USO - November CPI: Disinflation On Track With More Downside Into 2024

2023-12-12 12:15:23 ET

Summary

- The November CPI Summary showed the annual inflation rate fell to 3.1% from 3.2% last month.

- The data confirms consumer prices continue to stabilize lower, confirming the success in the Fed's strategy to engineer a soft landing while the economy remains resilient.

- Room for shelter and used car prices to fall heading into 2024 points to room for the CPI to trend lower going forward.

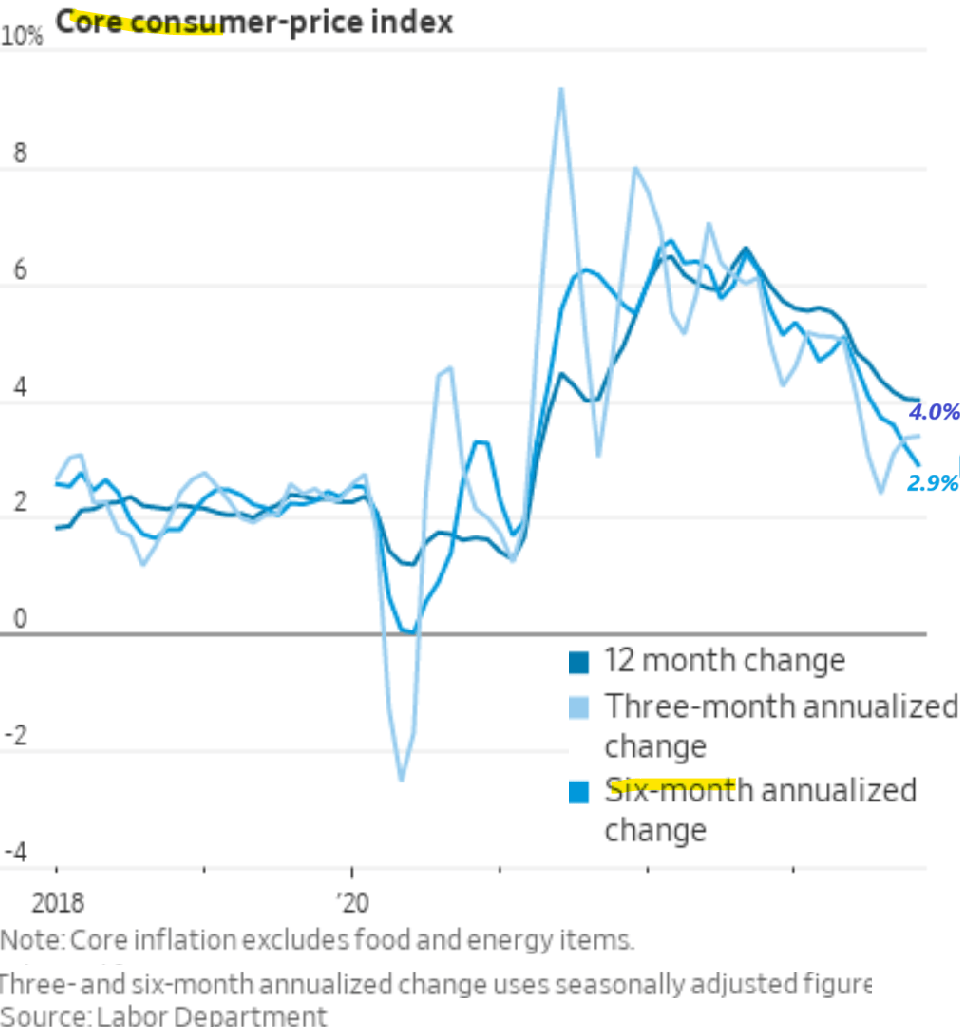

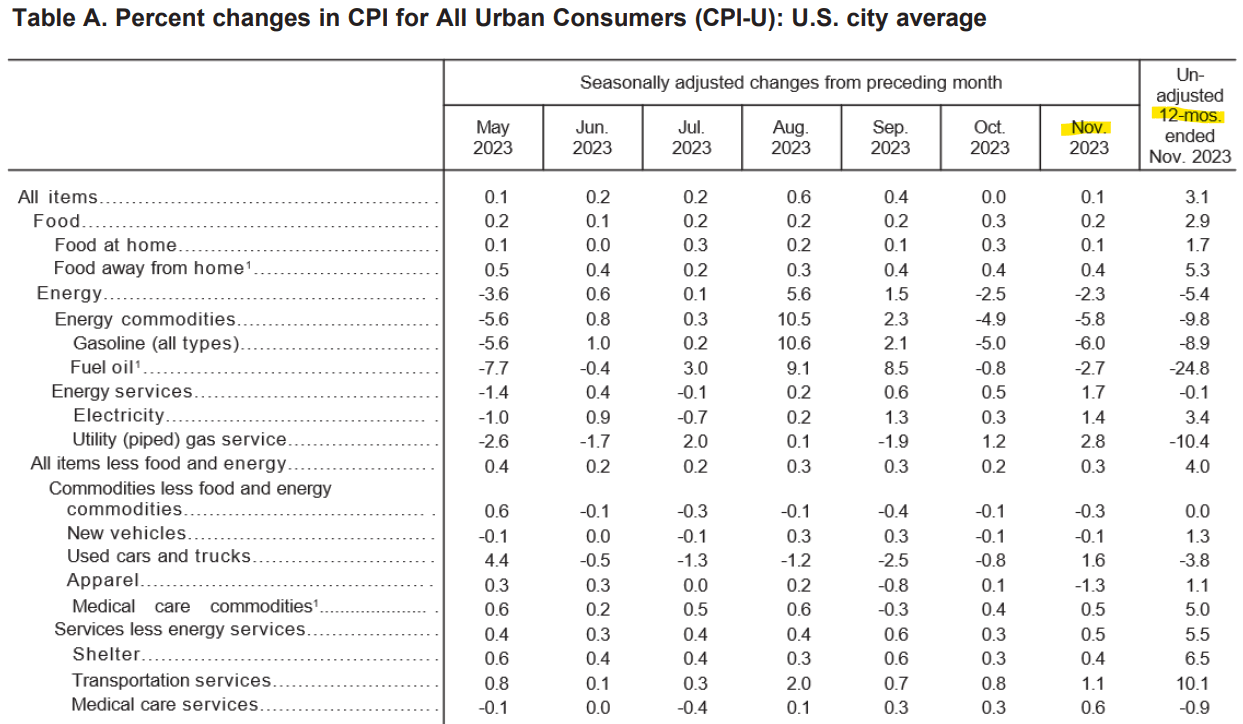

The November Consumer Price Index Summary came in largely at the consensus, climbing by 0.1% on the month helping the headline inflation rate tick lower to 3.1% from 3.2% in October. The Core CPI, which excludes food and energy, climbed by 0.3% month-over-month, leaving the annual core rate flat at 4%.

We can dissect the numbers in countless ways, but our initial take is that the report wasn't as "great" as the October update, which came in below expectations, but was good enough here to advance the narrative that disinflation is ongoing.

The CPI ending the year right around 3% is a night and day difference compared to the cycle peak of 9.1% in June 2022, and even significantly lower compared to 6.5% at the start of 2023. The Fed is using this report as its final big data point ahead of the December FOMC, and we believe they can take solace that inflation trends have progressed favorably.

It's the details that matter, and trends like the 6-month annualized core-CPI already under 3% point to further improvements going forward. Inflation at the end of 2023 is no longer a "problem," and that's a good thing for businesses and consumers.

{kind=link}

The November CPI Details

A major theme in pushing the CPI lower this year has been the decline in energy prices. That trend continued in November, with energy posting a -2.3% m/m decline and lower by -5.4% annually.

This has been particularly encouraging considering the setup going back to the late summer, and even early October when the Israel-Hamas war added to concerns that oil would break out higher and add inflationary pressures.

