NOC - Northrop Grumman: Q1 Stellar But Long Term In Doubt Due To Government Finances Deterioration

2023-04-27 15:39:14 ET

Summary

- After the launch of Russia's invasion of Ukraine over a year ago, most defense-related stocks saw a significant stock price boost, on the market's assumption that defense spending will rise.

- Northrop's stock is up about 50% compared with pre-war levels, even though its stock price saw a significant pullback recently.

- Massive street protests and strikes in Europe, and growing anxiety over seemingly out-of-control budget deficits in the US, suggest that defense spending will be cut in the long term throughout the Western alliance.

- The thesis that military spending might actually see a reduction seems counter-intuitive, given the geopolitical context, but in the longer-term bread & butter issues always win over geopolitical considerations.

- The growing rift between the US and traditional Middle East allies could also cut sales. A solid Q1 is arguably providing a selling window, rather than signaling a buying opportunity.

Investment thesis

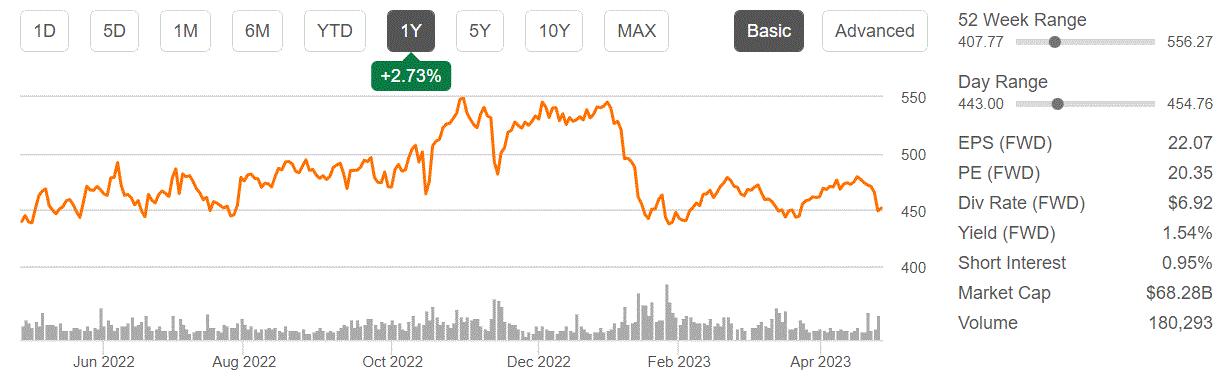

Russia's invasion of Ukraine last year provided defense stocks with a major boost to their valuations and stock prices. In effect, revenue and presumably profits growth has been baked into the outlook of most relevant Western Defense companies. Northrop Grumman ( NOC ) is no exception in this regard, with its stock price rising from just over $300/share the day before the war started, to almost $550/share by November of last year.

{kind=link}

Even though it has since retreated to well under $500/share, it still seems overvalued given longer-term fundamentals, despite what the recent Q1 numbers might suggest. Its current valuation suggests the market expects significant sales & profits growth in the coming quarters and years. A seemingly fundamental deterioration in Western fiscal positions, in my opinion, signals that budget cuts are on the way, with military spending being a far easier political target than the social safety net, despite the currently tense global geopolitical situation. If I am correct and this is set to occur in most Western countries, Northrop's outlook and financial results going forward could suffer significant setbacks.

Northrop's latest financial report and outlook

The first quarter of this year saw a beat of market expectations. Earnings per share of $5.50 was a beat of 38 cents. Revenue of $9.3 billion was higher than the market expected, beating expectations by $110 million. It should be noted however that it was about $700 million lower compared with Q4 of last year. As I shall point out, it might help to raise the expected increase in revenues for this year compared with last year, perhaps significantly, if Northrop will continue to beat expectations in the next few quarters.

