COM - Oil Prices Are Likely To Rise From Here

2023-03-23 08:30:00 ET

Summary

- Oil prices took a hit over the past few days, driven by concerns over the health of the economy.

- Prices have started to recover, but investors need to pay attention to the bigger picture.

- There are mixed signals in the space right now, but a full assessment of the space indicates that a bullish outlook is more likely the accurate approach to take now.

After a stellar 2022 fiscal year, where energy prices remained elevated, 2023 looked like it was slating up to be a rather difficult year for crude. After ending 2022 at $80.16 per barrel, crude prices plunged to under $70 per barrel as investors feared a potential glut, as well as broader economic concerns that could reduce the demand for it. Although prices are still quite low compared to where they began the year at, we did start to see what could be considered a recovery in just the past couple of days. In particular, on March 21st, WTI crude prices rose $1.86, which equals 2.75%, to close at $69.50. Whether or not this recovery will continue ultimately will be determined by the data. But the data that's out there today is rather conflicting at face value. It's only once you dig deeper that you start to understand why a bullish stance on crude and, in turn, a bullish stance on the companies that benefit from it, still makes logical sense.

Mixed results

Although oil markets are global and can be subjected to countless influences, it wouldn't be a surprise to many investors to say that the recent leg lower in pricing was the result of concerns over the global banking crisis that has developed. I say this because, on March 10th when a lot of this news began to surface that there was trouble brewing, WTI crude prices closed at $76.68. That was only marginally lower than the $80.16 per barrel that they traded at the end of 2022. By March 15th, prices had bottomed out at $67.61 per barrel. That's a drop in just a few days of 11.8%. Since then, stabilization in that market has helped push prices up about 2.8% to $69.50 per barrel as of this writing.

{kind=link}

It makes sense why energy prices would be susceptible to changes in the perception of the economy. In 2019, global oil consumption averaged 101.23 million barrels per day. In 2020, average daily consumption plunged to 91.80 million barrels per day. Though to be fair, this drop that was undoubtedly caused by the shuttering of the global economy in response to the COVID-19 pandemic could be considered something of an outlier since it was largely imposed by governments across the planet. A more appropriate comparison would be the 2008 and 2009 financial crisis. From 2008 to 2009, global demand fell about 1.7%, totaling 1.4 million barrels per day. And again, that was the worst collapse we have seen since the Great Depression.

If global oil markets had the opportunity to respond rapidly to changes in demand, then price volatility would not be as great as it is. But because oil production is often the product of significant amounts of capital that's planned months in advance and, in the case of the US, is subjected to market forces as opposed to the whims of the government, there can be a great deal of time between when expectations change and when market supply adjusts. This is further complicated by other actors in the space, most notably OPEC+.

As it became more likely that the world might be able to mitigate current banking issues, thanks to the combination of government and central bank interference, as well as the willingness of certain financial institutions to sweep in and pick up the assets of the banks that have failed, markets allowed the subsequent rise in oil prices to occur. But investors would be wise to ask themselves whether or not prices actually deserve to climb back up from where they dropped to. After all, WTI crude prices have been at or above the $70 range consistently since December of 2021. One thing that we do know is that high prices ultimately lend themselves to significant investments aimed at pushing production even higher. In time, a glut can form that can have profound ramifications on all market participants and that has the potential to last for years. That is why prices remained below $70 per barrel for much of the time between late 2014 and late 2021.

What the state of the energy market looks like depends on whom you ask. There are two primary sources of information that investors should rely heavily on when evaluating the state of the market. The first of these is the EIA (Energy Information Administration). Using data from the most recent STEO (Short-Term Energy Outlook) that was published earlier this month, we can see that their estimate is that global supply in the first quarter of 2023 should be around 100.73 million barrels per day. That compares to 99.94 million barrels per day worth of consumption capacity. Although this may not seem like much of a difference, such a spread existing for an entire year would cause global inventories to climb 288.35 million barrels.

