CA - NorthWest Healthcare: How To Play The Upcoming Distribution Cut

2023-03-30 10:50:13 ET

Summary

- We gave NorthWest Healthcare a Sell rating the last time around and the stock has dutifully moved lower.

- The glaring red flags on the dividend have only become a brighter shade of crimson since then.

- The distribution is now on the clock and we think it could be cut very soon.

Notes: All amounts discussed are in Canadian dollars. All prices refer to the stocks on TSX. OTC prices are not mentioned anywhere.

When we last covered NorthWest Healthcare ( NWH.UN:CA ), ( NWHUF ), we took an axe to our price target, just as we expected an axe to the distribution levels.

We think when all is said and done, interest coverage will deteriorate further and NWHUF will have a hard time holding on to even a 17 or 18 cent quarterly AFFO. The dividend will be cut ultimately in our opinion, and we are moving up the risk on our proprietary Kenny Loggins scale.

Trapping Value

We also are downgrading this to a sell and will revisit this should the news flow dictate.

This was our first sell rating on NorthWest, after covering it for more than five years. The stock gave a nod to our call and headed south.

Returns Since Last Article-Seeking Alpha

We are updating our thesis as the timeline of the distribution has changed in our opinion.

Upcoming Results

NorthWest's announcement (premarket March 31, 2023) for the Q4-2022 results is the latest among the companies we follow. It has a traditional December year end and the results will be coming at the exact end of Q1-2023. This is incredibly late and the last two year-end reports were around March 15. The delay likely comes from the company exploring alternatives to its major predicament. Another consequence of this delay is that at this point, NorthWest also has a firm grasp of how its Q1-2023 will look.

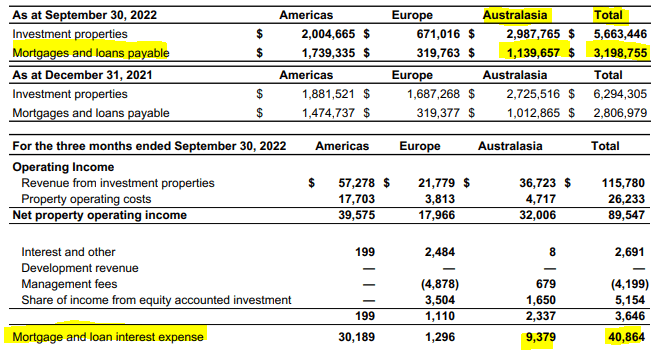

For NorthWest, revenues are rather predictable. Tenants are creditworthy and rent highly desirable properties. Rent coverage is generally superlative and late payments and renegotiations are extremely rare. What will drive the numbers is the change in interest payments. When we spoke about this in relation to Q3-2022, the interest payments had jumped. But that was just a warm up. Look at how much the Federal Funds rate has moved since then September 30, 2022.

Australian central bank has fired off its hikes as well since then.

RBA-Trading Economics

In case you're wondering why we're mentioning the Reserve Bank Of Australia's agenda, here's a picture for you.

{kind=link}

NorthWest Q3-2022 Financials

Australia is a key piece of the debt and interest rate puzzle and it forms about 35% of the total debt and 23% of the interest costs.

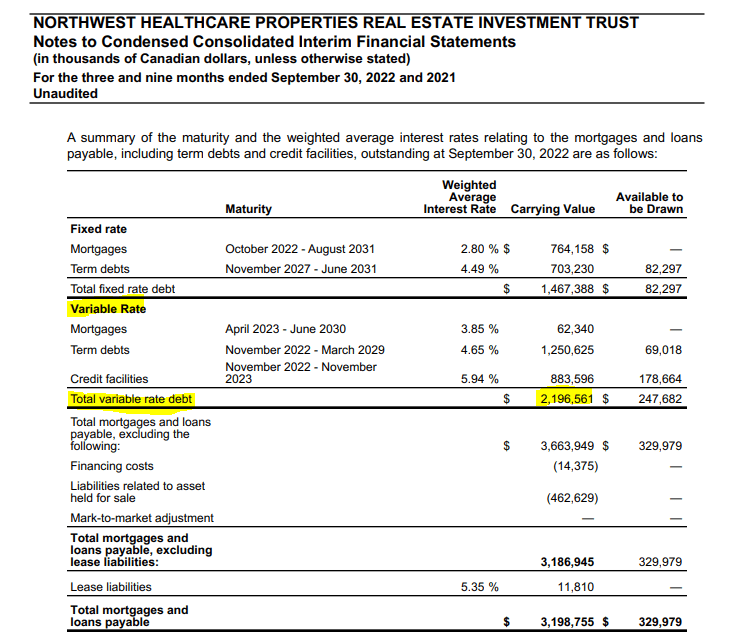

So here we would note two very important things. The first being that NorthWest has huge exposure to variable rate loans - 60% of loans were variable rate at the end of Q3-2022.

{kind=link}

NorthWest Q3-2022 Financials

The second point is that these all move up, with a lag of 60-90 days. So in Q3-2022, we were seeing baby impacts from the first hikes. The real fun and joy will come in Q2-2023 as everything flows through. This is basic finance and bulls that are missing this are doing themselves a huge disservice.

