COM - OPEC+ Cuts Irrelevant: Oil Still A Short

Summary

- An update on my oil short thesis published on August 15, 2022.

- Oil continues to trade at a premium.

- U.S. supply continues to rise.

- Global recession risk is higher than ever.

- OPEC+'s cuts are completely overblown.

On August 15, 2022, I published a report on Seeking Alpha titled Why Oil Is A Broken Market Ripe For A Short . A lot has changed since, with Crude Oil Futures ( CL1:COM ) jumping between a high of $97.51 and a low of $70.08. Therefore, I believe an update is in order.

This update will be broken down into five points plus a conclusion:

- Oil continues to trade at a premium

- U.S. supply continues to rise

- Global recession risk is higher than ever

- OPEC+'s cuts are completely overblown

- The Chevron ( CVX )/Venezuela deal is likely just the start

- Conclusion

A reminder:

I first took action on this belief on March 15, 2022, when I initiated a short position in WTI crude using WisdomTree WTI Oil 3x Short Daily ETP in USD (ticker:3OIS) through a margin product. I don't usually disclose my position in such detail, but I believe such a controversial issue must be read with disclosures in mind.

CL1:COM is a crude oil futures contract. Investors without access to the futures market may consider bearish crude ETFS. NOTE that leveraged ETFs (like 3OIS) are expected to suffer from price erosion over time and are usually only recommended as short-term investment options. For more information on the unique and challenging risks facing leveraged ETFs please see FINRA's article The Lowdown on Leveraged and Inverse Exchange-Traded Products.

Additionally, this article will focus on WTI crude prices, and any reference to oil price uses the price of crude.

Oil continues to trade at a premium

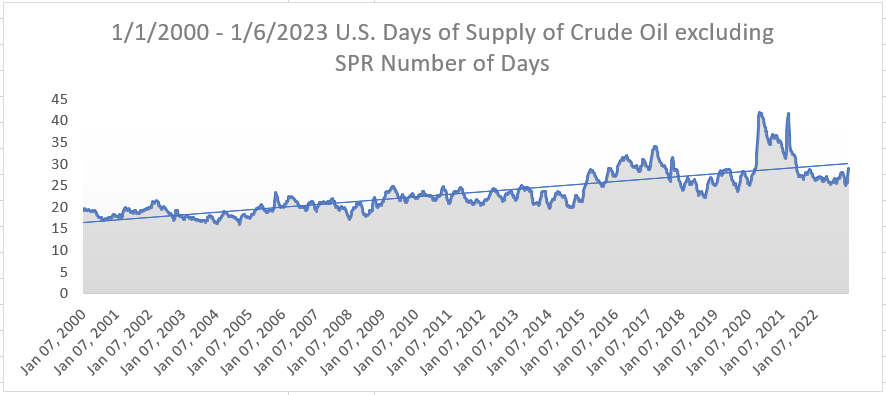

In my previous report, I discussed the misconception that oil is trading at fair value or is even undervalued. One point brought up in the comments was that stockpile levels are down. Unfortunately, this is not only false, but the trend has been the opposite. Excluding the United States (U.S.) Strategic Petroleum Reserve ((SPR)), U.S. stockpiles based on days of supply have been increasing for quite some time. I would go so far as to say the trend shows a consistent and rapid rise in days of supply. Just take a look at the below table and chart; as of January 6, 2023, the number of days reached 29.

Created by Russell Katz (1.) (Data collected from U.S. EIA)

{kind=link}

Created by Russell Katz (1.) (Data collected from U.S. EIA)

The price of oil is primarily based on three factors, current/future supply, the current stockpile, and current/future demand. Despite changes in the global environment, the U.S. SPR and international oil supply levels indicate oil is still priced at a significant premium.

As in my last report, data is gathered from the U.S. Energy Information Administration's ((EIA)) weekly This Week in Petroleum publication. The market always pays close attention to U.S. stockpile numbers, which affect price movements. However, if we take a more comprehensive look at days of supply historically, we find that oil is trading above the historical median based on current stockpiles. For reference, I used the median of the four crude oil futures contracts included in the weekly report for price.

Created by Russell Katz (1.) (Data collected from U.S. EIA)

While the numbers have gotten slightly better since my first report, they still show that at $80 a barrel, oil is trading a premium when compared to its historical fundamentals. Based on the risks discussed below, I believe oil currently deserves to trade at a discount.

U.S. supply continues to rise

On October 10, 2022, Jamie Dimon, CEO of JPMorgan ( JPM ) said to CNBC :

Obviously, America has to have some real leadership — America is the swing producer, not Saudi Arabia.

He's absolutely right, and while the U.S. has been slow to increase production after the COVID-19 slump, production has been trending upward at an increasing rate as shown in the below graphs:

Compared to my August 15, 2022 report, U.S. crude oil field production increased 608 bps to -4.1% off its high. There was a slight dip in production recovery, but this was due to the effects of Hurricane Ida and other temporary issues. This is further proven when you look at the latest U.S. oil rig count, which has increased 293 bps to -9.52% off its high from my August report; as shown below:

As I predicted in my previous report, U.S. oil drilling CAPEX has been increasing and will likely continue along this trend. This additional investment has led to continued growth in the number of active oil rig count in the U.S. since my report, and I believe with the political winds shifting towards encouraging drilling, at least in the short-mid term, this trend will continue, and U.S. supply is along for the ride, with a slight delay.

Global recession risk is higher than ever

While still not as certain as death and taxes, the risk of a worldwide recession in 2023 continues to grow. My base case predicts a sizable, but not a GFC-level global recession will occur by the end of 2023. My best case assumes a light global recession.

But just like my previous report, don't take my word for it; let's see what the experts say. We will review the recession risk of the United Kingdom ((UK)), European Union ((EU)), U.S., and China.

United Kingdom's recession risk

Starting with the UK, the Bank of England (BoE) raised interest rates by 50 bps in December 2022 as inflation remains difficult, declining only very slightly to 10.7% in November. The BoE won't be hitting its 2% annual target anytime soon.

However, the bank has offered some comfort, forecasting a gradual fall in inflation during the first quarter of 2023. One of the key reasons mentioned was the expected removal of energy price spikes. However, the political situation in the UK remains volatile, and many of the country's problems have no easy solution in sight, especially without the backing of the EU.

A key example of the unique problems facing the UK is its logistics crisis. Like many countries, the primary issue facing the UK is a pure shortage of truck drivers. Where the UK's problems become unique is the scale of the deficit. According to a survey by the Chartered Institute of Logistics and Transport (CILTUK), 64% of operators suffer from driver shortages. In the North East, Yorkshire & Humber, East of England and Scotland, the shortages have more than doubled since 2015. The situation is unlikely to be resolved, as the skilled workers that filled these positions mostly left due to BREXIT , and no amount of special visas has been so far successful in coaxing them back.

So when does the BoE expect the UK to enter a recession? According to commentary published with the September rate hike, the BoE believes the UK might already be in one. Labor data published in December showed an increase in unemployment and wage growth, combined with high levels of economic inactivity and long-term illness. As a result, the BoE now expects the UK's GDP to contract 0.1% during the fourth quarter of 2022.