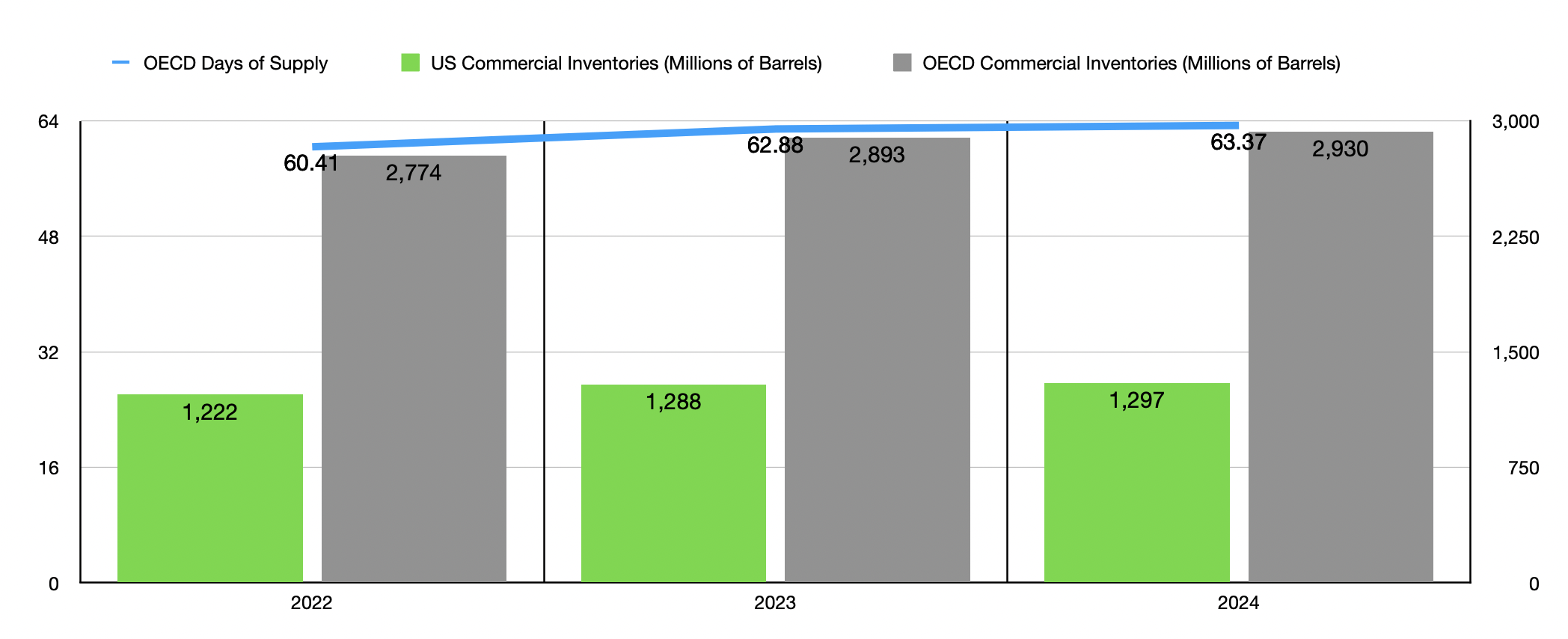

For 2023 as a whole, it's estimated that the amount of production in excess of demand should be around 0.57 million barrels per day. That should bring OECD commercial inventories up to 2.89 billion barrels by the end of the year. That's up from the 2.77 billion barrels at the end of 2022. Even though global demand should rise to 102.69 million barrels per day next year compared to the 100.90 million barrels per day forecasted for this year, global supply should also increase. If the forecast is accurate, this should cause OECD commercial inventories to climb further to 2.93 billion barrels. Some of this increase will undoubtedly be driven by higher production from the US. In 2022, domestic production was 11.88 million barrels per day. That should grow to 12.44 million barrels per day this year before hitting 12.63 million barrels per day in 2024. As a result, commercial inventories here at home should also increase, ultimately climbing from 1.22 billion at the end of 2022 to nearly 1.30 billion at the end of next year.

One of the best ways to measure whether we have a glut or not forming is to look at the days' worth of consumption held in OECD commercial inventories. Generally speaking, a range of between 55 days and 60 days suggests that the market is appropriately balanced. For 2022, that number was 60.41 days. By the end of this year, it's forecast to decline to 62.88 days before hitting 63.37 days in 2024. Such a small disparity may not seem material. But using the estimate for 2024 would imply a global glut of 156 million barrels. For context, if you look at the report released by the EIA back in June of 2017, the forecast translated to 63.40 days' worth of consumption held in inventories. And back then, WTI crude prices were consistently below $50 per barrel.

