CA - NovaGold: Limited Margin Of Safety At Current Levels

2023-03-21 09:33:05 ET

Summary

- NovaGold Resources Inc. had a successful 2022 drill program, continuing to report some of the best intersections sector-wide, with many that rival the best intercepts from NGM's Nevada operations (Carlin, Cortez, TRUG).

- However, this was partially overshadowed by worse-than-expected inflationary pressures which resulted in several capex blowouts, suggesting that the 2021 TR capital cost assumptions may not be conservative enough.

- In fact, and as noted previously, the 2021 TR used Q1-20 pricing & I see an extremely low likelihood of delivering this project at a cost of just $7.4 billion.

- While higher gold prices will lift all boats, NovaGold is not a beneficiary today (like producers or near-term producers) and upfront costs and a higher cost of capital are negatives, so I continue to see far more attractive ways to play the sector.

2022 was a year to forget for most names in the VanEck Vectors Gold Miners ETF ( GDX ), with several producers suffering considerable margin compression and many developers and small-cap producers seeing 20% plus increases in their share counts. This resulted from inflationary pressures that resulted in much higher operating costs and several capex blowouts and or major revisions globally (Magino, Cote, Tanami, Valentine, Pueblo Viejo). Fortunately, the larger producers didn't have to dilute shareholders to come up with the extra capital to complete these projects, but the smaller companies did, with Argonaut Gold Inc. ( ARNGF ) and Marathon Gold Corporation ( MGDPF ) seeing significant share dilution, while Iamgold Corporation ( IAG ) ended up divesting half its portfolio to ensure it can complete its share of Cote.

On the positive side, NovaGold (NG) isn't building Donlin currently and its balance sheet has allowed it to avoid share dilution, unlike other developers that have seen their share counts rise by upwards of 20% since 2021 in many cases. On the negative side, delivering the project as intended in the 2021 Technical Report [TR] is looking like a pipe dream, with the upfront capital costs estimated using Q1 2020 pricing and the industry seeing upwards of 25% inflation for greenfields projects since 2020 plus material increases to sustaining capital. At the same time, cost of capital has risen, suggesting that the project just became a lot more expensive for Barrick Gold Corporation ( GOLD ) and NovaGold, assuming it's built how envisioned in the 2021 TR. Let's take a closer look below:

Recent Progress

NovaGold and Barrick embarked on the most aggressive drill program in a decade at the Alaskan Donlin Project last year, with a 42,300 meter drill program that aimed to better understand the geological model through tighter spacing. The results of the program were exceptional, with NovaGold (50% interest in Donlin) reporting world-class intercepts from the project, with many rivaling or even beating the best intercepts out of any project or mine within NGM LLC's joint-venture in Nevada, including Turquoise Ridge Underground, the Carlin Complex and surrounding satellite opportunities and the Cortez Complex + Goldrush/Fourmile.

For NovaGold to be reporting drill results of the same caliber as a joint-venture with a production profile of 3.0+ million ounces of gold run by two $30+ billion dollar companies is quite impressive, and some highlights were as follows:

- 42.28 meters at 30.68 grams per tonne of gold

- 48.96 meters at 20.61 grams per tonne of gold

- 52.57 meters at 14.63 grams per tonne of gold

- 60.96 meters at 12.35 grams per tonne of gold

- 19.74 meters at 34.17 grams per tonne of gold

It's worth noting that while these results are helped to confirm the continuity and increase confidence in the ~39.0 million ounce resource base (100% basis) at Donlin, the drilling has continued to focus on just a 3-kilometer strike relative to the total 8-kilometer strike in the vicinity of current reserves, and drilling has been concentrated on an area that represents just 5% of the project. Hence, there is the possibility of uncovering another mini-Donlin on this property, and the company has already seen exploration success in historic drilling at other greenfield targets like Snow, Quartz, Far Side, and Dome, with highlight intercepts of 61.0 meters at 3.30 grams per tonne of gold (Dome) and 15.6 meters at 5.86 grams per tonne of gold (Far Side).

Overall, these drill results are very encouraging and continue to de-risk what could ultimately be a mine that is larger than the Cortez Complex in Nevada on an annual production basis and comes in just behind the massive Carlin Complex, the #1 complex by output on the famous Carlin Trend, owned by Newmont Corporation ( NEM ) and Barrick. In fact, in the first five years under the 2021 TR (53,500 tonne per day throughput rate and average recoveries of 89.8%), Donlin would produce 1.46 million ounces on average in its first five years, making this larger than two of Canada's largest mines combined: Detour Lake and Canadian Malartic.

