CA - Obsidian Energy Is Trying To Get To Easy Street

2023-03-31 16:00:53 ET

Summary

- The Obsidian Energy debt level is still likely too high compared to free cash flow at various commodity price levels.

- Obsidian Energy is making slower (than other competitors) progress towards debt reduction.

- The past balance sheet weakness and near-death experiences likely mean that weak valuation of the stock price will persist.

- Obsidian Energy management is clearly not taking advantage of the Clearwater Play as it should.

- A Obsidian Energy stock repurchase should not be an option until debt levels are suitable.

Obsidian Energy Ltd. ( OBE ) has had a long road back to normality. It clearly is not yet there. However, management seems to be persistent enough that the company will get back to investment acceptability from a more speculative level than the stock is currently at.

The market concerns about Obsidian Energy Ltd. appear to be about the level of free cash flow compared to the level of debt. After the downturns in 2015 and 2020, this market is concerned with debt levels at lower commodity prices than is the current environment. So, debt levels likely have to come down as this company had "stretched" financial ratios in the past, and Mr. Market does not want that possibility in the future.

Many managements and investors tout that debt ratios are now fine. For many financially weak companies, debt levels are usually fine at this stage of the business cycle. But the low visibility of the commodity industry and the presence of heavy oil production would seem to indicate a very conservative debt ratio (if any debt at all) so that the periodic downturns that plague this industry are not an issue in the future.

This is a company that experienced a near-death experience probably several times and needed a very heavy hitter like Rick George to get it out of trouble (along with the people he hired at the time). When he passed on from leukemia, that was leadership that was going to be hard to follow. Very few leaders in the industry make it to the Canadian oil and gas hall of fame.

Therefore, any market concerns are likely centered on the Obsidian Energy Ltd. debt load as well as whether the next management group will lead the company a whole lot better than what happened in the past. Such concerns will take some time. A re-evaluation of the company and its prospects will not happen overnight. Therefore, investors in a company like Obsidian Energy Ltd. need to be very patient.

Net Debt Reduction

It appears that the rate of debt reduction is concerning the market.

"C ontinued net debt reduction to C$323.1 million from C$428.1 million at September 30, 2021, including repayment of the C$30.0 million non-revolving term loan "

Source: Obsidian Energy Third Quarter 2022, Earnings Press Release .

This Canadian company reports in Canadian dollars unless otherwise noted. Canadian companies have an advantage in that benchmark oil prices are often related to United States pricing in dollars while the costs of production are in the weaker Canadian dollars. Still, the debt progress appears to be on the slow side.

Obsidian reported further progress to C$361.8 million in the fourth quarter. But that progress when compared to the total amount of debt likely has Mr. Market very worried about the debt repayment pace. Many companies looked at fiscal year 2022 as a year to reset the balance sheet . Compared to others in the industry, the Obsidian Energy Ltd. total debt progress is less than others. Meanwhile, many do not expect to see the high commodity prices that were part of fiscal year 2022 again for a long time.

Competitor Yangarra Resources Ltd. ( YGRAF ), for example, managed to repay about one-third of its outstanding debt and will likely soon have a balance that will not concern the market. Similarly, Yangarra Resources was one of the f ew companies that made a profit in fiscal year 2020. A debt-conscious market wants to see lots of profitability and a very fast progress towards satisfactory debt levels in considerably more hostile industry conditions.

On the other hand, Obsidian has a history of a lot of financial challenges, to say the least. That likely means a company like Yangarra will return to market favor a lot faster than the case may be here.

Heavy Oil Production

This company has leases in the important Clearwater and related areas that promise a lot of production with low breakeven points. The problem is that heavy oil production in the past has performed poorly during cyclical downturn. Sometimes there were years without cash flow or satisfactory cash flow (let alone profits). A company with heavy oil production needs to cater to even more concerns about balance sheet key financial ratios.

This management announced a stock buyback program that is only going to heighten concerns about the debt ratios. The market first wants the free cash flow ratio to debt to likely be far more conservative at lower commodity price levels. Therefore, any stock repurchase program needs to take that into consideration, or it is likely to prove to be counterproductive.

The whole Clearwater play appears to have unusually low breakeven points. But that has not erased some apparent concerns about the discount to pricing of premium oil grades expanding during a downturn. That may turn out to be a glaring weakness in the current management guidance (and hence future strategy) that may cause a weak stock price valuation well into the future.

