NOC - Northrop Grumman - Why I Remain So Very Bullish

2023-12-16 23:07:24 ET

Summary

- S&P 500 rose 2.1% fueled by Federal Reserve's comments on rate cuts, but Northrop Grumman shares fell 3.2%.

- Northrop Grumman received two major downgrades due to potential headwinds in its major programs.

- Despite challenges, Northrop Grumman maintains strong financials, an international growth strategy, and a commitment to shareholders through dividends and buybacks.

Introduction

What a week it has been!

The S&P 500 rose 2.1%, fueled by the Federal Reserve's comments that it may start cutting rates this year. This fueled a lot of beaten-down investments, including real estate investment trusts ( VNQ ) that returned 6.1%, dividend stocks ( SCHD ) that returned 4.1%, and tech stocks ( QQQ ) that returned 3.4%.

Unfortunately, one of my top holdings completely ignored the rally, as shares of Northrop Grumman ( NOC ) , one of the nation's largest defense contractors, fell by 3.2%, underperforming the market by more than 5%.

On October 12, I wrote an article titled I Just Made Northrop Grumman My Second-Largest Investment . In that article, I highlighted the company's ability to consistently grow shareholder distributions, ongoing tailwinds, including the war in Gaza, and its attractive valuation.

In this article, I'll go a step further, as a few important developments have given me enough reasons to take a closer look at the risk/reward of this company.

For example, the poor performance this week was caused by two major downgrades from sell-side analysts fearing that some of the company's major programs could turn into headwinds.

On top of that, the company presented at the Baird Global Industrial Conference, which gave us a lot of valuable intel.

Now, before I continue, bear in mind that this isn't a damage control article. Despite the fact that I have more than 25% defense exposure, I'm ready to sell any investment the moment I feel the risk/reward is turning against me.

The good news is that I continue to see tremendous value in NOC. While it may not be as cheap as my favorite plays, L3Harris Technologies ( LHX ) and RTX Corp. ( RTX ), the company is one of the most consistent performers among dividend growth stocks and in a great position to continue outperformance, even if it comes with some bumps in the road.

