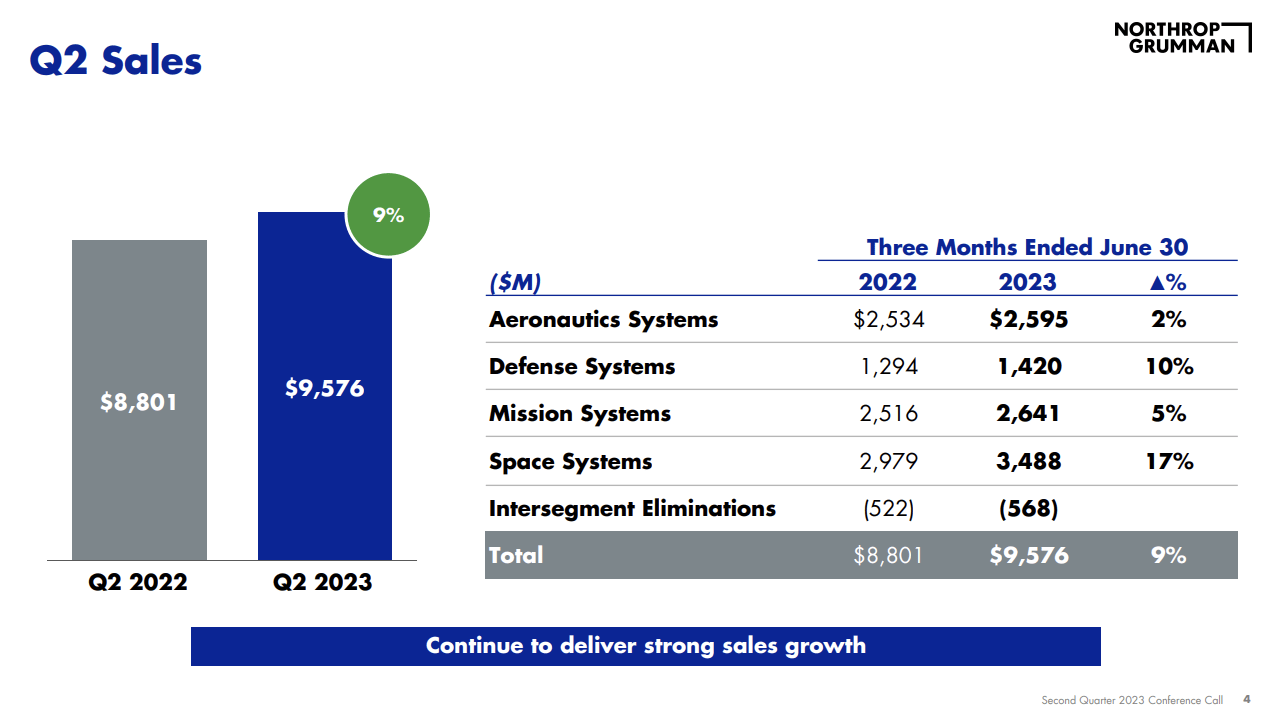

In 2Q23, Northrop generated $9.58 billion in revenue, which was 8.9% higher compared to the prior-year quarter and $240 million higher than expected.

The chart below shows that the company boosted revenues in all of its segments.

{kind=link}

Furthermore, the Virginia-based company generated $5.34 in GAAP EPS, which was in line with expectations.

According to Northrop, its ability to hire and retain talent, coupled with improving supplier deliveries, played a crucial role in improving its topline.

As the chart above shows, all four business segments saw growth in the second quarter, with Space leading the way with 17% sales growth for the second consecutive quarter, supported by GBSD, NGI, and restricted space programs.

Defense Systems saw a 10% increase in sales, driven by armaments and Missile Defense franchises.

Mission Systems experienced 5% growth due to restricted programs in the networked information solutions business, while aeronautics systems returned to growth, outpacing headwinds from legacy programs.

