RDFN - Offerpad Solutions: Flawed Business Model Insiders Selling Out Positions

2023-06-28 12:21:42 ET

Summary

- Insiders Selling their position, most notably, Offerpad co-founder Jerry Coleman.

- Flawed Business Model: This is reflected in unprofitable operations and no clear path to profitability.

- The exit of Redfin and Zillow from the iBuyers market, coupled with nearly two decades of negative earnings by Offerpad and Opendoor, serves as sufficient evidence to deem this model troublesome.

- The iBuyer Business Model is a money loser even in a bull real estate market.

- Company became publicly traded via Special Purpose Acquisition Company (SPAC), raising numerous red flags.

Introduction:

Offerpad Solutions Inc (OPAD) is not my usual cup of tea for pre-revenue biotechnology companies. Nonetheless, I became aware of this company during the regional CFA Stock Pitch competition and have decided to share my insights.

In my assessment, I strongly believe that this company holds no significant value. Its share price was trading at less than $1 before the reverse stock split in June and is now trading at approximately $10 per share. I have conducted a comprehensive analysis with various supporting factors, which I will present in descending order of significance.

- Insider Sell-Off: A worrisome pattern emerges as substantial shares are being sold by insiders, including Offerpad Co-founder Jerry Coleman and the sponsor, Supernova Partners LLC, which facilitated OPAD's transition to a publicly traded company.

- SPAC: The utilization of a Special Purpose Acquisition Company (SPAC) for its transition into a publicly traded stock is reason for caution.

- Flawed Business Model: Over the past 8 years, the company's inability to achieve positive net income highlights fundamental flaws in its business model. Additionally, the exit of Zillow and Redfin from the iBuyers market further supports this.

Considering these factors, I am convinced that the company's worth is effectively zero, warranting caution from potential investors.

Insiders Dumping Stock

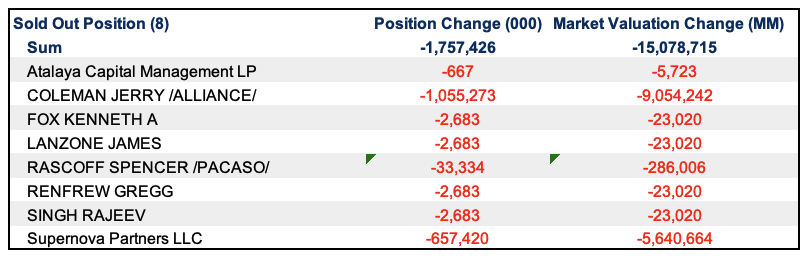

In the past six months, several OPAD insiders have completely sold off their positions, resulting in the sale of a total of 1.8 million shares (equivalent to 7% of outstanding shares) with a market value of 15 million USD. Of particular note is the co-founder of Offerpad, Jerry Coleman, who liquidated 1,055,273 shares (valued at approximately $9 million). Furthermore, during the first quarter of 2023, Supernova Partners LLC (the sponsor of the SPAC that facilitated Offerpad's public listing) and some of its key management also sold their entire holdings in OPAD. Notably, this includes Spencer Rascoff, co-founder of Zillow.

{kind=link}

Figure 1:OPAD Ownership Activity.

Special Purpose Acquisition Company (SPAC)

Companies that have gone public through SPACs tend to be highly risky. In this section, I will delve into the reasons behind this assertion.