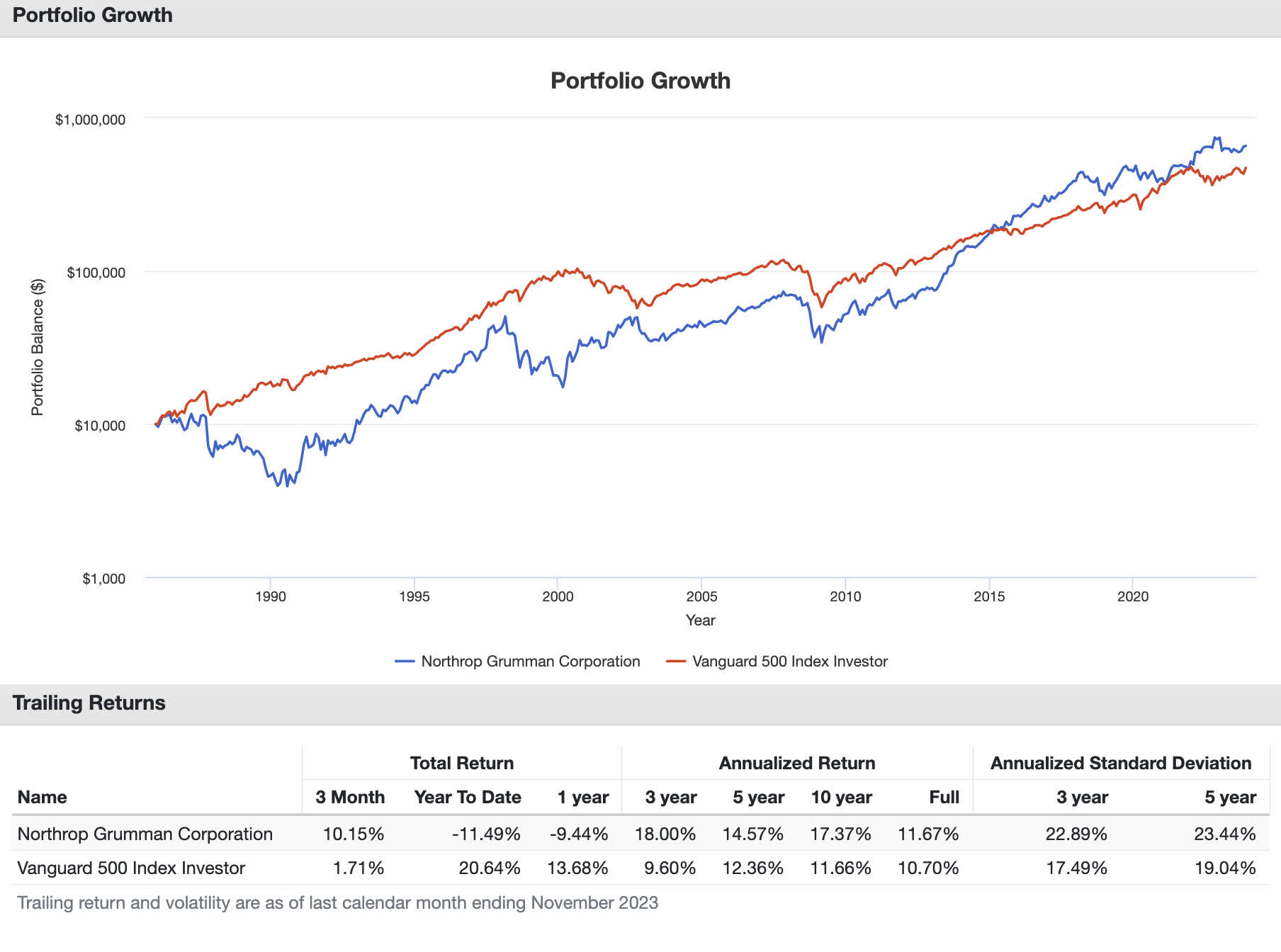

- Over the past ten, five, three, and one-year intervals, NOC shares have outperformed the S&P 500 by a wide margin despite budget uncertainties, pandemic-related supply chain issues, elevated inflation, and related issues.

- The company has beaten the market with a highly favorable standard deviation, making NOC a great pick for conservative investors.

{kind=link}

Portfolio Visualizer

With all of this being said, let's dive into the details!

Two Major Downgrades

Usually, I never address analysts who disagree with me, as I don't want to turn investments into a battle of who's right. People have different strategies, time horizons, and views on certain investments.

However, when it comes to major sell-side banks, I discuss what they have to say. After all, unlike my articles, the opinions of large banks and institutions move stock prices, as we found out last week.

One of the downgrades came from Deutsche Bank ( DB ), which downgraded Northrop Grumman to Hold , lowering the price target from $541 to $473.

Reasons are expected headwinds in two major programs: its new stealth bomber and the nuclear missile program.

As reported by Seeking Alpha :

They said the aerospace and defense company faces mounting costs for the LGM-35A Sentinel program , a modernized intercontinental ballistic missile system that’s intended to replace the aging LGM-30G Minuteman III land-based nuclear missile.

The B-21 Raider stealth bomber also may be profitless for Northrop , according to Deutsche Bank. The bank cut its price target on Northrop to $473 a share from $541 a share previously.

Wolfe Research also downgraded the defense giant to a price target of $450. Unfortunately, on this decision, public information is very limited, although I assume that its reasoning will be very similar to what Deutsche Bank wrote.

Strength Despite Challenges

Generally speaking, any comments regarding cost headwinds tend to hit a nerve in this industry.

After the pandemic, investors have been through a lot. Defense giants were among the biggest losers of prolonged material and labor shortages.

Even the latest third quarter was a good example of this.

The third quarter wasn't bad, as the company reported robust total revenue growth, with sales increasing by 9% year-over-year in the third quarter.

This growth was reflected across all four business segments, contributing to a record backlog of $84 billion. Notably, the company's book-to-bill ratio was 1.5x, indicating a strong performance in securing new contracts.

This means that for every $1.00 in finished work, it got $1.50 in new orders.

Despite the impressive growth in total revenue, Northrop Grumman maintained its earnings guidance for the year. It hikes its full-year revenue guidance.

{kind=link}

Northrop Grumman Corp.

The good news is that things are looking up.

During the November 12 Baird Global Industrial Conference , the company commented on margins and the aforementioned Sentinel program.

With regard to margins, Northrop Grumman operates in a long-cycle business, and the company highlighted that trends around margins take more time to cycle through in their business compared to shorter-cycle industries.

