TOL - NVR Inc.: Recession Fears Loom Over This Exceptional Homebuilder

2023-06-14 17:45:15 ET

Summary

- NVR has displayed a remarkable track record of growth and profitability with consistent revenue increases and substantial free cash flow growth.

- NVR's impressive return on equity (ROE) over the past decade, coupled with a solid balance sheet and successful share repurchase strategy, further highlight its effective management and financial strength.

- Our valuation analysis suggests potential overvaluation of the stock, while concerns over inflation, interest rates, and economic downturn persist.

Intro

NVR, Inc. (NVR) is a prominent US homebuilder that operates in the Homebuilding and Mortgage Banking sectors. The company specializes in constructing and selling a variety of residential properties, including single-family homes, townhomes, and condominium buildings under popular brands like Ryan Homes, NVHomes, and Heartland Homes. Its customer base spans from first-time buyers to luxury home seekers. Headquartered in Reston, Virginia, NVR primarily operates across multiple states and regions throughout the US.

In our previous coverage of NVR, we assigned a buy rating to the company due to its exceptional track record, unique business model, and attractive valuation. However, it's worth noting that NVR's stock price has surged by 27.9% year to date, outperforming the S&P 500 and raising questions about the validity of the buy rating. Furthermore, concerns around rising inflation and interest rates have emerged, prompting a re-evaluation of the investment thesis.

Track Record

Considering NVR's exceptional track record of growth and profitability is vital as it offers valuable insights into its historical performance and consistent returns. This information enables investors and stakeholders to evaluate the company's stability, competitiveness, and future prospects. Despite numerous market-moving events over the past decade, such as the Brexit referendum, two controversial US presidential elections, the COVID-19 pandemic, and the Russian invasion of Ukraine, NVR has demonstrated outstanding financial resilience.

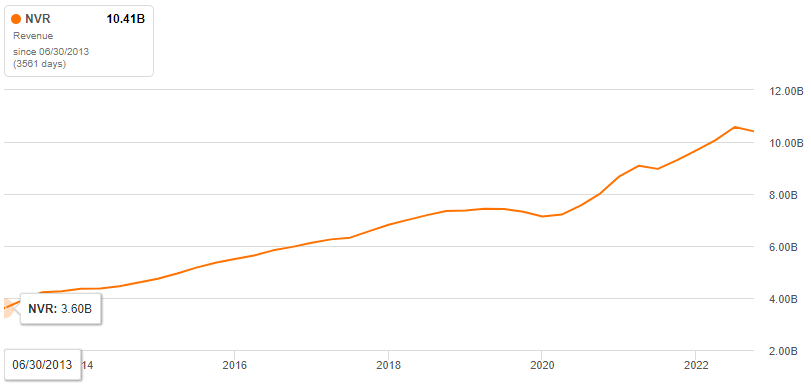

NVR has shown consistent growth over the past decade while increasing its revenue by a remarkable 150% over the period with not a single year of decline. Additionally, free cash flow has also grown by an astounding 637% during this period. Strong free cash flow growth is a significant indication that NVR is generating a significant amount of cash from its operations, which can be used to reinvest in the company, pay down debts, distribute dividends to shareholders, or pursue strategic initiatives.

{kind=link}

NVR's track record of profitability is truly impressive, showcasing the company's proficiency at utilizing its excess free cash flow. Over the past decade, NVR has consistently achieved an average return on equity (ROE) of 36.1%, never dipping below 19.7%. This consistently high ROE is a testament to the company's competitive advantage, efficient operations, and sound strategic decision-making by its management team. It reflects NVR's ability to generate substantial returns for shareholders and reinforces its position as a well-managed and financially successful business.

