BKR - Oil States International: The Improvement Continues

Summary

- Oil States had a solid Q4 and provided positive guidance for 2023.

- The oilfield services recovery continues, especially in the international and offshore markets.

- The crash in U.S. natural gas prices reflected negatively on some onshore services providers, but Oil States' management doesn't appear hugely concerned.

- I expect Oil States' revenue and profits to continue on their upward trajectory.

Investment thesis

Oil States International, Inc. ( OIS ) reported solid Q4 earnings and provided upbeat guidance for 2023. The demand for the company's products and services remains robust, especially in international and offshore markets. Management expects revenue to grow 15% in 2023 on the back of 25% growth in 2022. EBITDA and cash flow are also continuing to improve towards their pre-COVID levels.

While the stock price is up 43% since my prior article, I remain bullish and still see $14-$15 as a medium term target. OIS is also 15% down from its 52-week high of $10.44 on February 17th, and in the last week the stock has hovered around $9. We will have to wait and see if this is a new support level, but, in any case, initiating a position now would be buying after a decent pullback.

Background

This article should be seen as update of my prior coverage where I outlined my fundamental case for Oil States International. In summary, OIS checks all three components of my macro thesis for 2023:

- A shift in pricing power from upstream operators to services providers;

- Smaller cap valuations catching up with larger caps;

- Offshore markets driving most incremental activity.

I also explained in my prior article why I think OIS tends to lag behind other services providers ( OIH ), as was the case in the multiyear bull market for oilfield services that ended in 2014. Ultimately, though, Oil States outperformed Schlumberger ( SLB ) last time:

Earnings and guidance recap

The highlights from the earnings include:

- Q4 revenue of $202.4 million up 7% QoQ and 25% YoY;

- Positive net income of $0.05 per diluted share;

- Adjusted EBITDA, excluding a non-recurring litigation-related benefit in Q3, up 30% sequentially;

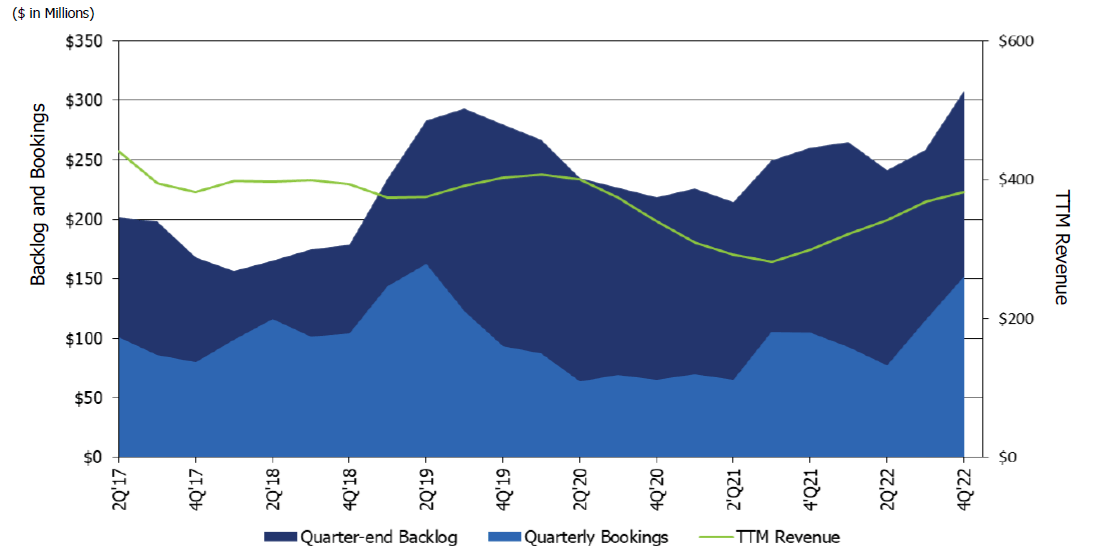

- The Offshore/Manufactured Products segment's backlog increased 19% QoQ to $308 million, which is apparently the highest level since 2015;

- The company announced a $25.0 million stock repurchase plan; this is not immaterial and right now represents about 4% of the market cap.

The book-to-bill ratio for the largest and most important Offshore/Manufactured Products segment is now 1.5x, reflecting significant additions to the backlog:

Oil States Investor Presentation

{kind=link}

Revenue is trending back to pre-COVID levels:

EBITDA margin is moving up above 10% though still below the 20s seen prior to 2014:

Management commented on the rise of deepwater long-term projects that are less cyclical:

Crude oil and natural gas prices corrected to the downside from the highs reached in early summer 2022 due to ongoing recession concerns, tightening global monetary policies and the associated impact on commodity band.