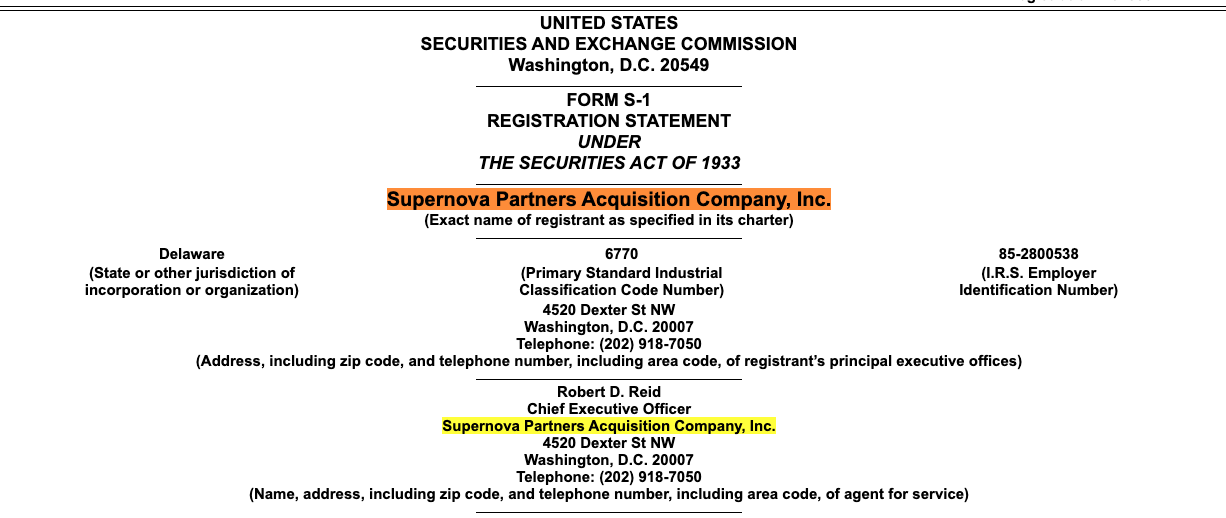

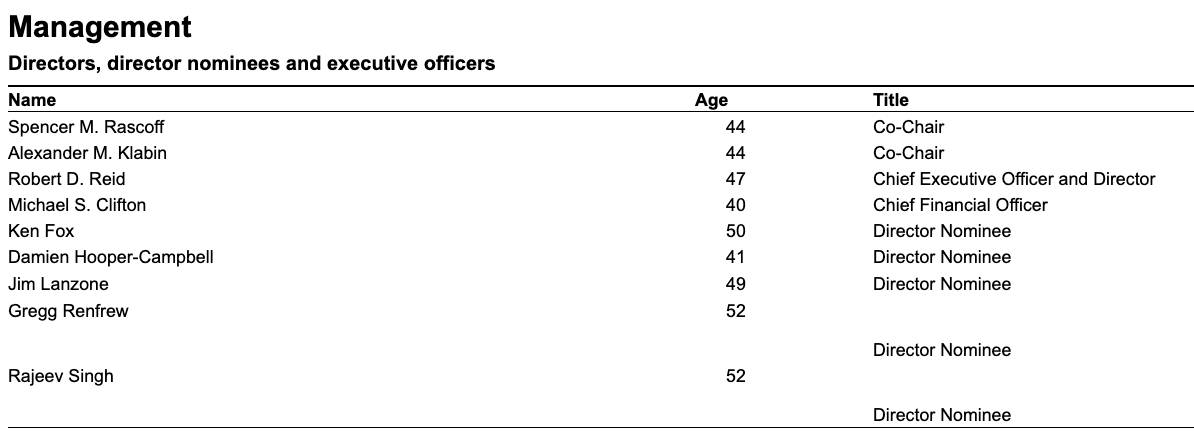

Supernova Partners LLC served as the sponsor of the SPAC (Special Purpose Acquisition Company) which played a crucial role in facilitating OPAD's transition into a publicly traded company (Figure 2). Figure 3 shows the management team behind Supernova Partners Acquisition Company, LLC, the SPAC that merged with the former Offerpad. Essentially, a SPAC acts as the vehicle through which a target company, such as OPAD, merges and becomes publicly traded. The sponsor assumes the responsibility of creating the SPAC.

{kind=link}

Figure 2: Supernova Partners Acquisition Company, Inc.

{kind=link}

Figure 3: Supernova Partners Acquisition Company, LLC Management.

