NXPI - NXP Semiconductors: Keeping A Hold Rating Even After Yet Another Strong Quarter

2023-11-08 12:16:29 ET

Summary

- The market does not seem to be very impressed by NXP Semiconductors' better than expected quarterly results.

- Margins are likely to come under pressure over the coming year as growth is also slowing down.

- Investors should also keep a close eye on inventory levels and management decisions regarding future capital expenditures.

After beating the consensus estimates for the third quarter of the year and providing an optimistic guidance for the next 3-month period, NXP Semiconductors' ( NXPI ) share price is little changed following the report.

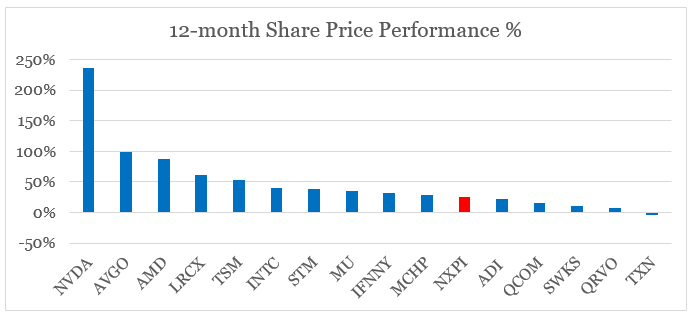

Over the past year, NXPI has also experienced significant volatility and performed roughly in line with its main competitors. For the past 12-month period, Infineon Technologies ( IFNNY ) ( IFNNF ) is now trading slightly above NXPI, and Qualcomm ( QCOM ) has suffered due to its significant exposure to the handset market.

The nearly 18% share price return, however, is far less impressive after considering returns achieved by the broader semiconductors peer group.

{kind=link}

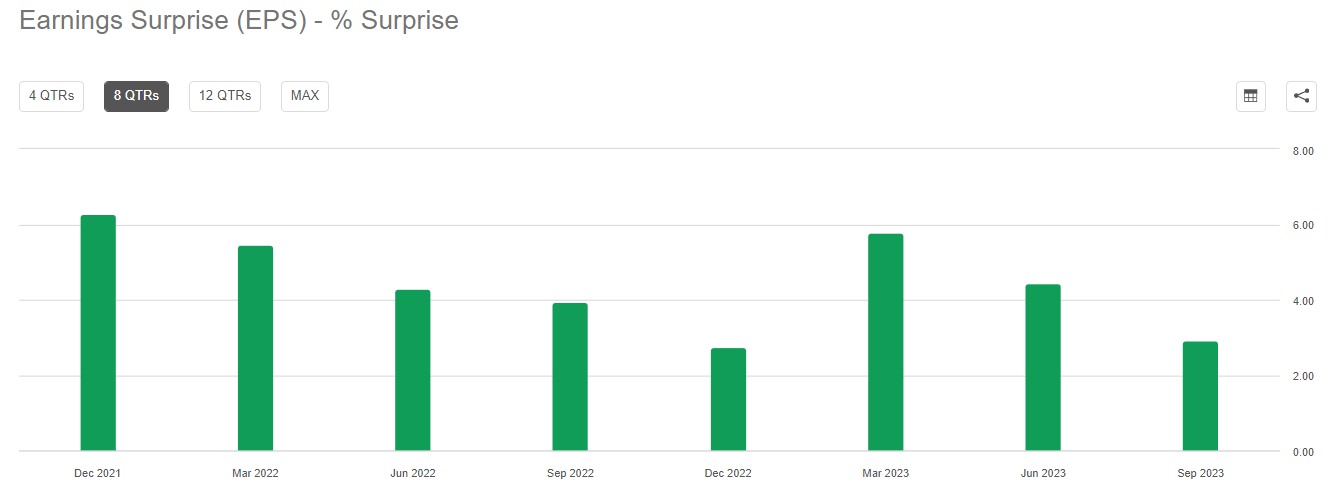

On top of that, NXPI has consistently beaten expectations on a quarterly basis with notable earnings per share surprise in each of the past eight quarters.