{kind=link}

The other source that we should be paying attention to is, surprisingly, OPEC itself. In the years I spent looking at oil data, I found their own reports to be some of the most accurate. They do not provide a forecast of their own production beyond what has been announced publicly. But they do tend to have really solid estimates when it comes to the rest of the world. For 2023, they have the data broken up into quarters. If we assume that the amount of production that they are responsible for remains unchanged moving forward, we could very well be experiencing an excess of crude today. That should peak at 0.30 million barrels per day in the second quarter of this year. But by the fourth quarter, we could be experiencing a shortfall of 1.18 million barrels per day. All told, 2023 could result in global crude inventories plunging about 126.16 million barrels if OPEC does not adjust its production accordingly and if their forecasts for the rest of the world turn out to be accurate.

{kind=link}

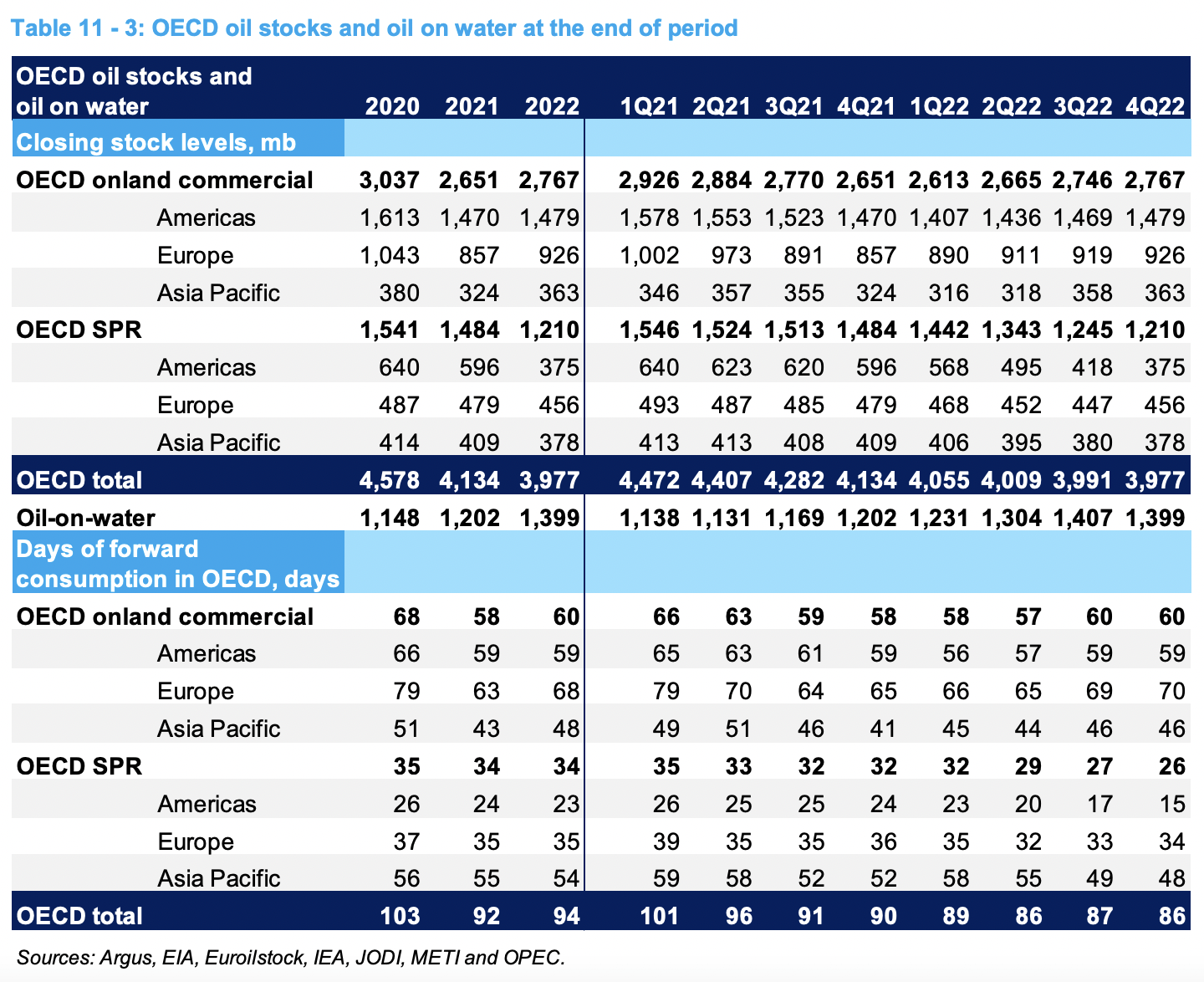

This would be great to see if you are an oil bull. After all, we have been seeing exactly the opposite up until this point based on the data provided by OPEC. At the end of 2022, for instance, total commercial OECD inventories came out to 2.77 billion barrels. That was up from 2.65 billion barrels reported one year earlier. That number excludes the amount of oil on water. That includes oil and transit, as well as oil that's being stored out at sea. Right now, OPEC pegs that number at nearly 1.40 billion barrels. That's up from 1.20 billion barrels reported one year earlier. On the other hand, a case could be made that when you factor in the need for governments to replenish their petroleum reserves, you do have a more bullish situation. Strategic petroleum reserves amongst OECD nations fell from 1.48 billion barrels at the end of 2021 to 1.21 billion barrels as nations released their inventories in order to reduce high energy costs at a time when inflation was prevalent. Although the oil on water is not necessarily bound to travel to OECD nations, adding that data up against the strategic petroleum reserve inventories and the OECD commercial inventories would imply total supplies in storage that are roughly flat relative to what they were one year earlier.

{kind=link}

The picture tilts bullish

What we have here is quite a quandary. On the one hand, you have the EIA data that suggests that we could be faced with a glut the likes of which should cause energy prices to plunge from where they are today. On the other hand, you have data provided by OPEC that suggests that the exact opposite is likely to transpire. To sort out whether we should be bullish or bearish in this environment, there are some other pieces of data that we should take into consideration. First and foremost is that, in the event that the OPEC data is correct, prices will certainly rise from here, even if the group elects to raise production some. In the event that the EIA data is accurate, however, it is an open-ended question as to whether they will cut output to keep prices elevated or let a repeat of what occurred around 2014 and beyond occur.

