TOL - NVR: Exemplary Capital Allocation

Summary

- NVR is a textbook example of excellent capital allocation, consistently earning a 20%+ ROIC on a growing capital base.

- NVR has reduced their share count by 75% since going public, increasing EPS four-fold on top of organic earnings growth.

- NVR is undervalued in the current price range, offering investors the opportunity to compound their capital for a long time.

- A temporarily weak U.S. housing market does little to detract from the long-term appeal of NVR stock.

Investment Thesis

NVR ( NVR ) is the fourth-largest homebuilder in the United States, and through a disciplined approach to capital allocation, centered on lot purchase agreements and share repurchases, has managed to compound capital at exceptional rates of return. Despite macroeconomic concerns, at 12x free cash flow, NVR offers one of the best opportunities for investors to compound their capital for a long time.

The U.S. Housing Market

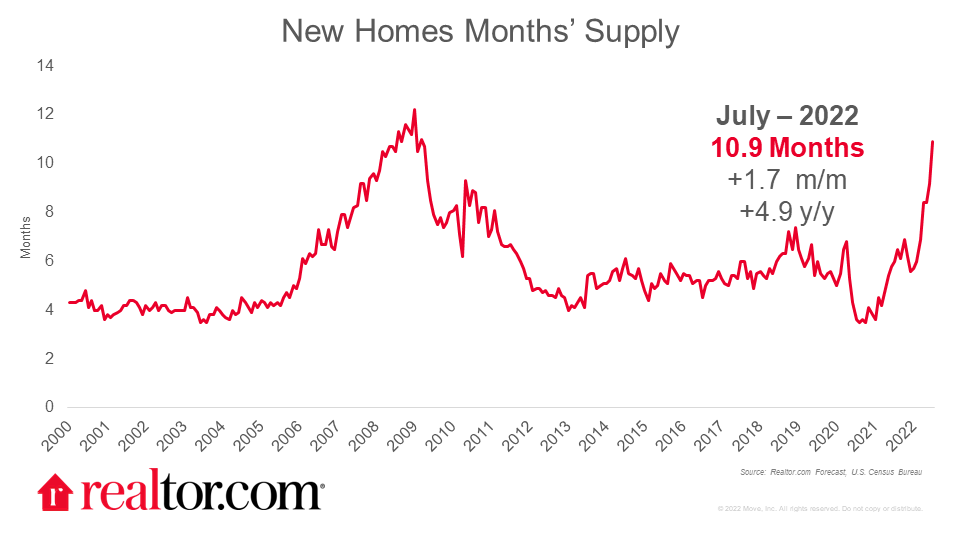

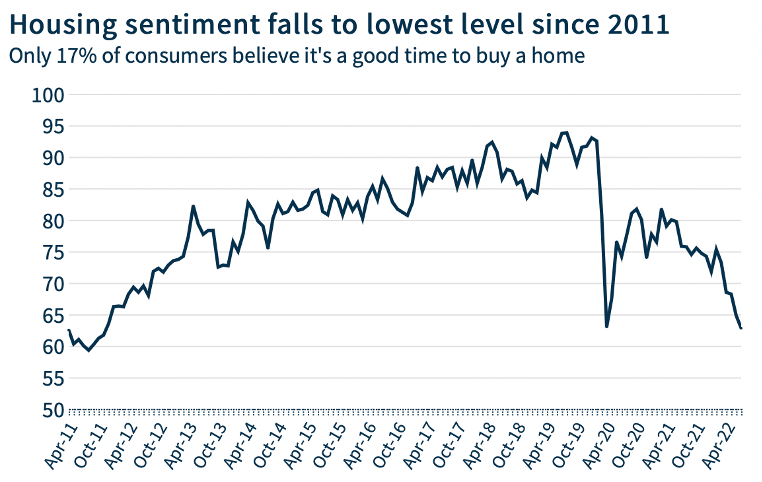

Any investor in homebuilders must first recognize the macroeconomic conditions surrounding the industry, and to be blunt, the homebuilding industry isn't looking good in the short term. Mortgage rates have been soaring and inventory is at levels not seen since 2009 , at 10.9 months of supply. At this moment, only 17% of Americans feel it is a good time to be buying a home - the lowest level since 2011.