Data by Stock Analysis

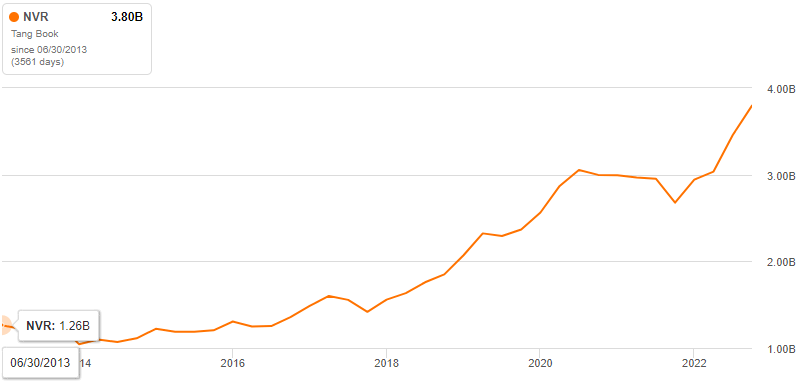

Moreover, NVR has effectively managed its debt, maintaining a solid balance sheet. The company currently boasts a debt-to-equity ratio of 0.26 and a current ratio of 5.75. What might be more impressive is NVR has tripled its tangible book value over the past decade. This is a significant achievement for the company, indicating substantial growth in its assets and overall financial strength. This demonstrates the company's ability to generate profits, reinvest in its operations, and increase its net worth.

{kind=link}

The company's share repurchase strategy has been commendable, as it has successfully bought back roughly 1.5 million shares over the past decade, accounting for an impressive 32% of the total outstanding shares. Share repurchases provide multiple benefits for investors, allowing those who wish to divest their holdings to receive cash for their shares, while simultaneously increasing the ownership stake and potential value for existing shareholders, without requiring additional capital investment.

Data by Stock Analysis

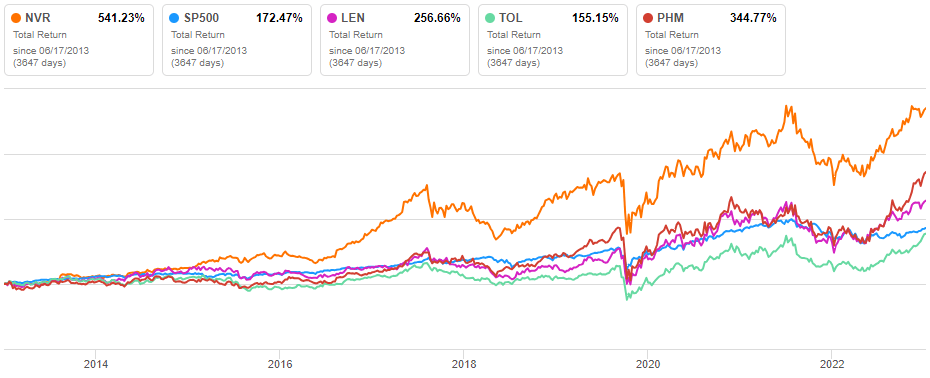

NVR's exceptional performance over the past decade has propelled it to deliver market-beating returns, surpassing not only the S&P 500 but also outperforming key competitors such as Lennar Corporation ( LEN ), Toll Brothers, Inc. ( TOL ), and PulteGroup, Inc. ( PHM ). With such impressive achievements, the lingering question on investors' minds is whether NVR can sustain this remarkable performance over the next ten years.

{kind=link}

Outlook

In our previous analysis of NVR, we emphasized the noteworthy risk factors associated with investing in the company, particularly in light of the economic conditions at the time (January). An economic downturn remains a significant concern as it can have a detrimental impact on the demand for new homes, resulting in reduced sales and negative effects on profitability, stock performance, debt obligations, and future cash flows.

High-interest rates and inflation continue to pose risks for NVR. Inflationary pressures may lead to even higher interest rates, making housing less affordable for potential buyers and increasing borrowing costs for the company. Additionally, fluctuations in commodity prices, including lumber, concrete, and steel, can escalate construction costs, potentially reducing demand for NVR's houses.

