NOC - Northrop Q1 Earnings: Solid Results And An Outlook Upgrade

2023-05-03 10:10:45 ET

Summary

- Northrop Grumman Corporation reported Q1 earnings on April 27 and managed to outperform both top and bottom-line estimates from Wall Street analysts, as well as my own estimates.

- Northrop continues to see strong demand across most of its segments, with the space segment, in particular, seeing very strong double-digit growth.

- EPS was positively impacted by multiple timing benefits and created a $0.30 tailwind, but even when we exclude this, Northrop outperformed the consensus.

- Following this EPS benefit, management upgraded its FY23 outlook, now expecting better EPS growth.

- The long-term outlook for Northrop remains impressive, and combined with excellent shareholder returns, this is offering an attractive risk-reward profile.

Investment thesis

I maintain my buy rating on Northrop Grumman Corporation (NOC) and update my revenue and EPS estimates following the company's Q1 2023 results which beat its previous guidance, my own estimates, and those of Wall Street analysts . Northrop delivered an outstanding quarter with solid growth across most of its segments and better than expected EPS as a result of some timing benefits. As a result, management increased its EPS outlook for the full year and expects solid continued growth in Q2.

I last covered Northrop in April, when I rated shares a buy. Northrop is one of my top picks in the defense and Aerospace industry, primarily due to its strong position in the space industry, where it has seen stellar growth over the last several years. In addition, the company is also one of the largest defense companies in the world, delivering high-tech hypersonic and strike missiles, missile defense systems, state-of-the-art long-range bombers through its B-21 program, and much more.

With both the space industry and defense industry seeing strong secular tailwinds (like commercial space travel, renewed space interest among governments, and increased defense budgets all around the world as a result of the Ukraine war), growth is expected to remain strong for Northrop over the remainder of the decade, allowing for significant margin improvements and shareholder returns.

Shares have seen a pretty impressive performance over the last decade with the share price up close to 500%, despite shares falling from a top of around $550 per share to just around $450 today. In addition to share price appreciation, Northrop has returned vast amounts of cash to shareholders over the years through a solid dividend (1.51%) which has been growing for 17 straight years and at a 5-year CAGR of 11%. Going forward, management targets to return 100% of free cash flow to shareholders, and with Northrop expected to see meaningful free cash flow growth, this will bode well for investors.

In this article, I will take you through the latest developments and financial results and update my estimates and view on the company accordingly.

Northrop delivered a very solid Q1 result, driven by space

Northrop released its Q1 earnings on April 27 and reported a solid beat on both the top and bottom-line consensus. Northrop is seeing a resilient operating environment and remains confident in its outlook. That Northrop is not seeing any sort of slowdown and strong demand is also highlighted by its growing headcount which, again during the latest quarter, grew significantly. On the supply chain issues, management stated that it is seeing a slight moderation here but is expecting issues in the supply chain to remain for some time. Also, while inflation is moderating, this is still affecting Northrop's cost base, as this drives cost increases. Yet, with inflation easing further over the next couple of quarters, there is some room for margin expansion as a result.

Moving to the results, revenue came in at $9.3 billion and was up a very decent 6% YoY. This was in line with the midpoint of guidance by management and shows the continued capacity expansion and strong demand. Also, revenue beat the consensus by $110 million and was $80 million above my own estimations. Bookings for the quarter came in at $8 billion, below revenue but in line with management's expectations. The backlog remains strong at 2x annual sales, nevertheless.

Looking at the individual business segments, growth this quarter was once again driven by stellar growth in the space segment as this one grew by 17% YoY and reported revenue of $3.4 billion, accounting for 37% of total revenue. At the same time, the Aeronautics segment was lagging slightly as revenue decreased by 7% YoY, primarily due to some timing on large programs. As a result, revenue for this segment came in at $2.5 billion, accounting for 27% of total revenue.

Mission systems sales were up 3% YoY and now totaled $2.6 billion, accounting for roughly 27% of total revenue. Defense systems were up 7% with revenue coming in at $1.4 billion, accounting for 15% of total revenue. These segments are both seeing robust global demand as a result of the global threat environment due to the war in Ukraine and tension between Taiwan, China, and the U.S.

Moving to the bottom line, the operating income also increased by 6% YoY as margins remained steady at 10.2%. However, EPS decreased by 10% YoY due to the $1 impact of low net pension income. Northrop expects this to remain a headwind for the remainder of 2023 due to a tough comparison, yet this should increase again at the start of 2024. Still, despite this impact, EPS came in at $5.50, which beat the consensus by $0.38 and my own estimates by $0.30.