{kind=link}

US Housing Sentiment (Fannie Mae)

{kind=link}

While such headlines are alarming for investors in homebuilders, markets are mostly efficient and much of this negative news is already priced in with NVR at 12x free cash flow.

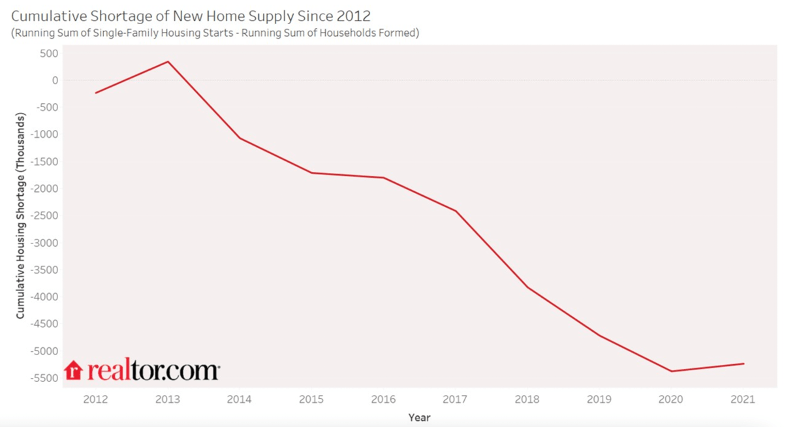

Despite short-term headwinds, long-term macro conditions look bright for homebuilders. Since 2012, the U.S. has seen 12.3 million new households form, compared to 7 million new homes, indicating that America is 5.3 million homes short of demand, and at the current pace of housing starts (1.446 million annualized), demand won't be met for the foreseeable future.

Cumulative US Housing Shortage (Realtor.com)

{kind=link}

The Beauty of NVR's Business Model

What sets NVR apart from other homebuilders, those who arguably operate commodity, low return on capital businesses, is NVR's devotion to lot purchase agreements (LPAs). And while some homebuilders have been adopting LPAs on a broader scale in recent years, NVR remains the gold-standard in the industry for execution.

LPAs are a valuable instrument, and are explained by NVR in their 10-Q :

We generally do not engage in the land development business. Instead, we typically acquire finished building lots at market prices from various development entities under LPAs. The LPAs require deposits that may be forfeited if we fail to perform under the LPAs. The deposits required under the LPAs are in the form of cash or letters of credit in varying amounts, and typically range up to 10% of the aggregate purchase price of the finished lots […] Our sole legal obligation and economic loss for failure to perform under these LPAs is limited to the amount of the deposit.

To summarize, NVR pays a small deposit to a developer to have the right of first refusal on a property. If NVR decides not to purchase the property for whatever reason - maybe they think the market's deteriorated - they don't have to buy the house, and simply lose their deposit.

This model is attractive because it makes the developer put up most of the capital to build a home, driving up NVR's ROIC, while also offloading a substantial amount of market risk (e.g., if home prices fall in an area, NVR's losses are mitigated). This capital-light, reduced-risk model enabled NVR to remain profitable and nimble throughout the Great Financial Crisis.

Unique Approach to Assessing Market Share

Competitors such as D.R. Horton ( DHI ), Lennar ( LEN ), PulteGroup ( PHM ), and Toll Brothers ( TOL ) often assess their success by their nationwide market share. NVR takes a different approach, preferring to be number one in a particular area, say Baltimore, Maryland. In fact, NVR only operates in 35 metropolitan areas across the United States.

NVR is clear about this strategy with shareholders and believes it enhances their market power and minimizes cyclicality.

We focus on obtaining and maintaining a leading market position in each market we serve. This strategy allows us to gain valuable efficiencies and competitive advantages in our markets, which we believe contributes to minimizing the adverse effects of regional economic cycles and provides growth opportunities within these markets.

