CA - October's Top 10 High Yield Stocks To Boost Your Dividend Income

2023-10-03 18:00:00 ET

Summary

- When aiming to reach a diversified investment portfolio with a reduced risk level, I suggest reaching a balanced mix between high dividend yield and dividend growth companies.

- High dividend yield companies can be an attractive extra source of income, which you can use to cover your monthly expenses.

- In today’s article, I have selected 10 high dividend yield companies that I believe are attractive right now due to a variety of reasons.

- The selected picks have an attractive Valuation, significant competitive advantages and are financially healthy, helping you to increase the probability of making successful investment decisions over the long term.

Investment Thesis

Companies that pay a high Dividend can provide you with excellent opportunities to increase your monthly income. However, they should be selected carefully in order to ensure that the dividends they pay you are sustainable. Sustainable dividend payments can help you to reduce the risk level when investing and they can help you obtain a more reliable income in the form of dividends.

In today's article, I will introduce you to 10 high dividend yield companies that I believe are attractive right now due to a variety of reasons: they have a relatively high Dividend Yield [FWD], have shown Dividend Growth in recent years, have a relatively low Valuation, and are financially healthy in addition to having significant competitive advantages. These characteristics can help you to increase the probability of making successful investment decisions when investing over the long term.

However, when building an investment portfolio, I suggest aiming for a mixed balance between high dividend yield and dividend growth companies in addition to having a portfolio with a reduced risk level, and therefore, increasing the probability of steadily raising your wealth. This strategy helps you to always be in control of your investments and means that you can care much less about stock market fluctuations. I am implementing this investment approach through the construction of The Dividend Income Accelerator Portfolio .

Below you can find the selection process of the 10 selected high dividend yield companies you could consider investing during this month of October.

Since I have already described this process in a previous article , if you are already familiar with it you can skip the following section written in italics.

First step of the Selection Process: Analysis of the Financial Ratios

In order to identify companies with a relatively high Dividend Yield [FWD], I use a filter process to make a pre-selection. From this pre-selection, I will later choose my top 10 high Dividend Yield companies of the month. To be part of this pre-selection of high Dividend Yield stocks, the companies should fulfil the following requirements:

- Market Capitalization > $10B.

- Dividend Yield [FWD] > 2.5%.

- P/E [FWD] Ratio < 30.

In the following, I would like to specify why I have chosen the metrics mentioned above in order to select my top 10 high Dividend Yield stocks of the month.

A Market Capitalization of more than $10B contributes to the fact that the risks attached to your investments are lower, since companies with a higher Market Capitalization tend to have a lower volatility than companies with a low Market Capitalization.

A P/E [FWD] Ratio of less than 30 implies that the price you pay for the company is not extraordinarily high, thus filtering out those that have stock prices in which high growth expectations are priced in. High growth expectations imply strong risks for investors, since the stock price could drop significantly. Again, the filtering process helps us to reduce the risk so that we are more likely to make an excellent investment decision.

Second step of the selection process: Analysis of the Competitive Advantages

In a second step, the companies' competitive advantages (for example: brand image, innovation, technology, economies of scale, etc.) are analyzed in order to make an even narrower selection. I consider it to be particularly important for companies to have strong competitive advantages in order to stand out against the competition in the long term. Companies without strong competitive advantages have a higher probability of going bankrupt one day, thus representing a strong risk for investors to lose their invested money.

Third step of the selection process: The Valuation of the companies

In the third step of the selection process, I will dive deeper into the Valuation of the companies.

In order to conduct the Valuation process, I use different methods and criteria, for example, the companies' current Valuation as according to my DCF Model, the expected compound annual rate of return as according to my DCF Model and/or a deeper analysis of the companies' P/E [FWD] Ratio. These metrics should serve as an additional filter to only select companies that currently have an attractive Valuation, which helps you to identify companies that are at least fairly valued.

The Fourth and final step of the selection process: Diversification over Industries and Countries

In the fourth and final step of the selection process, I have established the following rules for choosing my top picks: in order to help you diversify your investment portfolio, a maximum of two companies should be from the same industry. In addition to that, there should be at least one pick that is from a company that is based outside of the United States, serving as an additional geographical diversification.

My Top 10 High Dividend Yield Stocks to Invest in for October 2023

- Altria Group ( MO ).

- Boston Properties ( BXP ).

- Philip Morris ( PM ).

- Phillips 66 ( PSX ).

- Realty Income ( O ).

- Rio Tinto ( RIO ).

- Royal Bank of Canada ( RY ).

- The PNC Financial Services Group ( PNC ).

- United Parcel Service ( UPS ).

- Verizon Communications ( VZ ).

Overview of the 10 selected high dividend yield companies to consider investing in for October 2023

