OCN - Ocwen Financial Corporation: Need More To Make This A Buy

2023-07-18 10:48:14 ET

Summary

- Ocwen Financial Corporation reported a net loss of $40 million in Q1 2023, impacted by a $39 million reduction in unrealized MSR fair value due to lower interest rates.

- Despite cost reduction measures resulting in over $100 million less operating expenses, the company's ROE is negative, and its EPS results have been inconsistent over the past 5 years.

- With the current challenges in the mortgage industry, particularly the rise in interest rates, the company is considered a hold for investors until proof of improvement is shown in future quarterly reports.

Introduction

Ocwen Financial Corporation (OCN), is a company operating as a financial service company in the United States, India, and also the Philippines. They have divided the business into two different segments which make up the revenues, those being Servicing and Originations.

It provides mortgage loan services but seems to have had some difficult last few quarters. In Q1 of 2023, the net loss was $40 million, driven by a $39 million reduction in unrealized MSR fair value, impacted by lower interest rates. Liquidity has improved however and now sits at $233 million. But those positives aren't enough to justify a buy here for investors. Rather, a hold rating seems to be the most appropriate. Without a dividend, and based on the valuation of the sector, I find the risks suppress a buy case right now.

Company Structure

As we have learned, OCN is made up of two different segments , those being Servicing and Originations. Ocwen was founded back in 1988 and has grown steadily since, but boasts a rather small market cap of just $225 million. What investors should be aware of is the fact that OCN has a TTM negative ROE currently. This seems to have been affected by the fact that the fair value of mortgage service rights is decreasing. It seems reasonable to assume that this might continue for the short term and result in a low ROE.

Diving deeper though into the company structure, they offer mortgage loans and services associated with it. Apart from this they have some asset management services and reverse conventional and government-insured mortgage loans. OCN also engages with originating and purchasing conventional and government-insured mortgage loans.