European Union's recession risk

Jumping across the channel to the EU, we see a deteriorating situation, but one far better than in the UK. My last report quoted the European Central Bank's (ECB) July 2022 report as citing:

Risks to the forecast for economic activity and inflation are heavily dependent on the evolution of the war and in particular its implications for gas supply to Europe. New increases of gas prices could further drive up inflation and stifle growth.

I pointed out that gas futures had rallied hard since the forecast and were expected to continue along this trend.

{kind=link}

Screenshot taken 26-10-2022 (ICE Endex)

{kind=link}

Screenshot taken 26-10-2022 (ICE Endex)

While prices did rally well above 300 before the end of August, the situation changed at the end of the month. A combination of full storage, lower demand, and mild weather saw prices fall over 70% from their end-of-August highs. So yes, I was partially wrong here, but I would argue the damage had already been done.

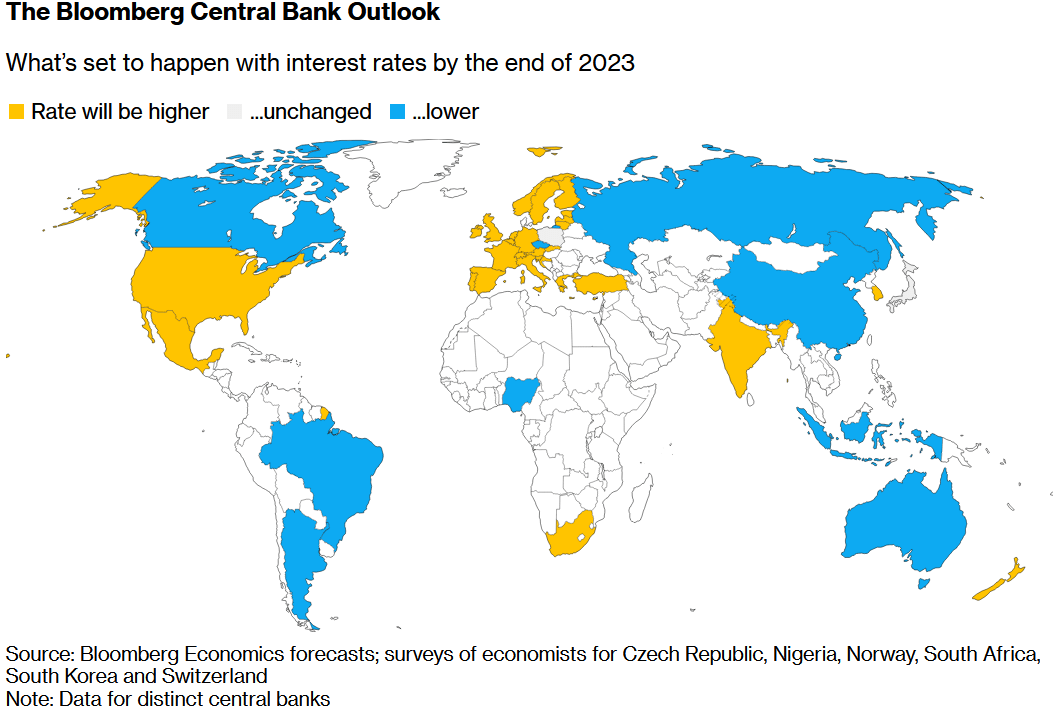

Inflation hit 10% in September 2022, largely due to energy prices rising 40.8% year-over-year. Food, alcohol, and tobacco also remained an issue, increasing 11.8% year-over-year. On the back of the continuing inflation problem, the ECB has become increasingly hawkish, leading many economists to believe a pullback in interest rate hikes to prevent a recession is unlikely. At least according to Bloomberg's Central Bank Outlook for 2023 , published January 9, 2023:

{kind=link}

The Bloomberg Central Bank Outlook for Global Rates 2023 (Bloomberg Economics)

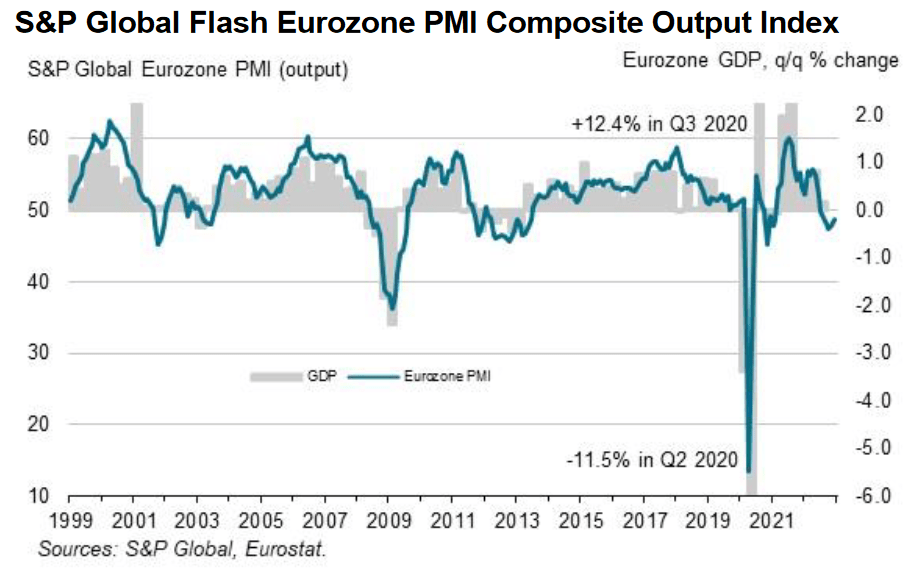

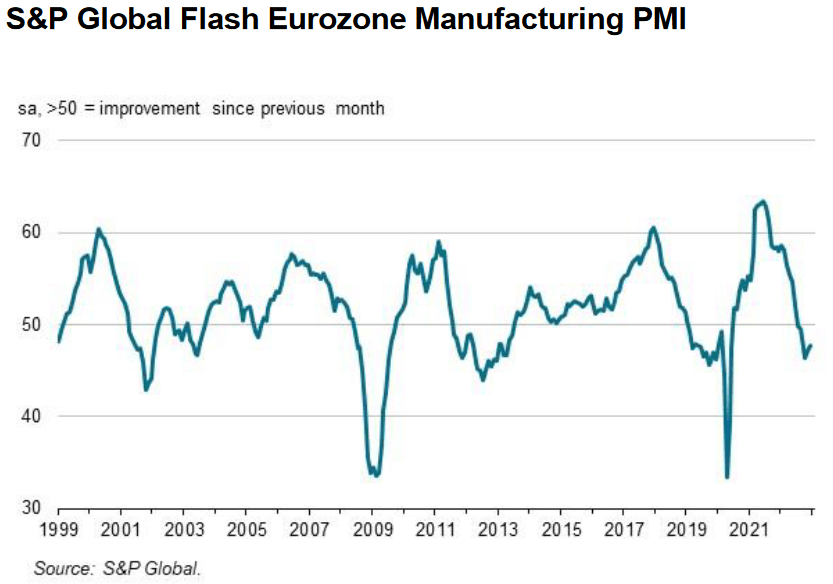

This new attitude among economists is rather telling, especially as S&P Global's Flash Eurozone PMI Composite Output Index and Manufacturing PMI Index have been mostly on a downward trend since they broke 50 in July. For those unaware, a PMI of 50 represents no change, below equals a contraction, and above indicates growth—the further from 50, the greater the change level. With global trade continuing to struggle, it seems unlikely that the recent small bump will be anything more than temporary.