Essentially, three primary factors will contribute to higher margins over the next few years:

-

Normalization of Macro-Economic Pressures: As older contracts with certain macroeconomic pressures gradually cycle out, there is an opportunity for the normalization of margin pressures.

-

Cost Efficiencies: The company is actively pursuing cost efficiencies across its portfolio. This includes examining supply chain costs, optimizing the real estate portfolio, and implementing digital technologies for operational efficiency.

-

Business Mix Improvement: the company emphasized the importance of the business mix, indicating a shift from cost-type contracts to fixed-price contracts. This shift is expected to occur as programs move from development to production phases, providing more margin opportunities. In 2022, roughly half of its contracts are fixed-price contracts.

{kind=link}

Northrop Grumman Corp.

This also includes the fact that the company withdrew its bid for the Next Generation Air Dominance sixth-gen fighter earlier this year .

It will likely be a secondary partner, which is a decision I support. Note that the company is already a secondary supporter of a wide range of programs, including the F-35, for which it produces fuselages - among a wide range of other products and services.

Working our way to the Sentinel program, the Space business, which has been a significant driver of growth, is expected to undergo a business mix transition.

While it has seen incredible growth in recent years, the company mentioned that the growth rate in the Space business is likely to moderate in 2024.

However, opportunities for growth still exist, particularly in areas such as launch support for projects like the Amazon Kuiper Constellation and the Space Development Agency's Tranche 2.

In 3Q23, Space sales rose by 8% to more than $310 million. A slowdown in this business is likely, as it is a fast-growing emerging market that is maturing. I'm not worried about that.

Going into this year, the Space segment had a backlog of almost $40 billion. More than 70% of its contracts are cost-type contracts, which is beneficial in times of elevated inflation.

{kind=link}

Northrop Grumman Corp.

With that said, the Sentinel program (LGM-35A) is a critical modernization of the ground-based leg of the strategic nuclear triad.

The Sentinel, which is a Ground Based Strategic Deterrent ("GBSD"), replaces the Minuteman III intercontinental ballistic missile system. This system has been in service for more than 50 years.

According to the company, this program, unlike some other programs, operates under a different contract structure.

The engineering and manufacturing Development phase of the contract is cost-plus, while the LRIP (low-rate initial production) and full-rate production phases have yet to be priced.

The LRIP phase of the Sentinel program is currently cost-plus. Negotiations with the customer are ongoing, and the company plans to update projections on the program's phases in each successive quarter.

In 2020, Northrop got $13.3 billion to develop the program. The entire program is expected to cost $100 billion, making it one of the most expensive defense programs ever.

{kind=link}

Northrop Grumman Corp.

While it needs to be seen if Deutsche Bank's fears are reasonable, it is hard to disagree with the fact that even Northrop is nervous about potential cost increases.

According to Defense News :

Kendall said “unknown unknowns” are surfacing that the department will have to work through, including factors related to command-and-control infrastructure, such as the complexes that missileers would use to launch the Sentinel.

Kendall said some costs may rise in the process.

“As we get more into the program, as we understand more deeply what we’re actually going to have to do, we’re finding some things that are going to cost money,” Kendall said. “We’re trying to assess how much of an impact that’s going to have and what kind of adjustments we’re going to have to make because of it.”

The good news is that the company is actively working on price adjustments.

To me, the biggest risk seems to be that the company underestimates certain costs. Other than that, I am very upbeat about the prospects of Northrop getting the resources it needs to successfully continue this major defense program.

Where's The Juicy For Shareholders?

