NWFL - Norwood Financial: Still No Good Reasons To Go Long

2023-11-30 10:30:00 ET

Summary

- Norwood Financial's Q3 results show a decrease in net interest income and a 50% lower pre-tax income compared to the same quarter last year.

- The bank's loan loss allowance and non-interest expenses are contributing to the decrease in pre-tax income.

- The bank's loan portfolio shows a decrease in the weight of commercial real estate loans and a 30% increase in consumer loans.

Introduction

Norwood Financial (NWFL) is the holding company that owns the Wayne Bank in Pennsylvania . With a balance sheet with total assets coming in close to $2.2B it for sure isn't the largest bank in the region, but I wanted to check up on this bank's performance as I have been keeping track , but I haven't found a reason compelling enough to warrant a long position.

I was eager to see the Q3 results

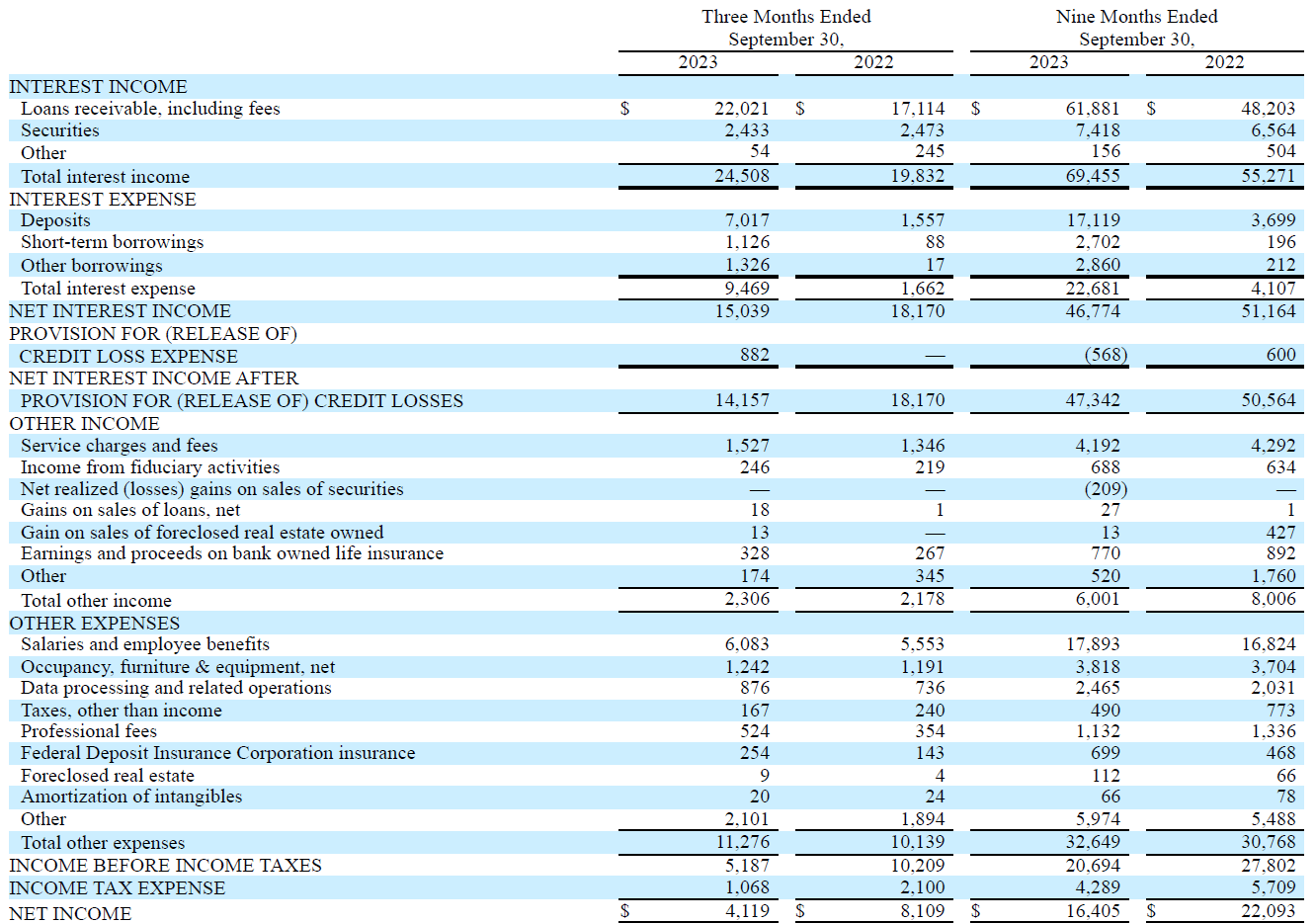

Of course, the evolution of the net interest income is very important for a bank like Wayne Bank (and thus Norwood Financial). And while we see the interest income has increased pretty substantially (by almost a quarter) compared to the third quarter of last year, the total amount of interest expenses has almost six-folded . This means the net interest income came in lower, at just over $15M, compared to almost $18.2M in the third quarter of last year.

