XOM - ONEOK's Premium May Be Justified By Growth

2024-01-15 03:10:01 ET

Summary

- ONEOK is positioned for a strong close to FY23 and beyond, with the acquisition of Magellan Midstream Partners providing optionality and the ability to bundle production on multiple pipeline systems.

- ONEOK will double their NGL transport capacity in the Permian Basin as they complete the loop by Q1'25.

- The Magellan acquisition strengthens ONEOK's position in the Permian Basin and allows for bundling of hydrocarbons, potentially driving more capacity and generating profit-driving synergies.

ONEOK ( OKE ) is set up to report a strong FY23, positioning themselves for a strong FY24 and beyond. With the acquisition of Magellan Midstream Partners, ONEOK now provides customers optionality and the ability to bundle production on their multiple pipeline systems, whether it is natural gas, NGLs, refined products, or crude oil. With a target leverage ratio of 3.5x net debt/EBITDA in 2024 along with management’s targeted aEBITDA of $6b and robust dividend yield of 5.45%, I provide OKE shares a BUY recommendation with a price target of $76.32.

Operations

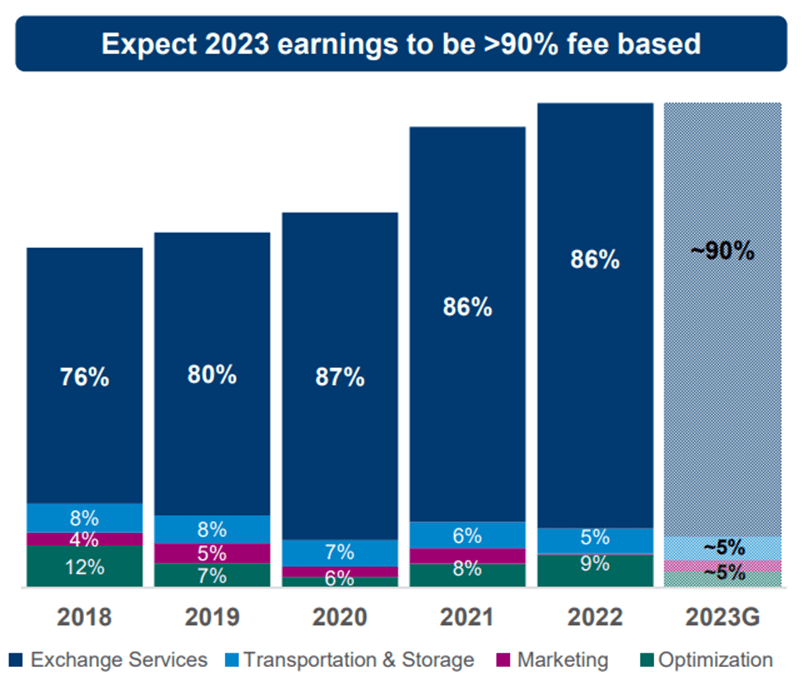

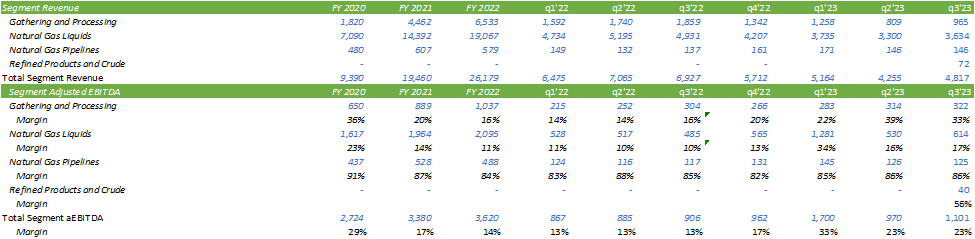

ONEOK experienced stronger volumes across their system in q3’23 with NGL volumes up 11% and gas processing up 12% from the previous year and expects over 90% of earnings being fee-based for FY23. The firm also connected 450 wells in the first 9 months of 2023, an 80% increase from the previous year, and expects to connect between 525-575 for FY23.

{kind=link}

ONEOK has fully subscribed to their additional 4Bcf of existing storage capacity in Oklahoma through 2027 and 90% through 2029. The firm also expects to complete the looping of the West Texas NGL pipeline by q1’25, which will double the NGL capacity out of the Permian Basin. When asked about overbuilds during their Wells Fargo fireside chat on December 5 th , 2023, management suggested that they have roughly 100 miles of pipe remaining as compared to 300 miles by their competitors.