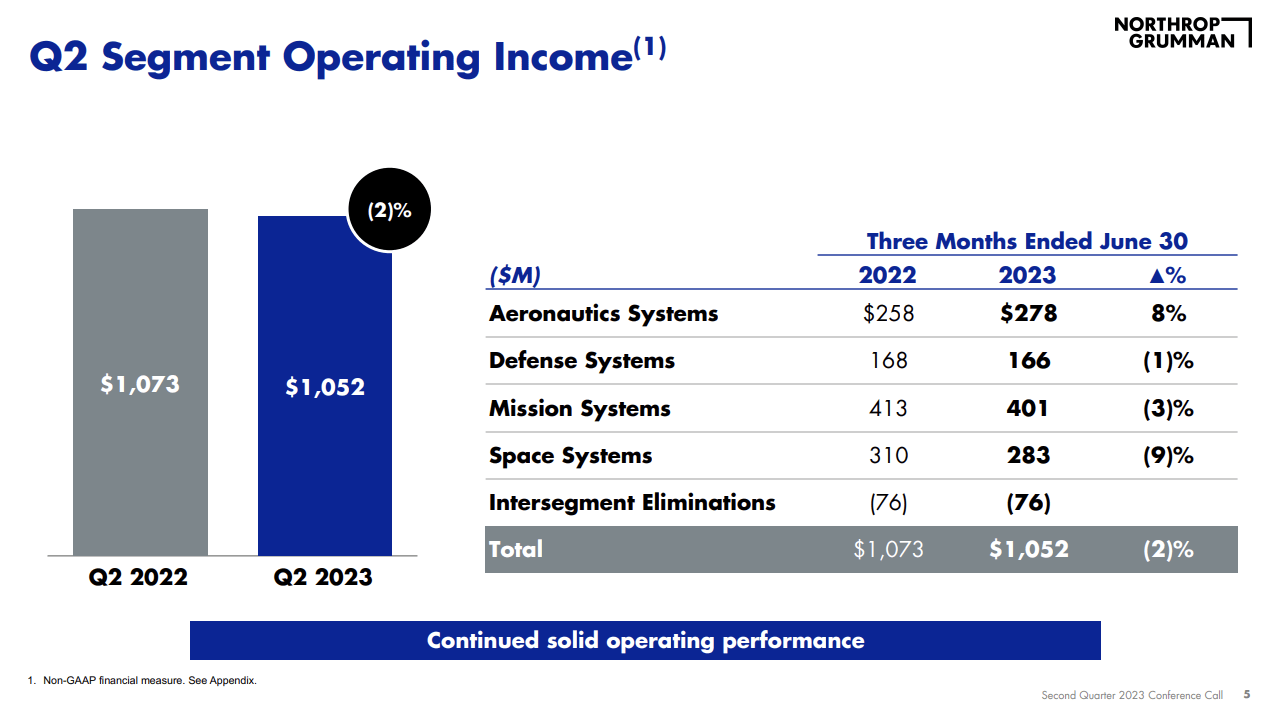

Unfortunately, higher sales did not lead to higher operating income. The company saw lower operating income in three of its four operating segments, with a 9% decline in Space Systems. This led to a 2% decline in total operating income with an 11% operating margin.

{kind=link}

This is what the company said with regard to the decline in operating income and profitability in the second quarter (emphasis added):

Keep in mind that Q2 of last year included over $70 million or 80 basis points of benefit from a land sale and a contract related legal matter.

Most importantly, margin dollars improved incrementally from Q1 , largely meeting our expectations. Program performance remains strong across the portfolio, as the team does a good job in navigating the lingering disruption from the pandemic and macro-economic factors we've been discussing . One area of pressure we experienced in the quarter was a $36 million unfavorable adjustment on NASA's habitation and logistics outposts program or HALO in our space system sector.

Since 2020, defense contractors have been struggling with subdued margins. The good news is that demand has improved, which was also an issue during the first two years after the start of the pandemic.