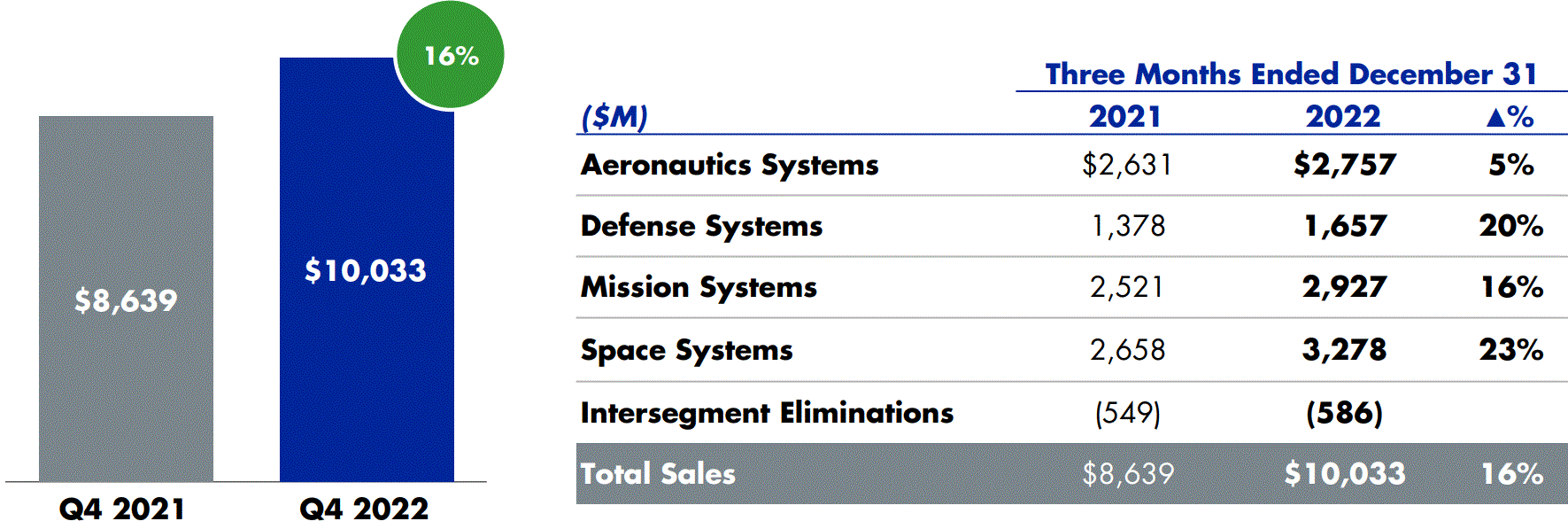

For the fourth quarter of last year, Northrop saw a significant increase in sales compared with the fourth quarter of 2021.

{kind=link}

As we can see, there was a significant increase in revenues, which arguably makes Northrop a growth stock. Looking at some factors such as its massive orders backlog of $79 billion as of the end of last year, it can arguably be assumed that the growth trajectory is set to continue for the foreseeable future. The current backlog is equivalent to about eight quarters worth of sales at current levels.