That said, while the drilling results continue to confirm that the gold is there and where expected at Donlin, the major negative development is that costs to build this project have risen considerably when we factor in the inflationary pressures that have wreaked havoc on margins and cost estimates for growth projects sector-wide. This doesn't mean that the project won't get built eventually, but those NovaGold investors hoping for commercial production by 2030 or earlier are likely to be disappointed. In addition, Barrick clearly stated in its most recent Investor Day Presentation that the project does not meet its investment criteria yet based on what has been done in the past.

Capex Estimates Not Conservative Enough

When it comes to putting the Donlin Project into production, it won't be cheap, and there are several reasons for its gargantuan capex bill that rivals early estimates for Barrick's Reko Diq Project in Pakistan. For starters, autoclaves are one of the most capital-intensive plants to build and operate, and this is a massive operation with a planned throughput rate of 53,500 tonnes per day. Second, the current development scenario envisions building a 44-kilometer access road, an airstrip, and a 14 inch and 507-kilometer long natural gas pipeline to the site from the west end of the Beluga Gas Field (53 kilometers west of Anchorage). Finally, a project of this size will require a massive waste rock and tailings storage facility, with costs for tailings management, processing facilities, site preparation/roads, and mining alone projected at ~$2.27 billion.

{kind=link}

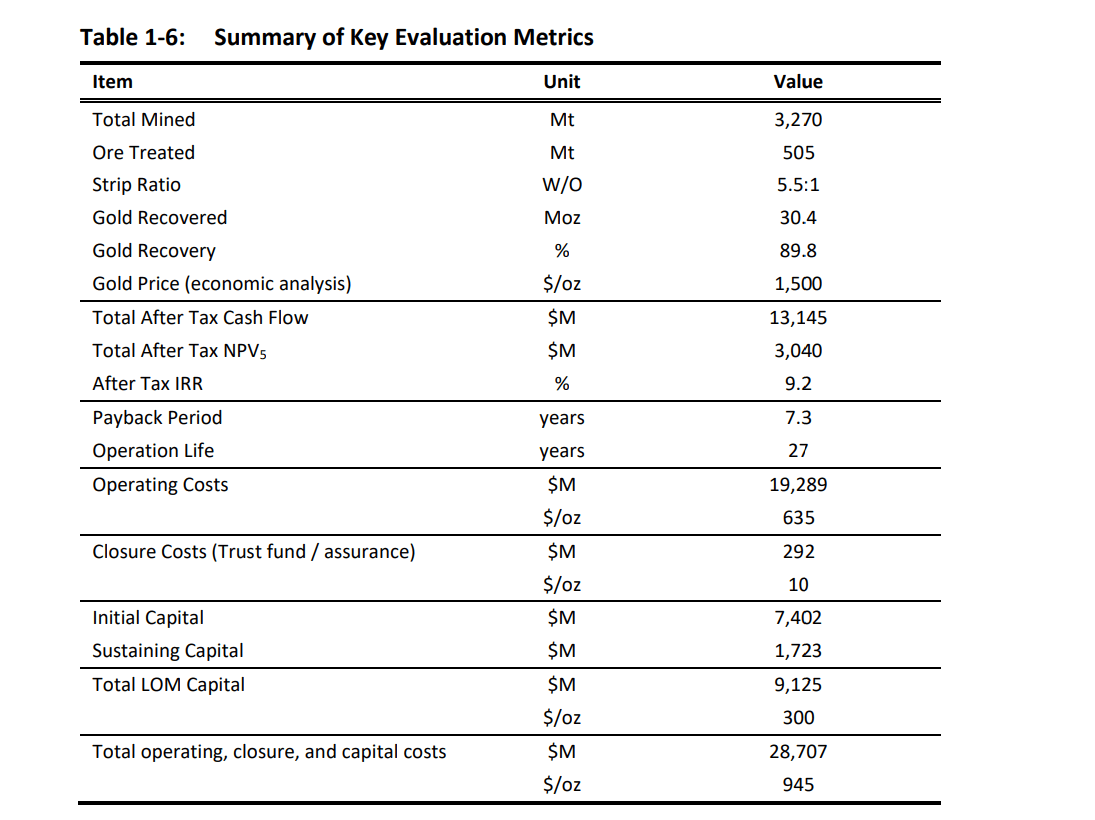