{kind=link}

Flash Eurozone PMI Composite Output Index (S&P Global)

{kind=link}

Flash Eurozone Manufacturing PMI (S&P Global)

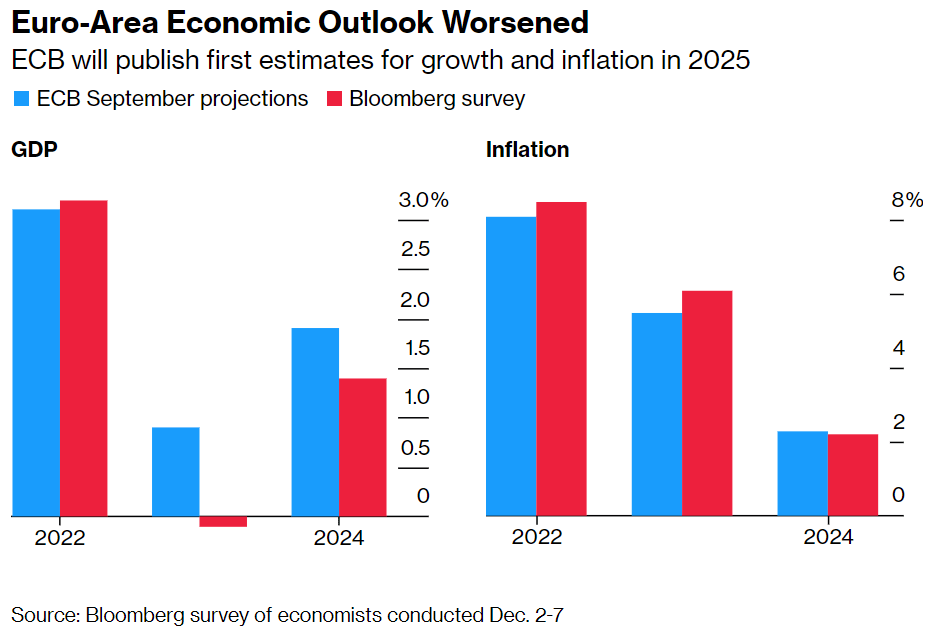

Still, the ECB has yet to move its base case forecast off subdued economic growth, but in late September, ECB President Christine Lagarde told the European Parliament that assumptions in its outlook have been “overridden by events.” I expect the ECB will soon acquiesce to the reality that a recession is the only realistic base-case scenario. Furthering my point, economics have already accepted a light one as likely in 2023 :

{kind=link}

Survey of economists conducted Dec 2-7 EU GDP and Inflation (Bloomberg)

United States' recession risk

Across the pond in the U.S., inflation is better but still worrying. In September, inflation reached 8.2% year-over-year, but most interestingly, this was primarily due to core inflation. According to CNBC, core inflation, excluding food and energy costs, grew 6.6% during September, the highest level since 1982. Still, December saw core inflation growth fall to 5.7% and headline 6.5% annually, representing a continued slowdown. And yet, excluding food and energy, core inflation grew 0.3% for the month. So inflation is likely on a downward trend, but it's extremely light and far from a certainty.

Furthering concerns of a pullback in the future, the U.S. Department of Commerce's Bureau of Economic Analysis has reported disposable personal income increased 0.4% month-over-month in November 2022.

| July |

| August |

| September |

| October |

| November |

| Disposable personal income (current USD) |

| 0.4% |

| 0.4% |

| 0.4% |

| 0.7% |

| 0.4% |

While 0.4% growth might seem fine, the notes in the report included clarification that not all is as it seems:

The $19.8 billion increase in current-dollar PCE in November reflected an increase of $79.2 billion in spending for services that was partly offset by a $59.5 billion decrease in spending for goods. Within services, the largest contributor to the increase was spending on housing.