However, despite these factors, WTI and Brent crude oil spot prices remain above $76 per barrel and $83 per barrel, respectively, with natural gas, currently trading at approximately $2.30 per MMBtu. These prices while lower than the average commodity prices realized in 2022 are likely to support demand increases in 2023.

Initially, the industry responded to higher commodity prices with accelerated shorter cycle investments in the United States, which we experienced in 2022 . We now expect to see investments pickup for long lead time projects as well, including those in international markets and deepwater basins around the world.

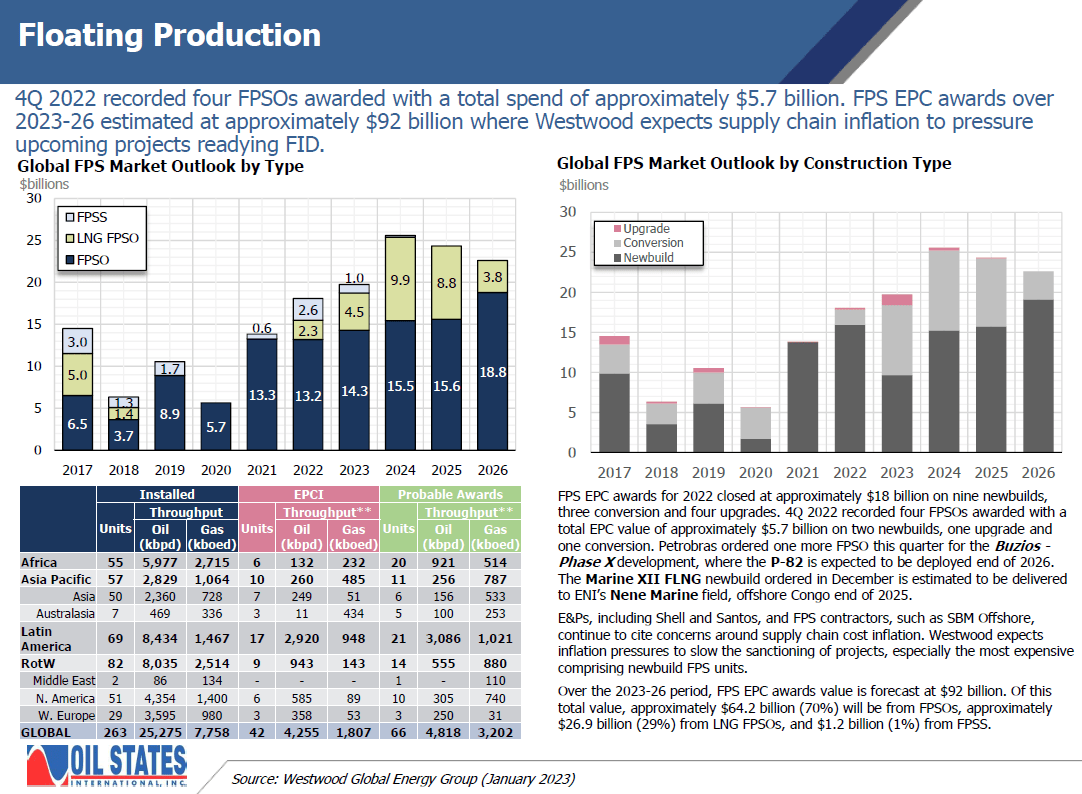

FPSO spend, which is big demand driver for Oil States' largest segment, continues to look promising:

Oil States Investor Presentation

{kind=link}

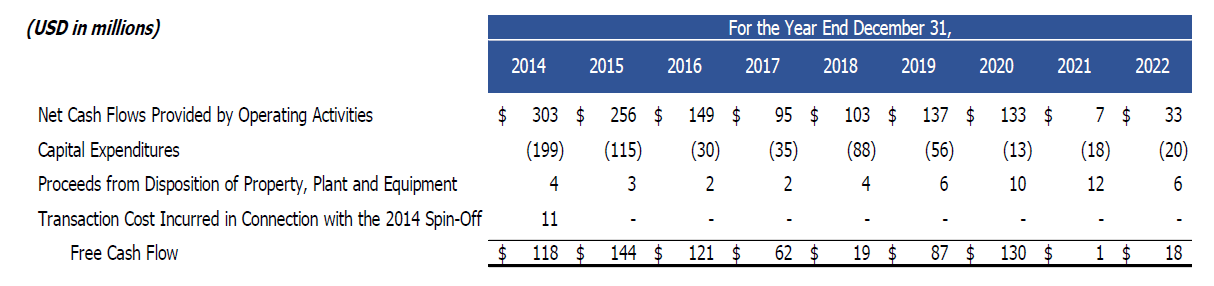

OIS' cash flow generation capability is also more robust to cycles than what is typically assumed of its industry:

Oil States Investor Presentation

{kind=link}

Even in 2020-2021, the company was cash positive.