{kind=link}

Nonetheless, the market was not impressed as recent industry-wide tailwinds associated with automotive semiconductor shortages are now cooling-off and other end-markets are experiencing difficulties. Quarterly revenue was essentially flat year-on-year and operating margin fell even after accounting for the one-off legal liability.

From a total operating profit perspective, non-GAAP operating profit was $1.2 billion and non-GAAP operating margin was 35%. This was down 190 basis points year-on-year and slightly below the midpoint of the guidance range due to the previously noted potential legal liability which created a 40 basis points headwind to non-GAAP operating margin.

Source: NXP Semiconductors Q3 2023 Earnings Transcript

The effective tax rate was lower during the quarter which resulted in earnings per share numbers coming slightly above the midpoint of the guidance.

Overall, the market is already looking past the recent tailwinds for the industry and although NXPI is well-positioned over the long-run, I do not expect significant upside in the near-term. Earlier this year, I discussed all that in a thought piece which outlined why NXPI remains on my watch-list, in spite of its strong positioning in the sector

Industry-Wide Tailwinds

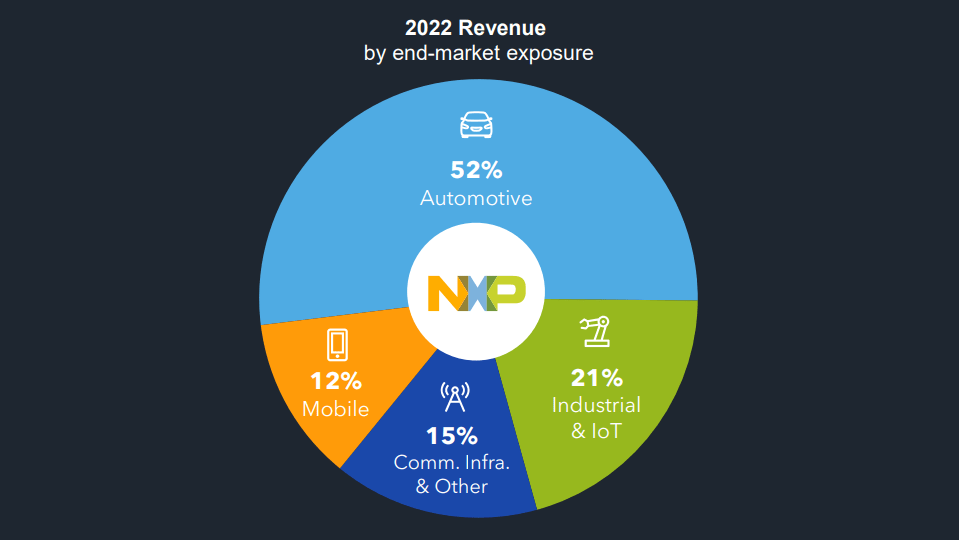

During the third quarter, NXPI's management noted that it was only Communication, infrastructure & other segment that performed below expectations, while all other segments were in-line with the previous guidance.

NXP delivered quarterly revenue of $3.43 billion, $34 million above the midpoint of guidance. Revenue trends in our Mobile, Industrial & IoT and Automotive end-markets all performed in-line or better than anticipated, while our Communication Infrastructure & Other end market was slightly below our expectations . The combination of our third quarter results, and the mid-point of our fourth quarter guidance indicates revenue for the full year 2023 will be flat versus 2022 in a challenging and cyclical market environment.

Source: NXP Semiconductors Q3 2023 Earnings Release

Although this might sound like good news, given the strong narrative around the automotive semiconductors, the Communication, infrastructure & other segment represents only a small fraction of NXPI's revenues and quarterly net sales figure still came in flat year-on-year.

{kind=link}

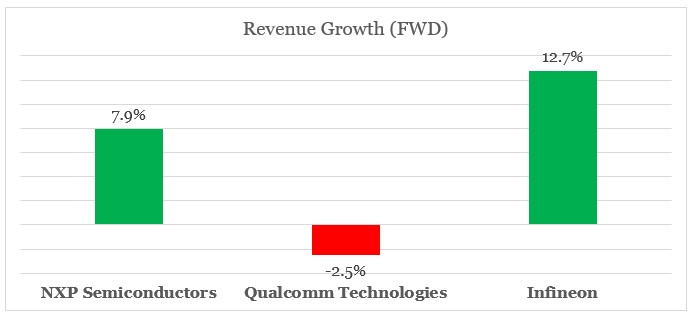

Going forward, NXPI is expected to grow at almost 8%, but this is still well-below the expected growth of one of its main peers - Infineon Technologies.