Our Numbers

Predicting funds from operations (FFO) is a complicated task as there are multiple adjustments that management makes. But we can make educated estimate based on what we do know. Our key number here is the $40.8 million in interest expense in Q3-2022. We see that moving up and over $51.0 million by end of Q2-2023. That's a bare minimum in the absence of those big asset sales that management has been aiming for the last three quarters. So if we take the baseline Q4-2022 rate and deduct out an additional $10 million in interest expense, we're left with about $27.1 million in FFO per quarter.

NorthWest Q3-2022 Financials

That works out to about 11 cents, vs. the 20 cents a quarter distribution. Now investors may have some gripes with using the last quarter's FFO run-rate. Management had noted some one-off expenses. That might be true, but two thirds of the FFO drop from Q2-2022 to Q3-2022 was simply from higher interest expense. So even if we assume that those one-time expenses reverse, we're looking at a sub 13-cent FFO run rate. Based on all the information we're moving up the risk of a distribution cut.

Based on all the information, NorthWest gets the following dividend safety rating on our proprietary Kenny Loggins Scale.

Trapping Value

A "Call Kenny Loggins" rating implies a 90% plus probability of a distribution cut within 12 months.

How To Play

If you're going to speculate here, you need to know a few things. The first being - what could make us wrong. If somehow management can pull off those asset sales, without taking a huge loss, it will delay the inevitable. It might even give the stock some life and perhaps allow equity issuance. That rare possibility aside, we think that the cut is coming between the results being announced tomorrow and the Q1-2023 results.

The second thing is to forget price anchoring. The stock is not cheap because it's substantially lower than where it was. If we're right and the FFO run-rate is 52 cents a year, NorthWest is trading at 16X FFO. That's stupidly expensive in today's market. The dividend also is likely to be 40 cents a year, which makes your new distribution yield 4.7%. that is hardly enticing in today's market.

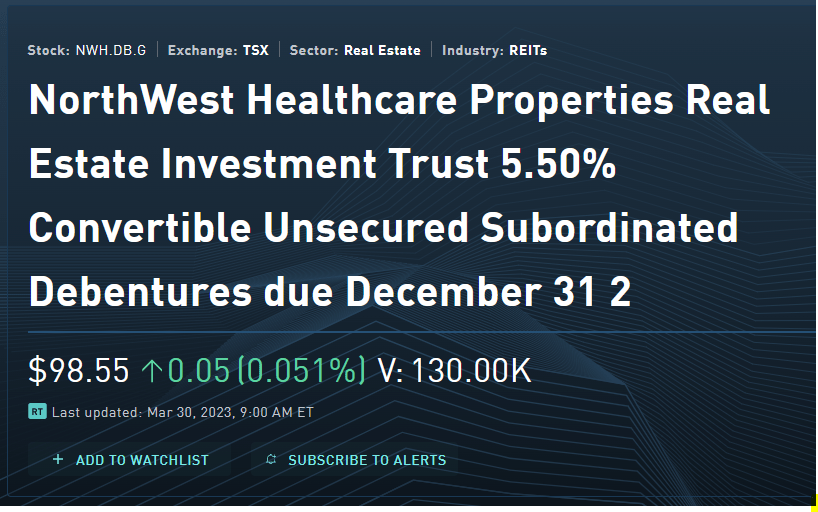

For those enamored by the assets and looking for a yield play, we would look at the convertible debentures. We would of course forget about the "convertible" part of the equation as NorthWest won't be in the same postal code as that conversion price. But they do offer very solid yields to maturity.

NWH.DB.G offers a 7.44% yield to maturity (December 31, 2023).

{kind=link}

TMX

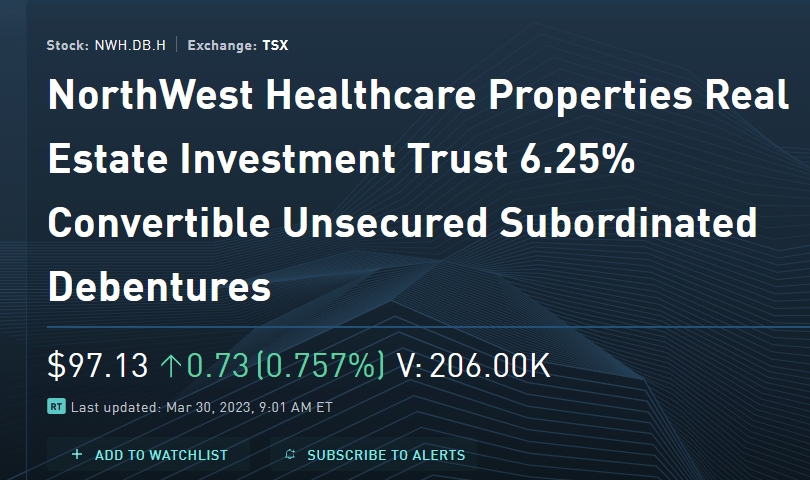

NWH.DB.H offers a 7.1% yield to maturity (December 31, 2027).

{kind=link}

TMX

Both are finer prospects than the common stock. We continue to rate that a "Sell" and think the distribution cut will still surprise the markets and the fan club. We would look to speculate on the long side only at a sub $6.00 price.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

NorthWest Healthcare: How To Play The Upcoming Distribution Cut