{kind=link}

As Norwood Financial is barely generating any non-interest income ($2.3M in the third quarter, mainly related to $1.5M in service charges and fees), the relatively high non-interest expenses of $11.3M are definitely weighing on the result. As you can see in the income statement above, the net non-interest expenses increased from $8M in Q3 last year to $9M in the third quarter of this year. And that most definitely helps to explain the almost 50% lower pre-tax income. There is one other factor that contributed to that pre-tax income decrease, and that is the $0.9M loan loss allowance recorded during the third quarter. This partially reverses the previous provision release the bank recorded in the first half of the year.

The bottom line shows a net income of $4.1M or $0.51 per share . Given the circumstances, that's not really bad, but the bank clearly has seen better times.

Looking at the 9M 2023 results, you see the net income in the first three quarters of the year was approximately $16.4M, for an EPS of $2.03. This indeed means the bank's first few quarters of the year were substantially stronger than the third quarter (obviously fueled by the reversal of the loan loss provisions in the first semester).

The bank currently pays a dividend of $0.29 per share , an increase from the $0.28 quarterly dividend it paid before. And even after seeing the relatively weak Q3 results, the dividend is still very well covered.

A closer look at the loan book

Banks definitely are 'black boxes' in the sense that investors don't really know what's on the asset side of the balance sheet. Sure, we get an idea of what percentage of the loans are for instance mortgages, but as everything is thrown on one pile, you still don't know which assets or homes the bank owns the mortgage on. And although that most definitely complicates figuring out what a bank actually owns, the summaries are useful to know at least the breakdown of the different loan categories.