| MO |

| BXP |

| PM |

| RIO |

| PNC |

| O |

| UPS |

| RY |

| PSX |

| VZ |

| Company |

| Altria Group |

| Boston Properties |

| Philip Morris |

| Rio Tinto |

| The PNC Financial Services Group |

| Realty Income |

| United Parcel Service |

| Royal Bank of Canada |

| Phillips 66 |

| Verizon Communications |

| Sector |

| Consumer Staples |

| Real Estate |

| Consumer Staples |

| Materials |

| Financials |

| Real Estate |

| Industrials |

| Financials |

| Energy |

| Communication Services |

| Industry |

| Tobacco |

| Office REITs |

| Tobacco |

| Diversified Metals and Mining |

| Diversified Banks |

| Retail REITs |

| Air Freight and Logistics |

| Diversified Banks |

| Oil and Gas Refining and Marketing |

| Integrated Telecommunication Services |

| Country |

| United States |

| United States |

| United States |

| United Kingdom |

| United States |

| United States |

| United States |

| Canada |

| United States |

| United States |

| Market Cap |

| 74.69B |

| 10.48B |

| 145.49B |

| 104.57B |

| 48.83B |

| 36.38B |

| 131.85B |

| 125.39B |

| 53.55B |

| 139.41B |

| Dividend Yield [FWD] |

| 9.31% |

| 6.57% |

| 5.55% |

| 5.61% |

| 5.06% |

| 6.00% |

| 4.20% |

| 4.45% |

| 3.49% |

| 8.02% |

| Payout Ratio |

| 75.96% |

| 53.75% |

| 86.10% |

| - |

| 41.07% |

| 74.06% |

| 55.33% |

| 47.90% |

| 21.79% |

| 53.05% |

| Dividend Growth 3 Yr [CAGR] |

| 3.98% |

| 0.26% |

| 2.75% |

| 1.36% |

| 9.56% |

| 4.07% |

| 16.94% |

| 7.36% |

| 4.60% |

| 1.99% |

| P/E GAAP [FWD] |

| 9.08 |

| 24.01 |

| 16.88 |

| 8.32 |

| 9.3 |

| 38.84 |

| 16.45 |

| 11.74 |

| 7.34 |

| 7.29 |

| Revenue 3 Year [CAGR] |

| 0.42% |

| 3.03% |

| 4.39% |

| 7.85% |

| 17.09% |

| 32.09% |

| 7.52% |

| 7.55% |

| 20.63% |

| 1.34% |

| EBIT 3 Year [CAGR] |

| 1.85% |

| 0.37% |

| 3.22% |

| 4.40% |

| - |

| 23.02% |

| 14.39% |

| - |

| 76.59% |

| -0.65% |

| Net Income Margin |

| 33.13% |

| 20.99% |

| 24.26% |

| 16.39% |

| 29.80% |

| 23.51% |

| 10.41% |

| 27.28% |

| 7.07% |

| 15.58% |

| 60M Beta |

| 0.62 |

| 1.15 |

| 0.74 |

| 0.7 |

| 1.13 |

| 0.79 |

| 1.09 |

| 0.79 |

| 1.37 |

| 0.33 |

Source: Seeking Alpha

Altria Group

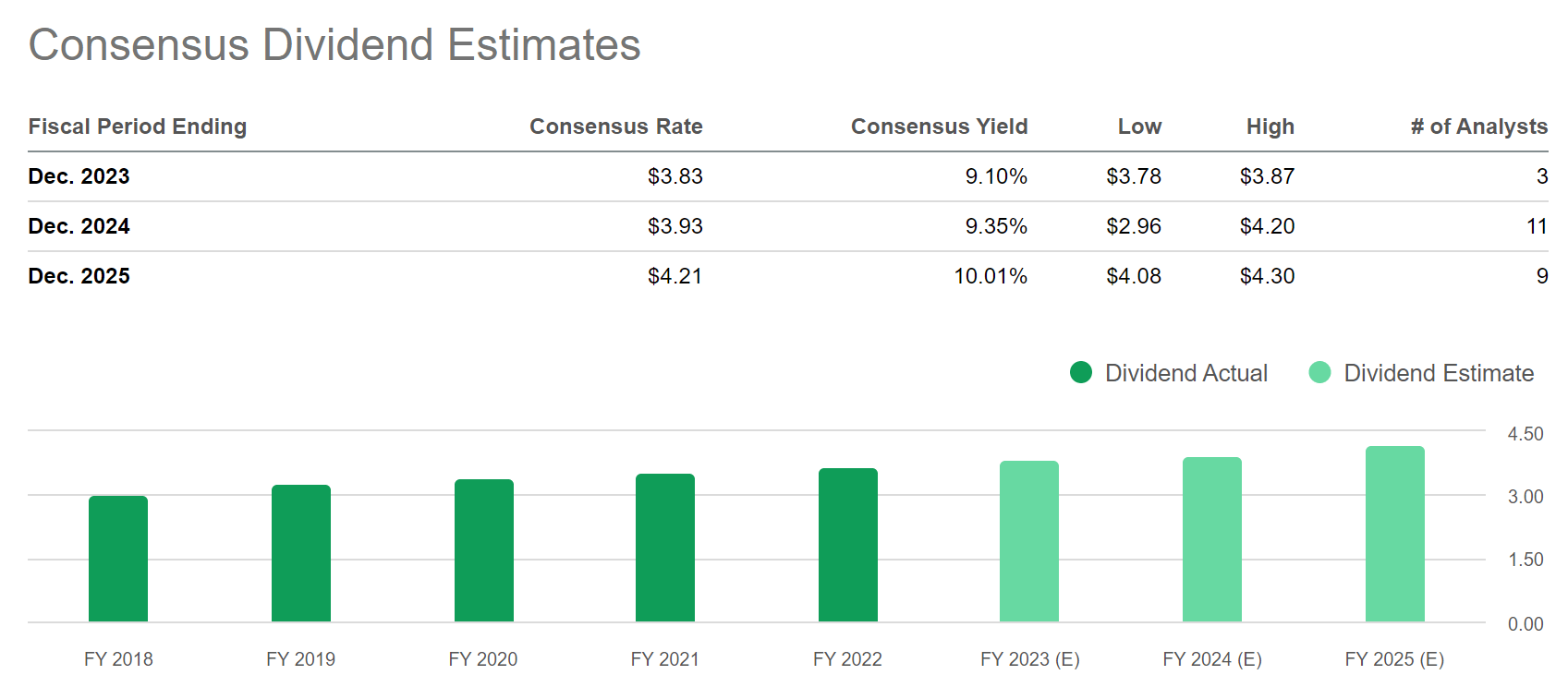

At Altria's current share price of $42.11, the company offers its shareholders an impressive Dividend Yield [FWD] of 9.31%. I firmly believe that this Dividend Yield is appealing for dividend income investors, especially when considering that Altria has shown a Dividend Growth Rate [CAGR] of 5.85% within the past 5 years and that its Payout Ratio currently stands at 75.96%. The company's Payout Ratio at its present level gives me confidence that its Dividend is relatively safe (even though not entirely safe).