This focus on being number one in a dedicated area also means that NVR has not begun to tap out their total addressable market. According to the Census Bureau , there are 384 metropolitan areas across the United States; NVR is present in just 9.1% of them. Additionally, as the trend toward urbanization continues, NVR's addressable market will only grow.

Capacity to Reinvest

One thing I look for in a business is the capacity to reinvest. Many of the greatest businesses in the world, whether it be Walmart ( WMT ), Amazon ( AMZN ), or Berkshire Hathaway ( BRK.A , BRK.B ), have gotten there by generating substantial amounts of cash and reinvesting those proceeds back into their business at high rates of return. NVR does the same.

A casual investor may think that because NVR invested just $16.9 million in capital expenditures in 2021, they don't reinvest. They would be wrong: NVR reinvests through substantial working capital increases.

Since 2019, NVR has increased working capital from $2.5 billion to $4.3 billion, averaging a 16.5% reinvestment rate, which was primarily driven by inventory growth in the form of LPAs while still maintaining a 25% return on invested capital. Such stellar results are demonstrative of NVR's capital allocation prowess, and ability to steadily compound profits.

NVR Key Operating Statistics (Author's Work, NVR 10-K)

{kind=link}

As the business and working capital needs grow, I remain confident that NVR's management team will continue to emphasize returns on capital, and as a result, shareholders will benefit.

Immense Capital Return Program

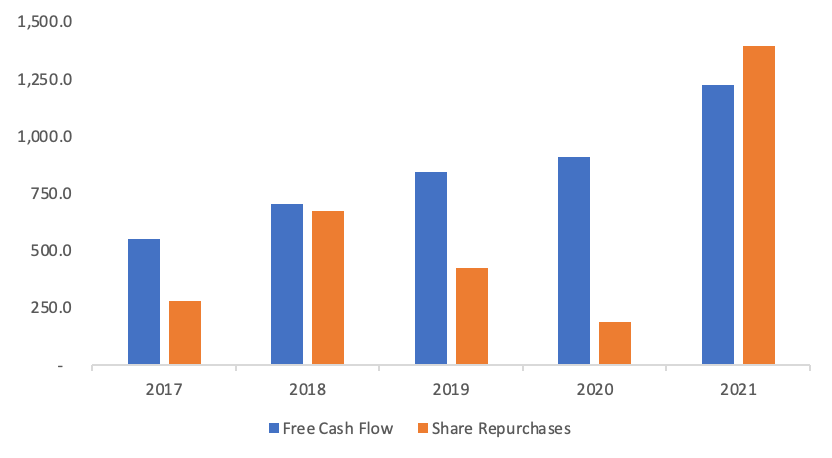

In response to high free cash flow generation, NVR has repurchased a massive number of shares. Since going public in 1993, NVR has retired 75% of all their shares, taking the diluted share count from 15 million down to 3.5 million today. The subsequent impact on EPS of these buybacks has been enormous.

This is a potent example of the power of negative compounding. A 75% reduction in shares does not increase EPS by 75%, instead, it results in a 300% increase in EPS. Put another way, if NVR had not retired any of their shares since 1993 and instead opted to pay dividends, the stock price would likely be at around a quarter of the level it is today.

In keeping with history, NVR has bought back $1.6 billion worth of stock over the past twelve months, approximately equal to their free cash flow, reducing the share count by 10.1%.

NVR Share Buybacks vs. FCF (Author's Work)

{kind=link}

Valuation

I will value NVR on a relative basis, an absolute basis through a discounted cash flow model ((DCF)), and through a reverse DCF to see what assumptions are baked into the current valuation.