No Skin in the Game:

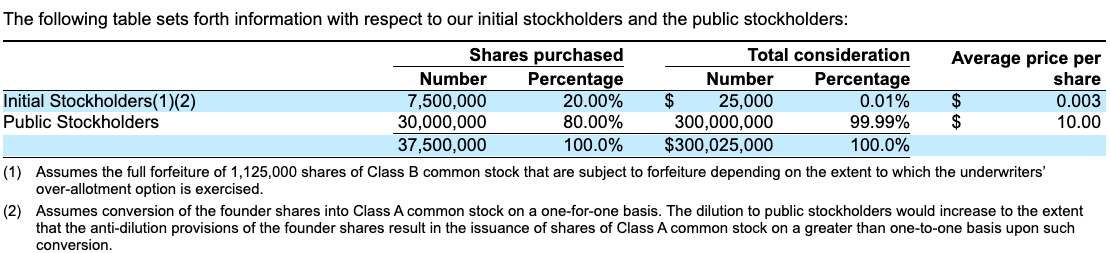

SPAC sponsors, in this instance Supernova Partners LLC, typically obtain a 20% equity stake in the company (Figure 4), for pennies on the dollar. In the case of OPAD, Supernova Partners LLC acquired a one-fifth equity stake in the company for a mere $25,000 (averaging $0.003 per share), as shown below. SPAC managers are indifferent towards the quality of the target company, as they enjoy all the potential upside without bearing any of the risks.

{kind=link}

Figure 4: SPAC Stockholders (Source: SEC.gov; From S-1)

In a 2020 study examining SPAC performance between 2019 and the first half of 2020, the findings revealed that while the creators of SPACs often experienced success, their investors tend to not fare as well. Public stockholders that buy the SPAC shares for $10/share are often the real losers.

It's a Pattern

There are two other SPACs sponsored by Supernova Partners LLC.

1. Supernova Partners Acquisition Company II, Ltd ( SPACII ): This SPAC successfully found a target company to combine with Regetti Computing, Inc. ( RGTI ).

2. Supernova Partners Acquiring Company III, Ltd which Failed to find a target company. SPACs usually have 18-24 months to find a target company, if not they must redeem the stocks back to investors.

In Conclusion, the pattern is evident: Supernova Partners LLC, and its managers, consistently introduce companies to the public markets through SPACs, while investing minimal capital (~$25,000) and obtaining a 20% equity stake in the company. The quality of the company and the asset is in question when a group gets all the upside and none of the downside. This point is better explained by Warren Buffett in this interview . As a general rule, I refrain from investing in companies that go public via SPACs due to the inherent risks involved. And the fact that they are all selling out their position in OPAD is alarming.

Flawed Business Model

Many will argue that timing and macroeconomic conditions are the culprits in OPAD's consistently negative net income, however, in reality, there are multiple flaws in the business model that make it almost impossible to reach or sustain profitability. I will discuss the main ones here.

Strong Revenue Growth, Yet Profitability Stagnates:

Over the past six years, OPAD has doubled its revenue annually, yet this has not been translated to profitability metrics. After 8 years of operation, the question remains: Is the iBuyer business model truly profitable?

This company faces significant challenges regarding profitability and its underlying business model. Despite a substantial 99% year-over-year revenue growth over the past 4 years, it has consistently failed to achieve positive net income, with the exception of an insignificant 0.19% net income margin in 2021. This translates to approximately $4 million in net income out of $2 billion in revenue. Over the past 11 quarters of operations, the company had negative net incomes in 9 out of those 11 (Table 1).

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Gross Profit Margin |

| 6.91% |

| 8.25% |

| 10.04% |

| 4.62% |

| Operating Profit Margin |

| -3.10% |

| -1.29% |

| 0.95% |

| -3.22% |

| Net Income Margin* |

| -4.83% |

| -2.17% |

| 0.19% |

| -4.36% |

Table 1: Annual OPAD Profitability Metrics (Source: Company 10k Filings)

| Q3 2020 |

| Q4 2020 |

| Q1 2021 |

| Q2 2021 |

| Q3 2021 |

| Q4 2021 |

| Net Income Margin* |

| -1.58% |

| -0.59% |

| -0.08% |

| 2.43% |

| -0.39% |

| -0.33% |

| Q1 2022 |

| Q2 2022 |

| Q3 2022 |

| Q4 2022 |

| Q1 2023 |

| Net Income Margin* |

| 2.57% |

| -0.09% |

| -9.98% |

| -18.38% |

| -9.75% |

Table 2: Quarterly OPAD Profitability Metrics (Source: Company 10Q Filings)