Below you can find Consensus Dividend Estimates for the company. Analysts estimate a Consensus Yield of 9.10% for 2023, 9.35% for 2024, and 10.01% for 2025. These Analyst Estimates strongly underscore my thesis that Altria is an ideal pick for investors seeking dividend income while aiming to increase this amount on an annual basis.

{kind=link}

Furthermore, I believe that Altria's current Valuation is favorable, with a P/E [FWD] Ratio of 9.08. Altria's current P/E [FWD] Ratio stands 51.69% below the Sector Median of 18.79, suggesting that the company is undervalued at its current price level. This reinforces my investment thesis that Altria is currently an appealing choice for dividend income investors.

Boston Properties

Boston Properties is a manager of premier workplaces in the United States. The company was established in 1970. At this moment in time, Boston Properties has 780 employees and a Market Capitalization of $10.48B.

At the time of writing, the company offers shareholders a Dividend Yield [FWD] of 6.57%. It has shown a Dividend Growth Rate [CAGR] of 4.47% over the past 5 years, indicating it can help you to blend dividend income with dividend growth. The company's Payout Ratio stands at a relatively low level of 53.75%. This mix between dividend income and dividend growth in combination with a relatively low Payout Ratio makes the company an appealing pick for those who want to generate extra income in the form of dividends.

Boston Properties currently has a P / AFFO [FWD] Ratio of 11.49, which stands 13.74% below the Sector Median of 13.32, suggesting that the company is undervalued at this moment in time.

My thesis that the company is currently an appealing choice for investors is underlined by the Seeking Alpha Quant Ranking, in which Boston Properties is placed 5th out of 23 within the Office REITs Industry and 37th out of 173 within the Real Estate Sector.

Source: Seeking Alpha

Philip Morris

I have just added Philip Morris to The Dividend Income Accelerator Portfolio. One of the reasons for deciding to include it in this portfolio are the company's strong competitive advantages and its appealing mix between dividend income and dividend growth.

Philip Morris has a Dividend Yield [FWD] of 5.55% and has provided investors with a Dividend Growth Rate [CAGR] of 3.89% over the past 10 years.