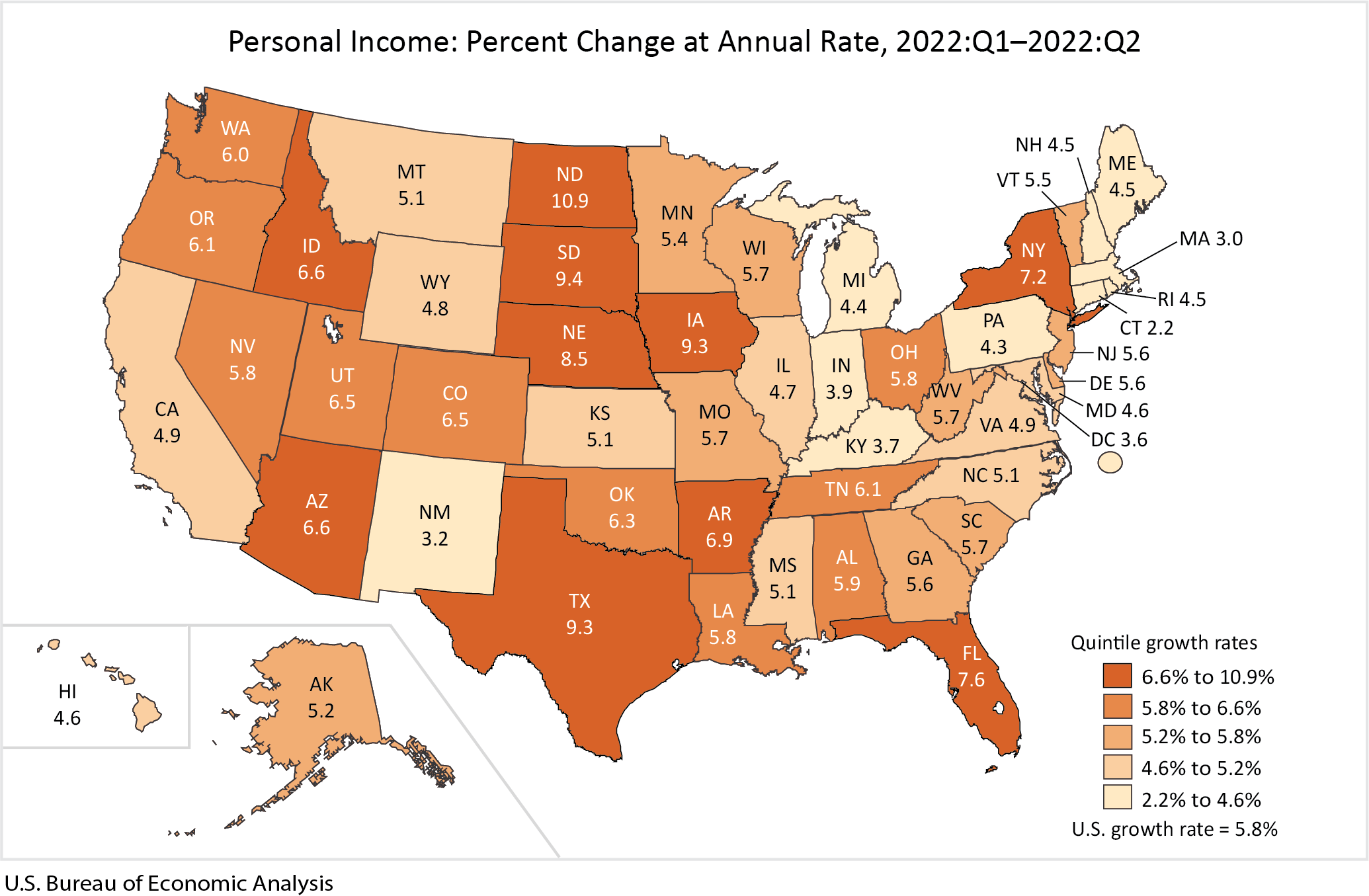

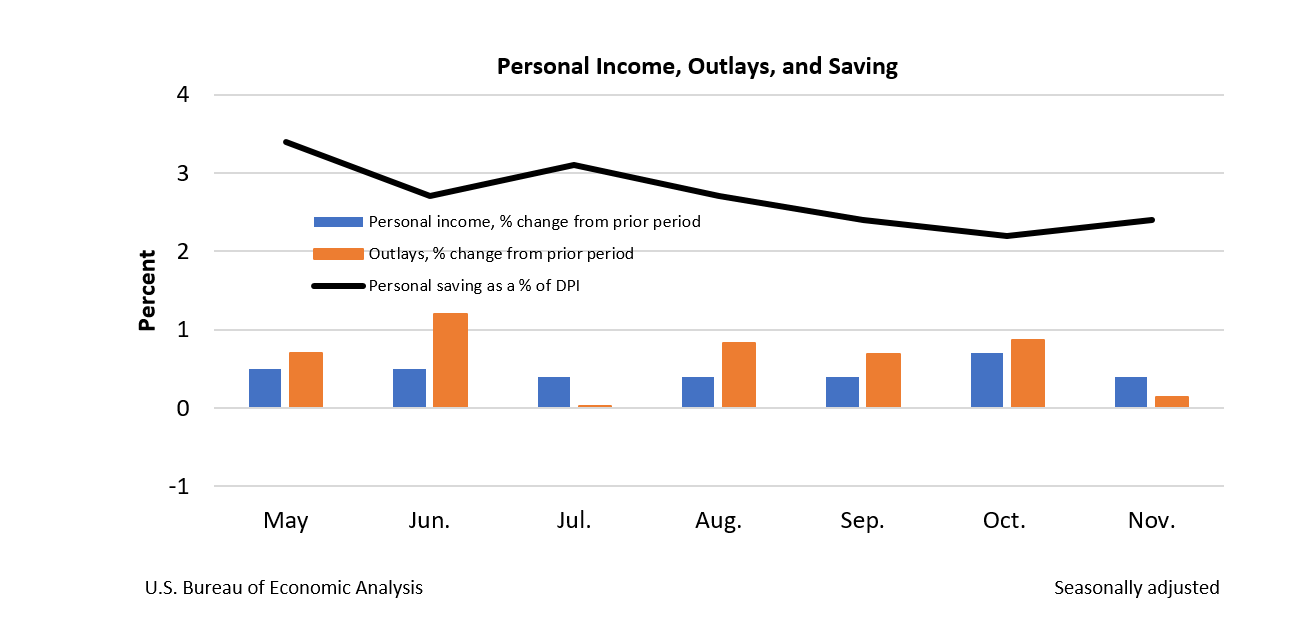

In the third quarter of 2022 , personal income grew at an average annual rate of 5.3% in the U.S.

{kind=link}

Personal Income Percent Change at Annual Rate 2022Q2 - 2022Q3 (U.S. Bureau of Economic Analysis)

This might seem like a fine result, but if we look at the data, there is a clear downward trend :

{kind=link}

Personal income outlays and savings (U.S. Bureau of Economic Analysis)

Therefore, I believe the economic situation is slowly deteriorating in the U.S., and with the U.S. Federal Reserve almost certainly committed to its hawkish policy of raising rates for the remainder of 2023, I think we will see this trend continue at an increasing pace. Remember, at the end of September , Federal Reserve Chair Jerome Powell said:

The chances of a soft landing are likely to diminish... We have got to get inflation behind us I wish there were a painless way to do that. There isn’t.

Chairman Powell even went so far as to say:

No one knows whether this process will lead to a recession or, if so, how significant that recession would be.

Economists seem to want to disagree with Chairman Powell, at least regarding whether this process will lead to a recession. Bloomberg Economics model's latest projections place a recession in the U.S. as "effectively certain" in the next 12 months. A survey by Bloomberg of 38 economists was more restrained, placing the probability of a recession over the next 12 months at 70% in December 2022, from 65% in November and 50% in September. Remember when I published my report, Vanguard reported the likelihood at 25% over the next 12 months. The odds seem to only increase with every new survey.

China's recession risk

China's economy has been rocky for a while now, with Q2 2022 's real Gross Domestic Product ((GDP)) declining at a 10% annualized rate. The situation is complicated and has many moving parts, but it can be traced to two key factors.

The first was a pre-existing condition of the Chinese economy before COVID-19, a bloated domestic credit market. Truthfully this is likely an understatement, but before we continue, it's important to note two important differences between China and the West when handling this type of crisis. First is China's court system, a topic I covered in detail in my 2018 report The Glaring Risk Coming To Crush Micron's Rally .

Chinese courts are far from impartial and rulings, especially when politics are involved, are often fraught with meddling from higher courts, local governments, and the federal government. Judges are often pressured by these groups to give rulings that favor their policies, initiatives, or goals.

In a report titled Judicial Independence in the PRC the United States Congressional-Executive Commission on China lent credence to my analysis stating:

Local governments are the most significant source of external interference in judicial decision making. Local governments often interfere in judicial decisions in order to protect local industries or litigants, or, in the case of administrative lawsuits, to shield themselves from liability.... According to one recent SPC study, over 68 percent of surveyed judges identified local protectionism as a major cause of unfairness in judicial decisions.... The Communist Party also influences judicial decisions in both direct and indirect ways. Party groups within the courts enforce Party discipline and the Party approves judicial appointments and personnel decisions.

This is important to remember, as it means China's government has tools at its disposal most Western countries do not. Specifically, the ability to ensure prosecutions are successful, especially during times of crisis. When a crisis threatens China's financial stability and trust in the government, the regime has, and I believe will, use the courts to clean house, including the use of the death penalty. A key example is Lai Xiaomin, a former top banker who was executed in January 2021 for taking US$265m in bribes. As SCMP columnist Wang Xiangwei said:

If there’s one thing that defines China’s leader Xi Jinping ’s 10-year reign, then it’s probably his signature anti-corruption campaign that he has used to consolidate power and bolster discipline and loyalty.

While this might positively impact any recovery (it's unclear until we see how it's exactly handled), I believe this type of action will compound declining business investment and confidence in the short term. Moreover, as China gets closer to a full-blown financial crisis, I believe another wave of "anti-corruption" purges will occur.