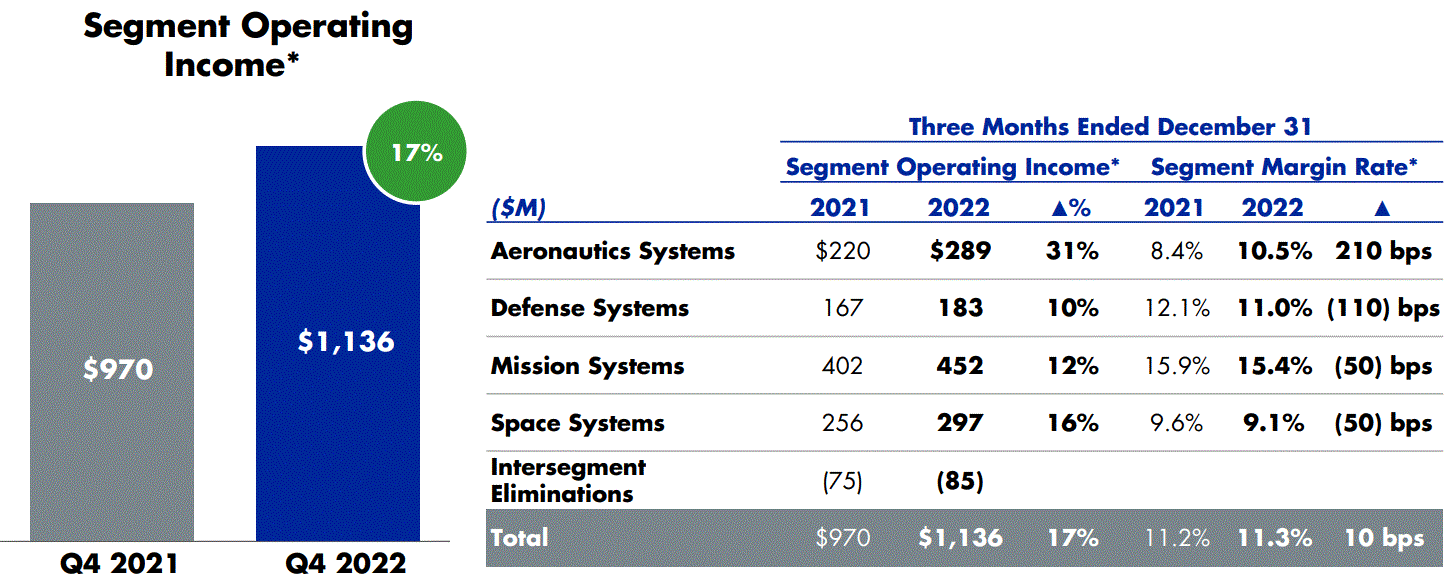

As far as the profitability of its sales, there seems to be some degree of uniformity across all its sectors in maintaining relatively healthy profit margins as well as growth in profits.

{kind=link}

It should be noted that revenue growth did not come at the expense of a loss in profit margins, since the increase was 16% & 17% respectively.

