CA - NorthWest Healthcare: The Distribution Is Set For A Big Cut

2023-08-16 12:19:37 ET

Summary

- NorthWest Healthcare Properties announced major changes to the executive team and their Q2-2023 results.

- The AFFO run-rate is now at an annualized 52 cents and the payout ratio is at 154%.

- We tell you why a minimum 50% distribution cut is needed to stabilize the REIT.

Note: All amounts discussed are in Canadian Dollars

The best weapon you have in the markets is the ability to change your mind when facts dictate. Most of the time it is a single switch, though even that is very hard to make as you have to first admit that you were wrong. Occasionally, you get to make a full 360-degree turn by admitting you were wrong and then admitting you were wrong about thinking you were wrong. We had one such recent experience with NorthWest Healthcare ( NWH.UN:CA ) ( OTC:NWHUF ).

The Original Story

We downgraded NorthWest to a sell in November 2022 . The key thesis was that the company was headed for trouble as it had an extremely short debt maturity profile, and it had bought tons of properties with the idea of offloading them later in a JV to earn management fees. That call was timely, and we stuck with the follow-up article .

Seeking Alpha

The Upgrade

In an unusual twist, NorthWest reported that it had actually managed to do the impossible. There were four points which they addressed, and frankly we thought even one of them would be impossible to do in 2023. Those were:

1) Completed a JV for the UK portfolio

2) Hedged interest rate exposure to a point where they would not be a further drag anymore.

3) Promised to deleverage post the JV down below 50% (53.1% on immediate closing).

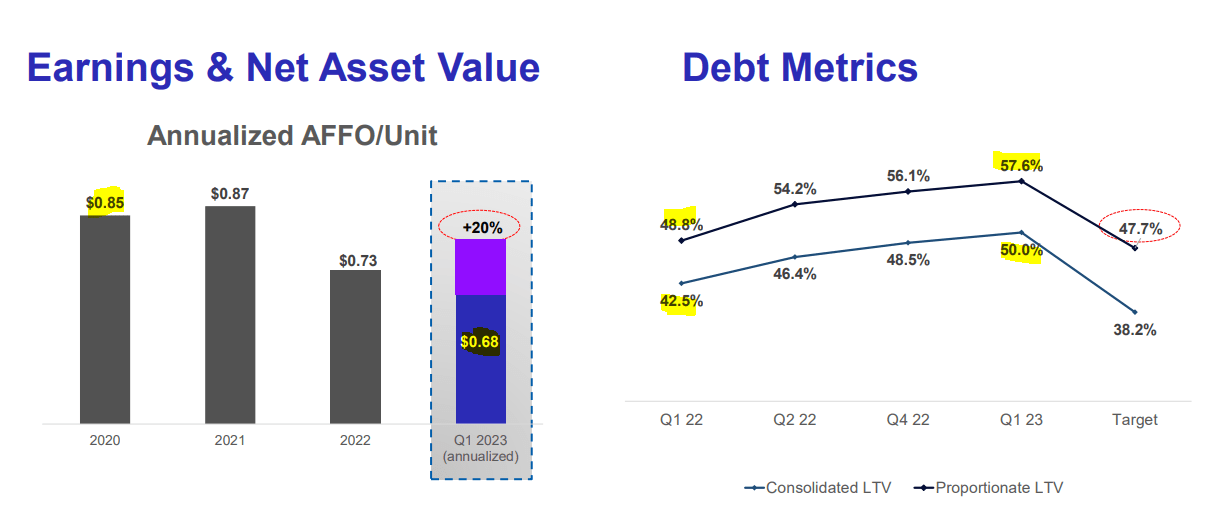

4) Suggested adjusted funds from operations (AFFO) would be back up to over 20 cents on a quarterly basis ( transcript comment of 20% increase over 17 cents in Q1-2023).

Ok, so we were wrong and we gave them an upgrade. That also had to do with the fact that the price was a little better suited for the market conditions, but the upgrade was earned because of what they delivered and promised to deliver.

The Second 180-Degree Turn

We can count on one finger the number of times a company has announced a massive transaction and then announced it got called off, two weeks later.

Northwest Healthcare Properties Real Estate Investment Trust (the "REIT") announces that its UK healthcare real estate joint venture will close in June 2023, the completion of the sale of its Bakersfield Hospital on May 31st, approval from the Toronto Stock Exchange (the "TSX") to acquire up to 10% of its public float under a normal course issuer bid and the suspension of its distribution reinvestment plan beginning with the upcoming June 2023 distribution.

Source: NorthWest June 7, 2023

Northwest Healthcare Properties Real Estate Investment Trust (the 'REIT'), announced today that the REIT and the previously referenced Institutional Investor will no longer be proceeding with the REIT's previously disclosed UK joint venture.

Source: NorthWest June 21, 2023

The company then followed that up with an additional major announcement and their Q2-2023 results. Let's look at both.

The Board Shuffle

In a long overdue move, NorthWest made some big changes to its board.

1) Mr. Dale Klein, formerly Lead Independent Trustee, was promoted to Non-Executive Chair.

2) Mr. Paul Dalla Lana resigned as Chief Executive Officer. Mr. Craig Mitchell, formerly President, has been appointed interim CEO.

3) Ms. Laura King, Trustee, was appointed Chair of the REIT's Compensation, Governance and Nominating Committee.

4) Ms. Maureen O'Connell, Trustee, was appointed Chair of the Audit Committee.

