CA - Nutrien: Don't Add Now As Its Growth Could Peak In 2022

- Nutrien has benefited from the demand/supply imbalance impacting the fertilizer markets, particularly in Potash. However, NTR lost all its post-conflict gains at its July lows before recovering.

- We posit that NTR stock is likely at a near-term bottom. But, we don't encourage investors to jump on a buy-the-dip opportunity yet.

- We believe a steeper fall could follow after a short-term rally. As a result, investors need to adjust their expectations of potential peak growth cadence in FY22. Remember, the market is forward-looking.

- Our valuation model indicates that Nutrien stock could likely underperform the market through FY26. Therefore, the market is likely demanding higher free cash flow yields to compensate for such risks.

- Therefore, we rate NTR stock as a Hold for now. However, we may be interested in adding if it falls below $60.

Thesis

Leading fertilizer company Nutrien Ltd. ( NTR ) stock has been battered over the past three months after setting up its April highs. The stock gave back all of its gains from the start of the Russia-Ukraine conflict at its July lows as the market digested its unsustainable surge from February to April.

We had also warned investors to be wary in our previous articles on Mosaic ( MOS ) and CF Industries ( CF ) - see here and here . We believe investors could be very confused as the war is still ongoing, and the world could be facing food shortages, exacerbated by the demand/supply imbalance in fertilizers, particularly in potash.

So, why did the market send NTR plunging back to its pre-conflict lows before recovering? Also, is the current bottom sustainable to help NTR recover from here?

Our analysis shows that NTR is likely at a short-term bottom, underpinned by its near-term support. However, we caution investors from adding at the current levels. We believe April's bull trap that led to its steep fall could be the start of a further drop to digest NTR's gains before an eventual bottom is found. Hence, we urge investors not to pull the buy trigger yet.

As such, we rate NTR as a Hold for now.

The Market Sent NTR Tumbling From Its April Highs Despite Its "Cheap" Valuations

We have made many mistakes in our investment and trading journey. One of our key learnings is always to remember that the market is forward-looking. It consistently attempts to price in events/expectations ahead of time.

We believe that the market has turned its focus on other macro headwinds that could impact the growth cadence of Nutrien moving forward. Recessionary risks and risks from surging inflation have driven global governments to focus on tackling challenges in food security.

Still, some investors could argue that NTR was priced at an NTM FCF yield of 11.5% at its April highs, well above its mean of 8.89%. Yet, the market sent NTR falling nearly 40% to its July lows? Did the market get it wrong?

Credit Suisse ( CS ) and Citi ( C ) weighed in, as they were concerned that the industry's best days could be behind us. Credit Suisse warned (edited):

Farm economics and fertilizer profitability are near peak levels. Peak conditions could continue longer than normal, and accelerated capacity will take time to bring online, but valuation for CF Industries and Nutrien will remain low until the cycle eventually bottoms. - Seeking Alpha

Citi also highlighted that " the Fed's aggressive rate hike [will likely] slow the economy." Therefore, we believe the market has markedly adjusted its valuation models to compensate for the risks of holding these stocks.