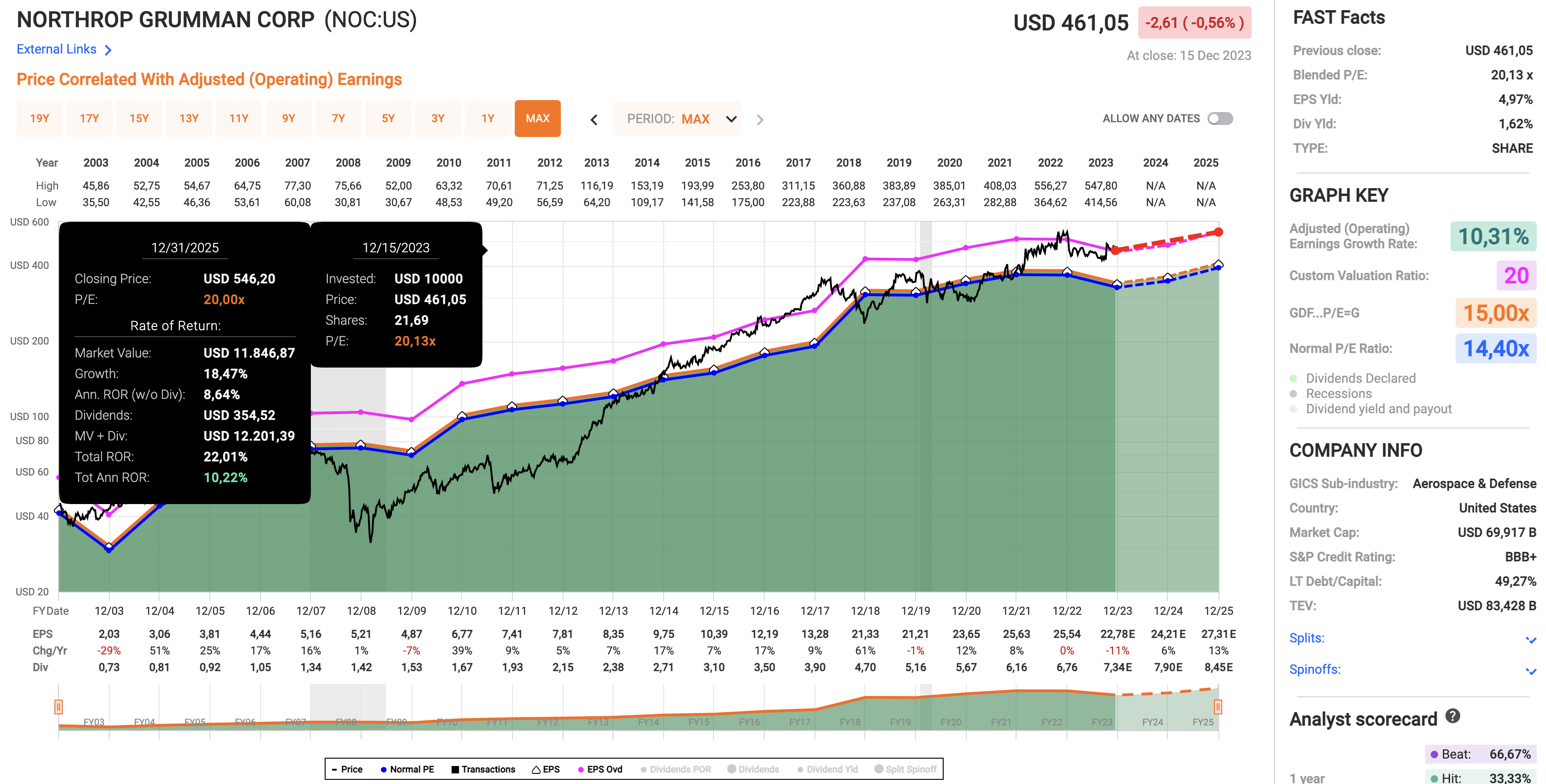

With that said, NOC has the most expensive valuation among the largest defense contractors in the U.S.

We see the same when looking at the chart below. NOC shares are currently trading at a blended P/E ratio of 20.1x (similar to the forward P/E ratio).

The normalized P/E ratio is 14.4x. This year, EPS is expected to contract by 11%, followed by 6% growth in 2024 and 13% growth in 2025.

This means that using its normalized valuation, the company has priced in the expected growth of the next two years.

The normalized valuation is displayed by the blue line in the chart below.

I also added a pink line. That line displays a 20x multiple, which would indicate a >10% annual total return through 2025 (and likely beyond).

{kind=link}

FAST Graphs

I am not doing this to cheat but because I believe that the company is in a good spot to maintain high-single-digit to low-double-digit annual EPS growth in the next few years. In that situation, a 20x multiple would be fair.

On top of having a strong backlog, a >1.0x book-to-bill ratio, and a focus on margin enhancements, the company has demonstrated resilience and growth, with an 8% year-to-date revenue increase through the first three quarters.

The company projects a 6.5% full-year growth with an initial outlook for 2024 ranging between 4% and 5%.