Relative

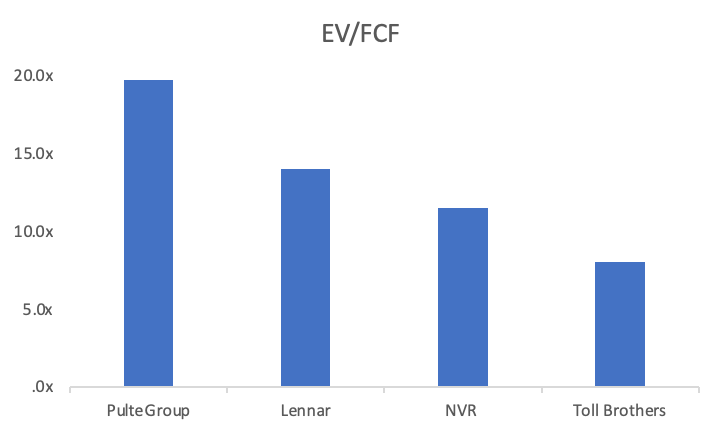

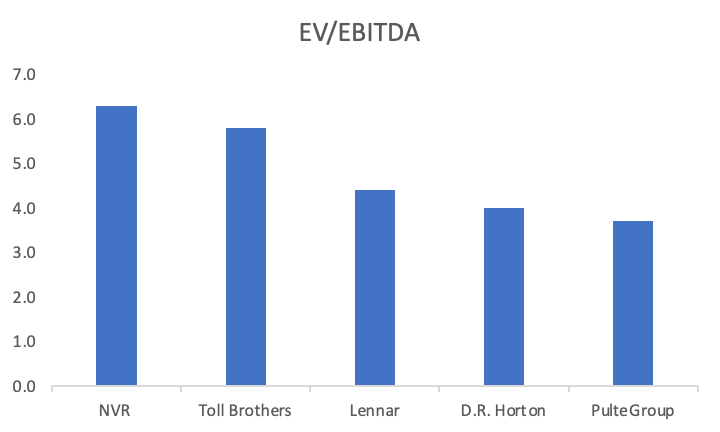

NVR's financial results are a lot cleaner than their competitors, many of whom don't generate consistent cash flows, which should be kept in mind when making this comparison. For the comparison basket, I'll be using some of their largest competitors: D.R. Horton, Lennar, PulteGroup, and Toll Brothers, and their respective P/E, EV/FCF, and EV/EBITDA multiples.

Enterprise Value to FCF Comparison (Author's Work) Enterprise Value to EBITDA Comparison (Author's Work)

{kind=link}

{kind=link}

{kind=link}

Despite the relative comparison making NVR appear somewhat overvalued, the consistency of free cash flow and returns on capital are what investors are paying for at NVR. Notably, all of NVR's competitors, except for DHI, earn less than a 20% ROIC, although DHI has negative free cash flow.