Investors Should Prepare For Growth Normalization

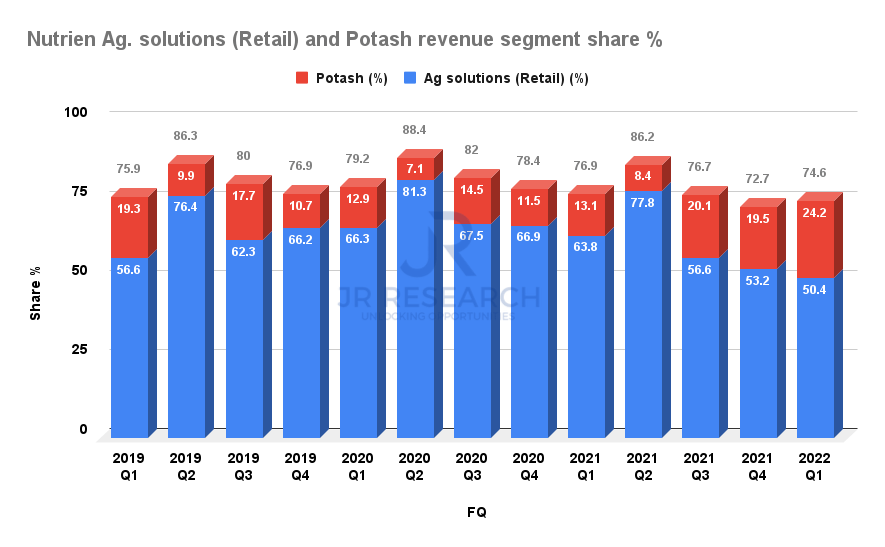

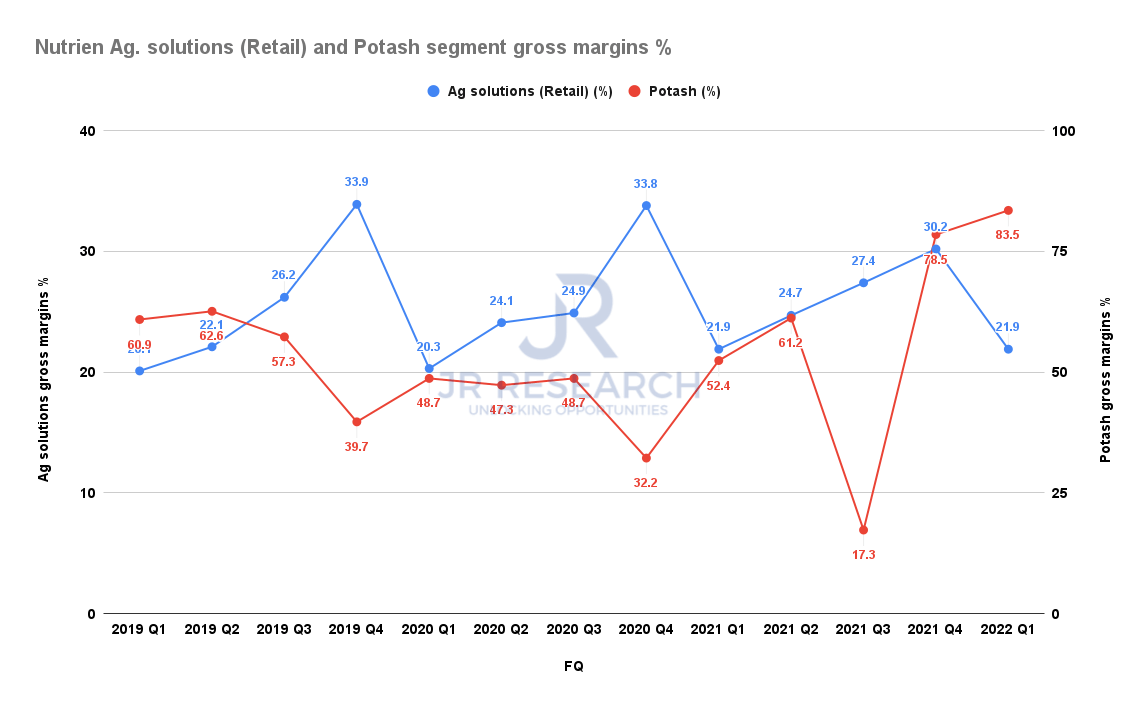

Nutrien ag solutions and potash segment revenue share % (Company filings) Nutrien ag solutions and potash segment gross margins % (Company filings)

{kind=link}

{kind=link}

Nutrien has benefited tremendously from its Potash exposure (24.2% of Q1 revenue) over the last two quarters. The demand/supply dynamics had helped its Potash segment's gross margins surge to 83.5% in FQ1.

But, we think the critical question investors need to deliberate on is whether such gains are expected to continue further?

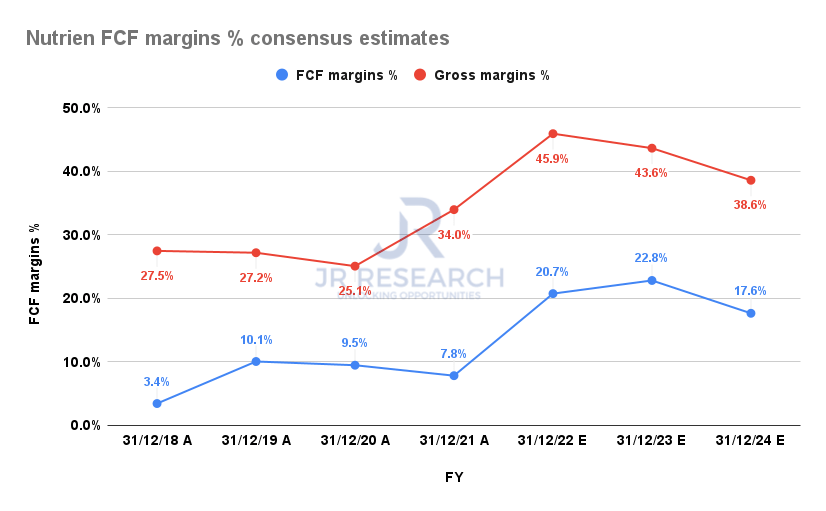

Nutrien gross margins % and FCF margins % consensus estimates (S&P Cap IQ)