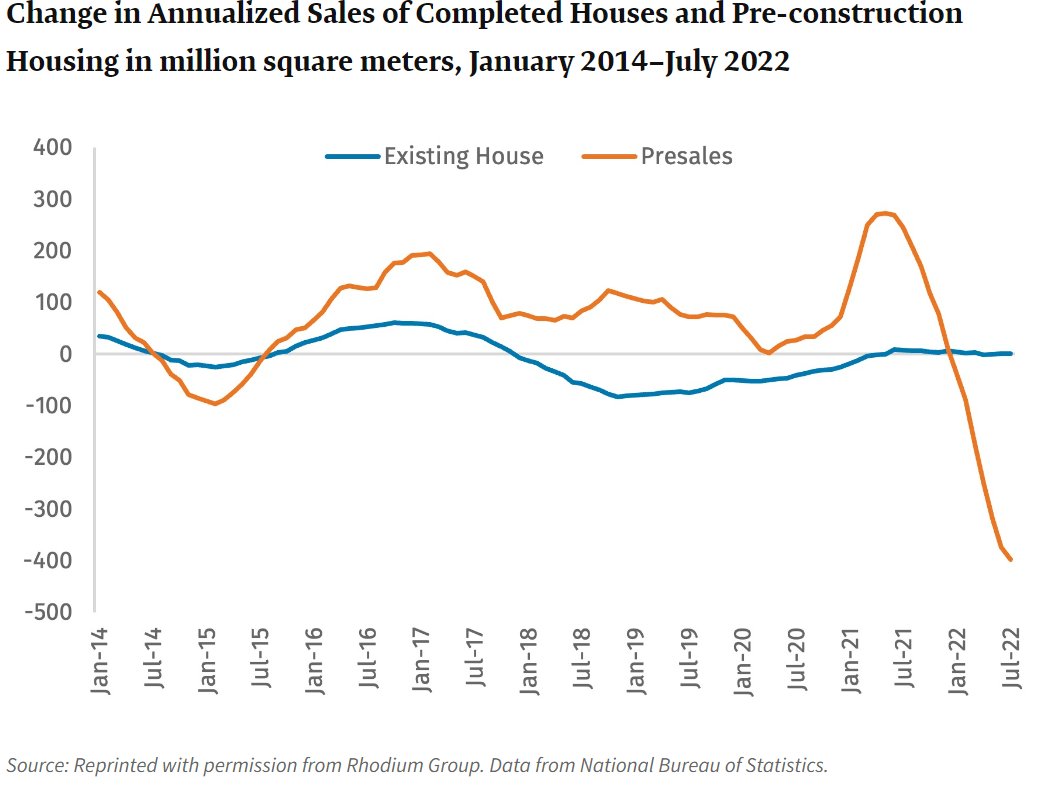

The second difference is a risk to my belief that China's economy will not avoid a recession. The fact is China has massive financial reserves. As of August 2022 , China's foreign exchange reserves dropped to the lowest since October 2018, but US$3.1t is no laughing matter. For comparison, the U.S. international reserve position stood at US$228b as of 21 October 2022 . In my opinion, China's political realities not only make it possible for the regime to issue massive bailouts combined with government takeovers and prosecutions but make it a likely occurrence. In September , S&P Global Ratings estimated US$99b was necessary "to ensure distressed developers can finish presold homes." Still, I doubt even a full-blown bailout of the real estate sector (likely costing well over US$1t) would prevent a recession, but it's still a risk to consider, and I believe a more minor but significant bailout is more likely.

{kind=link}

Change in Annualized Sales of Completed Houses and Pre-construction Housing in million square meters, January 2014 – July 2022 (Center for Strategic & International Studies)

The real estate sector is the source of many of China’s financial problems, with other key industries suffering knock-on effects. For example, an estimated 29% of the Chinese steel industry has announced it’s close to bankruptcy. Unfortunately, China’s credit crisis is far too complex to cover here appropriately. For more information, I recommend the Center for Strategic & International Studies 21 September 2022 report, China’s Slow-Motion Financial Crisis Is Unfolding as Expected .

What has driven the credit crisis into overdrive was China’s insistence on a zero-tolerance policy towards COVID-19. This policy has since been overturned, but the damage is essentially already done, and there are multiple reports that the country is being swept by a massive wave of COVID-19 since restrictions were removed. It seems likely this will lead to further global supply and logistics disruptions and even the potential for the resumption of COVID-19 restrictions. Although, I believe China reinstating its zero-tolerance policy are low at this time.

Altogether, it seems clear that China will most likely enter a deep recession within the next 12 months. With the world’s second-largest economy (by GDP) in such a challenging financial position, world recession risk is high.

OPEC+'s cuts are completely overblown

As I have discussed before, this is a follow-up report on my oil short position. As you should now know, my first report was called Why Oil Is A Broken Market Ripe For A Short . Many of you may have taken that statement as enthusiastic language to garner clicks. It's not; I genuinely believe oil bulls have broken the market due to a reliance on outdated core beliefs, false and misleading information, and biased reading of facts. A perfect example of this was OPEC+'s recent production cuts. For the purposes of this report, OPEC+ will be defined as OPEC and non-OPEC partners.

When I first heard about OPEC+'s decision to cut production, I thought my position might be blown. But notice how I said heard, not read because once I looked into the cuts, it became clear that not only would they upset both sides of the aisle in the U.S., but they were largely irrelevant. So let's dive into why.