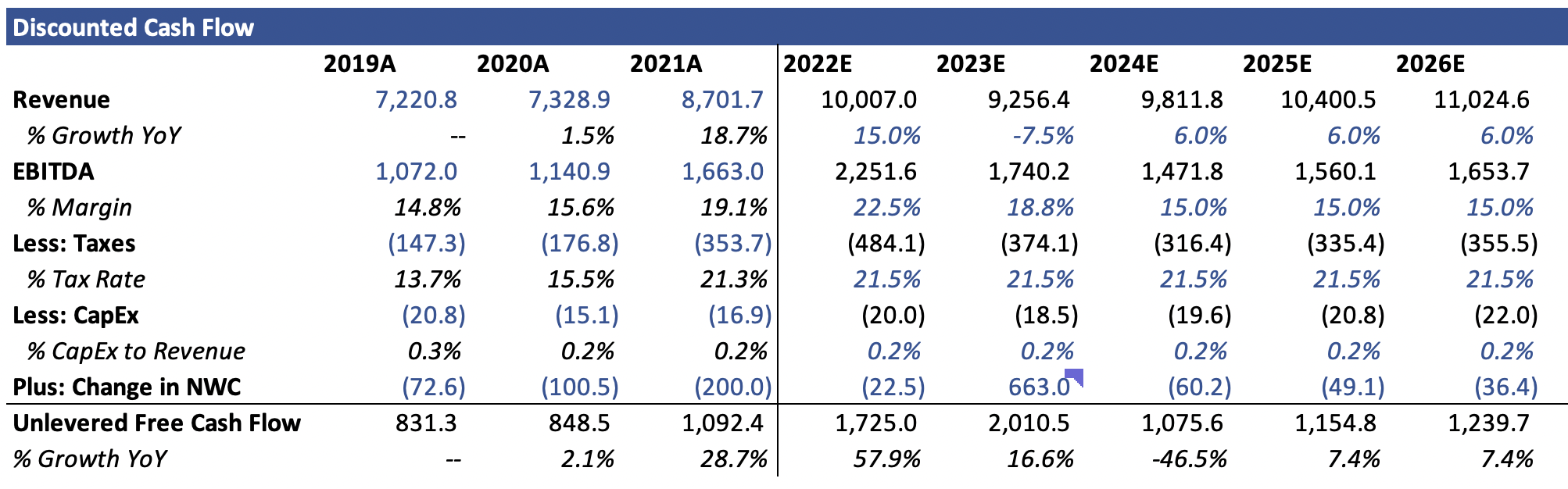

Discounted Cash Flow

Since a business is worth only as much as the present value of its future free cash flows, a DCF is necessary when valuing a stock.

Using what I believe to be reasonable assumptions: revenue growth approximately in line with consensus, EBITDA margins declining 750 bps to 15% by 2023, and all other percentage inputs in line with previous years, along with a 10% discount rate and 15x exit multiple, I reach an estimated intrinsic value per share of ~$4,800 per share after adjusting for debt and cash. This is ~12.5% higher than the current share price.

NVR Discounted Cash Flow Table (Author's Work, NVR 10-K)

{kind=link}

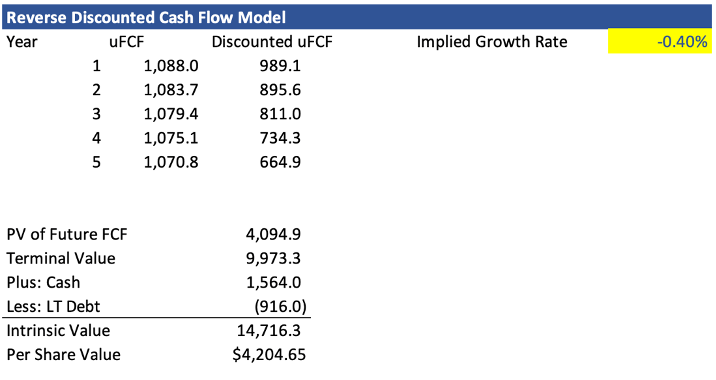

Reverse Discounted Cash Flow

Using the same discount rate and terminal multiple assumptions from the DCF, it appears as though the market is pricing in negative 0.4% annual FCF growth over the next five years off a base of $1.1 billion. These assumptions seem conservative and suggest there is substantial upside from the current price range.

NVR Reverse DCF (Author's Work)

{kind=link}

Risks

I can identify two key risks to the NVR thesis: the recent retirement of long-time CEO Paul Saville , and a macroeconomic backdrop that proves more challenging than expected.

- Paul Saville's Retirement : Saville had been the CEO of NVR since 2005, reinforcing the company's zealous devotion to returns on capital and share buybacks, and retired in May. While Saville will remain on board as Executive Chairman and a successor, Eugene Bredow, has already been appointed, his presence will be missed at the company, and it remains to be seen whether Bredow has what it takes to lead NVR to new heights.

- Challenging Macroeconomic Backdrop : Despite their capital allocation prowess, NVR's business is still dependent on economic cycles, and a harder recession and/or rapidly rising interest rates could put a larger-than-expected dent in earnings in 2023, potentially driving down the stock price.

Closing Thoughts

NVR is a high-quality, conservatively financed company with a clear runway for decades of continued growth. NVR also possesses the rare ability to generate substantial amounts of cash and reinvest those proceeds back into the business at high rates of return, the hallmark of any great compounder. I'm a happy buyer in the sub-$4,200 price range.

For further details see:

NVR: Exemplary Capital Allocation