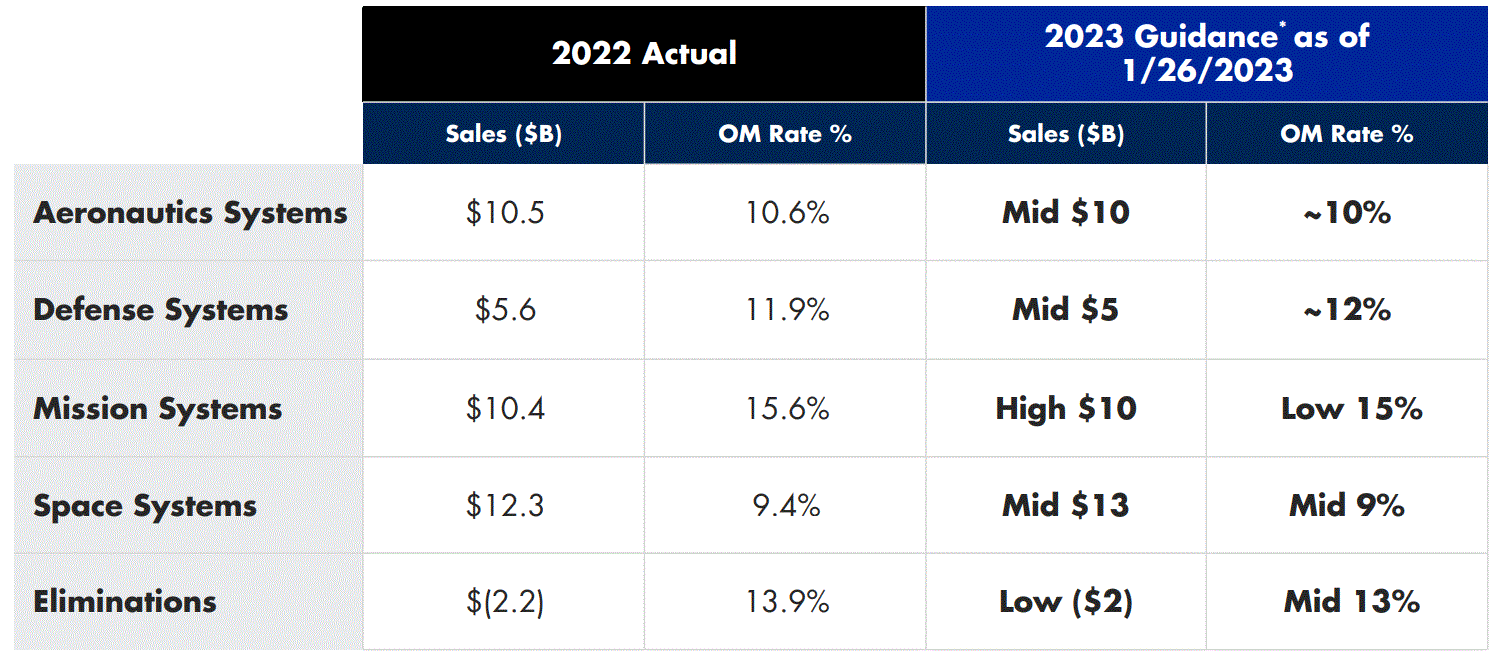

Its guidance for this year shows that revenues are expected to come in at around $38 billion, which is more or less a continuation of the sales growth trend we saw last year while operating income is expected to come in at around $4 billion, which is likewise more or less in line with the prior trend.

{kind=link}

The thing that jumps out in my view when looking at 2022 results, as well as the guidance for 2023, is that one might have expected to see a significant jump in sales this year, but it does not seem to be the case. There is growth, but it is very steady, with little evidence of a surge in demand due to the Ukraine war as well as heightened tensions with China. Q1 results might be an indication of Northrop's own estimates for 2023 perhaps being overly conservative. If it continues to beat expectations for the rest of the year, its stock could do well, even though there is in my view a high degree of risk of plummeting demand for its products beyond this year.

Northrop systems might be in high demand going forward within the context of the revival of big power competition

There is no denying the fact that Western military strategic thinking is in the course of readjusting after two decades of focusing on the war on terror, against mostly non-state actors, or semi-state actors, with many limitations in terms of the opponent's resources and capabilities. Just recently, it has been revealed that guided bomb systems provided to the Ukrainian military have been effectively countered by Russian jamming systems that throw them off course. Clearly, new capabilities are likely to be needed going forward, especially if big power competition will increasingly feature proxy conflicts, where one power will indirectly face off with a rival power by arming a proxy army with advanced capabilities.

Northrop does provide the capabilities that are potentially needed in a fight between more or less equally sophisticated opponents. Whether it will be future US military engagements, against increasingly well-armed proxies of opponents or the arming of proxies against opponent proxies it will help to have sophisticated weapons systems in the arsenal. For instance, Northrop is involved in the development of hypersonic missiles . The Ukraine conflict has highlighted among other things the need to defeat an opponent's air defense system. In the case of Russia, it is still working on taking out those air defense systems, given that Ukraine is said to have inherited one of the largest air defense capabilities arsenals in Europe, with as many as 300 S-300 launchers. By comparison, America's Patriot system launchers in service with the US military number about 1,100.

Assuming that the Ukraine proxy war will be the precedent that will shape future proxy conflicts, America's military has to be prepared to take on potentially robust air defense systems, as well as field a robust air defense system of its own meant to take on drones, missiles, opposing air power. Northrop offers air defense capabilities to would-be customers, along with an array of other potentially crucial defense products that are likely to be on the wish list of most militaries, including the domestic one.

Western budgetary constraints are set to become severe, putting military spending in doubt

Just because Western militaries and allies around the world would like to enhance their capabilities, it does not necessarily mean that it will happen. Expectations of a surge in military spending across NATO and other potential customers for Northrop products around the world seem to have become almost gospel within wider society and within the market. Fiscal realities may get in the way of expectations in this regard.