If margins improve, stocks like NOC turn into cash cows with high growth, which brings me to the next part of this article.

The Future Looks Bright

NOC's guidance is more important than anything else. After all, it includes demand developments, its view on margins, and so much more.

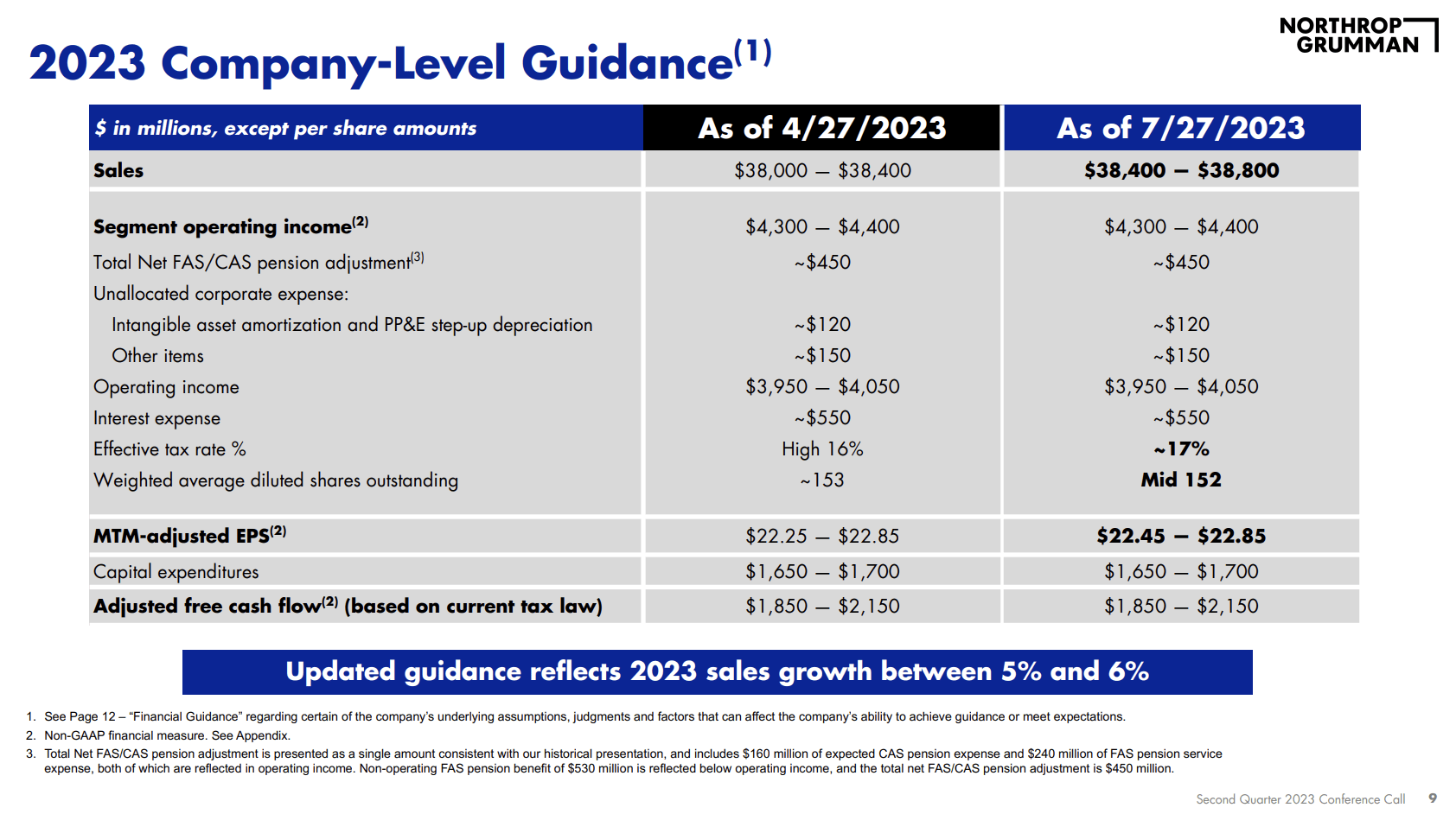

Having said that, based on the year-to-date sales increase of 7% and a positive outlook, the company announced an increase in the full year's sales guidance range by $400 million.