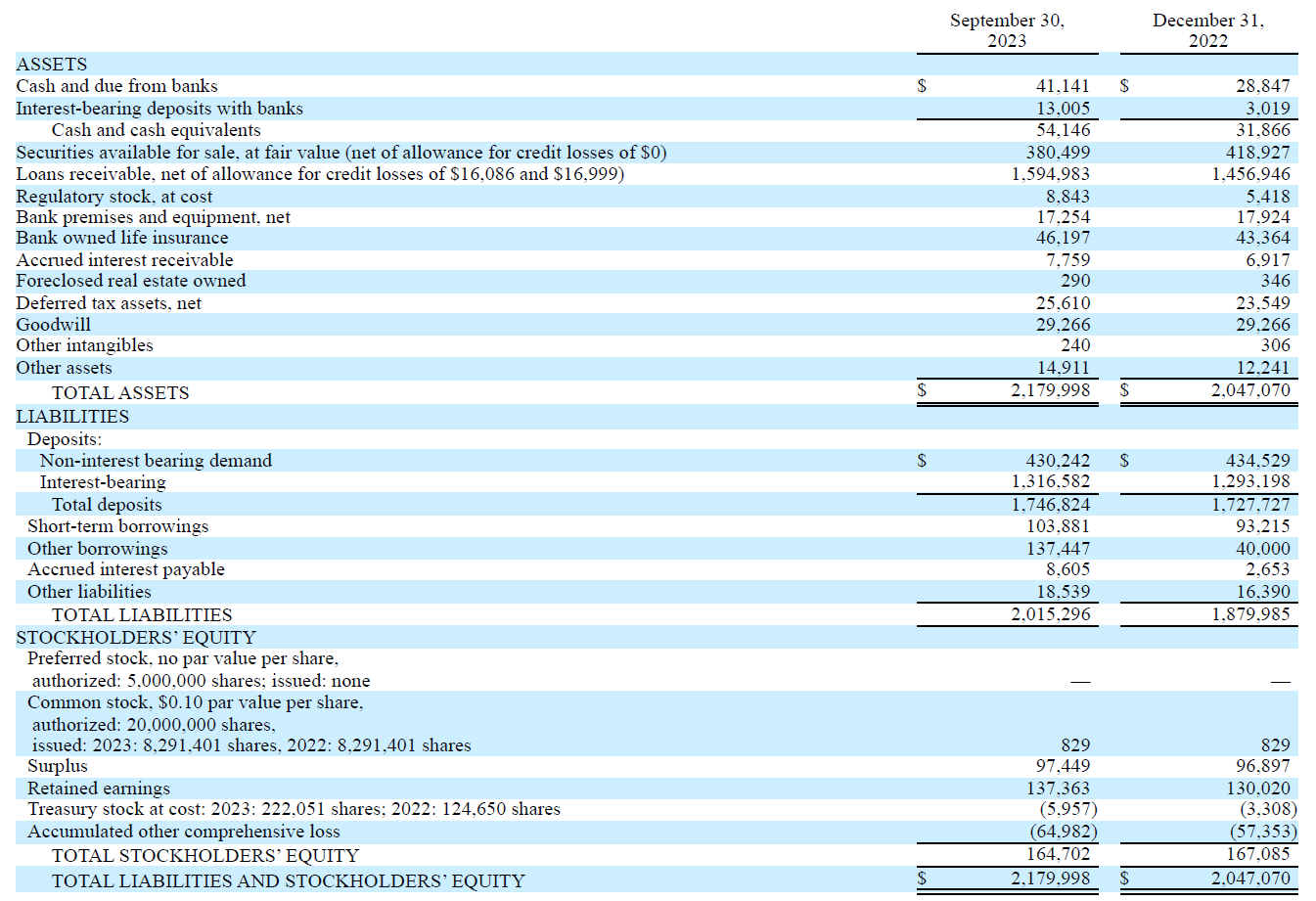

First, let's have a look at the balance sheet in general. The total size of the balance sheet increased to $2.18B, although the total amount of equity decreased by a few million dollars (the bank did retain the majority of its earnings, but it also accumulated some unrealized losses on its securities portfolio in the first nine months of the current financial year).

{kind=link}

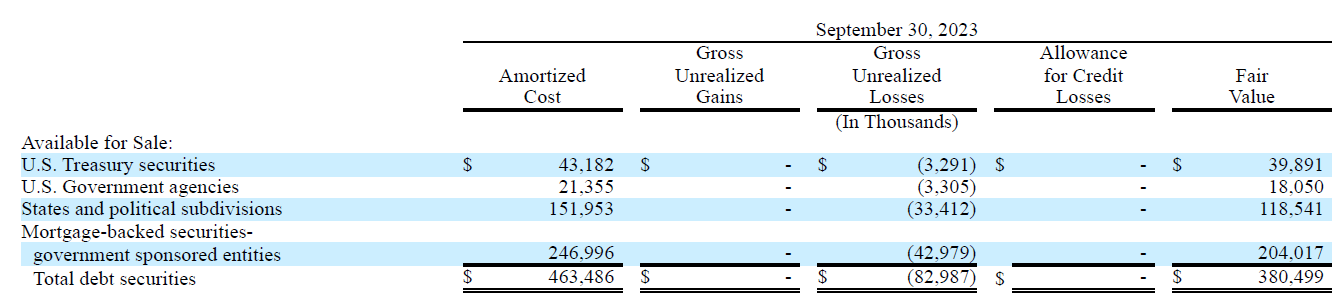

And as you can see above, the bank has about $54M in cash and deposits with other banks. It also has a pretty substantial portfolio with securities available for sale, totaling approximately $380M. As there are no securities on a held-to-maturity basis, there are no 'hidden' unrealized losses on the balance sheet, as the $380.5M in securities available for sale is the fair value as of September 30. And as you can see below, this already includes close to $83M in unrealized losses. So if the bank retains this portfolio of securities until their respective maturity dates, it will recoup a pretty substantial amount (vis-à-vis the total amount of equity on the balance sheet).

{kind=link}

Unfortunately, the remaining duration of those securities is very long. As the image below shows, less than 4% of the current value of the portfolio matures within the year, and just 14% of the securities mature within the next five years (the maturity dates of the MBS issued by GSEs have not been disclosed in the quarterly report so the real amount of near-term maturity dates may be higher). But in any case, we shouldn't bank on Norwood Financial recouping a big chunk of the unrealized losses anytime soon.

