CA - Numinus Wellness Q2 Results: Urgent Action Required

2023-04-17 05:08:55 ET

Summary

- Numinus announced 2Q23 results that did little to ease investor concerns regarding the rate of cash burn.

- The company says that it has sufficient working capital to continue for the next twelve months, but this appears somewhat optimistic.

- Numinus has introduced several new initiatives, including training courses and a clinic licensing scheme, but these projects are unlikely to solve the near-term cash flow problem.

- Although Numinus is one of the stronger players in the psychedelics sector, the stock remains a Sell.

Introduction

Numinus Wellness ( NUMI:CA ) reported 2Q23 results on 13 April 2023. The market was not impressed with the company's update, with NUMI's share price subsequently falling by around 7% to close at CA$0.19 on 14 April 2023. NUMI's share price has now fallen by ~60% over the last twelve months. In this note I take a look at interesting issues raised in the 2Q23 materials and consider whether or not the share price fall has captured enough downside to warrant a review of my January 2023 Sell rating (I note that NUMI's share price has fallen by ~33% since that Sell call).

Survival Of The Fittest?

In his opening comments, prior to discussing the 2Q23 quarterly result, CEO Payton Nyquvest referenced the failure/closure of players within and adjacent to the markets that Numinus operates in. Nyquvest points to competitor closures as being an opportunity for NUMI to grow patient numbers.

So while dynamics in our sector are changing and that volatility has impacted sector wide stock performance, in the long term, recent changes to the competitive landscape should affect -- should actually benefit Numinus. And we're ready to take -- we're already taking the initiative to grow our market and our client relationships in regions where our competitors have closed down operations. We're happy to be able to step in wherever possible to allow patients to continue with their important mental health treatments.

Source: NUMI 2Q23 Transcript , Seeking Alpha, page 4.

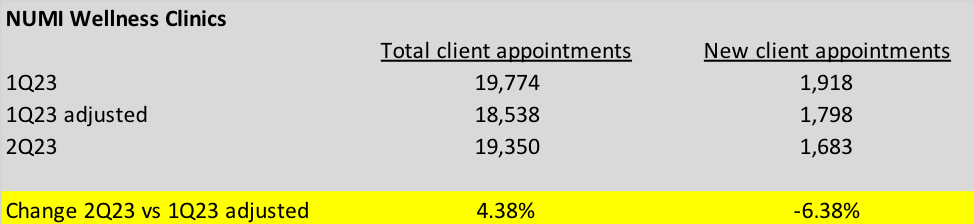

Unfortunately there is no clear evidence as yet that NUMI is actually picking up a material volume of new patients due to other groups and clinics closing. 2Q23 revenues from the Numinus clinic network fell by 9.9% relative to 1Q23; part of the decline is due to seasonality (fewer operating days in 2Q) but I would have expected a much stronger outcome if NUMI was suddenly seeing a wave of new clients coming in through clinic doors. Exhibit 1 looks at NUMI's wellness clinic appointment data for 1Q23 and 2Q23 (as per the MD&A reports). The '1Q23 adjusted' data (my calculation) provides for a fairer view of trends by adjusting the 1Q23 appointment data downward to align with the 6.25% fewer operating days in 2Q23. This simple analysis shows that appointments for new clients actually fell (on an apples with apples basis) by ~6.4% in 2Q23 relative to the 1Q23 run-rate.

Exhibit 1:

Source: analyst's calculations based on NUMI MD&A reports.

{kind=link}

The recent failure of Ketamine Wellness Centers and Field Trip suggests that the 'wellness clinics' space is heavily over-supplied. It may well be the case that this supply-demand imbalance will take quite a long time to correct; a rapid near-term improvement in clinic economics sounds like an optimistic scenario to me.

Diversifying Income Streams

NUMI's business model is rapidly evolving. In my previous Seeking Alpha NUMI note, I referenced NUMI's September 2022 announcement that the company had partnered with medical finance provider iFinance in a bid to generate new income streams through sales commissions. NUMI accelerated its efforts to expand existing offerings and also bring in new revenue streams in 2Q23; I briefly summarize and discuss these initiatives below:

- February 2023 - NUMI added a third US Cedar Clinical Research clinical research site in Phoenix, Arizona. The group now operates five clinical research sites in total.

- March 2023 - launch of psychedelic-assisted therapy ('PAT') training courses, under the Numinus Certification Pathway banner. NUMI is something of a late entrant to the PAT training space - which is already rather crowded - however the group's well-known brand name may be an asset in terms of attracting aspiring PAT practitioners. The recent high-profile failure of Synthesis Institute indicates that making money in the training space can be challenging (see Lucid News for a detailed article on the Synthesis blow-up , written by Josh Hardman, founder of Psychedelic Alpha ).