{kind=link}

Moreover, the award volume during the quarter was strong, resulting in a book-to-bill ratio of 1.14. This means the company gets $1.14 in new orders for every $1.00 in finished products.

As a result, the company increased its full-year book-to-bill projection to approximately 1.0.

The company's robust $79 billion backlog, which is more than two times the expected 2023 sales, further supports its long-term growth outlook.

With regard to the favorable demand environment, during the 2Q23 earnings call, Northrop Grumman expressed optimism about the budget environment in the United States, citing continued bipartisan support for national security funding to implement the administration's national defense strategy.

This is no surprise, especially in light of global geopolitical tensions that include the ongoing war in Ukraine. The just-released article below is a good example of higher spending goals and the need for higher production capacities.

{kind=link}

On Thursday, Republicans on the Senate Appropriations Committee joined Democrats in pushing a plan to increase defense spending beyond the negotiated cap, advancing an $832 billion Pentagon spending bill that includes an extra $8 billion in emergency funds.

[...] Additionally, the bill provides multiyear funding for all seven critical munitions categories that the Pentagon requested. Nonetheless, the bill report notes the Pentagon “is requesting funding to increase production capacity well above what is required by the proposed multi-year contract without firm private sector co-investment commitments.”

[...] Republican appropriators did not provide multiyear funding for the Standard Missile-6 nor the Advanced Medium-Range Air-to-Air Missile amid concerns about industry’s ability to produce the number of munitions the Pentagon seeks to procure with multiyear funds.

Furthermore, the FY2024 budget and recent congressional committee bill prioritize modernization efforts, benefiting areas where Northrop Grumman has a strong portfolio, such as the triad, space domain, information superiority, and advanced weapons.

Additionally, the company foresees continued support for Ukraine, leading to further increased demand.

Global demand for their products is also on the rise as allies increase their defense spending to address evolving threats.

According to Northrop Grumman, its positioning in multiple markets with programs like AARGM (air-to-ground missiles), IBCS (battle command systems), E2-D (surveillance airplanes), and munitions positions them to meet this growing demand.

Margins Could Soon Turn Into A Tailwind

With that in mind, the company did not hike operating income guidance, which remained unchanged with a $4.0 to $4.1 billion range.

I believe that this bothered investors, as it means that 2023 could yet be another year where strong sales growth doesn't lead to better-than-expected operating income.

After having witnessed poor margins for almost three consecutive years, I absolutely agree with investors that this is annoying.

However, things are improving.

During the 2Q23 earnings call, Northrop Grumman outlined its path to margin expansion, an (obviously) crucial element of their earnings and cash flow growth plan.

To achieve this margin improvement, the company is focusing on three key drivers:

- First, they are working to stabilize temporal macroeconomic factors that have driven higher costs and impacted the supply chain and labor efficiency.

- Second, they are implementing cost management programs across the company to drive affordability, competitiveness, and performance.

- Third, they are anticipating a shift in their business mix towards more international and production contracts as international demand grows and current development programs mature over the next few years.

The company also expressed progress in optimizing labor efficiency, implementing innovative training programs, and standardizing work instructions to improve profitability.

While inflation has been a challenge, the company expects the impact to stabilize and has already factored higher inflation expectations into new contracts.

The company is also working to drive additional discipline in its bid approaches, especially for fixed-price contracts, to protect against future dynamics.