The best indicator of enhanced profitability is the Spread, which is the difference between the average selling price and the average cost per home. The spread is positively correlated with profitability, serving as the margin for OPAD to generate profits. When the spread increases, it leads to enhanced profitability metrics, while a decrease in the spread has the opposite effect. The reason for the dichotomy between revenue and profits is that the company's revenue growth is tied to price appreciation (macroeconomic factors) and not efficient operations.

| Offerpad Solutions Inc |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Revenue Per Home (%change) |

| $233,497 |

| $229,889 (-2%) |

| $248,600 (8%) |

| $324,878 (31%) |

| $371,633 (14%) |

| Cost of Revenue Per Home (%change) |

| $215,521 |

| $213,995 (-1%) |

| $228,097 (7%) |

| $292,269 (28%) |

| $354,480 (21%) |

| Spread (%change) |

| $17,976 |

| $15,895 (-11.58%) |

| $20,504 (29%) |

| $32,609 (59%) |

| $17,153 (-47%) |

Table 3: Offerpad Solutions Spread from 2018 to 2022. (Offerpad Financial Statements)

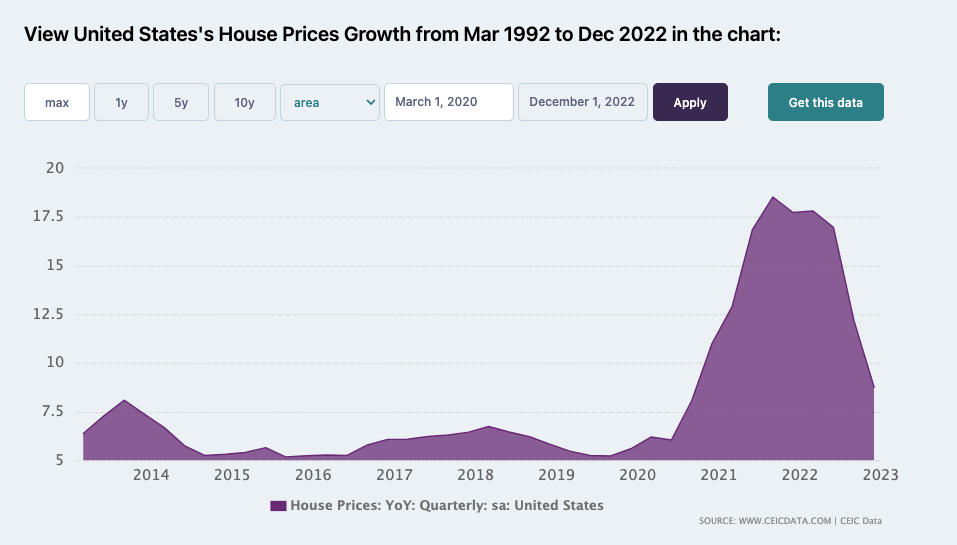

Offerpad has been operating in a bull real estate market (Figure 5) for the past 3 years. Even at the peak of this bubble, where OPAD's average resell price rose by 31% (Table 3), the company could not even manage a significant profit. The iBuyers model is a money loser even in a bull real estate market.

{kind=link}

Figure 5: House Price Growth in USA Y-O-Y.

No Room for Profit:

The crucial question is how this company can achieve profitability. To make the iBuyers business model lucrative, there are two primary methods: both involving increasing the spread.

1. Increase the selling price per unit:

To accomplish this, iBuyers must sell at a premium, which is no easy task. According to a 2019 analysis of over 20,000 iBuyer transactions, iBuyers achieve a median price appreciation of 3.3% (the difference between their purchase price and resale price). Demanding a premium on a home is challenging. Although OPAD's median revenue per home has been increasing and has fueled OPAD's revenue growth, this has been driven by macroeconomic conditions, i.e. the real estate bubble.

2. Decrease costs per unit:

To achieve this, iBuyers must acquire homes at a discounted price and sell them at market value or above. However, in reality, iBuyers tend to purchase properties very close to the market price. According to the same aforementioned study, iBuyers were found to acquire homes at 98.6% of the Automated Valuation Model (AVM) estimation.

