CA - NuVista Energy: Not Getting Slapped For Growth

Summary

- NuVista is a Montney producer with roughly 1/3 liquids and 2/3 natural gas production.

- Unlike producers, NuVista is one of the only E&Ps with the investors' blessing to grow.

- NuVista is virtually debt free and pledged to return 75% of free cash flow to shareholders in 2023.

- NVA's virtually debt-free balance sheet and its market diversification strategy provide downside protection.

- There is further upside with some kind of corporate transaction among the smaller Montney players.

Situation Overview

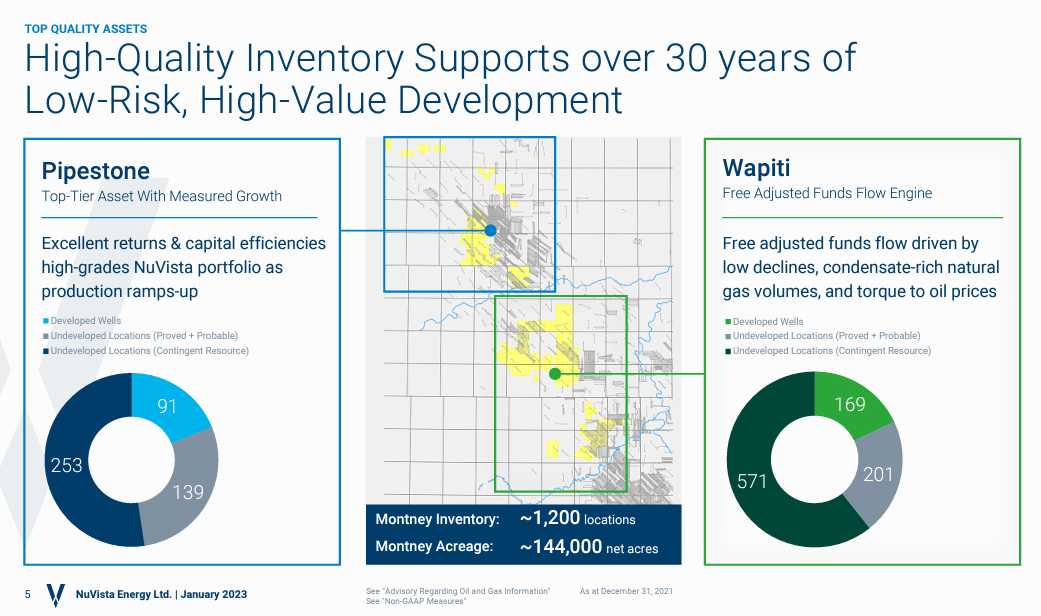

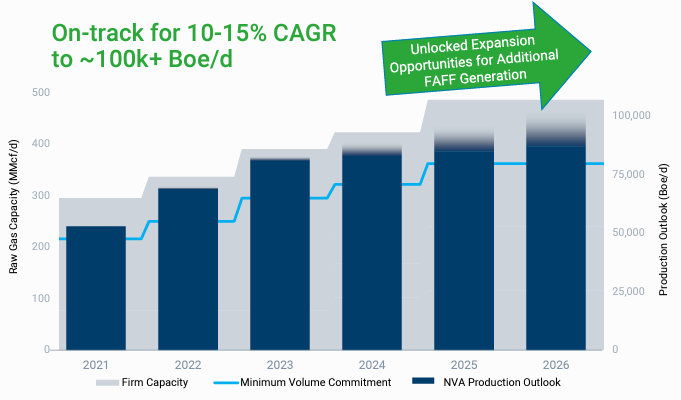

NuVista (NVA:CA) (NUVSF) is a liquid-rich natural gas producer. It exited 2022 with a production rate of ~68.5 kboe/d and is guiding 79-83 kboe/d for 2023. The two areas of focus are the Wapiti and the Pipestone. Wapiti is relatively more mature with a lower decline rate and can generate substantial free cash flow even in a low commodity environment. Pipestone is the growth engine due to its prolific nature of the rocks, making Pipestone more economic to develop. Combined NVA has a complementary portfolio of assets giving NVA a clear line of sight to +100kboe/d production by 2026.

{kind=link}

NVA is unique among the E&P players as it has the blessing of the market to grow production. This is because NVA has already signed up for midstream and downstream capacity to the equivalent of >100 kboe/d. In other words, NVA does not need to invest additional capital to grow production - it just needs to spend the half-cycle capex (drill, complete and tie-in) to fill up the plants and pipelines. For other E&Ps to grow, they will have to spend additional capex in processing and takeaway capacity to accommodate the volume growth.

{kind=link}

NVA carried over $600 million of debt into the 2020 energy downturn and fought very hard in order to survive. NVA has dramatically reduced the absolute value of debt over the past 2 years and is virtually debt-free. The $200 million net debt target was reached in Q4-2022. The leverage ratio (Net Debt to Cash Flow) can remain below 0.5x at $65 WTI and $3 NYMEX pricing environment.

Company Presentation

Given the supportive commodity pricing environment and a virtually debt-free balance sheet. NVA has pledged to return 75% of the free cash flow to shareholders in 2023. NVA has done a decent job at returning capital to shareholders - it has completed 74% of the stock buyback program (13.5 million shares bought back out of the 18.2 million allowed amount).

Valuation

First thing first, E&P stocks are partial derivatives of the commodity so you need to have a view of the commodity. For my base case, I'm using $3.0 gas and $80 oil. We can debate this in the comment section if you'd like. Using the higher end of the capex guidance ($450 million), I have NVA generating ~$380 million of free cash flow in 2023. This translates to a 15% FCF yield. If NVA is returning 75% of FCF, it means shareholders should expect $285 million of capital return. NVA should be able to pay a 5% dividend and still has $170 million cash to conduct a Substantial Issuer Bid ((SIB)).

To be fair, every decent E&P is trading at a double-digit FCF yield, but the unique thing with NVA is that there is substantial production growth in the near future. If I assume 8% YoY production growth in 2024 and 2025 (which is below the management's target of 10-15% growth) and no operating leverage from expanded production (just to be conservative), I see NVA generating ~$540 million free cash flow or 22% FCF yield. Remember this is at $3.0 gas and $80 oil.

Author's Estimate

M&A Upside?

The number of publicly traded E&Ps in Canada has come down dramatically over the years but there are still plenty of M&A opportunities, at least on paper. NVA's pipestone asset is directly adjacent to Pipestone Energy. NVA's Wapiti asset is right next to Paramount (of which owns ~17% of NVA). Sinopec owns a bunch of land around NVA's Wapiti area that makes sense for NVA to own and develop. Shell also owns some land in the surrounding area. No matter how you look at it, NVA and its neighbors should be able to consolidate to become a larger and more relevant player. The hurdle is that everybody is undervalued at 3-3.5x EV/EBITDA so the merger math might not make sense for all parties. However, there are certainly a lot of advantages with scale - e.g. negotiating with service providers and signing up for long-term supply contracts with LNG exporters or power plants.

Conclusion

Depending on your commodity price assumptions, you could make a case that every E&P is undervalued. It's less capital-intensive for NVA to grow production going forward as the firm commitment for processing and takeaway capacity are already in place. The return opportunity will not only come from a multiple re-rating (from share buybacks) but also from earnings/cash flow growth. NVA is in a unique spot compared to its peers.

For further details see:

NuVista Energy: Not Getting Slapped For Growth