Especially the last part is key, as I have often made the case that even fixed-price contracts are protected against inflation, as new rewards need to take inflation into account. The biggest risk related to fixed-rate contracts is prolonged projects that do not benefit from regular inflation adjustments.

So, these developments are promising.

Adding to that, the company is scaling a digital approach across its factories to drive efficiencies. They are centralizing procurement and securely connecting suppliers into their digital ecosystem to reduce costs and improve productivity.

More Good News For Shareholders

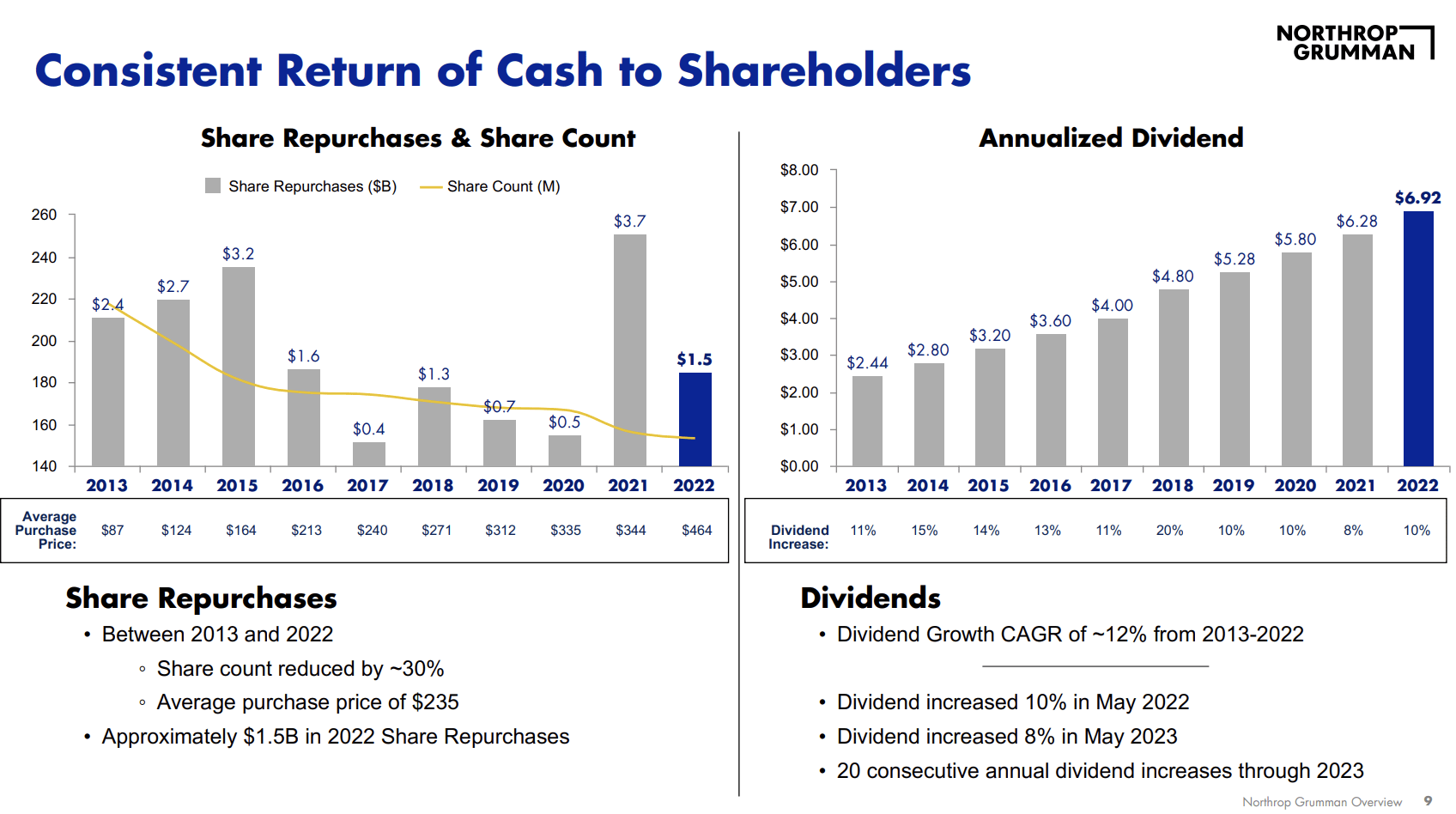

Northrop Grumman has a balanced capital deployment plan, which includes investments of over $2.8 billion in R&D and CapEx, along with returning excess capital to shareholders through quarterly dividends and share repurchase plans, which is what the company has been doing for decades.

Since 2013, the company has bought back roughly a third of its shares and hiked its dividend by 12% per year.

{kind=link}

Even better, the company aims to return over 100% of its free cash flow to shareholders this year, including approximately $1.5 billion in share repurchases.

Also, during the earnings call, plans to retire $1 billion of notes maturing in August were mentioned. The company has no additional bond maturities until 2025, which is terrific news in this high-rate environment. The company enjoys a BBB+ credit rating.