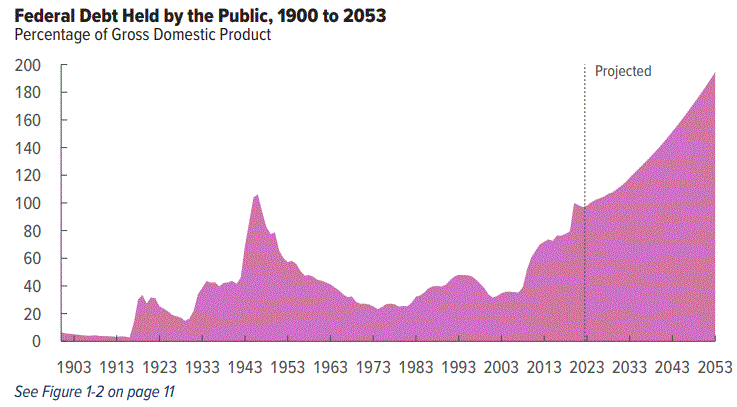

Recent data suggest that US deficits may be getting out of control, with CBO projections three decades out looking outright scary.

{kind=link}

Average yearly deficits are projected to be in the $2 trillion/year range in the coming decade, while for the current fiscal year, we are looking at a $1.4 trillion shortfall.