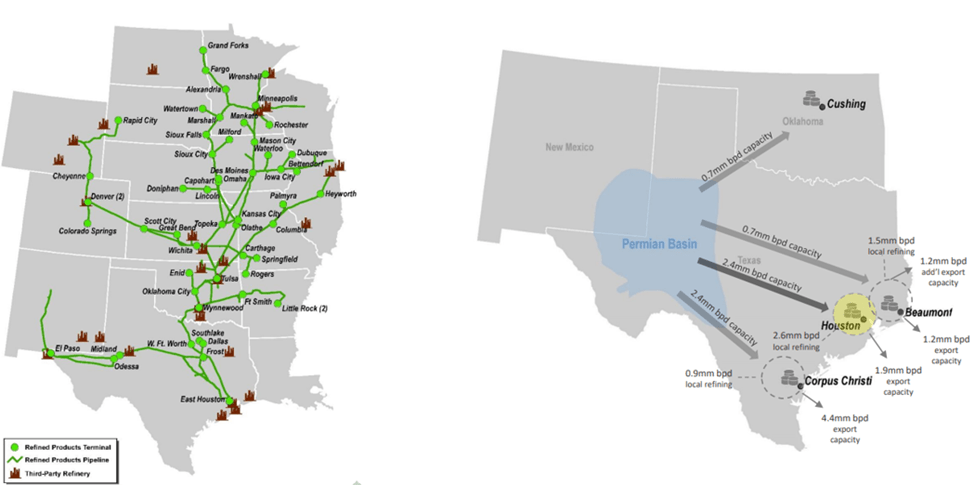

Looking at the Magellan acquisition, I believe this acquisition strengthened ONEOK’s position in the Permian Basin by allowing the firm to diversify their capabilities to their customers, making ONEOK the one-stop-shop for midstream services. Magellan brought a combined 6.2MMbbl/d of capacity out of the Permian Basin, with 2.4MMbbl/d going to both Houston and Corpus Christi and 700Mbbl/d going to both Beaumont and Cushing. In addition to their pipeline system in the Permian Basin, Magellan’s assets include refined products and crude oil pipelines and terminals throughout the DJ Basin, Powder River Basin, all the way up to the Bakken Formation in North Dakota, most of which is fee-based.

{kind=link}

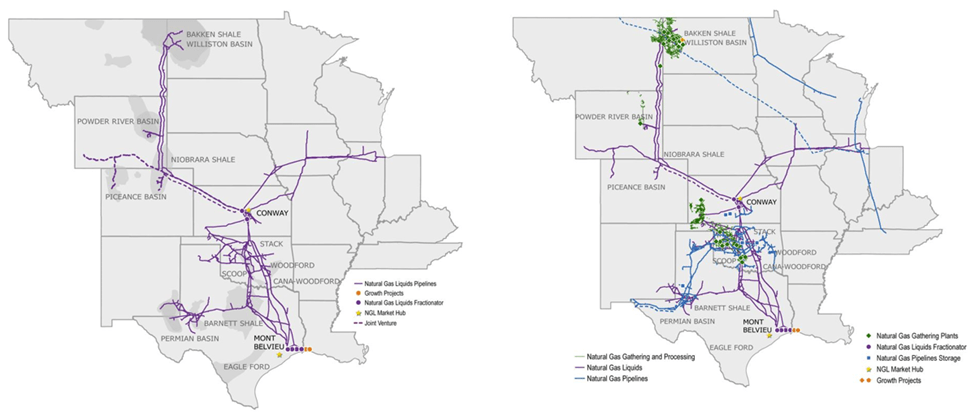

Magellan’s assets align well with ONEOK’s natural gas and NGL pipelines and G&P facilities in which the firm can bundle all hydrocarbons into one contract at an appealing fee, potentially driving more capacity.

{kind=link}

In total, management anticipates $200-415mm in total synergies with $100-315mm in commercial bundling/blending synergies. Though this will not be an all-at-once occurrence, management expects that as midstream contracts roll over, they will be able to renegotiate this bundled service.