This massive beat was due to a number of benefits. This included the relatively low corporate unallocated expenses, which Northrop also expected to be weighted toward the second half of the year, resulting in a $0.10 timing benefit. In addition, marketable securities also were favorable and contributed roughly $0.10 to EPS. Finally, the Q1 estimates tax rate came in lower than anticipated by management which caused another $0.10 benefit to EPS, totaling $0.30 benefit to EPS. Yet, even when we take out these timing benefits, EPS still beat the consensus by $0.08 and came in on par with my expectations, showing a solid financial performance from Northrop.

Finally, Northrop is fully focused on its capital allocation priorities, which are investing in the business and production capacity growth, as well as returning cash to shareholders. In previous earnings calls, management stated that it plans on returning 100% of free cash flow to shareholders. In the latest quarter, management returned approximately $1 billion to shareholders through both dividends and share repurchases. And indeed, with this, management returned almost 100% of free cash flow ("FCF") to shareholders as free cash flow came in at $1.01 billion, which is at the midpoint of what management guided for. FCF was impacted by higher net cash used in operating activities and slightly higher Capex, which caused free cash flow to come in $279 million lower.

Overall, this shows a financially strong quarter from Northrop as the company continues to perform strongly and beat analyst estimates. Now, before we get into the outlook for FY23 and the next quarter, let's discuss some of the most important developments from last quarter.

Quarterly developments - space, defense budgets, and capacity expansion

In March, the U.S. government released the proposed defense budget for fiscal 2024, and this was to the liking of Northrop management. During the earnings call, management was very optimistic about the proposed defense budget which is up nearly 4% and should support Northrop in strategic deterrence, space, missile defense, and advanced computing and communication technologies.

Specifically, management highlighted that the budget for weapons capability and capacity is expected to increase by 20% in FY24 to increase major weapon programs for which Northrop provides key components. This increase is no surprise after the U.S. government is forced to replenish its weapon inventory after sending many billions in weapons to Ukraine.

And there is more good news for Northrop in this proposal, as management believes funding for two of its franchise programs, being the GBSD and B-21, should see a prioritization in the new defense budget proposal, resulting in an increase in the budget from $8 billion in 2023 to $15 billion in 2024.

And also, outside of the U.S. Northrop is seeing strong demand as global demand budgets are increasing. During the latest quarter, Northrop was able to report significant orders from the likes of Australia and Japan. As a result of this significant increase in demand, the largest challenge for Northrop today is increasing its overall weapon production capacity to be able to satisfy global demand, which obviously is a huge positive. In my previous article on the company a month ago, I extensively discussed the global outlook for defense, and this is looking very good for Northrop as most NATO countries need to significantly up their defense spending to meet the 2% of GDP target. And while I am not expecting many to reach this target anytime soon, if ever, it is functioning as a tailwind and will boost global defense budgets over the next several years.

The investments from management in the capacity expansion are already visible in a huge state-of-the-art 113,000-square-foot facility designed to support the production of up to 600 strike missiles per year. Also, Northrop is building a new hypersonic center in Elkton, Maryland, which is expected to open in the summer and support programs like hypersonic attack cruise missiles. And Northrop is not only focused on attack missiles but sees that missile defense (including sensors, interceptors, and command and control systems) is a fast-growing product segment as well, with this now approaching to be responsible for 10% of company revenue. Therefore, with capacity increasing and demand accelerating, there is plenty of reason to be optimistic about the future of Northrop from a defense perspective.

Yet, I am even more bullish about Northrop's potential in the space industry. In my previous article on Northrop, I spend a lot of time discussing the strong outlook for the space industry and how I believe this to be a serious growth driver for Northrop in the decade ahead, driven by a fast-growing industry through consumer interest and government interest, as well as promising partnerships with the U.S. government and NASA. And this quarter was no different with Northrop once more reporting impressive growth rates for this segment as its market share in the space industry expands.

Moreover, while the cornerstone of the Northrop space segment is national security and supporting the U.S. and its allies, the company is also increasingly expanding its offering towards science and space exploration as it has the knowledge in-house. This, in part, has the potential to drive solid growth.

In addition, management expects space to be a future growth driver for the company. Yet, it warned investors during the earnings call not to get used to double-digit growth for this segment as we have been experiencing over the last several years as this might not be sustainable going forward. Still, Northrop has seen its position in the industry grow rapidly. And with most of the space programs still in their early stages, Northrop is seeing great growth ahead as these programs transition into production for higher volumes and higher margins. With this still ahead, the outlook is solid.

Also, Northrop is seeing no problem in the fact that SpaceX has now started focusing on defense work. During the Q&A with analysts, Northrop spoke about this and was enthusiastic about it as management was positive about its partnership with SpaceX to drive next-gen innovation. Overall, while competition might be increasing, Northrop remains very confident in its ability to innovate and emerge as the winner. I see no reason not to trust management in this.