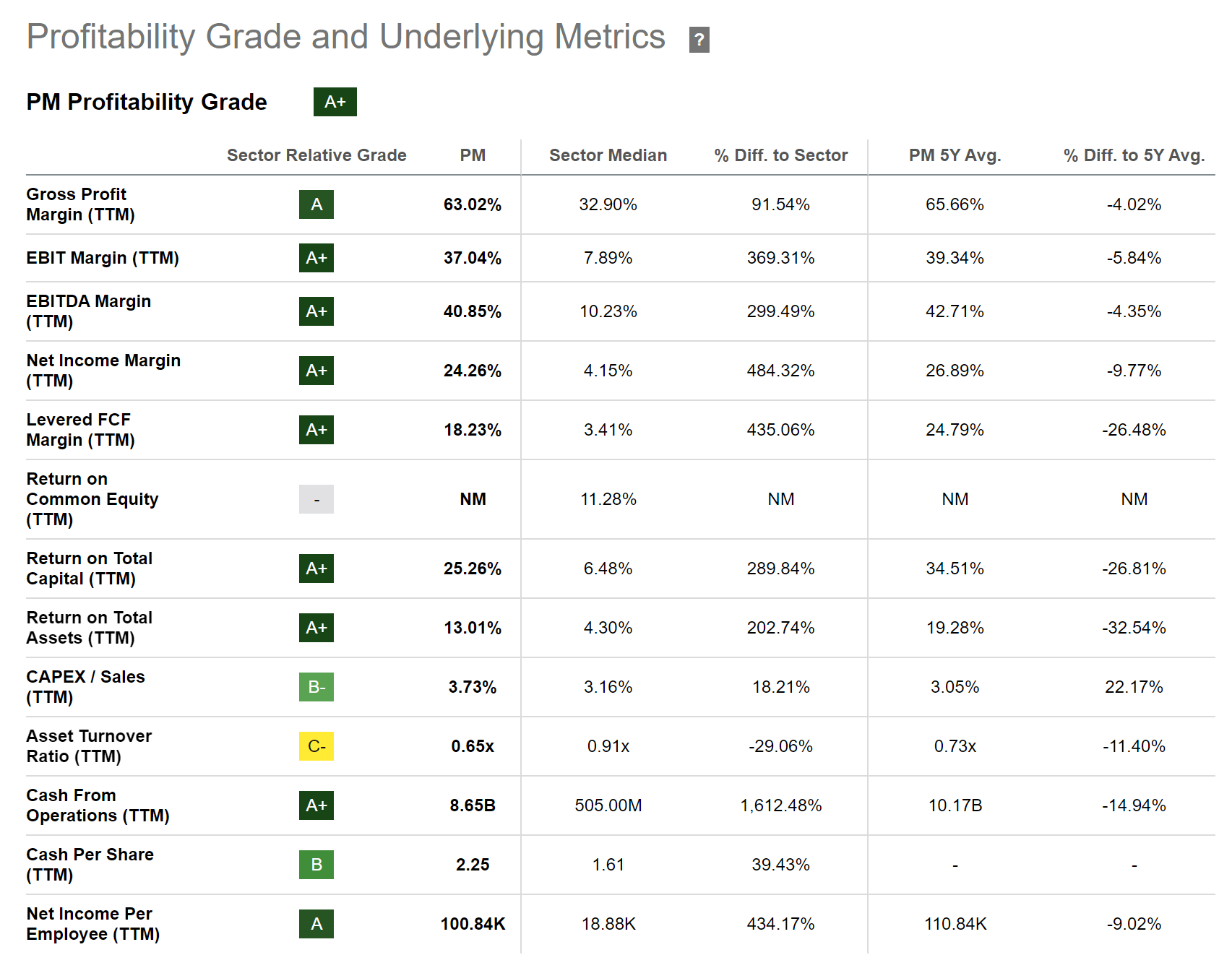

Furthermore, I believe that Philip Morris is an excellent pick in terms of Profitability. The company has an EBIT Margin [TTM] of 37.04%, which stands significantly above the Sector Median of 7.89%. The company's Net Income Margin [TTM] of 24.26% stands 484.32% above the Sector Median, further confirming its strong Profitability. The same is confirmed when having a look at the Seeking Alpha Profitability Grade for Philip Morris, which you can find below.

{kind=link}

I have discussed the reasons for including the company in The Dividend Income Accelerator Portfolio in the following article:

Realty Income

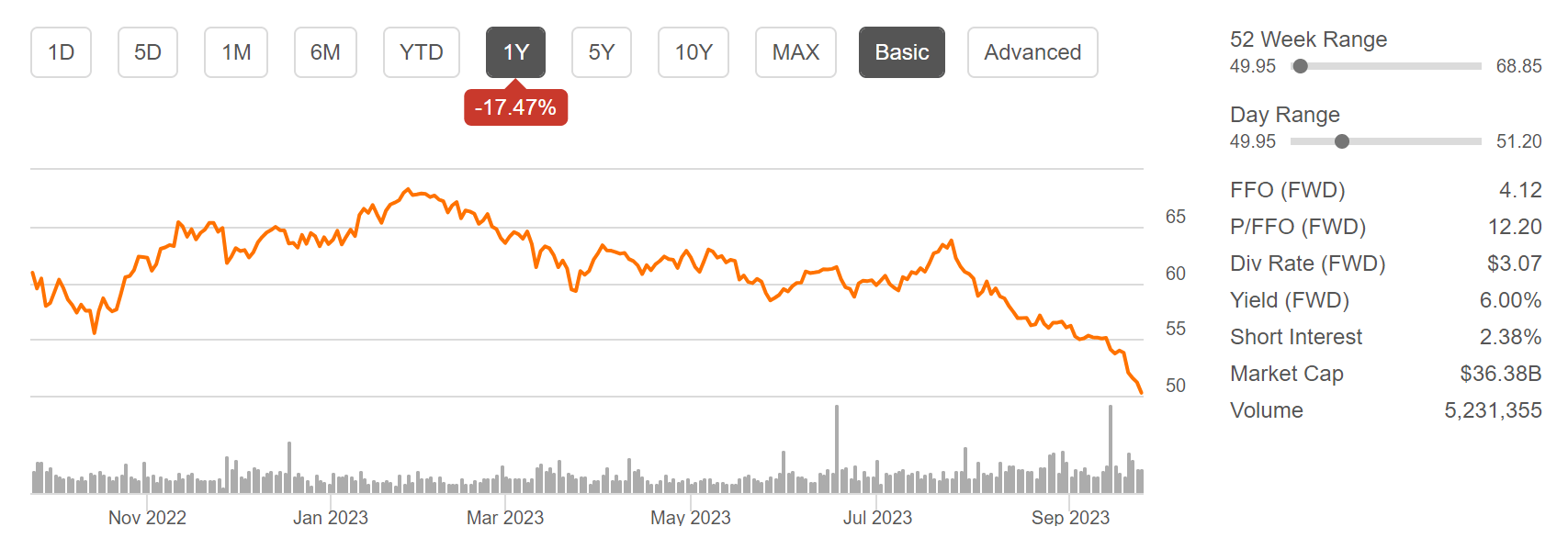

Realty Income has registered a decline of -17.47% within the past 12-month period. This weak performance has contributed to the fact that the company is now available for an even more attractive price for investors. The graphic below shows Realty Income's performance over the past 12-month period.

{kind=link}

Realty Income currently has a P/AFFO [FWD] Ratio of 12.83, which lies 3.69% below the Sector Median. In my opinion, however, Realty Income should be rated with a premium when compared to its competitors. This is because of the company's broad diversification and its enormous financial health (Realty Income has an A3 credit rating from Moody's and an EBIT Margin [TTM] of 40.11%, which stands 89.50% above the Sector Median).