{kind=link}

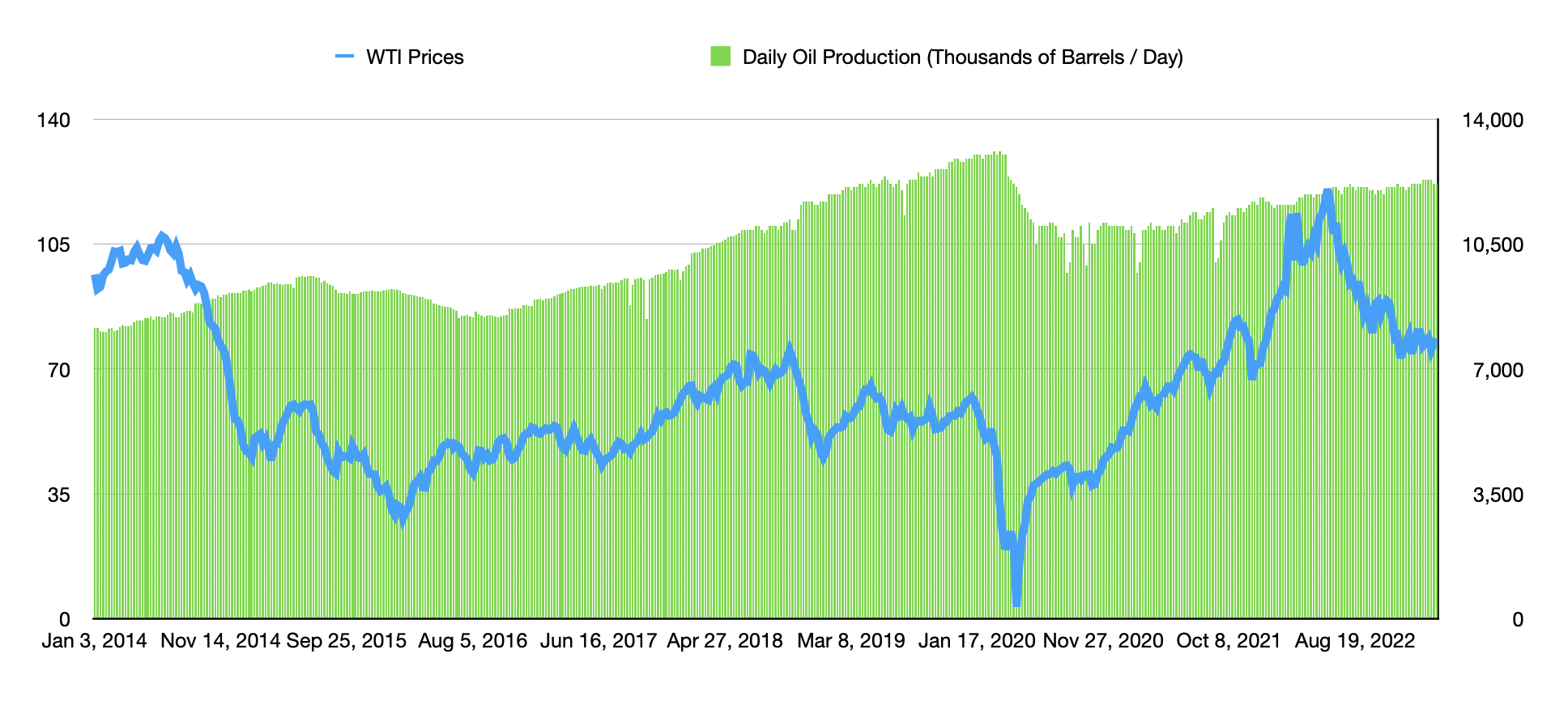

It's important to put in context exactly what market conditions were like back then. At the time, US production was rising materially and was at a real risk of causing further long-term pain for OPEC. In essence, the group decided to wage a war against American production in the hopes of crippling it in the long run. This took far longer than and was much more painful than expected. But at the end of the day, US production did fall. As you can see in the chart above, production did eventually fall, but only temporarily. It wasn't until the COVID-19 pandemic that production really took a deep plunge. Even so, that modest decline in output resulted in years of low prices for oil. If you look at the present day, however, we do still see output rising, but the move higher has been much less pronounced than it was in prior years. A lot of this can be chalked up to the drilling activity that's taking place in the US.