{kind=link}

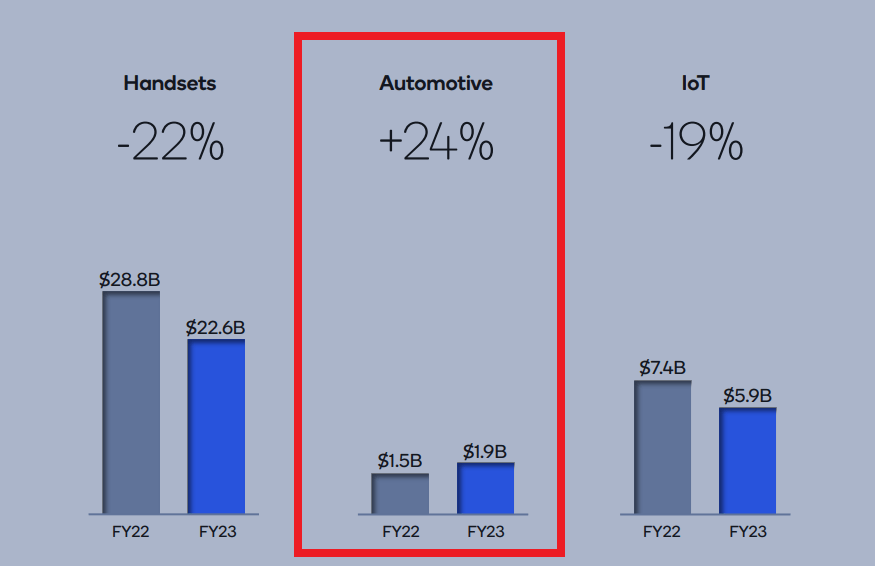

Qualcomm's forward revenue growth is in negative territory, but this is due to softness in handsets and IoT segments, while its automotive revenues grew by 24% during the past year.

{kind=link}

Similarly to QCOM, Texas Instruments' ( TXN ) revenue is also expected to decline over the coming year due to the company's significant exposure to industrial and personal electronics markets.

During the quarter, automotive growth continued and industrial weakness broadened. Similar to last quarter, I'll focus on sequential performance, as it is more informative at this time. First, the industrial market was down mid-single digits , with weakness broadening across nearly all sectors. The automotive market continued to grow and was up mid-single digits .

Source: Texas Instruments Q3 2023 Earnings Transcript

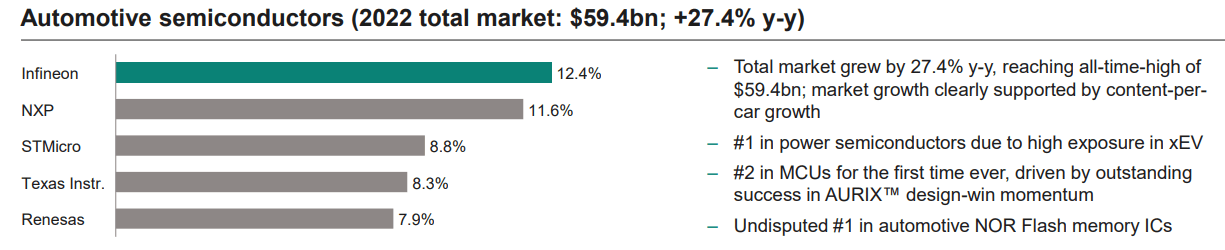

STMicroelectronics ( STM ), the third largest player by market share in the automotive semiconductor space, is also expected to achieve much higher topline growth than NXPI going forward.

{kind=link}

Seeking Alpha

In a nutshell, NXPI's expected growth is among the lowest within its peer group after taking into account the company's significant exposure to the growing automotive market. Even though the company is well-positioned in the highly attractive automotive end-market, it could also experience a gradual decline in margins.