Management announced its expectations for 2023:

We project that our annual revenues will grow about 15% on a consolidated year-over-year basis, with EBITDA ranging from $92 million to $100 million.

That would put 2023 revenue at about $850 million, so it would take another year of 15% growth to get to my $1 billion target. Management also seems to be guiding to 10% EBITDA margin; based on where things were pre-COVID and in the prior bull cycle, I would expect to see a minimum of 15% EBITDA margin in 1-2 years.

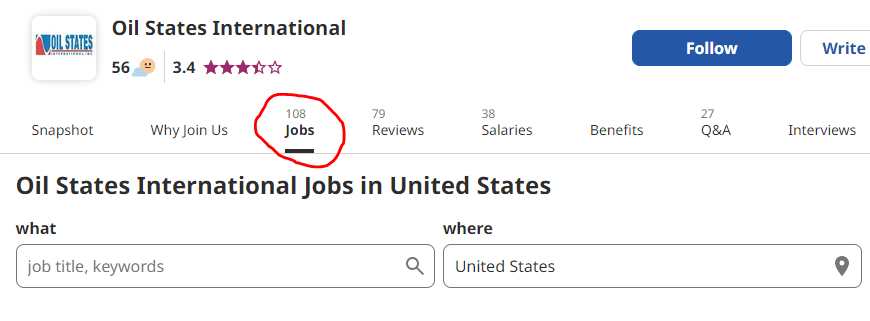

The company is hiring too

As of December 31, 2022, OIS had about 2,700 employees:

{kind=link}

A quick Indeed.com search shows 108 Oil States job postings in the US only:

{kind=link}

This is 4% of the current workforce, and I think is also bullish.

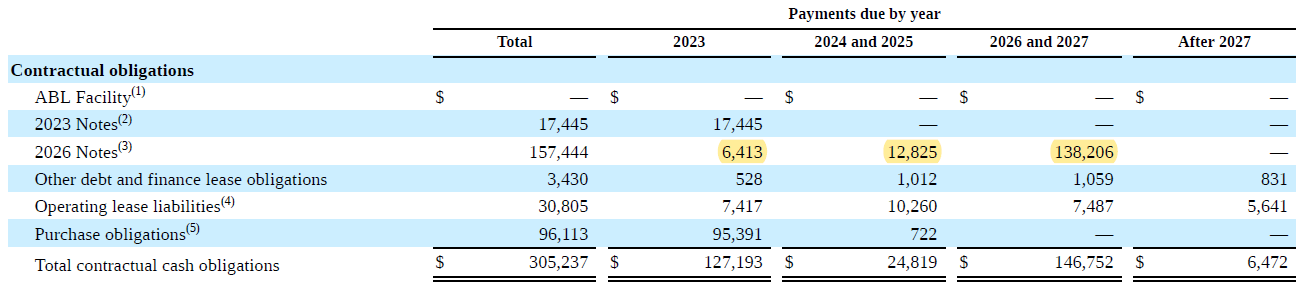

The debt is manageable

Management also commented on the progress of their debt reduction efforts:

At December 31, our net debt totaled $111 million, yielding a net debt to total capitalization ratio of 14%. On a leverage ratio basis, net debt to adjusted consolidated EBITDA has been materially reduced to 1.4 times.

The significant maturities aren't until 2026 either:

{kind=link}

Moreover, the 2026 Notes carry a fixed rate of 4.75% as result of a well-timed refinancing in 2021. This rate will soon be lower than the Fed rate.

The natural gas crash

I feel that many services providers, especially the onshore focused ones, have been penalized in the last few weeks by the crash in natural gas prices:

That may be a valid concern for some companies, but it doesn't affect OIS as much. Here is how the CEO responded to a related question during the earnings call:

Kurt Hallead, analyst

But I am just kind of curious, and then, as you kind of look at the dynamics at play, the confidence you have obviously oil basins holding up better than natural gas, but is there something specific to your customer base that will maybe shield you a bit from potential decline in gas activity , that's question number one. Question number two then is you typically get some churn in assets or business and there's going to be decline in natural gas activity, there's going to be a movement to these oil basins, which historically it's kind of created some asset on asset competition and some pricing pressure . So just wanted to get your perspective on how you are shielded and how -- if you think there's going to be asset on asset competition like we have seen in prior cycles.

Cindy Taylor, CEO

No. Those all are very valid and timely questions, Kurt. But, obviously, we are very attuned to our customers and to market concerns and the impact of pricing, which we all know very well. And so, I am going to echo some of what is on the street in saying that I think that, one given the growth in the rig count in the Haynesville in 2022 has set up power production in that basin, number one. It has a higher breakeven at least from all the research I have done than the Northeast market.