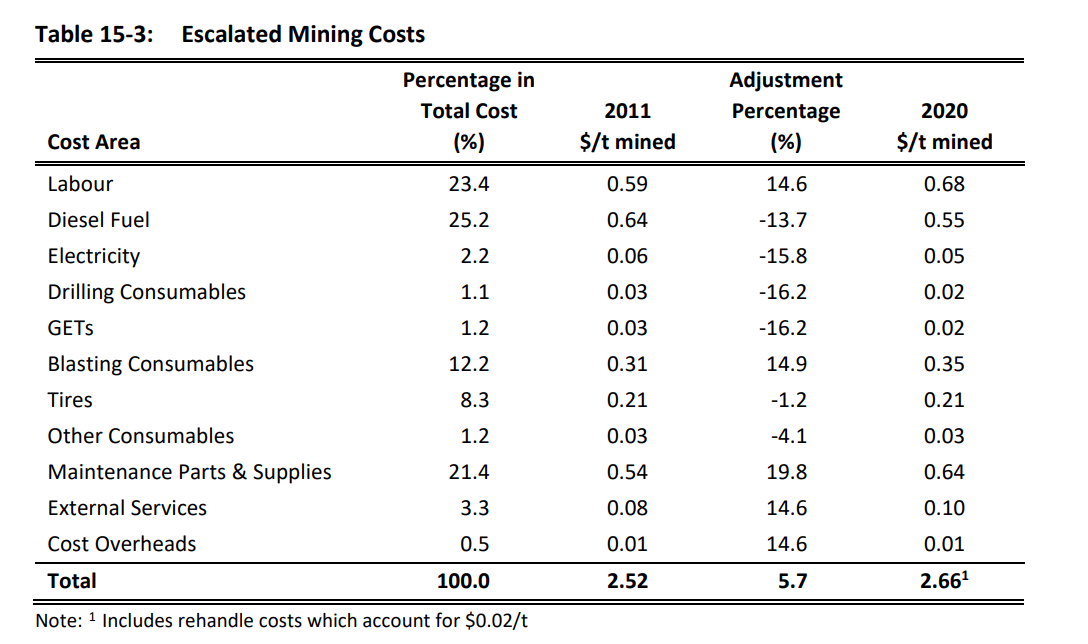

As the table below shows, upfront capex was estimated at ~$7.4 billion per the Q2 2021 Technical Report, but this was based on Q1 2020 pricing, meaning that these estimates did not incorporate any inflation over the past three years. The Technical Report also states that the construction schedule for the tailings storage facility [TSF] and the lower contact water dam [CWD] is aggressive, with the potential for weather delays to affect the schedule. So, given the inclement weather and the remoteness of the project plus the sheer scale, one could argue that this is a project prone to a capex blowout if things don't run very smoothly.

{kind=link}

Given that there's just a 17.7% contingency, no impact of inflationary pressures baked in (Q1 2020 pricing), and very stale estimates for diesel costs ($0.69/liter) and other consumables (lime, cyanide, labor) given the inflation we've seen since Q1 2020, I would argue that mining costs and capital costs are far too low for this project, suggesting a safer bet on actual upfront capex might be $9.0+ billion assuming constant assumptions for scale and plans to power the project from the 2021 TR but with today's pricing. The scary figure is that even at a $1,900/oz gold price assumption, the payback period on this (assuming zero cost creep which is an unreasonable assumption) is 5.5 years with a 13.2% IRR.

As noted in the 2021 TR :

"an estimated West Texas Intermediate fuel guidance price of $65.00 per barrel was used, as provided by Donlin Gold LLC. Based on this calculation, the price of diesel for the Project was set $0.69/L, including delivery costs but excluding any taxes."