Below you can find a detailed analysis on Realty Income, in which I have explained why I added the company to The Dividend Income Accelerator Portfolio:

Realty Income: A Strong Alignment With The Dividend Income Accelerator Portfolio Approach

Rio Tinto

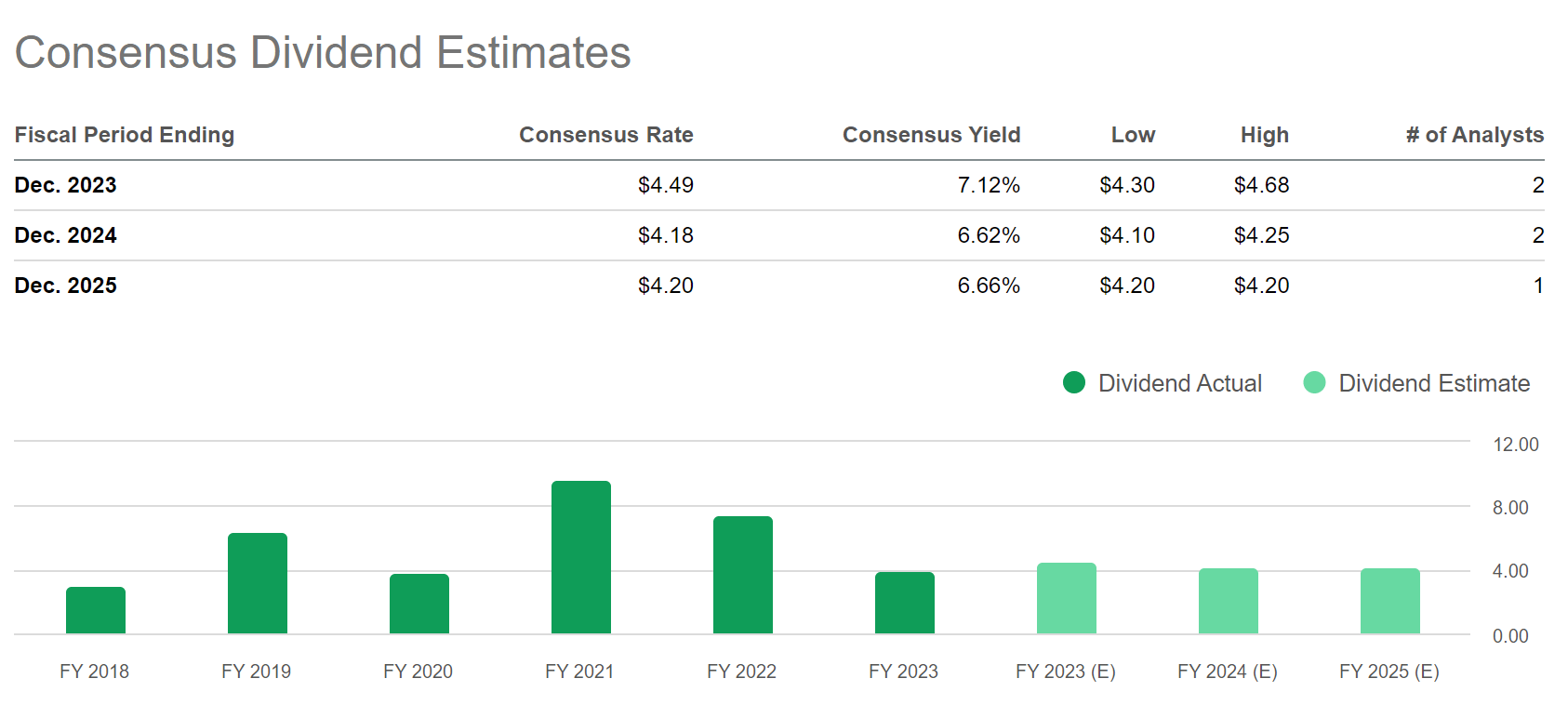

Rio Tinto is a company from the Diversified Metals and Mining Industry that was founded in 1873. At its current price level of $62.01, the company pays its shareholders a Dividend Yield [FWD] of 5.61%. Rio Tinto has shown a Dividend Growth Rate 5Y [CAGR] of 5.48%, as well as 16 Consecutive Years of Dividend Payments.

Below you can discover the Consensus Dividend Estimates for Rio Tinto, which are: 7.12% for 2023, 6.62% for 2024 and 6.66% for 2025.

{kind=link}

Rio Tinto currently has a P/E [FWD] Ratio of 8.32, which is 42.28% below the Sector Median, suggesting that the company is undervalued at this moment in time.

The PNC Financial Services Group

The PNC Financial Services Group currently has a P/E [FWD] Ratio of 9.30, which is 1.21% below the Sector Median and 22.49% below its Average from the past 5 years. Both metrics indicate that the company is undervalued.

In terms of Profitability, I see the company as being ahead of its competitors. This is proven by its Net Income Margin [TTM] of 29.80%, which lies 15.60% above the Sector Median. It is further underscored by the company's Return on Equity of 14.09%, which is 24.66% above the Sector Median.

I further consider the company to be an attractive pick when it comes to Growth: The PNC Financial Services Group has shown an EBIT Growth Rate [FWD] of 8.85%, which stands 109.96% above the Sector Median of 4.22%.

Below you can find the results of the Seeking Alpha Dividend Grades, suggesting that the company is an attractive pick not only for dividend income investors, but also for dividend growth investors. The company receives an A rating for Dividend Safety and for Dividend Consistency. For Dividend Yield, it receives a B rating, and for Dividend Growth, a B- rating.

Source: Seeking Alpha

United Parcel Service

United Parcel Service was founded in 1907 and currently has a Market Capitalization of $131.85B.

The company's strength in terms of Profitability is reflected in its high Return on Equity of 55.16%, which is significantly above the Sector Median of 13.60%, as well as its high EBIT Margin [TTM] of 12.38%, which stands 27.03% above the Sector Median.