Are Margins Sustainable?

In addition to NXPI's high market share within the automotive sector, the company's high margins are one of the most attractive features that supports the company's premium valuation to the likes of IFNNY and STM.

Seeking Alpha

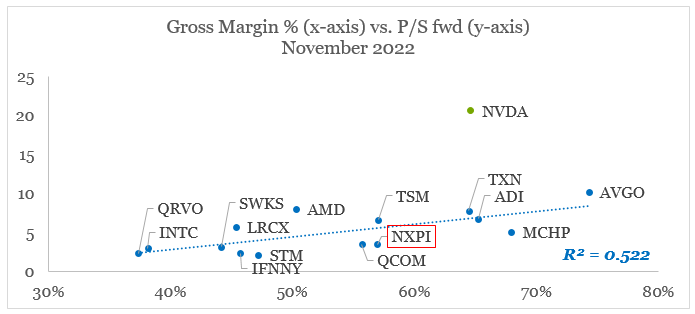

On a cross-sectional basis within the broader peer group in semiconductors, gross margin appears to be the key driver of price/sales multiples (of course once we exclude Nvidia ( NVDA ) due to the company's outlandish valuation).

{kind=link}

What we note from the graph above, however, is that NXPI, QCOM, STM and IFNNY all lie below the trend-line, meaning that the market is assigning lower sales multiples for these companies to what their current margins would suggest.

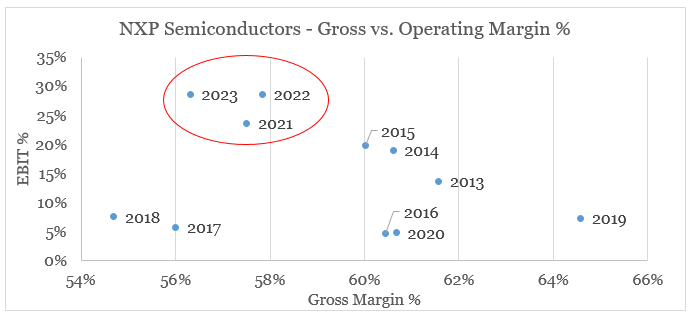

One of the main reasons being that the recent automotive semiconductor shortage resulted in much higher capacity utilization for NXPI and with that operating margins skyrocketed even as gross margins are at multi-year lows.

{kind=link}

This creates a risk of multiple contraction in the event of sustained difficulties for some of NXPI's end-markets and a slowdown in the automotive space. Even though the latter appears as an unlikely scenario at this point in time, the record high operating margins appear unsustainable as supply chains normalize and competition continues to intensify.

The Cash Flow Perspective

From a free cash flow point of view, NXPI appears to be trading at very attractive levels with current yield of above 5% which is notably higher than the sector median.

Seeking Alpha

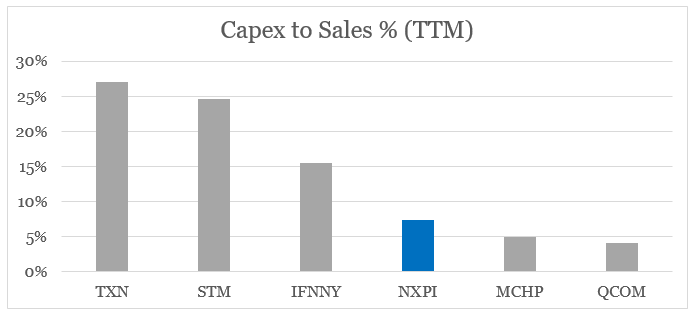

Most of NXPI's competitors, however, are taking advantage of the strong demand within the sector and the high cash flow associated with it and have significantly increased the amount spent on capital expenditure in their efforts to onshore more capacity.

{kind=link}

On one hand this significantly reduces their free cash flow, but it could also put NXPI at a disadvantage in the future. It should be noted that the company is among the smaller investors in the recently announced joint venture with TSMC ( TSM ) for the construction of a large 300mm fab in Germany. This will significantly increase the amount of on-shored capacity, but NXP's holding will still be limited to 10%.