Donlin Project 2021 TR - Mining Costs (2021 Technical Report)

{kind=link}

As those that follow Barrick might know, the company is looking for a minimum 15% IRR for new projects, and some investors might argue that a $2,150/oz gold price would fix this issue and push Donlin above the 15% IRR level required by Barrick even if we incorporate higher costs to build the project. However, the key point NovaGold investors might be missing in this equation is that Barrick is looking for Tier-1 gold projects (capable of producing 500,000 ounces in the lower end of the cost curve with 10+ year mine lives) that not only have at least a 15% IRR, but this IRR is based on its long-term gold reserve price assumptions of $1,300/oz .

Even if we assume Barrick's long-term gold price assumption increases to $1,500/oz by 2028, the Donlin Project's IRR at this level is 9.2%, and once again, that assumes that a miracle in which this project is built at the intended scale in the 2021 TR on budget, which I would argue is impossible given inflationary pressures we've seen. So, I don't believe the recent gold price strength changes anything for NovaGold, given that Barrick is now making decisions for growth projects on spot prices, it's using long-term gold price assumptions that have typically been a minimum of 30% below spot gold prices to bake in conservatism in its mine plans and capital allocation decisions. When looking at Barrick's framework, it's not surprising it made the following comments in its 2022 Investor Day when asked about Donlin:

"Right now, on the basis of what has been done in the past (Donlin) doesn't fit our investment criteria. But as we know, all of us here in the gold industry, this changes, and this is a significant deposit, it's real, it is double refractory, so it needs autoclaves. We are busy doing the test work, because maybe we could vary that flow sheet. This next year we'll re-model and then be able to do a preliminary assessment of mining shapes, the minimum mining block size, which will set the foundation for the whole revisitation of the project.

At the same time, we will continue some evaluation and trade-offs next year, and one of the big ones is power and how we manage power to the mine. Right now the capital tag on this thing is significant, and we think it's appropriate that we revisit that. But we can't revisit it in any detail until we've got the mining plan sorted out. So, that's the basis at which we've been working... At this stage, it's got a way to go before it would fit Barrick's portfolio."

- Mark Bristow, Barrick Gold CEO, Barrick 2022 Investor Day.

So, What's The Good News?

For starters, NovaGold has ~$150 million in cash including money set to be received from Newmont this year and a budget of $31 million for 2023, suggesting it can continue to fund its half of Donlin Project expenditures without equity raises until at least year-end 2025. Secondly, NovaGold and Barrick are looking at how they can tinker with the project in the form of trade-off studies to make it more robust and hopefully less expensive at the onset. This includes the potential to optimize the mining fleet to maximize grades, in addition to potentially looking at other power options. There's also the possibility of a phased approach.

While these are positives and the incredible grades in recent drilling suggest the possibility to enjoy even higher grades in the early years of the mine life, these optimizations may unfortunately be partially offset by an additional $2.0+ billion in upfront capex from inflationary pressures. So, while the project may have had a chance at coming in at a sub $5.0 billion upfront cost (100% basis) with a staged approach using Q1-2020 pricing, I'm less optimistic when factoring in high double-digit inflation vs. 2020 levels and up to 40% inflation for some greenfield projects in North America. Hence, even with a staged approach, I still see this as a $5.0+ billion build which is a major decision for Barrick on a 50% basis when it has less complex projects elsewhere in its portfolio, and some that leverage off existing infrastructure like Fourmile.

So, with the impact of inflation, the fact that Barrick's priority is Reko Diq and NovaGold can't build this alone, the fact that an updated Feasibility Study likely won't be delivered until at least H2 2024 and that this is a multi-year build, I see a very low likelihood of first gold pour by 2030, meaning that NovaGold investors will have to be patient for at least another seven years before NovaGold graduates to producer status. Let's look at NovaGold's valuation to see whether this timeline is baked into the stock and how it's valued relative to other developers and producers.

Valuation

Based on ~345 million fully diluted shares and a share price of US$5.93, NovaGold currently trades at a market cap of ~$2.05 billion. At first glance, this might seem like a very attractive valuation with the stock valued at just $121.30/oz on attributable reserves when we've seen other companies scooped up for well over $200.00/oz on reserves, such as Pretium by Newcrest Mining Limited ( NCMGF ), and Detour Gold by Kirkland Lake. However, the major difference here is that these are mines that have their massive capex bills behind them, they're generating free cash flow from day one, and they aren't sitting in the middle of nowhere in Alaska, over 450 kilometers west of Anchorage. So, while valuing NovaGold on a per ounce basis relative to past acquisitions might suggest fair value is much higher, I would disagree with this valuation method given that these are hardly apples vs. apples comparisons

For those unfamiliar, Pretium's Brucejack and Detour's Detour Lake Mine are currently in production and producing ~400,000 to ~750,000 ounces per annum, while NovaGold's Donlin (50%) Project still has no concrete date for construction start and no guarantee the project will get built this decade).