In conclusion, the company has no pricing power in either the purchase or sell of homes. This issue is complicated by the inaccuracies of the Automated Valuation Model (AVM) upon which iBuyers rely for making offers, thereby introducing an additional layer of risk to the entire business model. For further insights into this matter, I refer you to the following article by The Wall Street Journal.

Added Expenses:

The iBuyers business model adds additional expenses not usually associated with traditional brokerages.

- Interest Expense: iBuyers use debt to finance their cash offer, which results in an added interest expense. Interest expense per unit for FY 2022 was $4324.

- Renovation Expense: OPAD appears to be the only one insisting on costly renovations. Quoting OPAD CEO Brian Bair ( Q3 2022 Earnings Call ):

What you want to do, you can make money through your service fee and by maximizing the price of your home through renovation.

Lack of Economies of Scale:

A major drawback to the iBuyers business model is the lack of economies of scale. Despite an increasing volume of home purchases, Offerpad has not witnessed substantial profits or improved margins.

- Between 2020 and 2021 , Offerpad's home purchases and sales grew by 48.9% (2,092 homes), and the SG&A per unit increased by 26.3% ($5,780 per house).

- Similarly, between 2021 and 2022 , despite a 67% rise in home purchases (4,262 houses), the SG&A per unit remained unchanged at ~$27,000/unit sold.

This illustrates that Offerpad's costs and expenses have remained fixed on a per-unit base and do not decrease as the number of units bought and sold increases. In reality, it has increased as the company scales its operations.

Zillow & Redfin Exit the Market:

The exit of Zillow and Redfin is empirical evidence of the failure of the iBuyers business model.

Redfin Corporation (RDFN) launched RedfinNow, the iBuying branch, in 2017 in California and was shut down in late 2022. In a very recent article , Redfin's CEO reflected on the iBuyers model saying:

"I probably should have closed the iBuying business earlier, ... It shouldn't have taken a housing market correction to realize how capital-intensive and risky that was."

Zillow entered the iBuyers market in 2017 and exited in Q4 of 2021. It only took a 900M loss for Zillow to exit. Zillow CEO, Rich Barton, explaining his reasoning for exiting the iBuyers market ( Q3 2021 Earnings Call ):

This decision was not taken lightly, especially considering the hard work and commitment from the Zillow Offers team. But ultimately, we determined that further scaling up Zillow Offers is too risky, too volatile to our earnings and operations, too low of a return on equity opportunity and too narrow in its ability to serve our customers, a tough but necessary determination... When we decided to take a big swing on Zillow Offers 3.5 years ago, our aim was to become a market maker, not a market risk taker.

Risks

1. Bankruptcy Risk:

The iBuyer Business Model is very capital-intensive and operates in a volatile market. The risk of bankruptcy is significant.

- The Current Ratio as of Q1 2023 is 1.82, meaning the company can cover its short-term liabilities. The Quick Ratio on the other hand is 0.86 which increased due to a decrease in inventory.

- The Interest Coverage Ratio as of March 23 (LTM) was at -4.84 indicating an inability to cover interest expenses with its earnings.

2. Dilution Risk:

The stock was trading at around $0.55/share before the reverse stock split that took place on June 8th, in which the stock is now trading at $10/share. There is a significant risk of dilution. OPAD has a history of negative cash flows that are expected to persist in the foreseeable future. The company is capital-intensive and heavily relies on debt and equity financing to support its operations.

In a Nutshell

There are multiple red flags with this company that I would rate this stock as a STRONG SELL . Considering that macroeconomic impacts will likely persist in the foreseeable future and the continued failure of their business model, I believe the company will file for bankruptcy by the end of the year. The main reasons are:

- Insiders liquidating their position: Including the co-founder of Offerpad and the managers of Supernova Partners LLC.

- Disproven business model: The exit of Zillow and Redfin is clear evidence of the failure of this business model.

- Profitability: The company has never been profitable over its 8-year history with no clear path to profitability. In fact, no iBuyer has ever been profitable.

For further details see:

Offerpad Solutions: Flawed Business Model, Insiders Selling Out Positions