I further believe that UPS is currently undervalued. This theory is supported by the company's P/E [FWD] Ratio of 16.45, which stands 15.40% below the Sector Median.

UPS' Free Cash Flow Yield [TTM] of 4.65% strengthens my belief that the company is an attractive risk/reward choice, since it indicates that its current share price is not based on high growth expectations. This helps us invest with a lower risk level, increasing the probability of making successful investment decisions when investing over the long term.

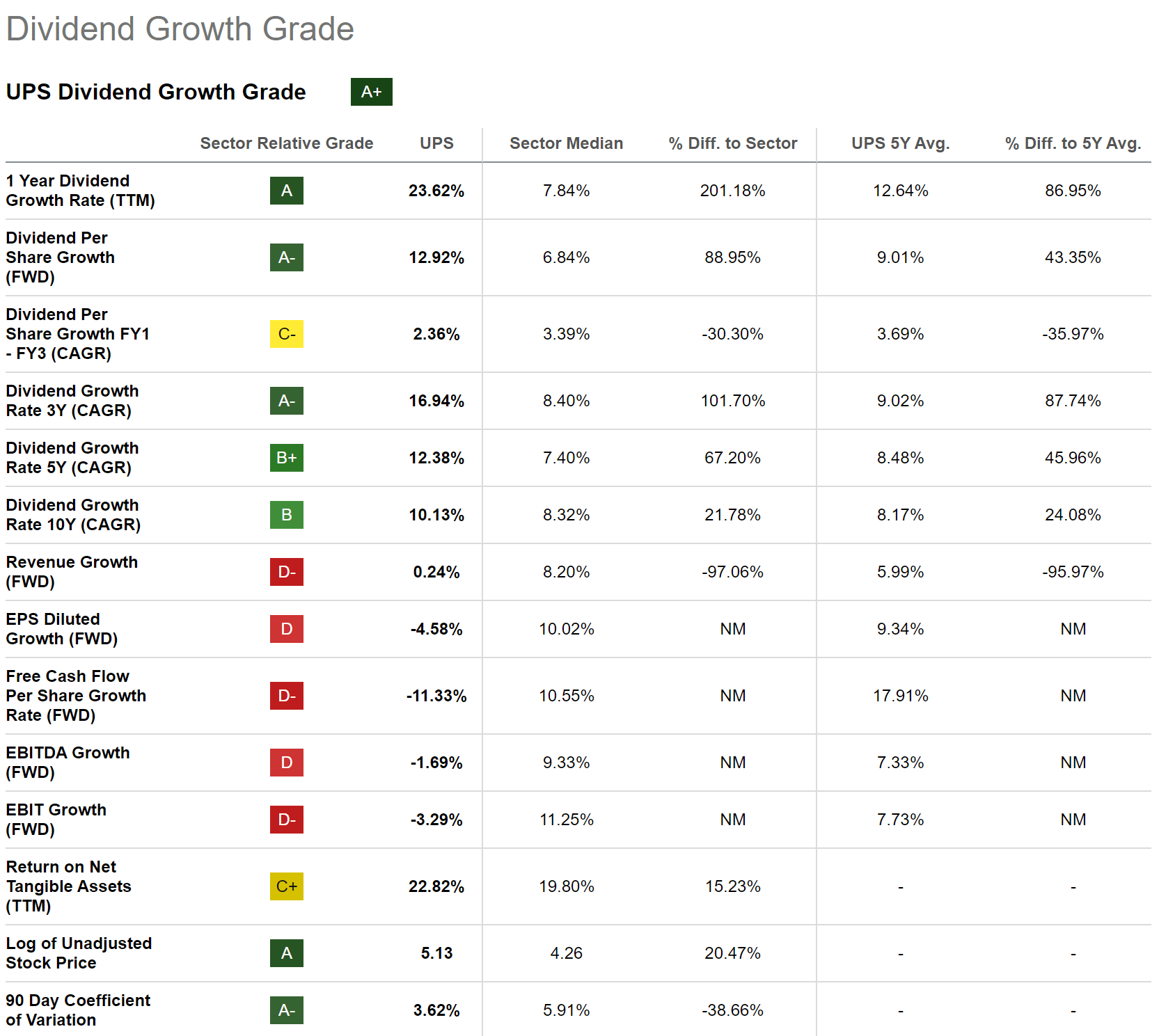

UPS currently has a Dividend Yield [FWD] of 4.20% and a Payout Ratio of 55.33%, which shows that there is plenty of room for dividend enhancements in the future. It is also worth mentioning that UPS has shown a Dividend Growth Rate [CAGR] of 16.94% over the past 3 years, making the company an excellent choice to blend dividend income with dividend growth.

Below you can find the Seeking Alpha Dividend Growth Grade for UPS, which underscores the company's strength in terms of Dividend Growth.

{kind=link}

Royal Bank of Canada

Royal Bank of Canada currently has a P/E [FWD] Ratio of 11.74, which is slightly below its Average from the past 5 years (which is 11.84). This comparison shows that the Canadian bank is at least fairly valued.

Furthermore, the bank shows strong metrics when it comes to Profitability: its Return on Equity of 14.26% is significantly above the Sector Median of 11.30%. In addition to that, it can be highlighted that Royal Bank of Canada's Net Income Margin of 27.28% is also above the Sector Median (which is 25.78%).

Furthermore, I strongly believe that Royal Bank of Canada is an attractive pick when aiming to combine dividend income with dividend growth: this is the case due to the bank's Dividend Yield [FWD] that currently stands at 4.45% and its 3 Year Dividend Growth Rate [CAGR] of 7.37%. It is also worth mentioning that the bank's Payout Ratio of 47.90% leaves enough room for future dividend enhancements.