{kind=link}

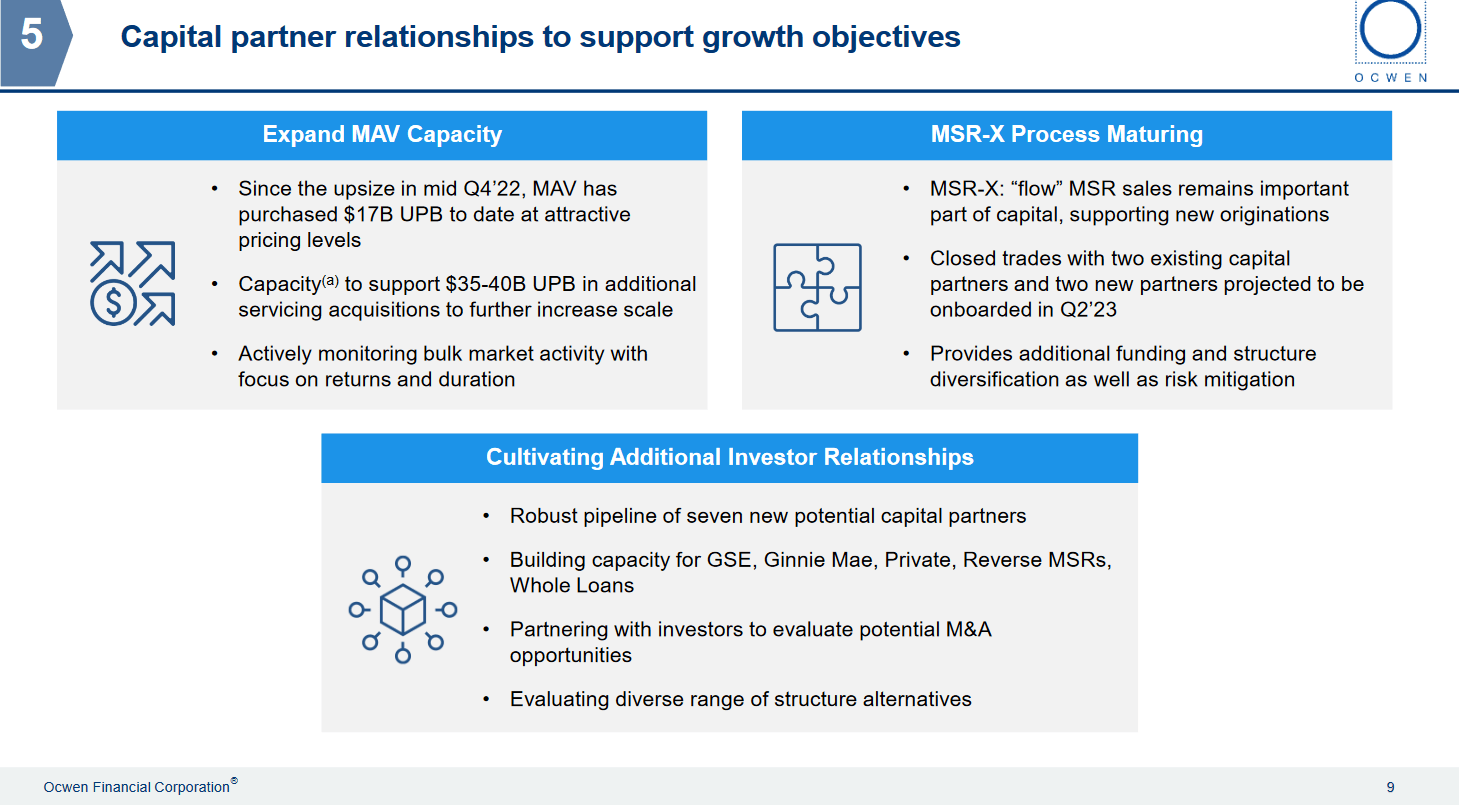

OCN sees a lot of potential in this market and is expanding further into MAV capabilities. They have since just Q4 2022 purchased an additional $17 billion of UPB at what they find to be very attractive levels. But the expanded capacity is making room for an additional $35 - $40 billion of additional service acquisitions. This scalability could transform into a significant tailwind for the business I think, but time will tell, and right now it still feels like a bet.

Fundamentals

As said earlier, the ROE of OCN is rather disappointing, and negative when using the TTM numbers. The financials sector sits at an average of 11.1% and OCN has a negative 15.2%. This paints the picture that the company has been largely unsuccessful in properly capitalizing on what they have grown. Total equity is at $416 million as of the last report, down a large amount from the highs of $1.8 billion back in 2013.

Growth Rates (Seeking Alpha)

This has over the years led to a rather disappointing path of growth, or lack of growth, seeing as the revenues have on average decreased by 0.99% in the last decade.

EPS History (Seeking Alpha)

Apart from that, the EPS results have also been quite inconsistent over the last 5 years. Estimates might be positive for 2024, but as we have seen historically, OCN has very much underperformed expectations. In 2022 for example when EPS estimates sat at over $11 per share, OCN posted $2.85 instead. That sort of discrepancy should result in a lower valuation as the company comes off as risky.

Earnings Transcript

On May 4 , OCN posted its earnings report and listening to the earnings call some comments caught my attention.

"We continue to drive growth in our servicing portfolio with total UPB and subservicing up versus the fourth quarter of 2022. We are seeing the benefits of our cost reduction actions with total operating expenses down in the first quarter, over $100 million annualized versus the second quarter of 2022. Total liquidity of $233 million is up 7% versus the fourth quarter of 2022, and we continue to take a prudent view of our liquidity and capital, given interest rate and economic volatility, potential cash consumption from our increased MSR hedge coverage position, and market risks and opportunities."

I think that OCN taking significant cost reduction measurements could result in the earnings estimates being somewhat achievable. EPS estimates are though very optimistic and 2024 has a median estimate of $14 per share. Which would value OCN at under 3x earnings. but if the coming quarters in 2023 post similar cost reduction effectiveness then it might happen. Although as I said, I am somewhat skeptical. A higher ROE needs to be achieved as well, a negative one just isn't acceptable.

Risk Associated

In the ever-changing landscape of the mortgage industry, the current scenario poses unique challenges, particularly with the persistent elevation in interest rates. As inflationary pressures loom, the question arises: how well-prepared is the industry to navigate potential further increases in interest and mortgage rates?

Inflation Rate US (tradingeconomics)

The impact of rising rates can reverberate across the housing market, affecting homebuyers, homeowners seeking refinancing options, and lenders alike. As rates climb, the affordability of homes can be compromised, potentially leading to a slowdown in demand for new mortgages. Additionally, existing homeowners may find it less advantageous to refinance their mortgages, impacting the overall loan volume.

Investor Takeaway

OCN has seen a difficult quarter it seems as the net income was negative by $40 million. That puts pressure on coming quarters to deliver strong results. The share price hasn't been trending higher, but rather the opposite in 2023 so far. But OCN still has a p/e higher than the sectors right now at just above 11. I think the lackluster last report doesn't help a buy case. Even if estimates are very positive towards the company, I think proof needs to be shown before a buy case can be made. I appreciate the cost reduction measures the company has taken which seemingly resulted in over $100 million less operating expenses when compared to Q1 in 2022. I find OCN to be a hold for now though, and will be watching it carefully in the upcoming quarterly reports.

For further details see:

Ocwen Financial Corporation: Need More To Make This A Buy