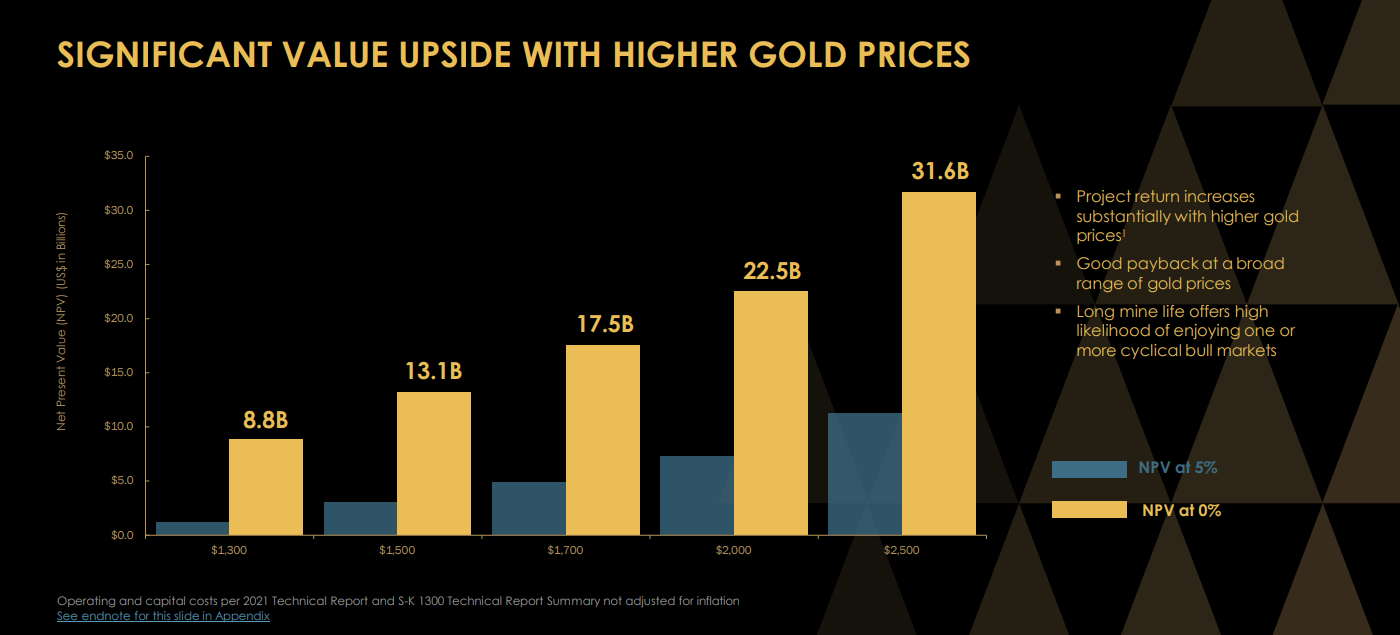

Donlin Gold Project - NPV (0%) and NPV (5%) - 100% Basis (Company Presentation)

{kind=link}

Moving over to valuing the stock on a P/NAV standpoint, NovaGold highlights its Donlin Project economics at a 0% and 5% discount rate, with the choice of a 0% discount rate option being surprising given that the cost of capital for most companies is well above 6% (even if we envision a more relaxed interest rate environment). I would argue that even a 5.0% discount rate is too low regardless of the project's location in a top mining jurisdiction, but it is the industry standard. To offset the lower discount rate but still maintain an apples to apples comparison, I prefer to use a conservative gold price assumption and I typically use the 3-year moving average (currently at $1,800/oz).

{kind=link}

Given that Donlin is a post-2029 opportunity, one could argue that even $1,900/oz is conservative if we assume a minimum 2% increase in the gold price per year and a base case price of $1,700/oz. By applying an average $1,900/oz gold price assumption over the mine life and using a 5% discount rate, NovaGold's Donlin Project has an After-Tax NPV of $6.45 billion. However, we must divide this figure by two in order to account for its 50% interest ($6.46 billion x 0.50 = ~$3.23 billion) and I believe a minimum 20% discount should be applied to this figure to account for the study being stale and using 2020 pricing which was ahead of three years of near unprecedented inflation. This places the value of NovaGold's interest in Donlin at ~$2.58 billion.