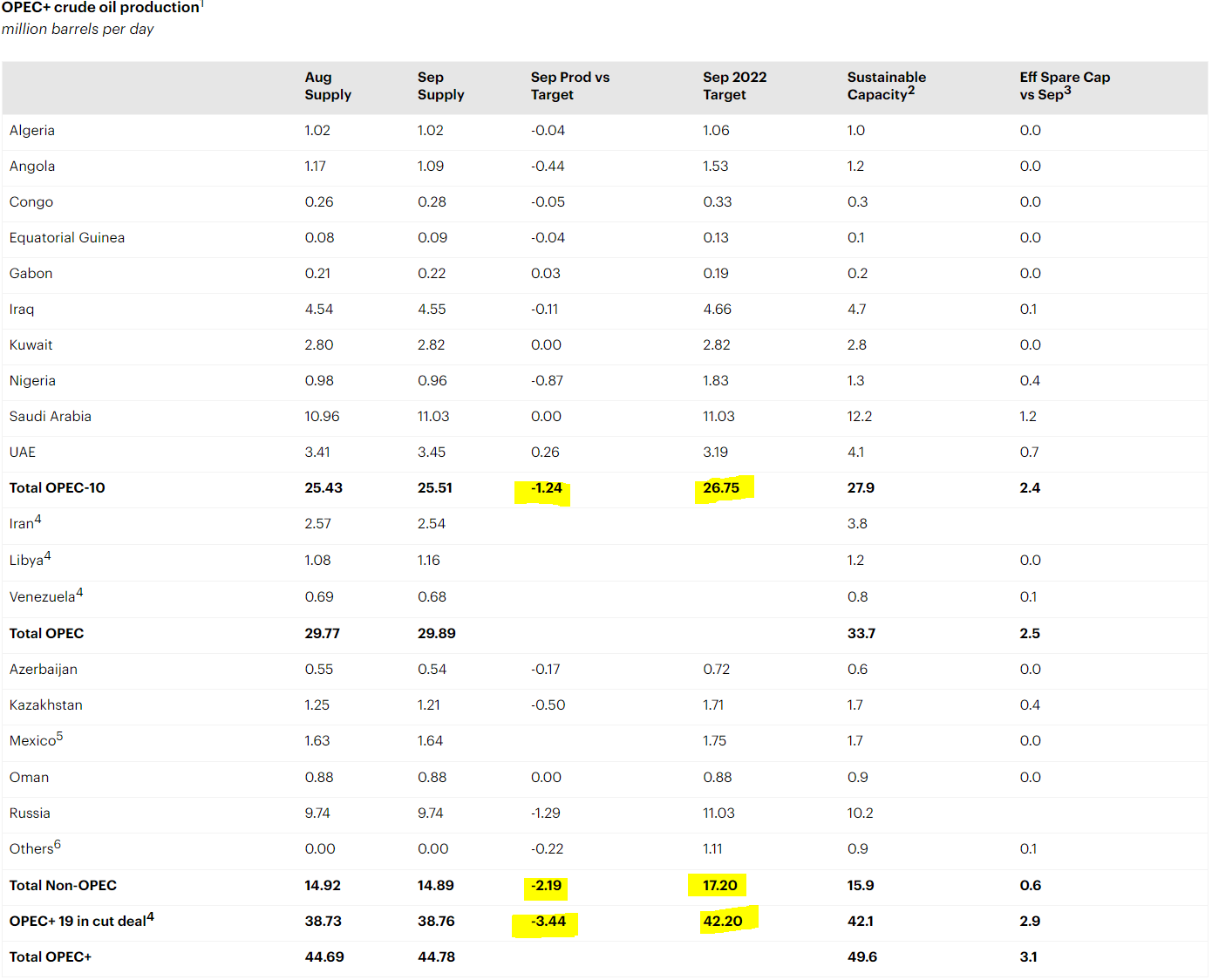

First, let's take a look into the October 5, 2022, cuts themselves.

{kind=link}

OPEC+ Crude Oil Production Table September (IEA)

As highlighted in the above table, OPEC+ was missing its production targets by 3.44m barrels per day when the cuts were announced. Therefore, OPEC+ is effectively not taking any actual barrels of oil off the market but instead cutting its ideal production closer to its realistic capacity.

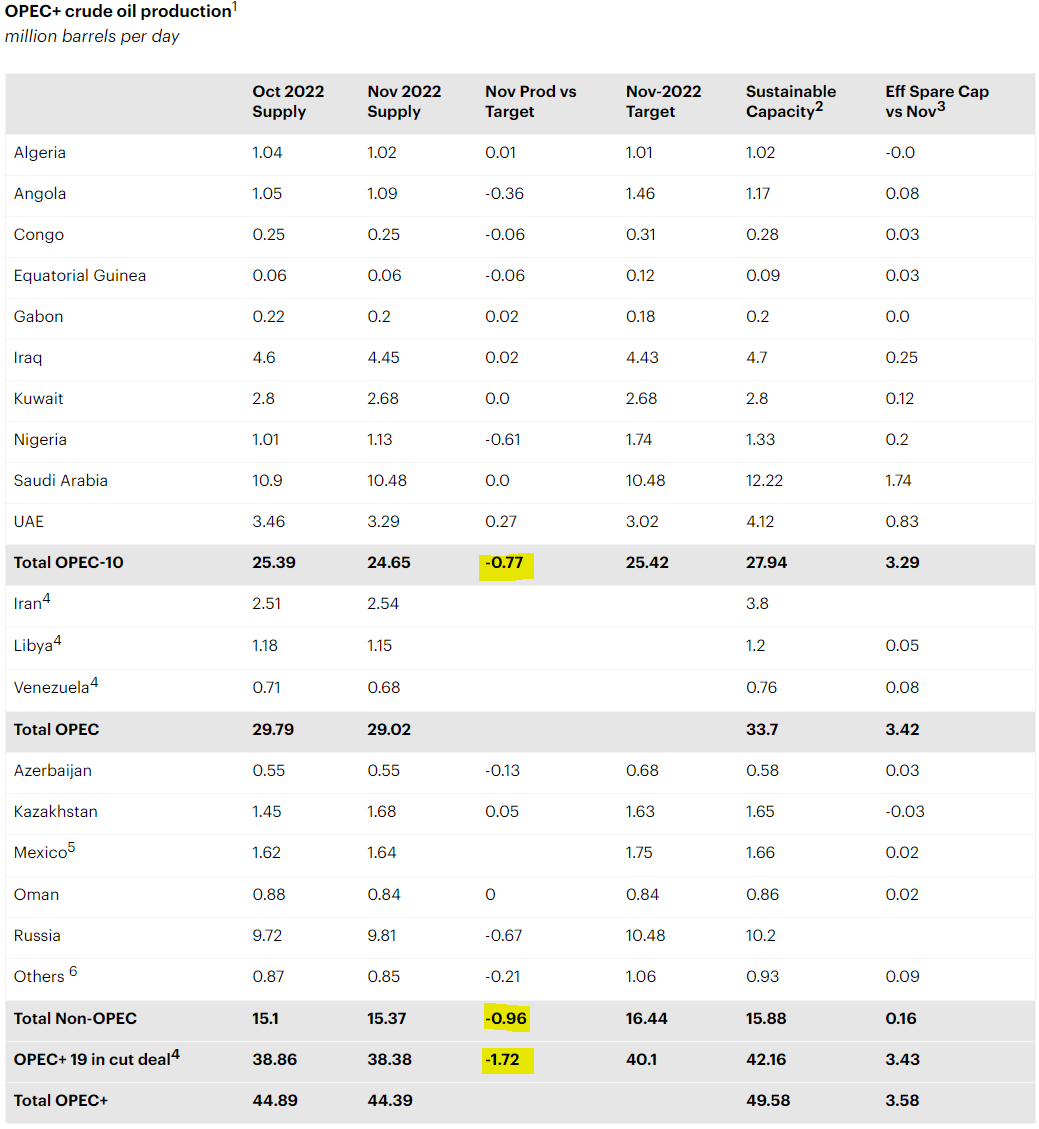

OPEC+ failing to meet its production targets is nothing new and will likely continue far into the future. In fact, OPEC+ missed its target production levels by 1.72m barrels per day in November, the month the cuts went into effect.

{kind=link}

IEA OPEC+ Crude Oil Production Table November (IEA)

In another piece of bad news the market chose to ignore, the December 2022 IEA report announced Russian imports had actually increased, despite market panic over Putin's threats:

For now, Russian oil continues to flow. In November, total oil exports increased by 270 kb/d to 8.1 mb/d, the highest since April. Crude oil loadings were unchanged on the month at just over 5 mb/d, despite a 430 kb/d drop in shipments to Europe. By contrast, product flows (in particular of diesel) surged, including to Europe. Russian oil production rose 90 kb/d to 11.2 mb/d, just 200 kb/d below pre-invasion levels.

So what did the oil cuts really achieve?

For one, the market bought heavily on the news, with WTI Crude rallying in response throughout October 2022.

But I think the cuts have and will backfire on OPEC+ and the oil bulls.

Why? I believe all the cuts have done, in reality, is upset the current U.S. administration, given rise to additional claims of attempts to influence elections due to their timing and support of Russia against Ukraine, propelling the U.S. government to action.

The Chevron/Venezuela deal is likely just the start

One of the first moves by the U.S. in response to OPEC+'s recent cuts was the announcement of a deal with Venezuela. But before we dive into the deal reached with Chevron, we need to briefly explain why this is such a risk for oil bulls in the medium to long term.