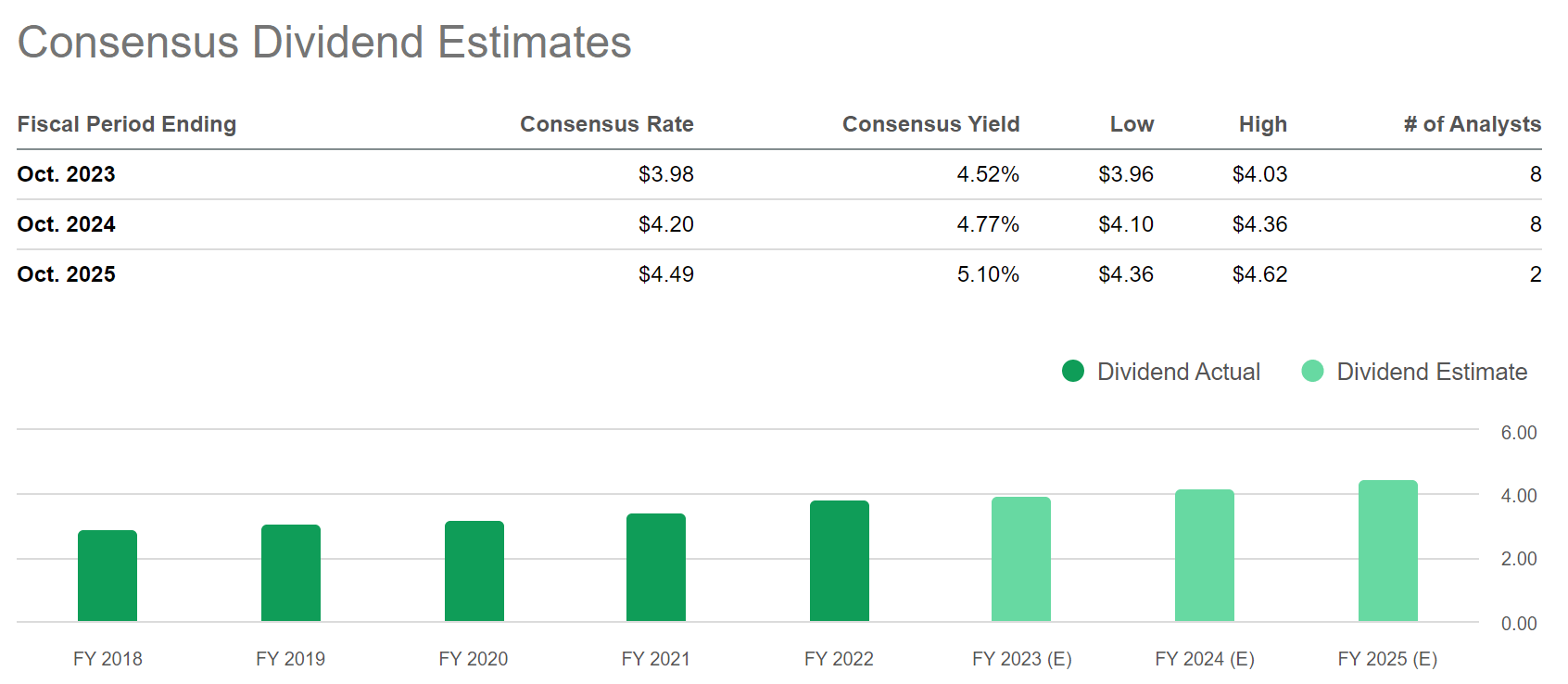

Below you can find the Consensus Dividend Estimates for Royal Bank of Canada. Consensus Dividend Estimates are 4.52% for 2023, 4.77% for 2024, and 5.10% for 2025. These Estimates strengthen my investment thesis that Royal Bank of Canada is attractive for you as an investor when looking for an investment to combine dividend income and dividend growth.

{kind=link}

I have recently added Royal Bank of Canada to The Dividend Income Accelerator Portfolio. Below is a link to my detailed analysis on Royal Bank of Canada:

Royal Bank Of Canada: The Fourth Buy For The Dividend Income Accelerator Portfolio

Phillips 66

Phillips 66 is a company from the Oil and Gas Refining and Marketing Industry that was founded in 1875. I believe that the company is currently available at an attractive price level for investors: its current P/E [FWD] Ratio stands at 7.34, which is 30.65% below the Sector Median of 10.58.

When comparing Phillips 66 to companies such as ExxonMobil (NYSE: XOM ) and Chevron (NYSE: CVX ), it can be highlighted that Phillips 66 has the significantly lower Valuation: while Phillips' 66 P/E [FWD] Ratio stands at 7.34, ExxonMobil's is 12.90, and Chevron's is 12.44.

The company's Free Cash Flow Yield [TTM] stands at 13.63% and strengthens my theory that Phillips 66 is an attractive risk/reward pick for investors.

The company currently pays a Dividend Yield [FWD] of 3.49% while it has a Payout Ratio of 21.79%, which further strengthens my belief that there is enough room to increase the dividend in the future. This makes the company an appealing pick when striving to combine dividend income and dividend growth.

Below you can find the results of the Seeking Alpha Quant Ranking, underscoring my theory that this could be an excellent moment to add Phillips 66 to your investment portfolio. The company is ranked 4th out of 22 within the Oil and Gas Refining and Marketing Industry, and 11th out of 245 within the Energy Sector. Within the Overall Ranking, Phillips 66 is ranked 72nd out of 4661.