- April 2023 - NUMI announces the launch of a Numinus Network branded wellness clinic licensing platform. NUMI aims to generate monthly license fees by providing clinic owners with therapy protocols, administrative services and marketing support. In addition, NUMI will offer license holders the option to lease a turnkey Numinus Wellness clinic via a partnership with Healing Commercial Real Estate Inc ; I assume that NUMI will receive a commission or revenue share for any leases arranged through the Healing Commercial Real Estate Inc offer.

- April 2023 - NUMI announces the launch of a new website featuring enhanced navigation for clients seeking mental wellness services. This is part of an ongoing investment in the group's digital service platform.

Ordinarily I would be quite supportive of a company strategy that seeks to diversify income streams by moving into adjacent markets. That said, I'm struggling to see the training and licensing offers making much traction, and both come with risks that need to be considered in conjunction with the revenue opportunities. However, the bigger issue here is one of timing - I'm far from convinced that it currently makes sense for NUMI to be spending cash building out these new offers and distracting management from the core operations. Read on for an explanation as to why I believe that NUMI should be in cash preservation mode rather than service expansion mode.

Capital Injection - Not If, But When

NUMI's balance sheet cash ended FY22 at CA$33.044m. By the end of 2Q23, the cash balance had fallen to CA$19.707m, a drop of -CA$13.377m, or roughly -CA$6.7m per quarter. Operating cash flow (cash used in operating activities) was -CA$7.102m in 1Q23 and -CA$6.044m in 2Q23. I conclude that a reasonable estimate of NUMI's quarterly cash outflow run rate is around -CA$6.5m. With that in mind, have a read of the following extract from NUMI's 2Q23 MD&A report:

As at February 28, 2023, the Company had cash and cash equivalents of $19,706,862. Management estimates that the Company has sufficient working capital to continue operations for the next twelve months.

Source: NUMI 2Q23 MD&A , page 8.

Effectively, NUMI is saying that they expect to burn through less than CA$19.707m of cash in the next twelve months - this is equivalent to a quarterly cash outflow rate of no worse than -CA$4.927m, which is some 24% better than the -CA$6.5m quarterly outflow run rate as per the simple analysis above. Put another way, if NUMI continues to burn through cash at a rate of -CA$6.5m per quarter, the company's cash pot will run dry after slightly over nine months. Perhaps NUMI's management and board know something significant that I don't, but personally I'd feel very uncomfortable if I was required to state with confidence that NUMI had enough cash to continue operations for the next twelve months. I should also note that in 1Q23, NUMI's cash balance benefitted from ~CA$0.92m of cash inflow relating to the exercise of warrants and options - future cash inflows from warrants and options are highly unlikely given where the share price is trading (~CA$0.19).

Given the precarious financial position that NUMI appears to be in, I'm pretty flummoxed as to why the company has been pushing ahead with the revenue diversification plans discussed above. These initiatives may well be sound, but in the near-term they are likely to be cash flow negative.

Conclusion

In late January 2023, I downgraded NUMI to Sell based mainly on concerns regarding the group's high cash burn rate. In recent weeks, I've taken a look at COMPASS Pathways ( CMPS ) and Cybin Inc. ( CYBN ) and published Sell ratings on both stocks based on cash burn rate concerns. It is becoming increasingly apparent to me that many, and perhaps almost all, of the listed psychedelic stocks will soon be looking to raise capital, and doing so at a time when speculative asset classes (the psychedelics sector is most certainly deserving of the speculative label) are being avoided.

There was nothing in NUMI's 2Q23 materials to shift me from the position that I adopted in January, and if anything I feel more confident that a large capital raise is likely in the coming months.

Of course, there are levers that management and the board can pull to buy NUMI's balance sheet more time. For example, the company is spending ~CA$1.7m per quarter on professional and consulting fees - surely this outgo can be trimmed without hitting the revenue line. Expenses relating to salaries and wages are ~CA$4m per quarter; management may need to make some tough decisions regarding headcount reductions.

NUMI's share price fell by 7% following the 2Q23 release. Investor sentiment toward the stock appears to be heading downhill, which does not bode well for a company that may soon need to come to the market to seek fresh capital. I therefore conclude this review with a continuation of my Sell rating.

For further details see:

Numinus Wellness Q2 Results: Urgent Action Required