On August 8, 2023, TSMC, Bosch, Infineon, and NXP announced the planned formation of a joint venture European Semiconductor Manufacturing Company ((ESMC)) GmbH, in Dresden, Germany to provide advanced semiconductor manufacturing services predominantly to the automotive and industrial sectors. The planned 300mm fab joint venture will be 70% owned by TSMC, with Bosch, Infineon, and NXP each holding 10% equity stake ;

Source: NXP Semiconductors Q3 2023 Earnings Release

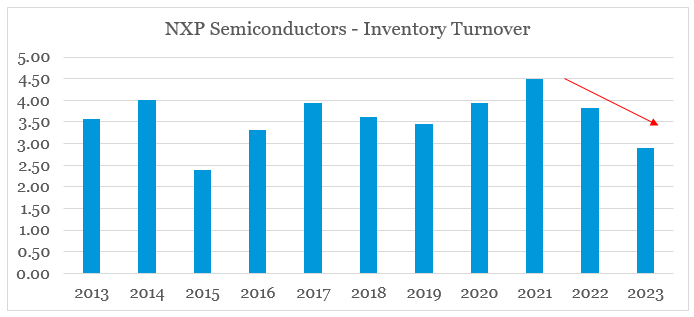

In addition to capital expenditure, changes in working capital and more specifically inventory levels also deserve attention when evaluating NXPI's ability to grow free cash flow.

In spite of the talk about inventory level improvements, on a 12-month basis NXPI's inventory turnover continues to fall from its highs in 2021.

{kind=link}

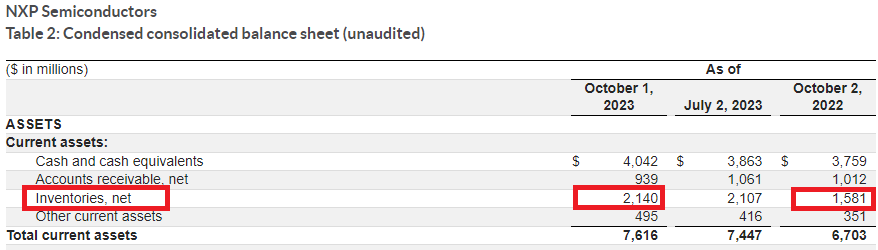

The total amount of inventories increased significantly during the last quarter from a year ago, even though revenues are essentially flat.

{kind=link}

During the last quarter, it also became clear that NXPI's management currently expects an increase in channel inventory during next year, in order to support future growth.

We expect to increase channel inventory sometime in 2024 to support anticipated growth, ensure proper customer stock levels, and to support our long-tail customers.

Source: NXP Semiconductors Q3 2023 Earnings Transcript

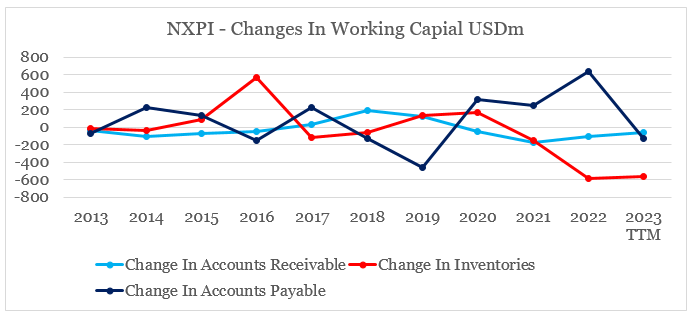

Therefore, should change in inventories continue to be a significant cash outflow, while the tailwind from higher payables is reversing, NXPI's free cash flow could experience a major headwind in 2024.

{kind=link}

Even though, the company is still in a good position to consistently increase its free cash flow in the long-run, this dynamic could easily derail stock price returns in the more immediate future.

Conclusion

NXPI continued to deliver better than expected results during the most recent 3-month period and although the company is well-positioned to compete in the highly attractive automotive semiconductor market, I do not see any immediate upside for the stock. Both margins and free cash flow would likely remain under pressure over the coming year, even if demand in from automotive OEMs and distributors remains robust.

For further details see:

NXP Semiconductors: Keeping A Hold Rating Even After Yet Another Strong Quarter