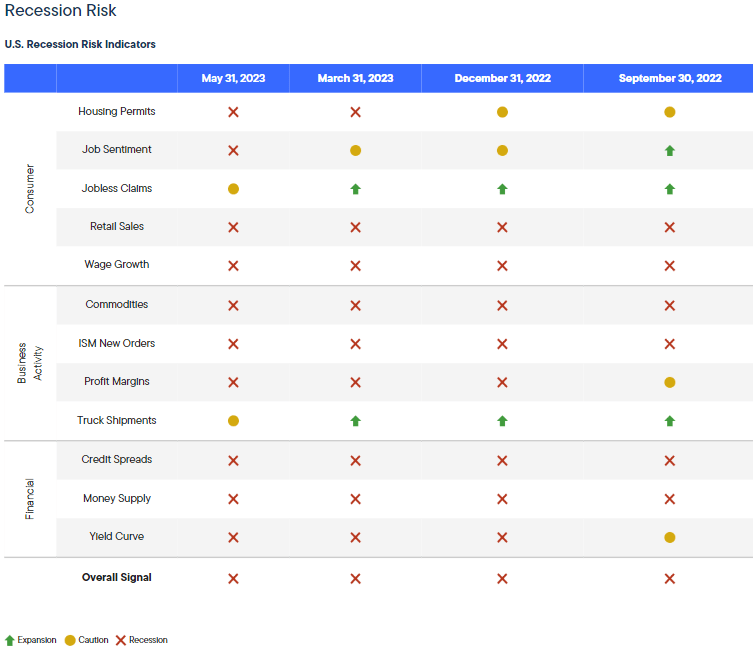

The homebuilding sector is particularly vulnerable to economic downturns due to the substantial financial commitment involved in purchasing a home. Speculating on the future state of the US economy remains challenging due to the multitude of unpredictable factors at play. In our previous article, we referenced a valuable chart from Franklin Templeton's " Anatomy of a Recession " program. Regrettably, the latest results from Franklin Templeton indicate a weakening economy, with nearly all factors pointing towards a potential recession.

{kind=link}

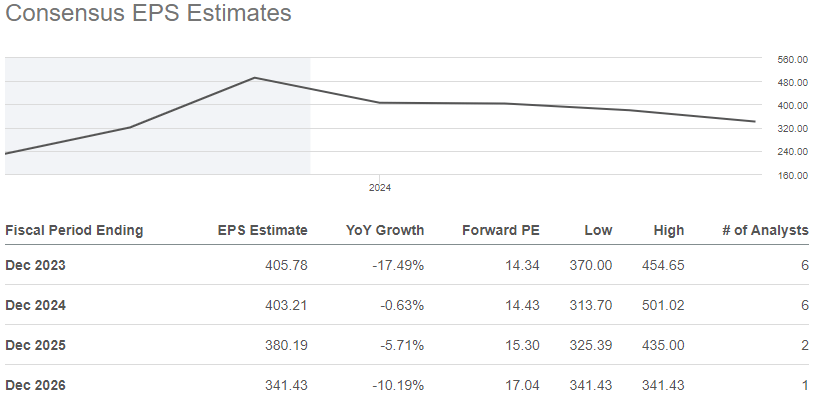

Fears of recession coupled by rising interest rates and inflation have had an impact on analyst who are predicting a difficult road ahead for NVR. For 2023, analyst estimate earnings of $405.78 for the home builder which represent a year over year decline of 17.49%. To make matters worse analyst are then predicting three consecutive years of declining earnings through 2026.

{kind=link}

Despite these risks, NVR continues to perform strongly. The company exceeded expectations in the first quarter , surpassing estimated earnings per share ((EPS)) by $10.93 with an impressive EPS of $99.89. NVR also reported revenue of $2.13 billion, a 7.7% decline compared to the previous year but still surpassing analyst expectations by $45.4 million.

New orders in the first quarter of 2023 slightly decreased by 1% to 5888 units compared to the same period in 2022, but they saw a substantial 41% increase compared to the fourth quarter of 2022. It is important to highlight that the average sales price of new orders in the first quarter of 2023 experienced a decline of 5%, reaching $441,200. Therefore, demand is improving but there are ongoing affordability challenges due to higher mortgage interest rates and home prices.

The current environment is challenging, but we have confidence in NVR's ability to capitalize on potential opportunities resulting from future economic and homebuilding market fluctuations. This optimism is driven by the robustness of the company's balance sheet which will allow the company to weather any storm and its prudent approach to acquiring lots, which positions NVR favorably for the future.

