CA - Obsidian Energy Will Boost Output By 50% But I'd Prefer Lower Debt

2023-12-28 10:30:00 ET

Summary

- Obsidian Energy plans to increase its output by 50% by the end of 2026, with a focus on heavy oil production.

- The company reported a net income of C$24.8M for Q3, with a pre-tax income of almost C$33M.

- Obsidian Energy's production growth plan for 2024-2026 includes a tripling of heavy oil production and a decrease in light oil production.

Introduction

As it has been over a year since I last discussed Obsidian Energy ( OBE ) ( OBE:CA ), I wanted to have another look at this oil and NGL producer, especially after it announced plans to increase its output by 50% by the end of 2026. Additionally, the main focus will be on increasing the output of heavy oil, which will represent about half of the production mix. An interesting move, even more so as the heavy oil price has recently been in rough shape.

While Q3 was good, the capex will increase sharply in Q4

During the third quarter, the company produced almost 33,000 barrels of oil-equivalent per day with approximately 38% of the equivalent output consisting of light oil with heavy oil representing just under 20% of the oil-equivalent output.

{kind=link}

The heavy oil was sold at an average realized price of just over C$80/barrel , while the company fetched almost C$110 per barrel of light oil it produced and sold. The total revenue generated during the third quarter was approximately C$200M, resulting in a net revenue of C$180M after also taking the royalty payments into account.

{kind=link}

Obsidian's production cost is still pretty low, and the low transportation expenses are also a blessing. The company reported a pre-tax income of almost C$33M and as you can see in the image above, in excess of a third of the total operating expenses were related to depreciation and depletion expenses.