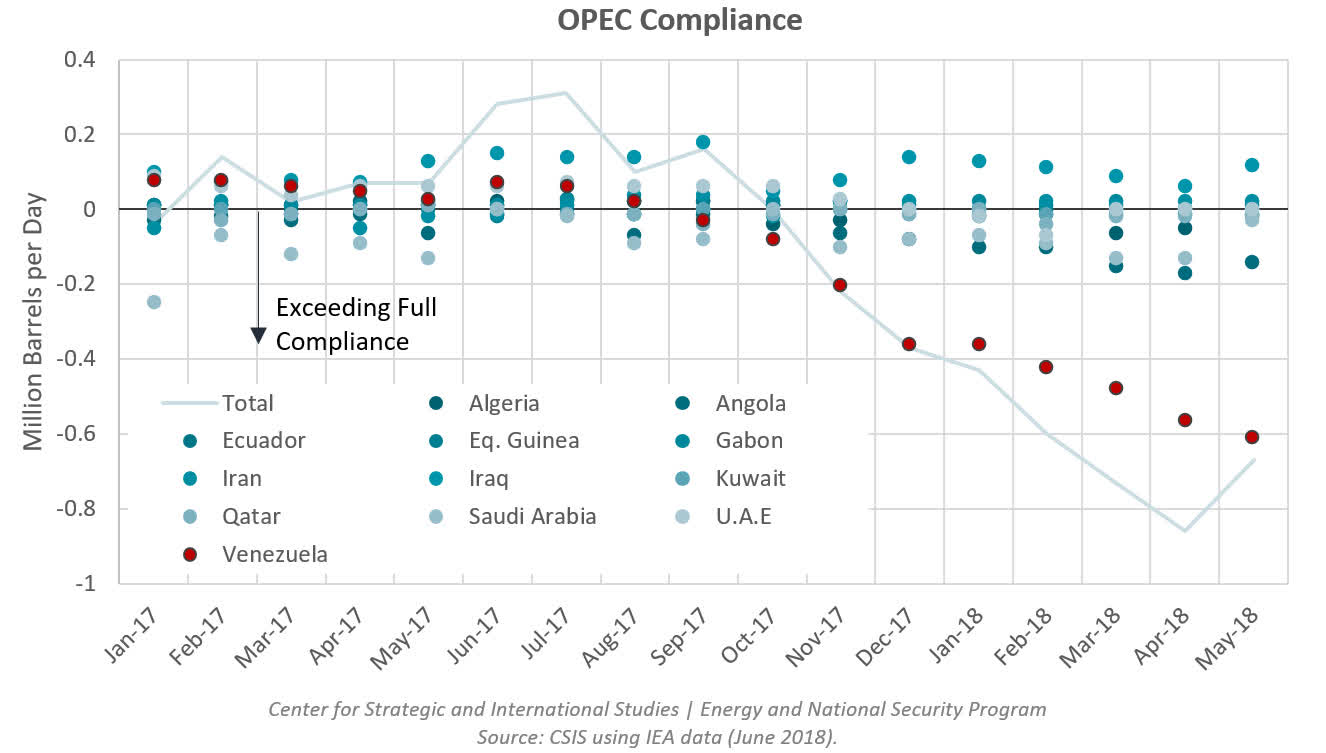

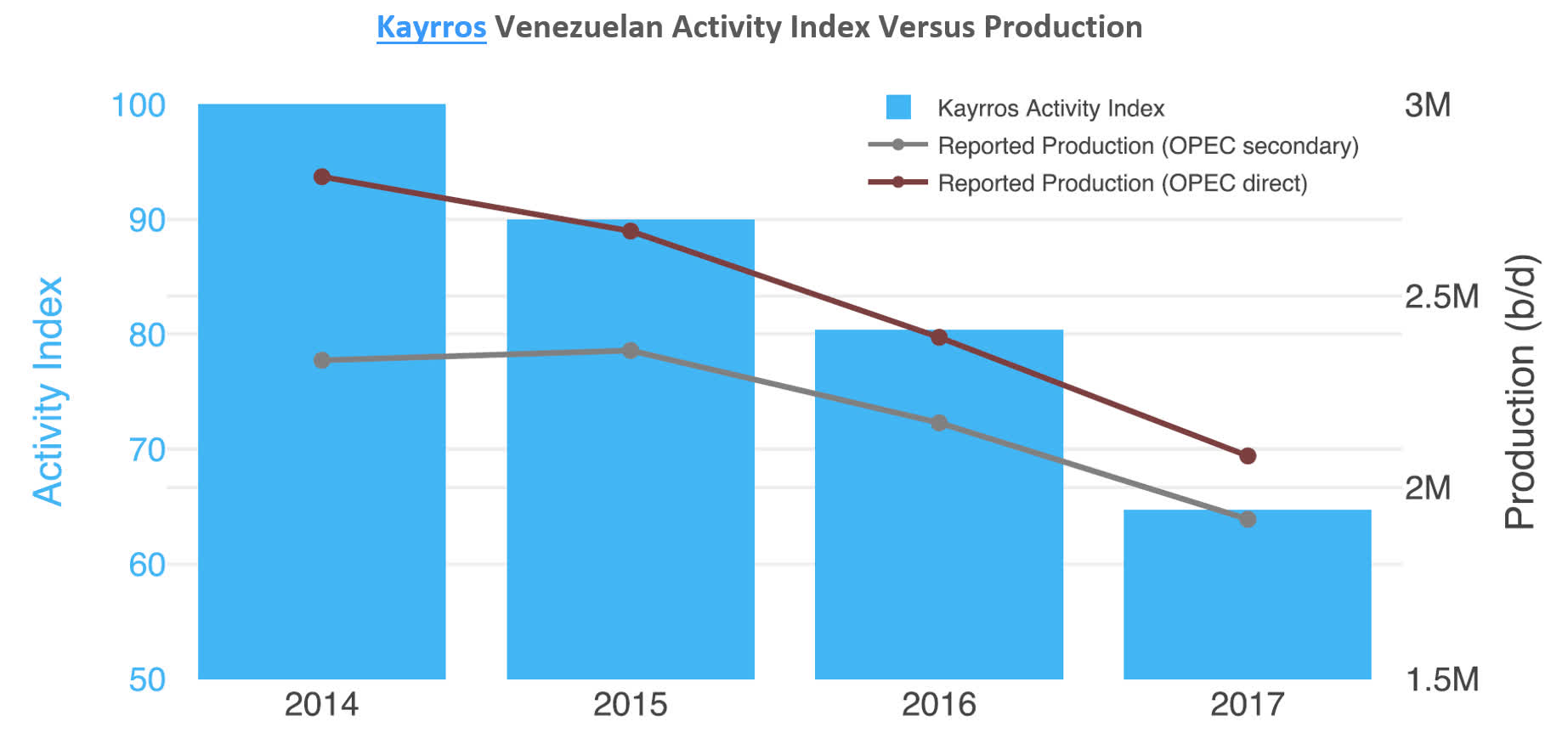

Venezuelan crude oil production reached its monthly output high at the end of the 1990s. But as the new millennia rolled around, production began to decline. At first glance, it might seem like the direct result of the governmental regime and the instability this caused, and this is true to a point. But the primary reason is underinvestment and mismanagement caused by the removal of the skilled workforce.

But don't just take my word for it; the Center for Strategic & International Studies published a comprehensive report, How Low Can Venezuelan Oil Production Go? on 18 June 2018. The report stated:

Venezuela’s deteriorating condition looks poised to continue and only get worse... The culmination of chronic mismanagement and underinvestment, which resulted in shortages of basic equipment and supplies for years now across Venezuela’s oil fields, has all taken its toll.