Mr. Dalla Lana spearheaded the growth strategy at NorthWest. When we say "growth" we really mean unbridled purchases of properties with zero value creation. Don't believe us? Think that is too harsh? Well, don't take our word for it. Just ask NorthWest. At the end of Q1-2023, AFFO had dropped 20% on an annualized basis from 2020 numbers. All while debt to assets was up by about 8%.

{kind=link}

That is not the kind of growth anyone should sign up for. Investors may argue that maybe this is too short a timeframe to understand the growth. That is a reasonable counterpoint, so let's look back further. Over the last decade, unit count has exploded up 527%.

You just have to Google "secondary offering for NorthWest" to find out just how frequently NorthWest did them under its now ex-CEO. Almost every single one of them was under their own estimates of net asset value. Going back to the beginning of this timeframe, AFFO and FFO were higher than what we saw in Q1-2023.

{kind=link}

The counterpoint here is that the CEO does own a lot of the stock. More than almost any other real estate company we follow with just one exception. Mr. Dalla Lana owns more than one quarter of the firm on last check. So there is a vested interest here but so far that has produced really poor results. The idea of moving to a capital-light model where third-party fees made up the majority of the revenues is also not something we found appealing. Investors might remember that W.P. Carey Inc. ( WPC ) sacrificed a few years of AFFO growth just to unwind that third-party portion.

Q2-2023

Q2-2023 was the quarter for NorthWest to deliver. After poor showings in Q4-2022 and Q1-2023, the stage was set for that increase in AFFO that would save the distribution. Of course, we would not have expected to see anything big as the UK deal was thrown out. Even if that had occurred, it would be late in the quarter to have influenced things materially. The hope was for about 17-18 cents of AFFO that would be helped by the interest rate hedging that management talked about. The revenues came in fine. Although down from Q1-2023 we had two assets less in this quarter due to sales. Net operating income (NOI) was great and the number rising 2.7% while revenues were down 7% from Q1-2023 is exceptional. But those aside, the overall showing was still problematic. AFFO dropped 20% from Q1-2023.

Q2-2023 Financials

That's right. A 20% drop from the last quarter. That made it a 32% drop from Q2-2022. The payout ratio which looked bad last year and horrible in Q1-2023 catapulted to 154%.

A Closer Look At That Interest Expense

Leaving aside the one-off items that always get blamed for the AFFO miss, the biggest factor was the interest expense. We are up 65% year over year while investors have been stuck on the "great properties" line.

Q2-2023 Financials

Interest coverage is still not extremely bad (1.79X), but the REIT is hemorrhaging cash when taking into account how much it is paying in distributions. More longer-term concerns remain. The front end of their debt maturity has already taken a hit from the high rates, but the refinancings in 2025 will blow through any bull case if rates remain anywhere near here.

{kind=link}

If you think that NorthWest has great access to funds at low rates, you just need to read what they are paying on recent transactions.

On July 21, 2023, the REIT refinanced Australasian term debt maturing in September 2023 with an outstanding balance as at June 30, 2023, of $70.0 million and bearing variable rate interest of 6.35% to extend the weighted average term to maturity by 4 years. The refinanced facility bears interest at 5.95% .

Northwest Healthcare Properties REIT 3 MD&A - Second Quarter 2023 ii. On August 2, 2023, the REIT executed an interim non-revolving tranche under its revolving credit facility to increase availability by $50.0 million. The tranche matures in October 2023 and can be extended until January 2024 under certain circumstances. The facility is secured by certain assets in the REIT's Americas portfolio and it bears interest ranging from 10.6% to 13.8%.

Subsequent to June 30, 2023, the REIT extended the maturity date of its revolving unsecured credit facility with an outstanding balance of $125.0 million credit facility by one year to November 2024. The facility bears interest ranging from 8.73% to 10.01% (previously 8.23% to 9.51%) .

Source: Q2-2023 Financials (emphasis ours)

Verdict

The plan forward has to be one to go to an emergency mode until the REIT can stabilize and improve its core metrics. At a minimum it means not paying more than what they make. Ideally, they should be paying only what is required under REIT rules and stopping the distribution to deleverage. If we were to bet, we would wager that they cut it by 50%, within three months. NorthWest gets the maximum rating on our proprietary Kenny Loggins, dividend danger, scale.

Author's Scale

That is still, only the first step. Debt to gross book value needs to go back to 42%, where it was before NorthWest went all-in on "if we buy it, they will come to form a JV".

{kind=link}

Even they believe that if you go by what they said on the conference call.

Shailen Chande

Yes. So Tal, I'd really say, I mean, as you know, the REIT's current debt to gross book value is circa 50% on a consolidated basis and circa 58% on a proportionate basis. That's higher than where we'd like to see it longer term. We've historically guided to circa [ 45% ] on a consolidated basis. And as we consider our strategic review and as the Board engages on that, we'll be announcing to the market our initiatives and target balance sheet metrics.

Source: NorthWest Q2-2023 Transcript

The current NAV ($12.55) might be a piece of solace for the bulls. A good chunk of that is the valuation NorthWest assigns itself for the fee-bearing capital.

{kind=link}

We remain skeptical that even $10.00 could be realized in today's market and estimate NAV to be closer to $8.00 today. Currently, there are seven NAV estimates from analysts on NorthWest with a low of $9.20 and a high of $12.50. The median is $9.75. Obviously, we think those are optimistic. Further, NAV does not pay the bills, cash flow does. You can still lose money by buying a discounted NAV REIT as the NAV falls and the discount widens. That is what we see happening here and would look to only buy after the distribution cut assuming a coherent plan to address the longer-term concerns is put into place.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

NorthWest Healthcare: The Distribution Is Set For A Big Cut