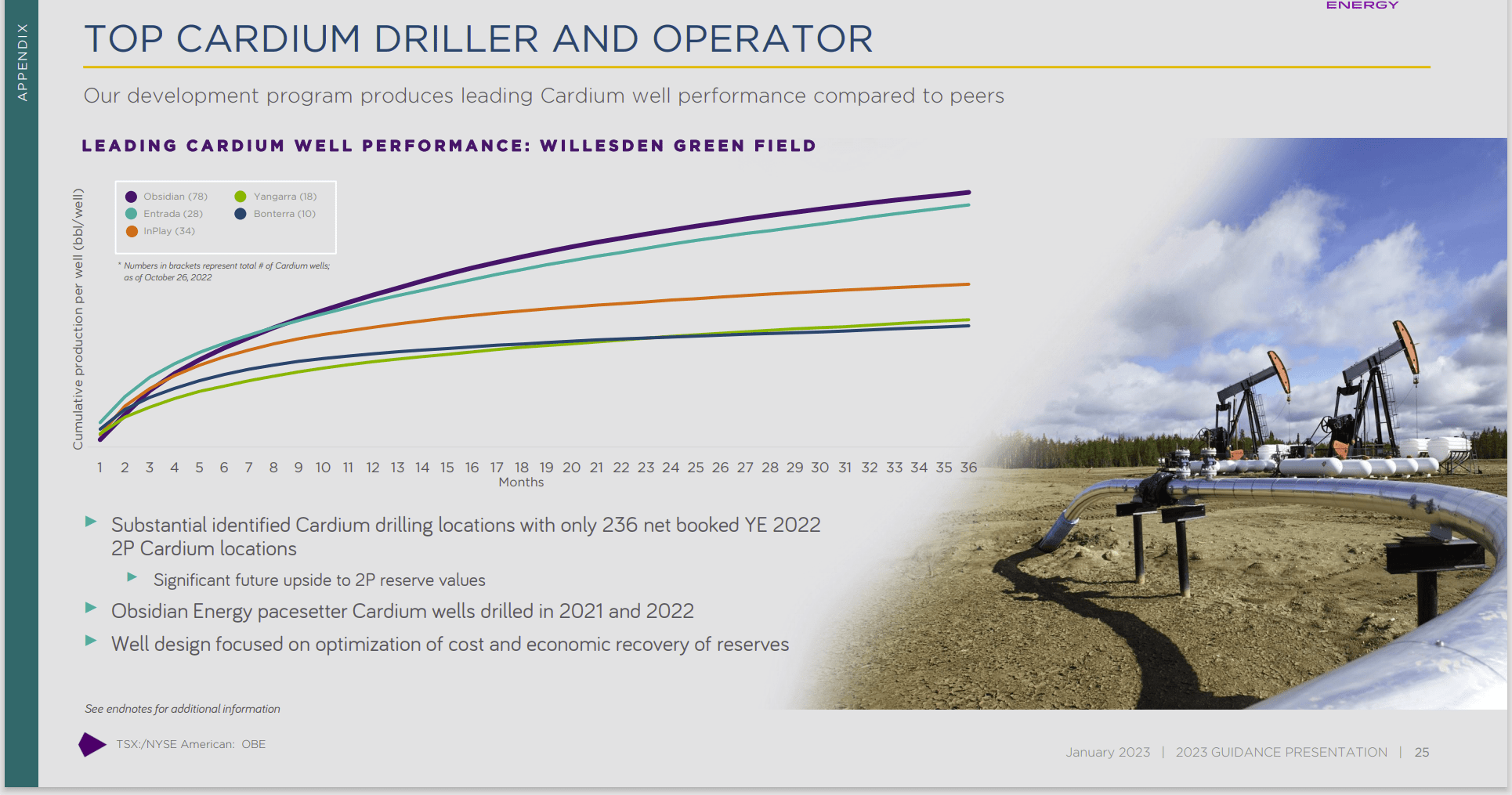

Top Production Is Not Everything

This management clearly touts the production of its wells, as shown below:

Obsidian Well Performance Comparison (Obsidian Fiscal Year 2023 Guidance Presentation)

{kind=link}

Clearly, the accomplishment shown above is worth noting. But what is really lightly covered in the presentation is how this affects profitability compared to competitors (and of course free cash flow).

Yangarra, for example, repaid a greater percentage of its debt. It is also a far more profitable (in my opinion) little company, despite the well performance shown above.