The report further highlighted the point in the two graphs below.

{kind=link}

Venezuela OPEC Compliance ((CSIS))

{kind=link}

Kayrros Venezuelan Activity Index Versus Production ((CSIS))

So sure, instability caused part of the problem, but the primary issue is a lack of skilled labor and equipment. This is why I believe the new Chevron deal, sanctioned by the U.S. government partially in response to OPEC+'s cuts, poses a significant unknown risk to mid-long-term supply projections.

In a nutshell, October 5, 2022 , saw the Biden administration announced a plan to reduce sanctions on Venezuela's regime. The reduction in sanctions was specifically targeted to allow Chevron and potentially other U.S. companies to resume pumping oil in the country. In exchange, the Venezuelan regime resumes talks with the opposition about elections in 2024. Remember, the reduction in sanctions is predicated on talks resuming, not them being successful.

As the Wall Street Journal reported:

Venezuela, which sits atop some of the world’s largest oil reserves, could serve as a longer-term strategy for the U.S. and European countries...

With Chevron in charge of all aspects of the projects, and the U.S. providing clearance to export oil, Venezuela could regain the relevance in the oil market that it enjoyed during the early 2000s, when it was one of the main exporters of crude to the U.S. The country is now exporting about 450,000 barrels a day and could double that figure in a matter of months, say people who are familiar with Venezuela’s oil industry and are bullish about its prospects.

Since the deal was first announced, the U.S. has granted Chevron a license in November to resume oil production and expansion operations in Venezuela. As a result, January 10, 2023, saw the first Chevron-chartered tanker carrying Venezuelan oil leave for Mississippi, and two others are expected to depart and deliver over the next month.

This is likely just the beginning of oil flowing out of Venezuela as efficient and well-resourced U.S. companies like Chevron resume operations. Additionally, I believe the U.S. has other levels it will pull in response to OPEC+'s cuts, including placing pressure on domestic oil producers to increase production. For example, the United States administration threatened oil companies with higher taxes if they did not increase production, as reported by CNBC on 31 October 2022 . Remember, whether intentional or not, by cutting oil production, many Republicans and Democrats now see OPEC as siding with the Russians against Ukraine.

Conclusion

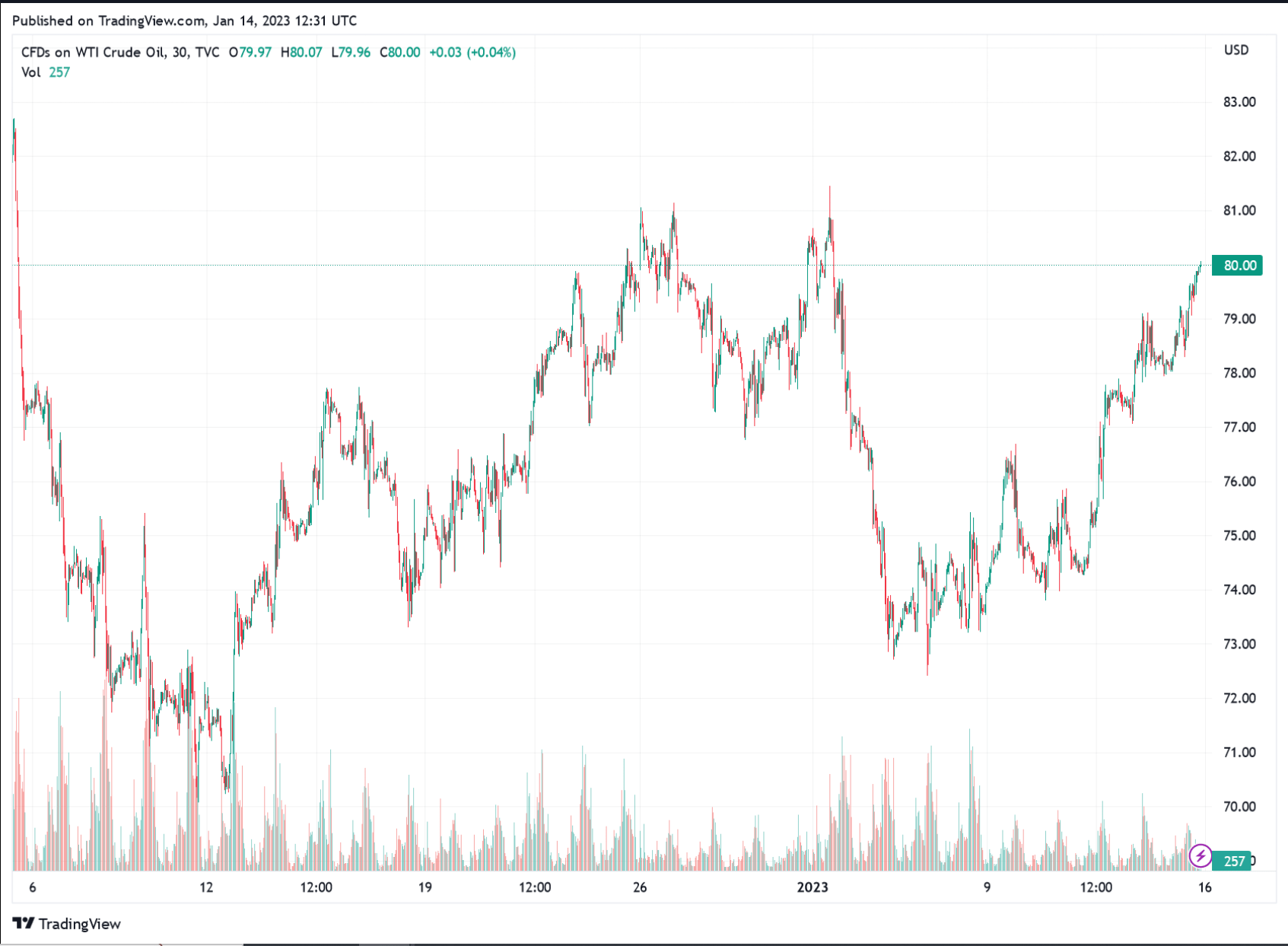

In conclusion, the only thing that has changed since my first report is the risks are mounting and oil has reduced its trading range.

{kind=link}

Oil Trading Range (TradingView)

Where before good news would send the price shooting towards $100 a barrel, now the price can barely breach $80 before crashing down towards $70, where it is spending a lot more time. I see this as a sign the market is moving more towards my way of thinking and is finally recognizing it has woefully misread oil's risk profile.

Even excluding the risks, it's clear that there is a lack of a fundamental basis for oil's price when we look at both long-term prospects and more recent historical data.

I will admit one risk which has mostly faded into the background is the Iran deal, mentioned in my previous report. At this time, it seems highly unlikely it will go through. However, if the recent protests either bring significant concessions (a decent possibility) or are quashed, and the global economic situation deteriorates sufficiently towards a recession, the risk may re-emerge.

All-in-all, I believe you will now be able to understand why my short-medium term base case for the price of oil is $65, having successfully reached my base case of $70 stated in my previous report. However, the best case (from a short perspective) remains between $50 and $60. If you would like to dive deeper into my research, please find my excel document below and check out my previous report.

Excel Source Documents

For further details see:

OPEC+ Cuts Irrelevant: Oil Still A Short