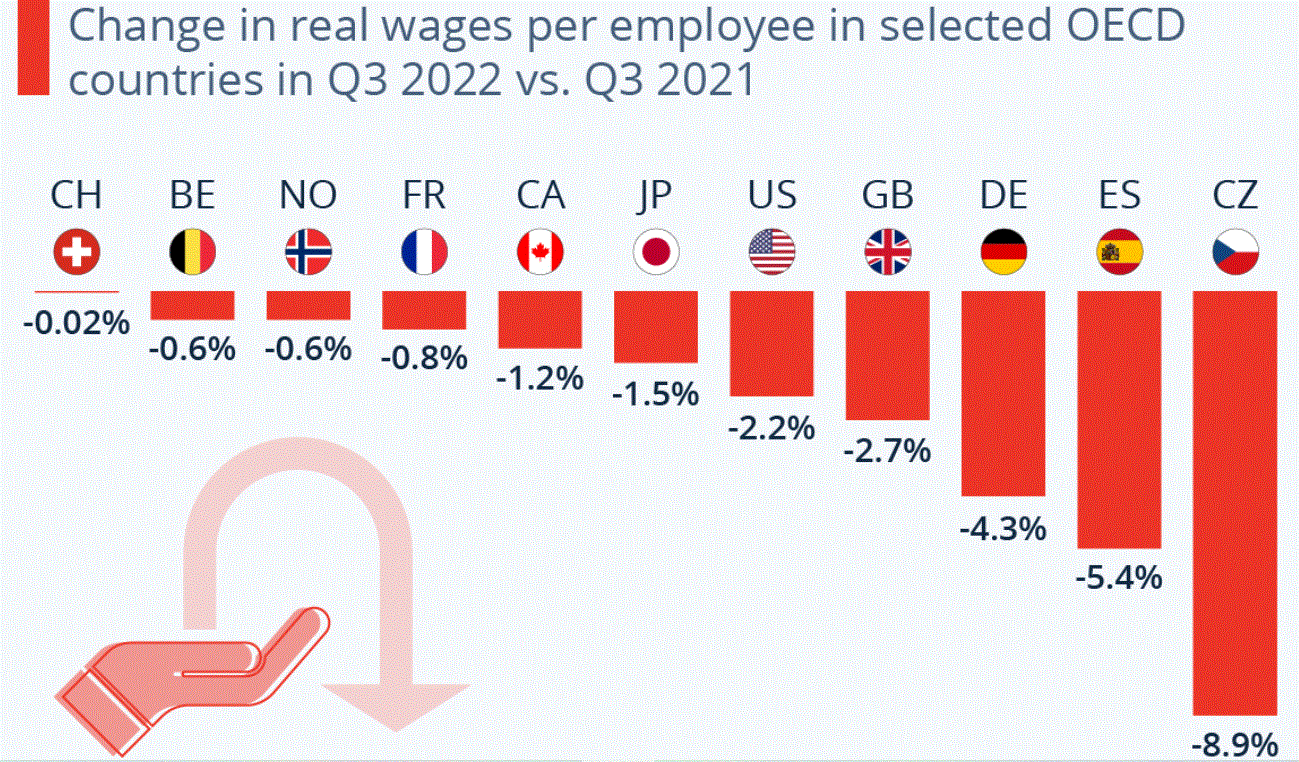

Over in Europe, protests, strikes, and other forms of dissent aimed at declining living standards, and worsening perceived prospects for the future are spilling into the streets, and showing up in polls that suggest support for establishment political groups are evaporating very fast. For instance, Politico reports on recent Dutch polls that suggest a new farmer's political party now has twice as much support as the nearest establishment rival party that is currently in power, sitting at 33%. In Italy, we saw the rise of anti-establishment right-leaning parties that won the latest elections. In France , anti-establishment potential candidate Marine Le Pen would comfortably win the next presidential elections according to a recent poll. These numbers are a reflection of disillusionment as workers in Germany for instance saw a decline in real wages of over 4% last year. Most advanced economies saw a decline in real wages last year.

{kind=link}

I personally doubt that in the long term, politicians will win votes by pledging to increase defense spending, while we see such trends in place, which have a dramatic effect on the everyday life of the electorate. If anything, we may actually start seeing a dramatic slashing in military spending in the Western World as well as globally. The pivot may come with a robust diplomatic effort to reverse the current course of confrontational rivalry and return to policies meant to find ways to boost economic performance, which is the only way to reverse the current, increasingly entrenched trend of widespread loss of real buying power among consumers.

It may seem like an incredible, in other words not a credible hypothesis, given the current trend of rising geopolitical tensions. As unlikely as that may seem right now, given the public discourse we are seeing, as well as ongoing policies meant to further inflame the situation, my view is that there is nothing like the factor of necessity to force a dramatic pivot away from the current course. Based on everything we are seeing, between ballooning deficits and an increasingly battered working class, it does make sense in my view to assume that we are likely on the cusp of a dramatic public policy pivot in the sphere of geopolitics.

Investment implications

Most of the stock price increases we have seen with defense companies like Northrop in the past year or so are predicated on the assumption that long-term government policies which are assumed to be eager to pursue dramatic defense spending hikes are being shaped by the current geopolitical trend of rising global tensions. It is a good thesis, with only one flaw, namely that it relies solely on one driving factor being considered to the exclusion of all others, including the social and fiscal factors I touched on. With the positive factor arguably priced into Northrop's stock price, while the contrarian factors are not, the risk/reward equation, looks too heavily slanted toward the risk side.

If I am correct and we will see a pulling back from the ratcheting up of geopolitical tensions, Northrop's stock price has the potential to retrace back to pre-war levels in February 2022. On the other hand, there is seemingly little that can be expected in terms of further upside. Western governments are tapped out and in much need of addressing rising domestic discontent. The Middle East is gradually hedging its bets by embracing China, and to some extent Russia, therefore US weapons sales in the region could decline significantly.

It is hard to see where those expected higher sales will come from, once one moves away from only considering one aspect of current trends. Northrop may perhaps do better than its industry peers if, for instance, its products will prove to fit new military strategic thinking better than that of its peers. Having said that, it has to be recognized that there are plenty of reasons to expect public policies that currently favor the bullish thesis for the Western defense industry to be reversed, meaning that the defense industry overall is not likely to be a long-term winning investment choice, especially at current stock price levels.

There is of course always a chance that despite all other social, economic, fiscal, monetary, and other issues, Western governments and other allies around the world will nevertheless continue growing their military budgets for the foreseeable future. The Q1 beat in expectations that we saw could continue this year and extend into next year, and perhaps beyond. If that is the case, it will be good for Northrop's business. Given that it is already more or less market consensus that this is the way that events will unfold, a lot of it is already expected and therefore baked into Northrop's current stock price. With a forward P/E ratio of over 20 currently, it is not a cheap stock by any means, which is a symptom of the market expectations that are already priced in. In conclusion, limited upside, and significant downside risk, therefore this is not currently an attractive investment opportunity, at least not by my standards, even though it does have some potential to provide investors with positive results this year.

For further details see:

Northrop Grumman: Q1 Stellar But Long Term In Doubt Due To Government Finances Deterioration