If we compare this figure to NovaGold's current market cap of ~$2.05 billion, some investors might assume that NovaGold is a steal at a share price of US$5.93. However, it's quite rare for developers to trade at even 0.80x P/NAV given that they are riskier than producers and there's no guarantee that their project ever goes into production (let alone 1.0x P/NAV), even if their partner on a project is Barrick. So, even if we use a fair value of 0.90x P/NPV, which is above the high end of the range for developers and above that of some producers like Orla Mining Ltd. ( ORLA ), Eldorado Gold Corporation ( EGO ), and i-80 Gold Corp. ( IAUX ) at 0.80x, 0.85x and 0.55x P/NAV, respectively, this would place a fair value on NovaGold of $2.32 billion [$2.58 billion x 0.90], or US$6.72 per share.

{kind=link}

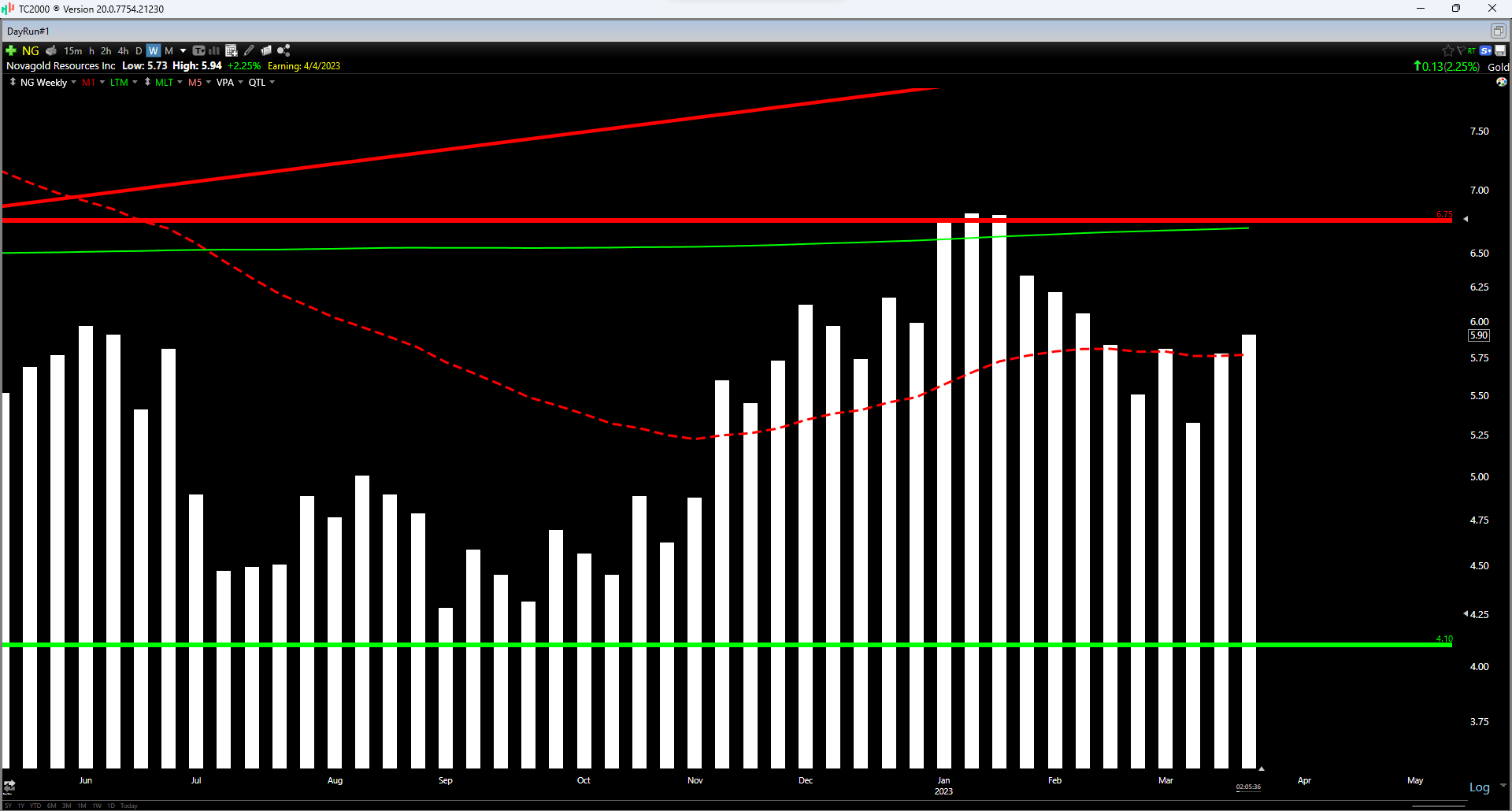

Although this points to a 14% upside from current levels, I'm looking for a minimum 40% discount to fair value to justify buying non-cash flowing developers given that they are typically more volatile and carry higher much risk (they're not yet fully permitted, they're not yet fully financed, we haven't seen how the actual operation reconciles to the mine plan, and cost overruns have become the new normal, potentially leading to additional share dilution during the construction/ramp-up stage). After applying this required discount of 40%, the ideal buy zone for NovaGold comes in at US$4.05 per share, suggesting that the stock is nowhere near a low-risk buy zone currently. The technical picture corroborates this view, with NG trading in the upper portion of its support/resistance range (US$4.10 to US$6.75).

Summary