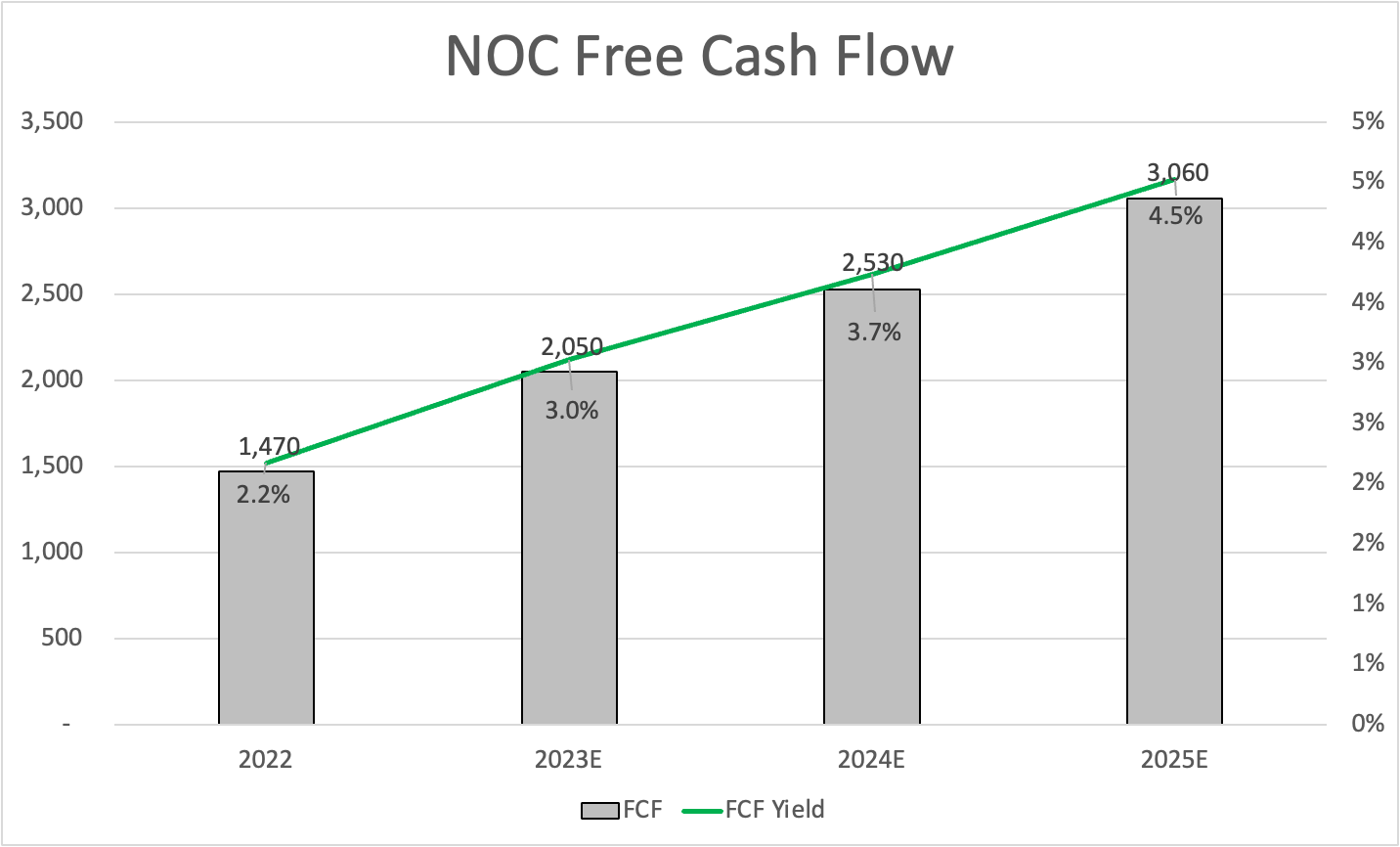

However, it gets even better than that, as the company sees the potential to double its current level of free cash flow over the next five years, which brings me to the next part of this article.

Valuation

So far, the biggest takeaways from this article - to me - is the fact that the company is stepping up its fight against low margins and its outlook to double free cash flow over the next five years.

Looking at analyst estimates below, we see that they expect the company to follow through on its promise. Over the next three years (including 2023), free cash flow is expected to rise by 28% per year, resulting in $3.1 billion in 2025E free cash flow.

{kind=link}

If we assume that growth declines to the low-double-digit range, we can assume that the company can generate more than $4.0 billion in 2028E free cash flow.

This longer-term outlook is why it is somewhat hard to put a valuation on NOC using short-term expectations. While it sounds a bit like finding an excuse to validate a poor performance, it makes sense to look further into the future.

- The demand environment is highly favorable and likely to remain that way.

- Supply chain issues were persistent and are finally starting to ease, with support from company initiatives.

- Inflation has turned out to be very sticky, which makes growing margins even harder.

Now, the company is finally in a situation where multiple headwinds turn into tailwinds. Given the slow nature of defense giants, it will take some time until it bears fruit.

With that in mind, NOC traded at 46x free cash flow in 2022 (I left it out of the chart below as it messed up my y-axis). The company is trading at 33x 2023E free cash flow and 22x 2025E free cash flow (I skipped 2024).