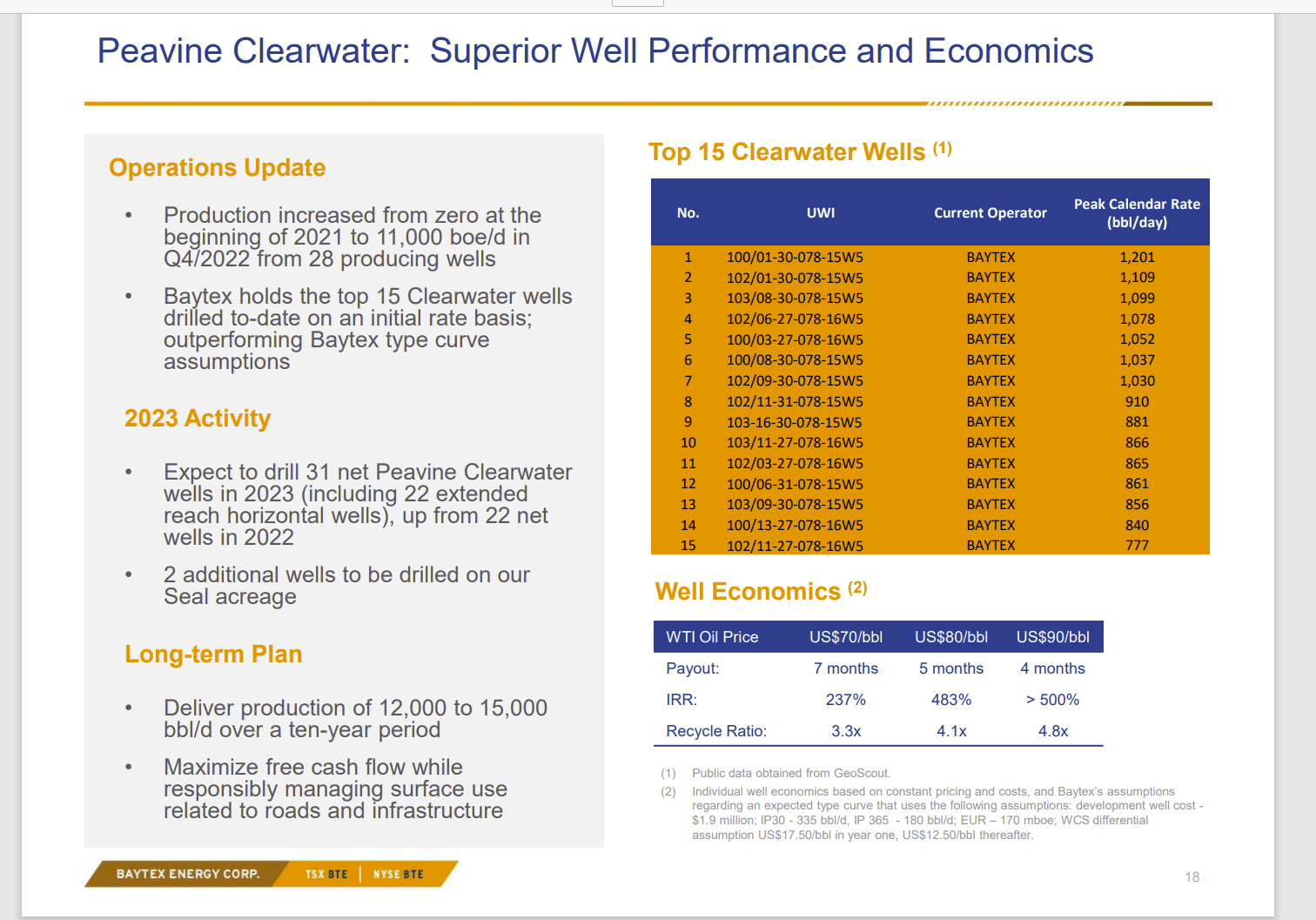

Competitors such as Baytex Energy Corp. ( BTEGF ) are in a position to expand the Clearwater Play materially with the latest guidance. Management is even acquiring some light oil production to open up the possibility of more heavy oil production.

Meanwhile, this company is drilling test wells long after much of the industry "jumped-in." Based upon the profitability of the Clearwater Play reported by competitors such as Baytex Energy, it would appear to be a far better strategy to get the debt down, so the profitability of the play can be taken advantage of now.

Baytex Energy Summary Of Clearwater Profitability (Baytex Energy March 2023, Corporate Presentation)

{kind=link}

One of the things about something potentially as profitable as Clearwater is that as a company, you have to be flexible enough to get those profits while they last. The Obsidian management does not appear to be that flexible. As a result, they could miss a fair amount of profit opportunity.

The current management proposal to repurchase shares does in effect return capital to shareholders. But it begs the question "do you really want to return capital when the potential to make 500% on that money is available?" That is such a huge return that even in an industry like this with high volatility and low visibility, that type of return should be obvious to investors.

Key Takeaways

It takes some serious planning to "get lucky." Some managements seem to just be in the right place at the right time very often. Rick George was one of those people.

This management appears to be fumbling away some profit opportunities. But it can learn from companies all around it. Murphy Oil Corporation ( MUR ), for example, talks about how the latest price environment accelerates the payback of a Gulf of Mexico platform by something like five years in various places of the fourth quarter update . But you have to plan ahead to even be in a position for that to happen.

Obsidian definitely has its debt issues, and that may be why management is not developing the heavy oil play to the extent of a lot of competitors.

The type of management now in control often wants a profit now rather than later. But the Clearwater play offers such potential that a stock buyback should probably not even be a thought. Such a plan likely costs a lot of future appreciation potential when there is a profitable alternative like Clearwater.

Obsidian Energy Ltd. management does get credit for navigating a company through some tough times with a weak balance sheet. But now is the time to go for profits while that time lasts. Management appears to have a weak spot there. As such, the weak Obsidian Energy Ltd. pricing is likely to last a while longer.

For further details see:

Obsidian Energy Is Trying To Get To Easy Street