Management is also optimistic relating to industry consolidation on the producers’ side. With Occidental ( OXY ) acquiring CrownRock with primary assets in the Permian, Exxon ( XOM ) acquiring Pioneer Natural Resources ( PXD ) with primary assets in the Permian, and Chevron ( CVX ) acquiring Hess ( HES ) with primary domestic assets in North Dakota in the Bakken Shale, there may be further opportunities to bundle more volumes with fewer producers across the different basins. Exxon alone anticipates to expand Permian production to 2MMbbl/d by 2027. Oxy’s acquisition added 170Mboe /d of volumes in the Permian Basin for 2024 production with q4’23 guidance of 571-591Mboe/d. The firm also guided production in the Rockies of 263-269Mboe/d. Chevron produced 750Mboe/d in the Midland & Delaware Basin in the Permian and anticipates in-basin growth in 2024. Devon Energy ( DVN ) produces 440Mboe/d in the Delaware Basin and expects to maintain this level of production through q4’23. With ONEOK’s operations connecting the basin to Cushing and Houston, I believe the firm is well-positioned through their current assets, acquired assets, and growth capital investment to service future production needs.

{kind=link}

ONEOK is in the process of expanding their capacity in the Permian to 740Mbbl/d as they complete the remaining loop of the West Texas NGL Pipeline that will connect to their Arbuckle II pipeline, coming online in q1’25. In addition to this expansion, the firm has outlined an additional 125Mbbl/d NGL fractionation facility in Mont Belvieu with operations commencing in q1’25. These two projects come out to be $1.7b in growth capital.

Financials

{kind=link}

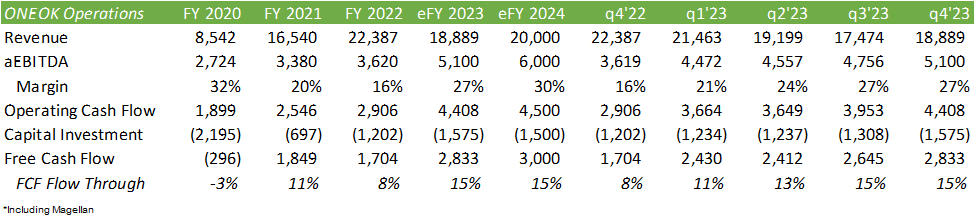

ONEOK generated $1,101mm in aEBITDA for q3’23 for a TTM figure of $4,756mm with a margin of 27%. Management anticipates aEBITDA to come in at $5.1b inclusive of the Magellan acquisition with legacy ONEOK being $4.8b. Assuming similar margins, ONEOK should generate $18,889mm for FY23 with 2,833mm in free cash flow.

{kind=link}

Valuation & Shareholder Value

{kind=link}

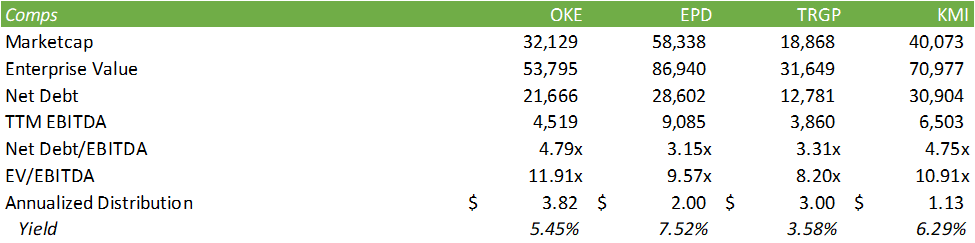

ONEOK currently trades at a relative premium when compared to its peers. Given the growth outlook for the firm and their forecasted aEBITDA for 2024, this premium may be justified.

{kind=link}

Projecting out EBITDA to 2024 and using the average multiple of this cohort of 9.56x, we can value OKE shares at $73.11. I believe ONEOK is in a strong position where it stands. As management has guided, the firm is expected to reduce their leverage ratio to 3.5x in the next year through cash generation. With the assumption of reaching that 3.5x leverage ratio and still using the 9.56x multiple, we can value OKE shares at $76.32. Given this and their 5.45% dividend yield, I provide OKE shares a BUY recommendation.

{kind=link}

For further details see:

ONEOK's Premium May Be Justified By Growth