During the aforementioned conference, the company emphasized the stability in upticks, driven by a robust demand environment and Northrop Grumman's ability to strategically align with customer needs.

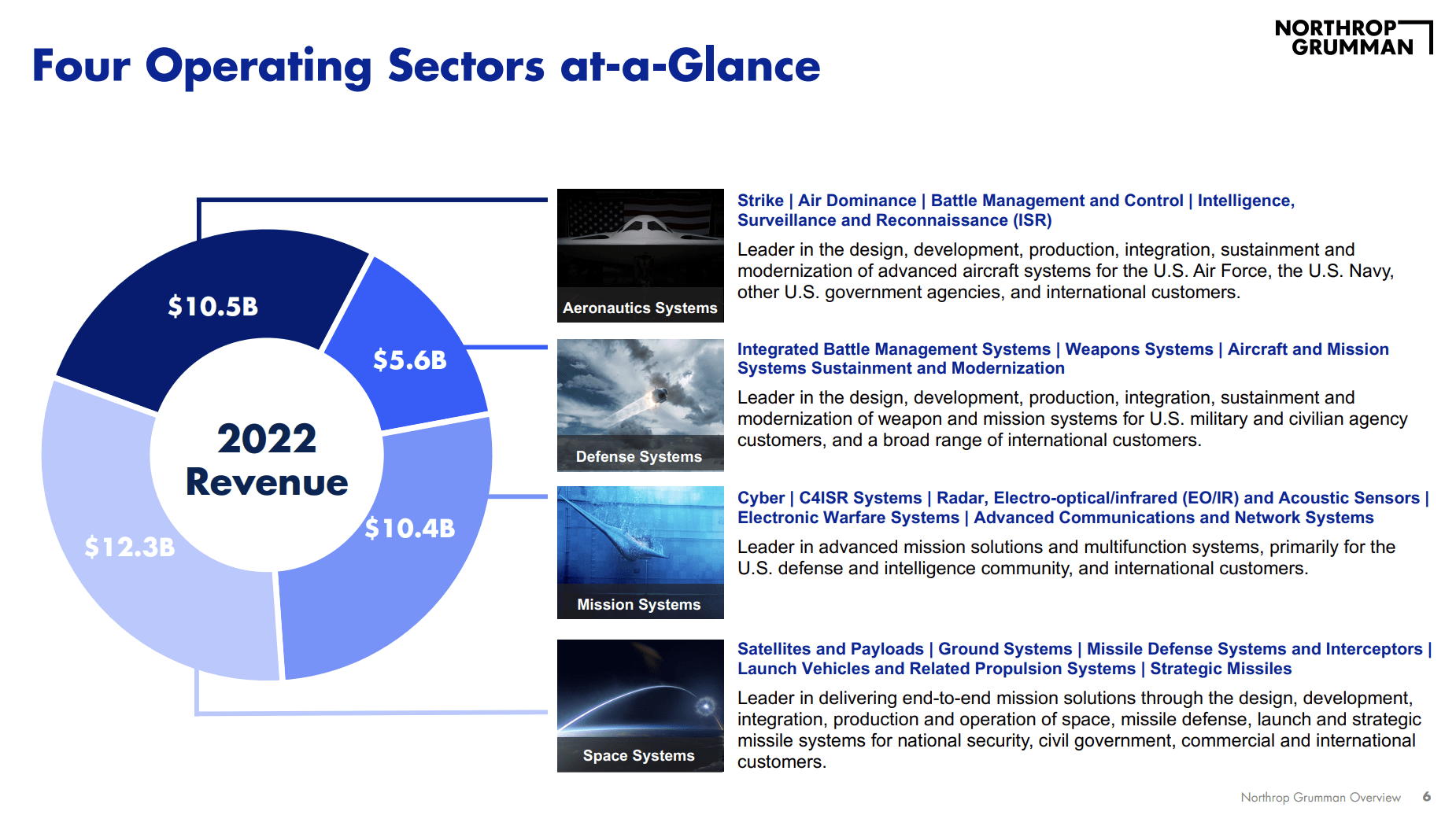

After all, it has one of the most well-diversified portfolios in the defense industry.

{kind=link}

Northrop Grumman Corp.

On top of that, Northrop Grumman's international growth strategy, aiming to increase the 15% international portfolio at a rate exceeding the company's overall growth, presents a promising outlook.