By this measure, the turn of events with the current price of a barrel of crude oil (CL1:COM) down more than -25% from its September peak, and even the retail price of gasoline in the United States to around $3.00 a gallon, has been a welcomed development.

Even as energy services prices jumped higher in the month at +1.7%, the understanding is that weak energy trends could keep this area covering electricity rates and utility gas price increases limited from here.

The bigger picture considers a more widespread trend in stabilizing prices across most categories. Food climbing just 0.2% m/m at a 2.9% annual rate includes the food at home category up just 1.7% y/y. A combination of the impact of higher interest rates and shifting economic conditions has helped contain the overall rise in prices.

What we've seen is that compared to 2022, when producers were rushing to hike prices as a response to higher input costs, the prices for all types of goods overall have stopped climbing. Within the core-CPI apparel, prices fell by 1.3% in November, likely reflecting an effort by retailers to discount inventory.

source: Bureau of Labor Statistics

{kind=link}

Going through the CPI report, one area of concern would be transportation services, which climbed by 1.1% m/m and are up 10.1% for the year. Digging into that figure, motor vehicle insurance up 19.2% y/y has driven the bulk of the increases corresponding to a wider trend of elevated insurance prices.

At the same time, it's important to recognize that there are always many moving parts to the CPI with some items presenting more favorable trends than others. That's normal. We can also connect the dots to make some assumptions about where trends are going.

More Downside To Core-CPI Into 2024

Maybe the biggest "surprise" in the November inflation data was the curious jump in used car prices, up +1.6% m/m, the first increase since May. The reason this one is a head-scratcher is that all indications are that vehicle prices are declining.

The evidence points to the automobile industry in an ongoing normalization between climbing production of new cars, growing dealer inventory levels, and cooling demand compared to the pandemic era of supply chain shortages.

The industry group Cox Automotive throughout the " Manheim Used Vehicle Value Index " notes that prices fell by -2.1% m/m in November according to their tracking. The annual decline they are seeing at -5.8% y/y is at a spread compared to -3.8% CPI measured just -3.8% lower. Similarly, the separate " CarGurus used car price index " shows a 1.4% decline over the last 30 days.

The read is that this critical core CPI category of vehicle prices has room to converge to more real-time market indicators over the next several months.