{kind=link}

The consensus estimates (bullish) suggest that Nutrien's gross margins are expected to peak in FY22 before falling through FY24. Consequently, its free cash flow ((FCF)) profitability is also likely to be impacted. Notwithstanding, we believe the supply imbalance has likely been reflected in the Street's bullish bias, as they are still projected to be markedly higher than Nutrien's FY21 metrics.

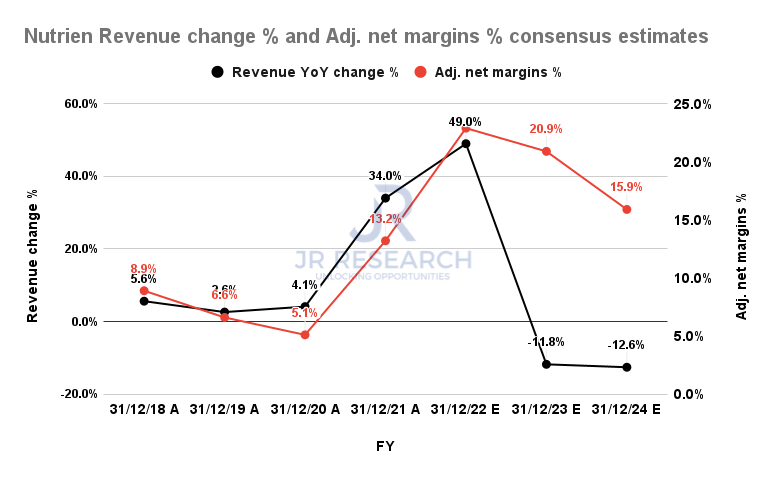

Nutrien revenue change % and adjusted net margins % consensus estimates (S&P Cap IQ)

{kind=link}

Furthermore, Nutrien's revenue growth is expected to decline from FY23, impacting its adjusted net margins markedly. Therefore, we believe that investors need to adjust their valuation models to factor in potential peak growth expectations in FY22.

Nutrien Could Underperform In the Medium Term

| Stock |

| NTR |

| Current market cap |

| $43.18B |

| Hurdle rate [CAGR] |

| 11% |

| Projection through |

| CQ4'26 |

| Required FCF yield in CQ4'26 |

| 10% |

| Assumed TTM FCF margin in CQ4'26 |

| 16% |

| Implied TTM revenue by CQ4'26 |

| $42.9B |

NTR reverse cash flow valuation model. Data source: S&P Cap IQ, author

We applied a market-perform hurdle rate of 11% in our valuation model to assess whether NTR can potentially perform in line with the market moving ahead.

So the critical question is the selection of its FCF yield. We applied a 10% yield based on our assessment of an appropriate level of risk that the market is willing to accept in holding NTR currently. Why?

Note that the market rejected further buying upside decisively in April at an NTM FCF yield of 11.5%. But, if we used its FY24 FCF estimates, the yield would be lowered to 8.44% (in line with its all-time average). Because the market could expect Nutrien to post a decline in its FCF profitability moving ahead, thus impacting its valuation.

Consequently, we require Nutrien to deliver a TTM revenue of $42.9B by CQ4'26. However, based on the revised consensus estimates, Nutrien could disappoint, given the falling revenue growth cadence.

As a result, we believe the market has been adjusting its yield requirements for a lower implied hurdle rate. It suggests the market could expect NTR to underperform in the medium-term through FY26.

Is NTR Stock A Buy, Sell, Or Hold?

We rate NTR as a Hold for now.

We believe the market has adjusted its expectations on NTR, focusing on worsening macro headwinds and potential peak growth cadence.

Our valuation model indicates that NTR could underperform the market through FY26.

Notwithstanding, we believe NTR is likely at a near-term bottom. Therefore, a short-term rally could follow, but we do not encourage investors to add at the current levels.

Instead, we may find NTR interesting if it can retrace further to levels below $60 (another 23% downside).

For further details see:

Nutrien: Don't Add Now As Its Growth Could Peak In 2022