The consensus price target is $510, which is 15% above the current price.

I agree with that and believe that NOC is now in a position to deliver double-digit annual total returns on a prolonged basis.

This includes my expectation that NOC will outperform the market again, as it has failed to beat the market over the past five years - prior to that, it beat the market by a wide margin.

Hence, I used the post-earnings dip to add to my position. I have now added to RTX, L3Harris Technologies ( LHX ), and Northrop this week, which is not what I expected to do going into this week.

However, I believe that these opportunities are too good to ignore, especially for a dividend growth investor like myself who likes to buy high-quality companies at good prices.

Takeaway

Despite the recent post-earnings dip and ongoing margin challenges, Northrop Grumman presents a promising opportunity for long-term dividend growth investors.

The company's sales are improving, fueled by strong demand and a robust backlog. While margins have been a concern, NOC is actively working to stabilize costs and implement cost management programs.

The positive outlook, driven by favorable demand and international growth, indicates the potential for aggressive future cash flow expansion. With a balanced capital deployment plan and a track record of returning excess capital to shareholders, NOC remains an attractive prospect for investors seeking potential double-digit annual total returns.

As a dividend growth investor, I have taken advantage of the post-earnings weakness to add to my NOC position, confident in its potential for long-term success in the defense industry.

For further details see:

Northrop Grumman: Strong Buy As It Sees A Path To Double Free Cash Flow