Source: Seeking Alpha

Verizon

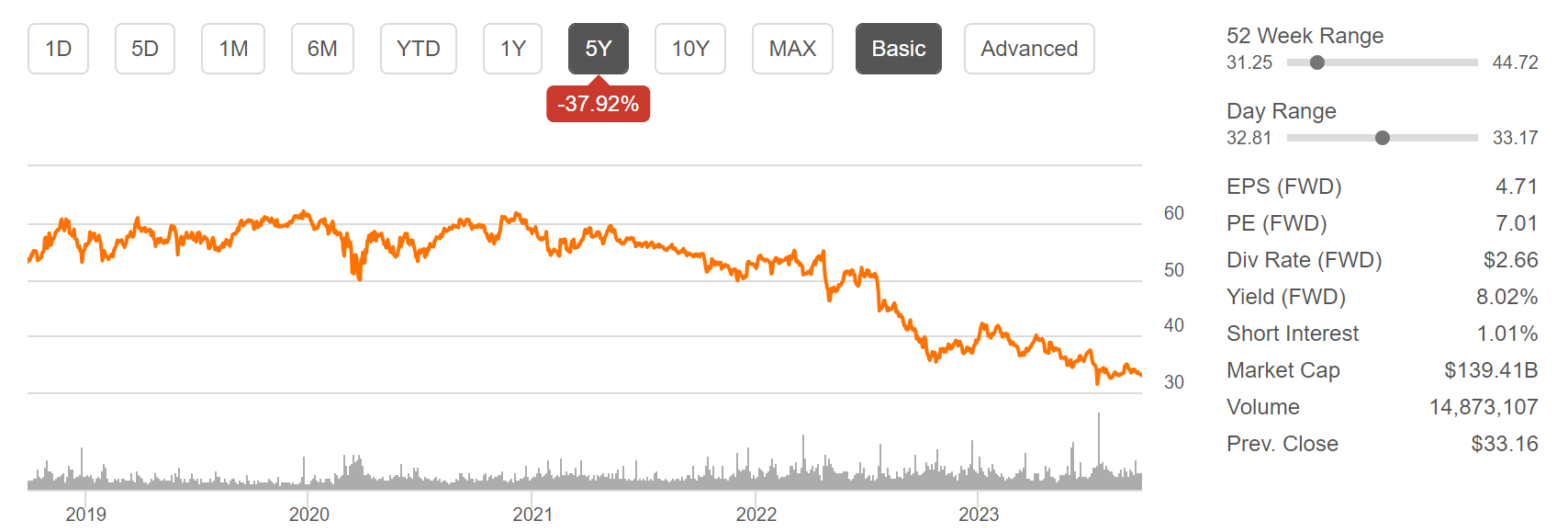

Within the past 5 years, Verizon has shown a performance of -37.92%.

{kind=link}

Verizon's weak performance implies that the company is now available at an attractive price level: its P/E [FWD] Ratio of 7.29 is not only 54.74% below the Sector Median, but also 32.87% below its Average from the past 5 years. Both metrics underline my investment thesis that Verizon is currently undervalued.

The largest benefits I see for Verizon investors is the company's high Dividend Yield [FWD] of 8.02% and its relatively low Payout Ratio of 53.05%. This strengthens my belief that the company won't cut its dividend in the near future, thus making it an excellent pick to combine dividend income and dividend growth.

When compared to competitor AT&T (NYSE: T ), it can be highlighted that Verizon has the slightly higher Dividend Yield [FWD] (8.02% compared to AT&T's of 7.39%) and has shown higher Dividend Growth Rates (while Verizon's 5 Year Dividend Growth Rate [CAGR] stands at 2.03%, AT&T's is -5.88%).

However, due to the company's relatively high Total Debt to Equity Ratio of 188.91% and its relatively limited growth perspective (Revenue Growth Rate [FWD] of 0.52%), I suggest underweighting the Verizon position in an investment portfolio.

Conclusion

I believe that a well-balanced dividend-oriented investment portfolio should consist of a mixture of high dividend yield and dividend growth companies as well as a reduced risk level, in order to increase the probability of achieving excellent investment results over the long term. I am implementing this approach with the construction of The Dividend Income Accelerator Portfolio.

In today's article, I have introduced you to 10 high dividend yield companies that I consider to be currently attractive for investors due to the fact they have an attractive Valuation, significant competitive advantages, a strong financial health and have shown Dividend Growth in recent years.

These kinds of companies can be particularly useful as they help to generate a large amount of extra income and contribute to covering your monthly expenses. At the same time, some of these picks can help you mitigate the downside risk of your portfolio (6 out of the 10 selected companies have a Beta Factor below 1 and can therefore help to protect your portfolio during a stock market decline).

I believe that these high dividend yield companies could further contribute to raising the Weighted Average Dividend Yield of your portfolio while boosting its dividend income, thus helping you potentially accumulate wealth.

However, you should always keep in mind to strive for a balanced portfolio in order to accumulate your wealth with a high probability and continuously limit the downside risk of your investment portfolio.

With a well-balanced and low-risk portfolio you will be able to steadily accumulate your wealth. By periodically rebalancing your portfolio, you can achieve excellent investment results when investing over the long term.

Author's Note: I would appreciate hearing your opinion on my selection of high dividend yield companies to consider buying in October 2023. Do you already own or plan to acquire any of the picks? Which are currently your favorite high dividend yield companies?

For further details see:

October's Top 10 High Yield Stocks To Boost Your Dividend Income