NVR lot acquisition strategy is unique within the industry. NVR mainly buys ready-to-build land from other developers through agreements. These agreements require a deposit, usually around 10% of the total price. If NVR doesn't follow through with the agreement, they may lose the deposit, but they aren't obligated to continue with the purchase. The developers they buy from cannot hold NVR responsible for any financial obligations. This approach helps NVR avoid the risks and costs of owning and developing land directly while still ensuring they have enough land for their future plans.

This approach has helped NVR optimize its inventory turnover, which we think reduces market risk and allows the company to operate with less capital. As a result, it improves the company's returns on investment and enables the business to achieve the superior financial results we discussed in the previous section.

Valuation

We will use the discounted cash flow ((DCF)) analysis, which is a method we prefer for valuing companies, to assess NVR's true value. The DCF analysis calculates the present value of the company's expected future cash flows to determine its inherent worth.

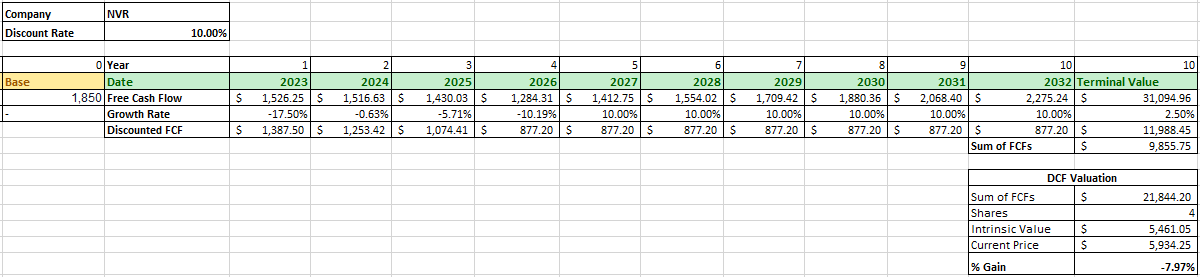

To begin the analysis, we'll start with NVR's free cash flow from the previous year, which was $1.85 billion. For 2023, we'll consider the average analyst earnings growth rate of -17.5%. Then, based on the average analyst earnings estimates, we'll use growth rates of -0.63%, -5.71%, and -10.19% for the following three years. Predicting NVR's future free cash flows beyond the next four years is challenging due to uncertainty and limited visibility but considering the company's strong historical performance with an average annual free cash flow growth rate of 24.9% over the past decade, a more conservative growth rate of 10% for the next six years seems reasonable.

To calculate the terminal value, we'll use a more conservative perpetual growth rate of 2.5%. With a discount rate of 10%, taking into account the long-term return rate of the S&P 500 with dividends reinvested, we determine NVR's intrinsic value to be $5461.05. This suggests that NVR might currently be overvalued, potentially resulting in a loss of -7.97% for investors compared to the company's current market price.

{kind=link}

Takeaway

NVR has displayed a remarkable track record of growth and profitability. With consistent revenue increases and substantial free cash flow growth, the company demonstrates its ability to generate significant cash for reinvestment and strategic initiatives.

NVR's impressive return on equity (ROE) over the past decade, coupled with a solid balance sheet and successful share repurchase strategy, further highlight its effective management and financial strength.

Our valuation analysis indicates that the stock might be overvalued at present, implying a potential downside for investors relative to the current market price. Additionally, the presence of concerns surrounding inflation, interest rates, and a possible economic downturn persist. However, NVR's strong lot acquisition strategy and solid balance sheet make it prudent to retain a HOLD recommendation.

We appreciate your perspective on our evaluation of NVR, whether you agree or have differing opinions. If you have insider knowledge from the housing industry or just an avid follower and wish to provide additional insights, we invite you to share them with us. Your comments and input are highly valuable to us, so please feel free to participate in the conversation by leaving your thoughts in the comments section below. Let's engage in a discussion and learn from each other's perspectives.

For further details see:

NVR, Inc.: Recession Fears Loom Over This Exceptional Homebuilder