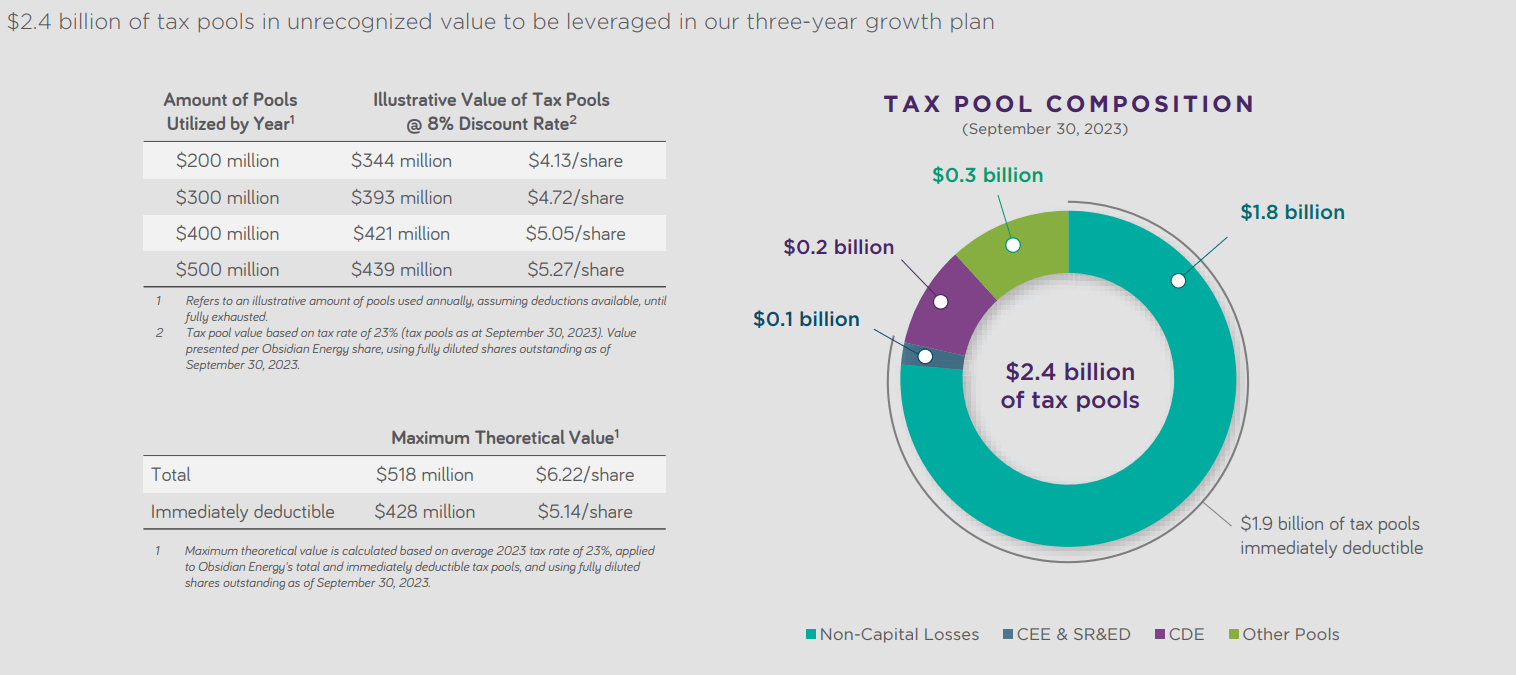

The net income was C$24.8M for an EPS of C$0.31 per share. That's a good result for a company that is trading with a sub-C$10 share price, but I was also expecting the free cash flow result to be higher than the reported net income as the company has access to billions of dollars in tax pools. Obsidian mentioned it won't have to pay any cash taxes for at least the next decade, using $75 WTI as a base case scenario.

{kind=link}

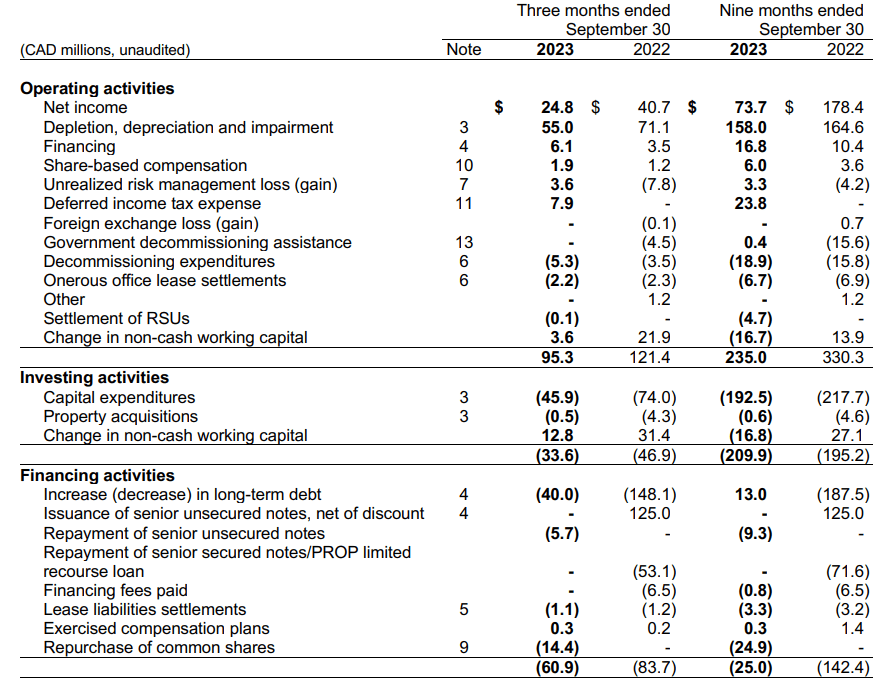

During the third quarter, the operating cash flow came in at C$95.3M, but this included a C$3.6M working capital release and excluded the C$1.1M in lease payments. This means the underlying operating cash flow was approximately C$90.5M. This includes the deferred tax expenses as no cash tax payments will be owed in the foreseeable future.

{kind=link}

The total capex was C$46.5M, resulting in a net free cash flow result of C$44M during the third quarter. Looking at the 9M results, the adjusted free cash flow was C$56M as the company's first semester was pretty capex-heavy. The full-year capex was reaffirmed at C$300M which means the final quarter of the year will be pretty capex-heavy and that explains why the year-end net debt position is estimated to increase to C$310M compared to just C$295M at the end of the third quarter. The company-provided net debt guidance includes the working capital deficit.