{kind=link}

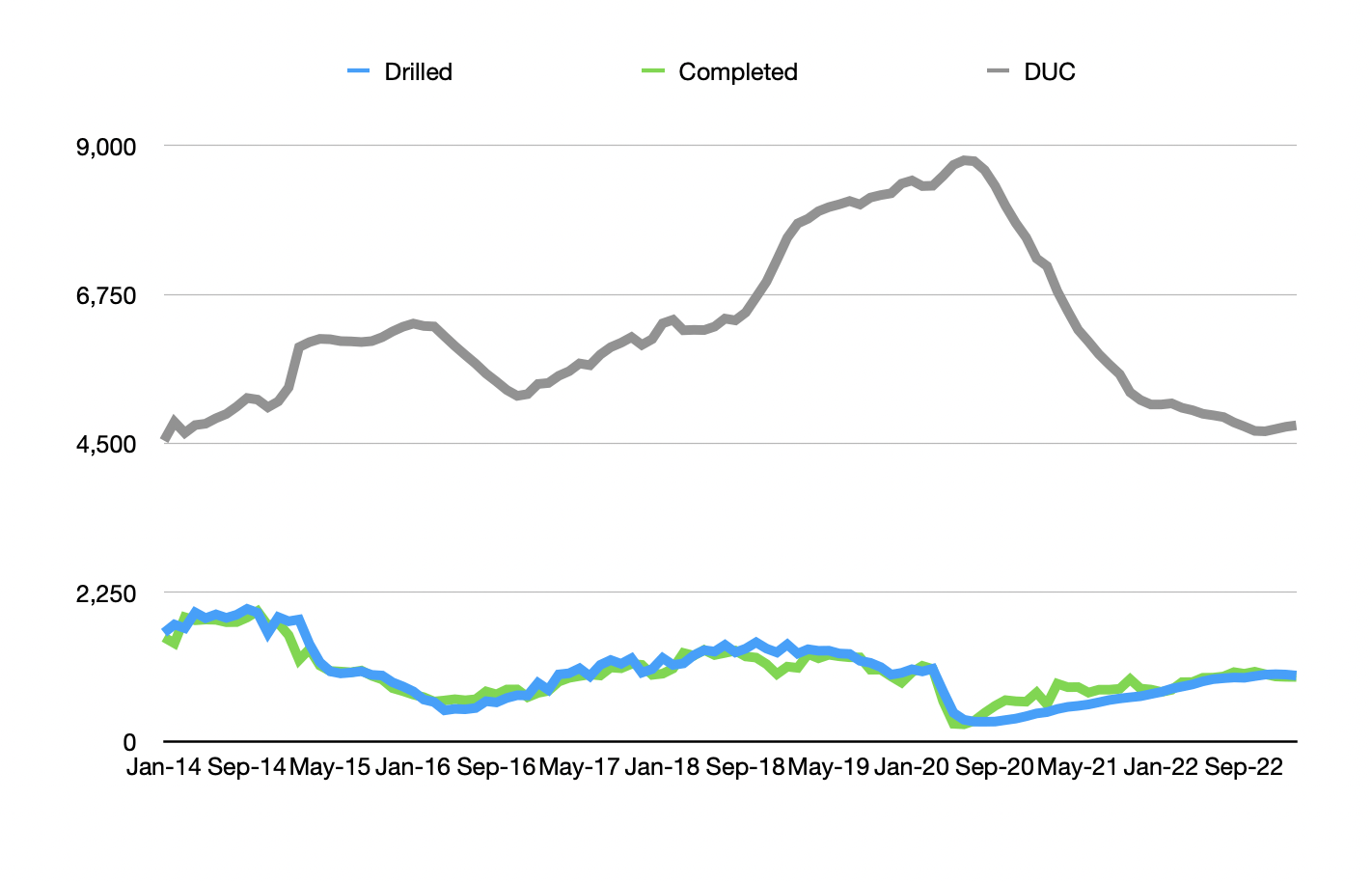

As the chart above illustrates, there also is not the number of wells being drilled that existed back then. We could pick really any month. But if we pick January of 2014, as an example, the major regions covered by the EIA reported 1,638 wells drilled and 1,569 completed. The total number of DUC (drilled but uncompleted) wells came out to 4,542. Fast forward to January of this year, and these numbers are 1,007, 972, and 4,752, respectively. Although the amount of DUC wells is slightly higher, overall drilling activity is undeniably lower. In addition to that, it's important to note that, as time progressed, the number of DUC wells grew, eventually hitting a high of 8,778 by June of 2020 in response to the number of drilled wells far exceeding the number of those completed. The decline since then was in response to the pace of completions surpassing the pace of wells that were drilled. Although energy prices remain elevated and that could, in theory, make drilling more attractive, higher interest rates will make this less appealing than it otherwise would be, and the pace of drilling is still significantly lower than what fueled the last rise of inventories. This means that we have a structural issue where relatively low drilling levels mean that OPEC is less likely to view US production levels as a threat at this time. So in the event that the EIA data turns out to be accurate, it would be more likely that they would be willing to cut production to keep prices elevated as opposed to engaging in another lengthy and costly price war.

Takeaway

At this point in time, it seems clear to me that there is a lot of uncertainty in the energy space. The recent downturn was largely driven by concerns regarding the banking crises. But as that shows signs of improving, prices are starting to move back up. As for the long run, it remains to be seen what will happen with energy prices. Data provided by the two primary authorities on the matter is split between how healthy inventories are. The way I see it though, prices should move higher if OPEC's data turns out to be accurate. And in the event that the EIA data is correct, the environment in which a glut might occur today is different than what it was the last time we had this concern. Because of this, OPEC would be more willing, I believe, to prioritize keeping prices elevated over waging a price war. When weighing these different scenarios and their likelihoods together, I view this as bullish for the global oil market.

For further details see:

Oil Prices Are Likely To Rise From Here