{kind=link}

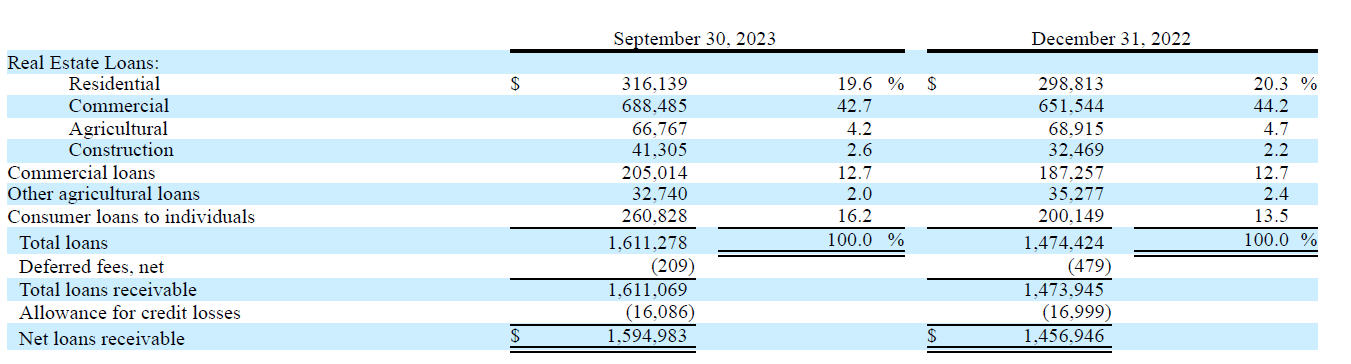

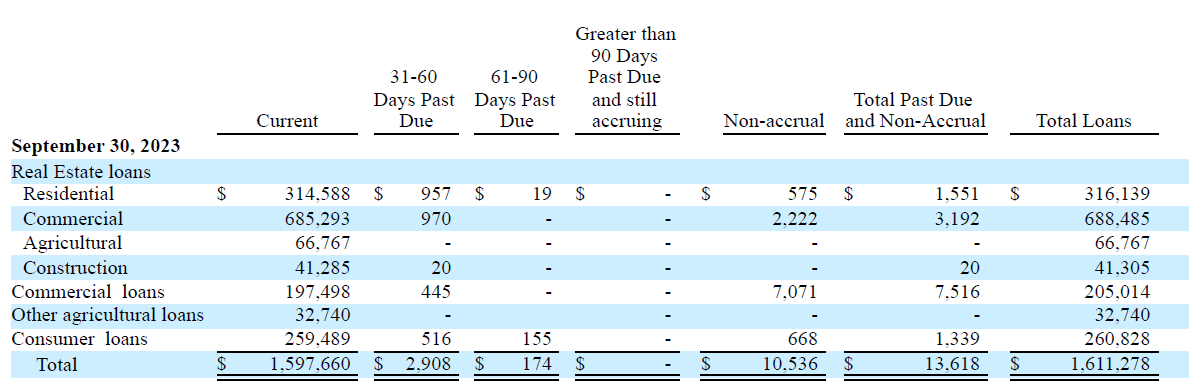

The balance sheet also shows the bank owns a $1.6B loan portfolio, and I'm always interested in seeing the breakdown of the assets in that portfolio. Interestingly, the total weight of commercial real estate loans in the portfolio has decreased, although the amount of exposure has increased in absolute numbers. Perhaps the most interesting evolution of the loan portfolio is the 30% increase in the amount of consumer loans. This increased by in excess of $60M resulting in a total weight of just over 16% of the entire loan book.

{kind=link}

While I am not very keen on consumer loans, it is a category Norwood Financial has had success in. As you can see below, only $1.34M of those loans are currently past due and no longer accruing, and that's about 0.5% of that portion of the loan book. It appears the commercial loans are the main category to keep an eye on, with $7.1M of the $205M exposure no longer accruing and an additional $0.45M of loans past due.

{kind=link}

With just over $16M in loan loss provisions, I definitely understand Norwood's decision to record a loan loss provision in the third quarter of the year.

Investment thesis

At the end of the third quarter, the company had a book value of $21.15 per share, but the tangible book value was just $17.49 which means the stock is currently trading at a premium of approximately 60% to its book value. That's pretty rich given the issues the sector has had to deal with in the recent few quarters. As the stock is also trading at a double-digit earnings multiple (especially now it looks like it will have to record additional loan loss provisions in the next few quarters to ensure its non-performing loans are well covered), I am still not a buyer of Norwood Financial.

For further details see:

Norwood Financial: Still No Good Reasons To Go Long