According to the company, opportunities in munitions, integrated air and missile defense, aeronautics, and mission systems contribute to a diversified international portfolio, aligning with global demand signals.

Furthermore, the company is very upbeat about free cash flow growth.

Projections indicate not only an excess of $2 billion in free cash flow for the current year but also substantial growth in the upcoming years, reaching $2.25 to $2.5 billion in 2024.

Over the next five years, the company expects to double its free cash flow, which shows how much confidence the company has in its business.

This would suggest that the company could generate close to $4.5 billion in free cash flow over the next five years. If we assume a free cash flow multiple of 20x, the company has at least 28% to 30% upside, excluding stock buybacks, which enhance the per-share value of the company.

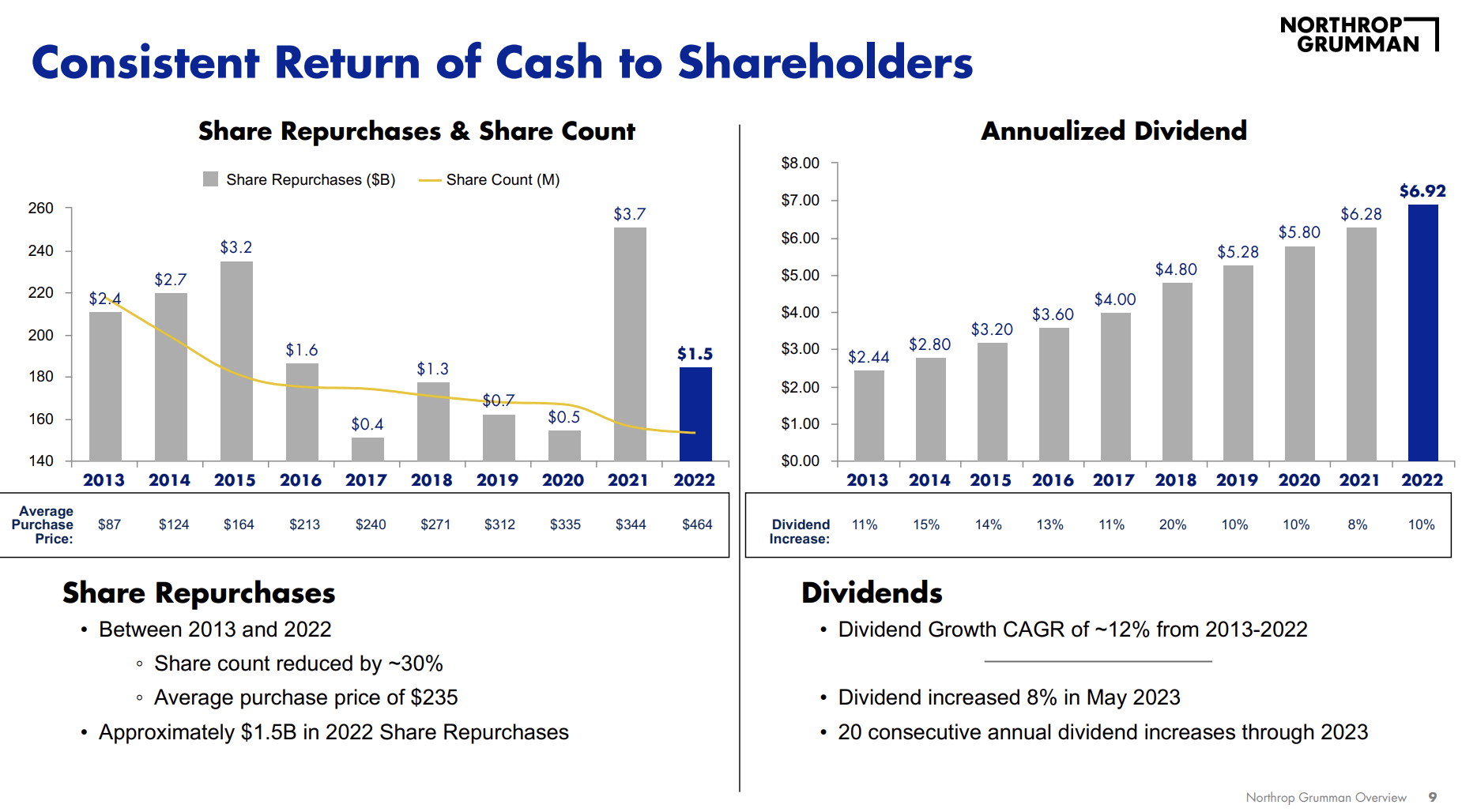

Speaking of buybacks, the company is very supportive of its shareholders.