{kind=link}

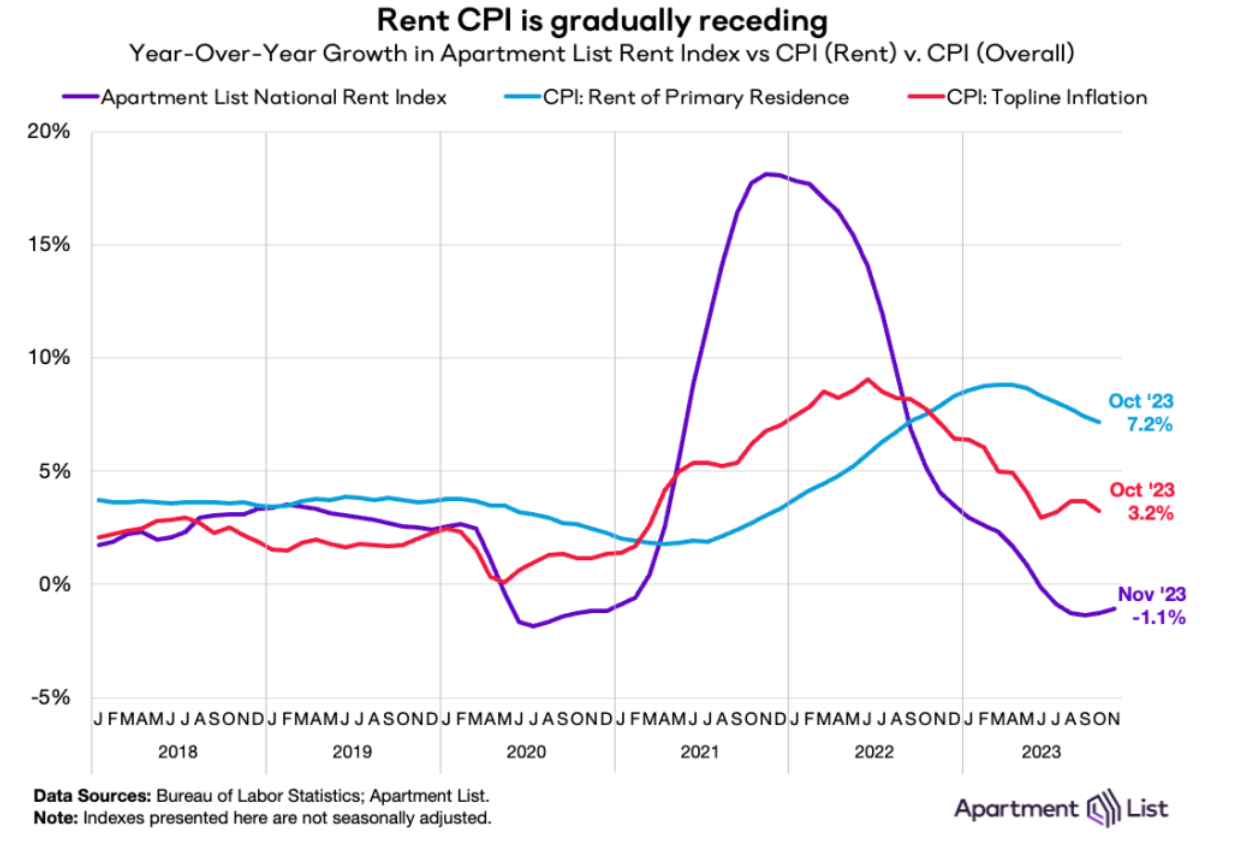

That's also the case when we think about CPI Shelter, which shows a +6.5% annual increase as a benchmark for the "housing market." In this case, the spread that we can focus on is indicators like the Case-Shiller , where the price trend is at a more moderate +3.9% y/y with data from September.

Other references include residential home rental prices that are even presenting a decline with a negative annual rate. The latest November update for the "CPI rent of primary residence" component showed a 6.9% annual rate, down from 7.2% in October but still dislocated from market trends.

Our interpretation is that there is a time lag in the BLS data that can play out over several months but ultimately correct lower, helping to push core and the headline CPI toward the official Fed target of 2% over time.

{kind=link}

Inflation Outlook Into 2024

We believe enough components are trending toward the 2% annual rate presenting an overall good backdrop. From a high-level perspective, there just isn't any indication that consumer prices are "re-accelerating" or that the decline in the headline CPI has stalled.

Already thinking about how inflation is evolving into December, keep in mind that oil prices are currently down about 9% this month. This will have the effect of keeping the headline CPI contained, likely tracking under 3% into the early part of 2024.

{kind=link}

With that, the key here is that we get the stubborn areas including shelter and even transportation services to make a more convincing correction that will help drive inflation expectations lower.

On this point, consumer inflation expectations for the year ahead were last reported at 3.4% compared to 3.6% in October. Over the past year, this survey-based indicator has typically lagged the official CPI data.

We sense that as oil and gas prices fall, which is often the most visible variable spending component for consumers, there is room for inflation expectations to continue declining. The Fed is likely considering all of these details when it thinks about the next steps in monetary policy, opening the door for interest rate cuts by next year.

{kind=link}

Final Thoughts

The latest inflation update confirmed that trends are moving in the right direction with impressive progress made over the last several months. In many ways, the gradual process for the CPI to reach the 2% Fed target is a better outcome compared to some sharp deflationary outcome that would represent a more concerning signal towards the strength of the economy.

Considering data suggesting a resilient labor market with positive job gains and positive economic growth, what we have here is evidence that the Fed has been successful in guiding the economy toward a soft landing. Investors should be cheering for this scenario, and it appears the market's approval is reflected in strong stock market gains this year pointing to a positive macro outlook.

For further details see:

November CPI: Disinflation On Track With More Downside Into 2024