And so I do think that basin is more sensitive to activity declines, that's number one . There are plenty of analysts out there estimating what kind of decline we might be looking at. But with this massive switch over the last 15 years or so, but rig count dedicated to oil basins, the overall gas count is probably percentage wise about 20%.

And I do think that the weakness will see is likely in the Haynesville, a lot people are speculating maybe 20 rigs to 30 rigs off of a basis 73 rigs operating in that market. So that's not a huge impact on total rig count .

I do think that the Northeast holds up better and it's a narrow customer base up there that we know well and typically our work there is highly complex multi-well pads. I really don't see a significant change in that Northeast market as it relates to our operations.

The next part of your question is, if in fact you do lose some 20 rigs or 30 rigs in the Haynesville, does that create downward price pressure in other basins. And I will just be honest, for the type of equipment that we have, we don't believe that is the case .

And I will also say, our equipment it's been a bit different. We haven't been pushing 90% utilization and pressing day rates materially in 2022, unlike maybe other product offerings where the equipment has been tighter.

And for that reason you may have some market shifts, but you may also just have an improvement in certain other basins offset by some weakness in the Haynesville. But in totality, particularly with our international and our Gulf of Mexico exposure, I am not going to say, I am totally sanguine about it, but I am not heavily concerned either .

Valuation considerations

My valuation estimates haven't really changed from my prior coverage. Longer term, I would expect to see $1 billion revenue / $150 million EBITDA / 10x EV to EBITDA ratio. Doing the math, that comes to about $21 per share, consistent with where the stock was back in 2018, in a weaker environment for the sector.

In the shorter to medium term, I think it is reasonable to expect a 10x EV multiple on 2023 EBITDA, similar to where Baker ( BKR ) and NOV ( NOV ) trade now. This scenario would be consistent with $13-$14 share price. A 10x multiple may appear generous for the sector, but we are also growing now at 15-20% annually and still only at the early stages of the upcycle.

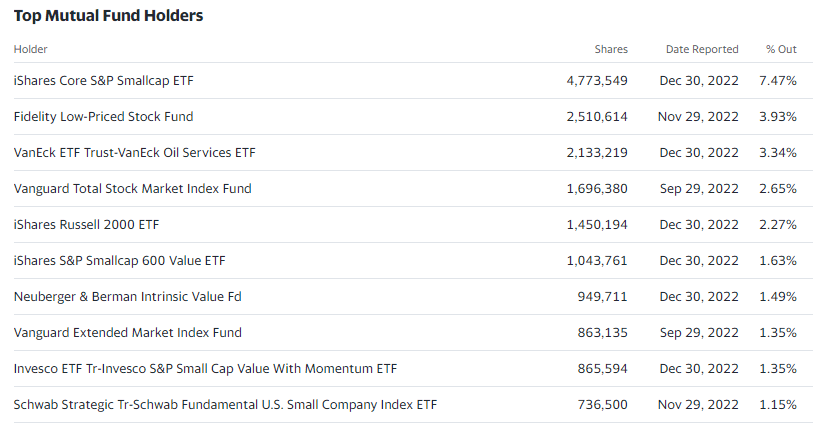

Ownership effects

Oil States doesn't have significant short interest, but much of stock is owned by passive ETFs:

{kind=link}

This may drive additional volatility and lead to situations like last October when the stock was less than $4.

Commenting on the buybacks, the CEO Cindy Taylor said:

So kind of early part, probably not going to see a lot of share repurchases, even last year the bulk of our free cash flow was generated in the second half of the year. I see the same trend occurring in this year and so I think it's important to have authorization in place.

We do want to be opportunistic, and as recently as four months ago, our stock was depressed for reasons unknown and it's done better over the last 90 days, I will call it. But I just think we are going to be thoughtful and smart and absolute given is that smart organic investments will always be first.

The $25 million of buybacks may end up punching above their weight if we see continued volatility and pricing anomalies like last October.

Conclusion

Oil States is a small oilfield services company that is making nice progress towards its pre-COVID revenue and profitability levels. The company's exposure to international and offshore markets also helps it capitalize on the macro trends in the energy space that I believe are unfolding.

Except for the volatility discussed above, I am not finding many other negatives. Yes, a recession would be bad for sure. However, it would hurt more oilfield services providers with exposure to short-cycle barrels. I don't think many long-cycle projects will get canceled even if we have a repeat of the 2008 GFC. Oil supply has now also become a national security matter, and much of the international drive is from NOCs that can afford to take a longer term view.

For further details see:

Oil States International: The Improvement Continues