A cornerstone of Northrop Grumman's shareholder distribution strategy is the regular increase in dividends. The company has a remarkable track record of dividend growth, having raised dividends annually for nearly two decades.

Share repurchases also play a significant role in Northrop Grumman's approach to shareholder distributions. By actively buying back its own shares, the company not only signals confidence in its valuation but also enhances shareholder value by reducing the overall share count.

- Over the past ten years, the company has bought back roughly a third of its shares.

- During this period, it has grown its dividends by 12% per year. The current yield is 1.6%, protected by a 30% payout ratio. The five-year dividend CAGR is 9.3%.

{kind=link}

Northrop Grumman Corp.

In recent years, the company has distributed all of its free cash flow to shareholders, which is expected to continue in 2024 and beyond.

Even better, if the company grows its free cash flow to $4.5 billion, it has an implied free cash flow yield of 6.4%.

This implies a future 25% cash payout ratio and a lot of room for buybacks.

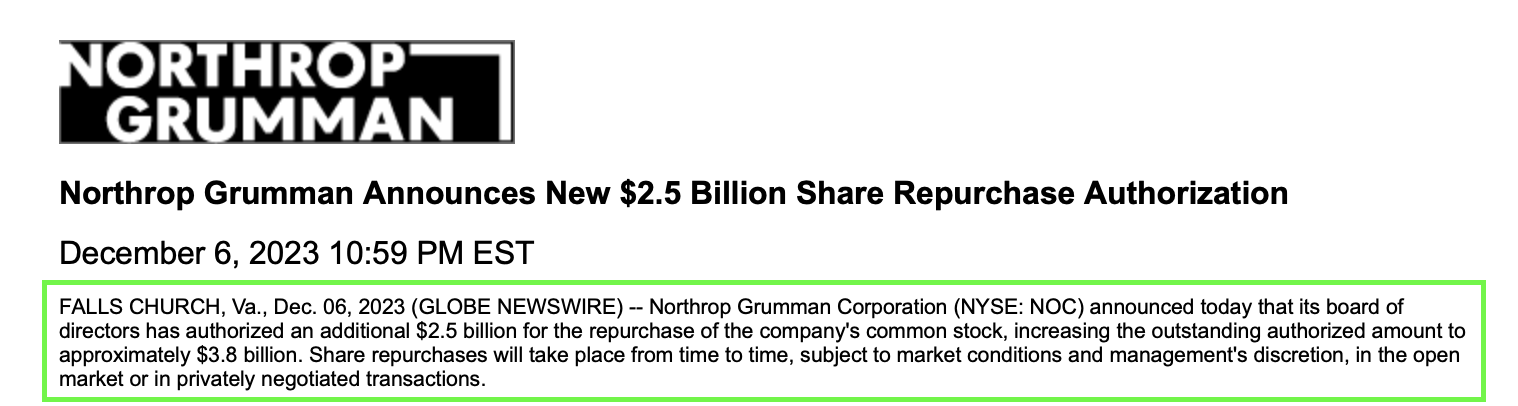

On December 6, the company boosted its buyback authorization by $2.5 billion to $3.8 billion.

{kind=link}

Northrop Grumman Corp.

In other words, despite justified concerns of elevated costs, I believe that Northrop Grumman remains in a great spot to generate tremendous long-term shareholder returns, fueled by an increasing focus on cost management, higher margins, and elevated growth in space, next-gen weapons, and international operations.

Although I am not planning on adding more NOC shares in 2024 after adding so much in 2023, I may use opportunities if the stock shows more weakness.

Takeaway

Despite major downgrades due to potential headwinds in key programs, my confidence in NOC remains strong.

While concerns about cost increases persist, the company actively addresses them.

Meanwhile, NOC's robust financials, international growth strategy, and commitment to shareholders through dividends and buybacks make it a compelling long-term investment, balancing potential risks with substantial rewards.

For further details see:

Northrop Grumman - Why I Remain So Very Bullish