I am intrigued by the three-year production growth plan

The company recently also announced its production plans for the 2024-2026 era. As you can see below, the company expects to increase its output to 36,000 boe/day in 2024 followed by further increases to 42,000 boe/day in 2025 and 50,000 boe/day in 2026 .

{kind=link}

Interestingly, Obsidian is focusing on heavy oil production as it will see its light oil production rate decrease by approximately 5% while the production of heavy oil will almost triple between 2024 and 2026.

That decision made sense in September as the WCS differential versus the WTI benchmark oil price was pretty low over the summer, but this differential has widened in the past few months to the point where heavy oil producers are hurting somewhat.

Fortunately, Obsidian also published a sensitivity analysis and the table below is coming in pretty handy.

{kind=link}

Just to be clear, the company used a WTI oil price of US$75 and a WCS differential of US$15/barrel, which means the assumed realized heavy oil price is US$60/barrel. While that may be a reasonable long-term price, the current WCS price is trading slightly below $60/barrel, after dipping as low as $50/barrel earlier this month. The future looks slightly better though as the WCS price expressed in USD is quoted in the high-50s range for delivery over the summer. This means Obsidian's guidance is definitely still valid, although slightly optimistic based on the current situation (which can obviously change very fast).

If we pull up the guidance for 2025 we see Obsidian is expecting an FFO of C$515M and a free cash flow result of C$47M based on a C$445M capex budget. If I would assume a WTI oil price of US$72.50 and a realized WCS price of US$55/barrel, the FFO would decrease by approximately C$60M and Obsidian would be slightly free cash flow negative.

Of course, the negative free cash flow status would be entirely caused by the investment in production expansion. Assuming the 25% decline rate will remain stable (that's what Obsidian has been guiding for), I expect the sustaining capex to remain at a steady-state production rate of 42,000 boe/day to be around C$250-275M. This means that applying the oil prices mentioned above, the updated FFO of C$455M would still very generously cover the C$275M capex requirement. In the situation above, the sustaining free cash flow would be approximately C$180M or C$2.25/share based on a share count of 80 million shares.

Investment thesis

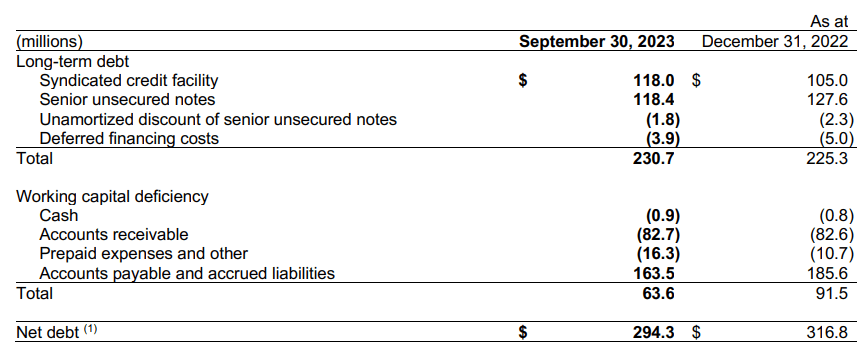

While I appreciate Obsidian's plans to grow its production rate within its financial means, I'm not sure it is the best capital allocation at this point in time. With a net debt that will likely exceed C$300M at the end of this year, perhaps a more moderate production growth plan would be more appropriate as the cost of debt is pretty high.

{kind=link}

While one could argue the net financial debt is just C$230M, the cost of debt exceeds 12% as the company paid in excess of C$7M in interest payments. About half of the debt consists of an 11.95% senior unsecured note maturing in 2027 while there is a C$118M credit facility. While I understand the desire to boost the output, repaying the credit facility would save the company close to C$15M per year in interest expenses.

I currently have no position in Obsidian Energy, but I am considering initiating a speculative long position. While I like the cash flow projections, I'd prefer to see more cash going towards debt reduction. I would love to be a creditor, but unfortunately, none of my brokers allow me to trade in the 11.95% 2027 unsecured notes. As part of my plan to initiate a long position, I will likely write some put options that are just out of the money.

For further details see:

Obsidian Energy Will Boost Output By 50% But I'd Prefer Lower Debt