Finally, other business updates included the B-21 program, which remains on the government's baseline for cost and schedule, according to Northrop. Demand for the product is strong as this should become the centerpiece of the Airforce's long-range strike portfolio. Therefore, the long-term outlook for this program remains robust and should bring in solid amounts of cash over the decade to come.

Outlook & NOC stock valuation

For the second quarter, Northrop guides for revenue to be flat sequentially and to account for less than 25% of FY23 revenue, with revenue growth expected to be slightly better in the second half of the year. In addition, the timing benefits seen last quarter should ease off in Q2 and just like in Q1, management plans to return 100% of free cash flow to shareholders through both dividend and share repurchases which are expected to be around $720 million.

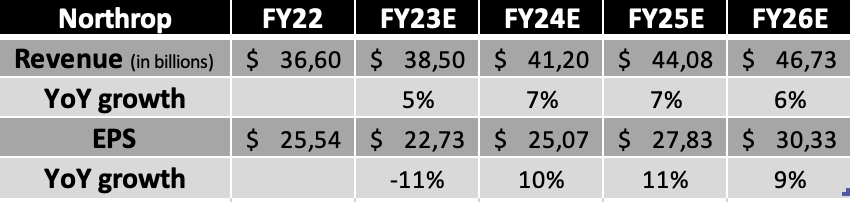

With first-quarter results coming in roughly in line with previous expectations from management, they reaffirmed FY23 guidance with no changes in its segment results. This means Northrop is still targeting revenue of $38 billion to $38.4 billion for the full year or about 4.5% growth at the midpoint. Also, the book-to-bill ratio is expected to be just under 1x for the full year.

Yet, management has increased EPS guidance by $0.40 following the $0.30 beat last quarter and the divesture of a small minority investment expected to close sometime later this year. As a result, management now projects an EPS of $22.25 to $22.85

Finally, management believes revenue to accelerate again, after a relatively flat 2023, in the following years, due to the timing of some major programs. Also, management remains confident in its ability to show significant free cash flow growth until the end of the decade.

Following these updates from management, the strong quarterly results, and the improved outlook, I now arrive at the following expectations until FY26.

{kind=link}

Shortly explaining these estimates, I now expect Northrop to report slightly higher revenue of $38.5 billion, up from $38.42 billion before. In addition, EPS is now up $0.25 from my previous target following a much better Q1. At the same time, I have slightly lowered my long-term estimates as I expect Northrop to see somewhat lower growth in defense, and from FY24 onwards, I expect the space segment to fall back to high-single digits growth. EPS is expected to grow slightly faster from FY24 onwards, driven by Northrop's lower share count and margin improvement. Overall, I think the long-term outlook is still very strong and this should result in very strong shareholder returns.

Moving to the valuation, this one has come down a bit after a 5% drop in share price as shares are now valued at a forward P/E of close to 20x. This is what I said regarding the valuation back in April:

And when comparing its current valuation to those of its peers, we can see Northrop is the most expensive by far. Yet, this is partly due to its EPS falling off a cliff next year due to pension liabilities as mentioned earlier. Taking these liabilities out of the equation, Northrop would trade at a forward P/E of approximately 18x, much more in line with its peers."

Considering better growth expectations and a highly volatile and uncertain market right now, a higher valuation compared to the last 5 years and its peers should not come as a surprise. As a result, I believe a P/E of 20x is justified for this quality compounder and offers a fair entry valuation.

I still believe Northrop deserves to trade at a premium when considering its long-term outlook and stability. Therefore, my opinion remains unchanged, and I believe a P/E of 20x is justified. Therefore, based on my FY24 EPS estimate and a 20x P/E, I calculate a target price of $501 per share, down slightly from a previous $503 per share and leaving investors with an upside of approximately 12%. (Please note, this target price is solely based on its forward P/E and is only for indicative purposes.)

For comparison, 21 Wall Street analysts currently maintain a price target of $511 per share, combined with a buy rating.

Conclusion

I remain bullish on Northrop Grumman Corporation after the impressive quarterly results delivered by the company and the strong (upgraded) financial outlook. Northrop once more outperformed the consensus and my own expectations. Moreover, the company looks poised for solid growth over the remainder of the decade, driven by its exposure to the space industry, solidifying its position, and strong growth in defense spending, which benefits Northrop's missile and defense segments.

Yet, despite the solid Northrop Grumman Corporation quarterly results and improved outlook, I slightly lowered my price target from $503 to $501 per share, leaving approximately a 12% upside for investors. And while this is not quite as much as I would prefer, this is offering a better entry point compared to my April article, as the upside has grown following a dip in the share price. Therefore, I maintain my buy rating on Northrop Grumman Corporation as the current share price weakness offers an attractive starting point to build a position in Northrop and benefit from its consistent revenue and FCF growth over the remainder of the decade.

For further details see:

Northrop Q1 Earnings: Solid Results And An Outlook Upgrade