While several gold producers have a lot to be excited about over the past week, as they might benefit from selling some ounces at or above $1,970/oz, NovaGold Resources Inc. has little to celebrate. This is because today's, this week's, and this year's gold prices mean little for the company given that it will not be in production for at least another five years, and likely much longer. In fact, I would be shocked if Donlin was in commercial production by 2030, and in the period that NovaGold is not generating free cash flow, other producers will gush free cash flow, including those like Barrick that have the same interest in Donlin as NovaGold (50%).

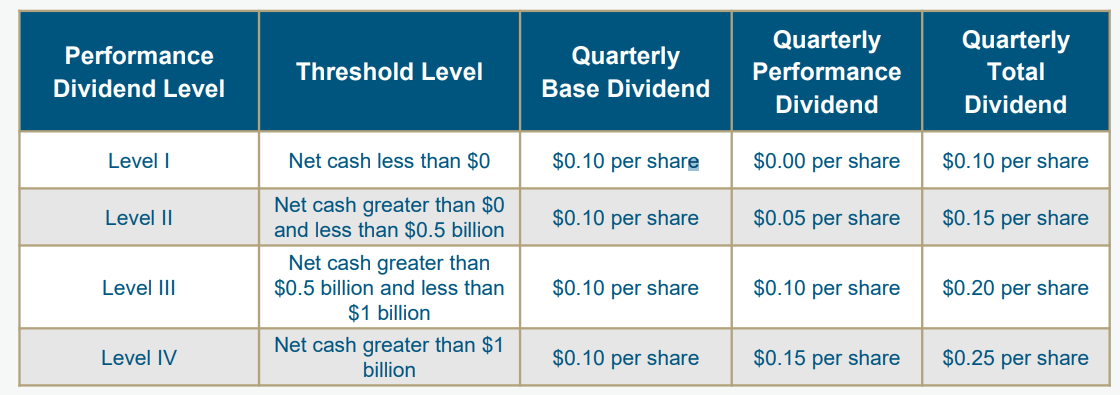

Barrick - Quarterly & Performance Based Dividend (Barrick Presentation)

{kind=link}

So, while some investors might not be able to imagine parting with their NovaGold stake if they're enamored with the quality of the massive Donlin Project, an alternative way to get exposure to this asset is Barrick Gold. Not only do they get the same exposure, but with a declining share count (Barrick is actively buying back shares), but they have the benefit of being paid to wait for the eventual autoclave startup at Donlin given that Barrick could return well over 5% this year to shareholders through dividends (Level III/Level IV mix) and its share buyback program. Plus, investors get exposure to copper, a commodity with an even more attractive supply/demand picture than gold.

To summarize, I continue to see NovaGold as a less attractive to play the sector, with better options being Barrick among large caps and i-80 Gold among small-caps.

For further details see:

NovaGold: Limited Margin Of Safety At Current Levels