COM - OPEC+ Has Not Spoken: VDE Is In The Buy Zone

2023-11-28 13:08:38 ET

Summary

- OPEC faces disagreement on production policy, causing a delay in the biannual meeting and sending futures markets lower.

- Saudi Arabia and Russia control OPEC and need higher oil prices for their respective economic and geopolitical reasons.

- U.S. energy policy and commitment to climate change initiatives are uncertain, but crude oil continues to power the world.

- Vanguard Energy Index Fund ETF Shares could be a compelling pick for 2024.

On November 26, 2023, the OPEC oil ministers should have met in Vienna, Austria, for the 36 th OPEC and non-OPEC ministerial meeting. The international petroleum cartel faces oil prices (CL1:COM) around the $77 per barrel level on nearby January WTI NYMEX futures and the $82 per barrel on the January Brent futures.

Prices have declined from the March 2022 highs at over the $130 per barrel level and have remained under $100 per barrel throughout 2023. Crude oil is a highly political commodity, facing wars in Ukraine and the Middle East, a bifurcation of the world’s nuclear powers, and climate change policies in the U.S. and Europe.

OPEC aims to achieve the highest possible petroleum price while balancing supply and demand fundamentals. However, the cartel has increasing control of supplies, translating to significant price influence. Over the past meetings, OPEC has tightened supplies, citing Chinese economic weakness, but the geopolitical landscape has been a substantial backdrop to the cartel’s policy decisions.

The Vanguard Energy Index Fund ETF Shares ( VDE ) owns shares in the leading U.S. oil-related companies. VDE moves higher or lower with crude oil prices.

OPEC has a problem- Disagreement on production policy

OPEC’s biannual meeting in late November establishes the cartel’s production policy for the coming year. The cartel scheduled the late 2023 meeting for Sunday, November 26, but the oil ministers could not agree on output quotas during preliminary meetings, causing a delay in the meeting until the end of November.

Over the past months, Saudi Arabia singlehandedly cut production, supporting higher petroleum prices. The Saudis want help from the other cartel members, but that assistance was not forthcoming at preliminary meetings, causing a delay until Thursday, November 30.

The November 22 news that OPEC cannot agree on production quotas sent futures markets lower.

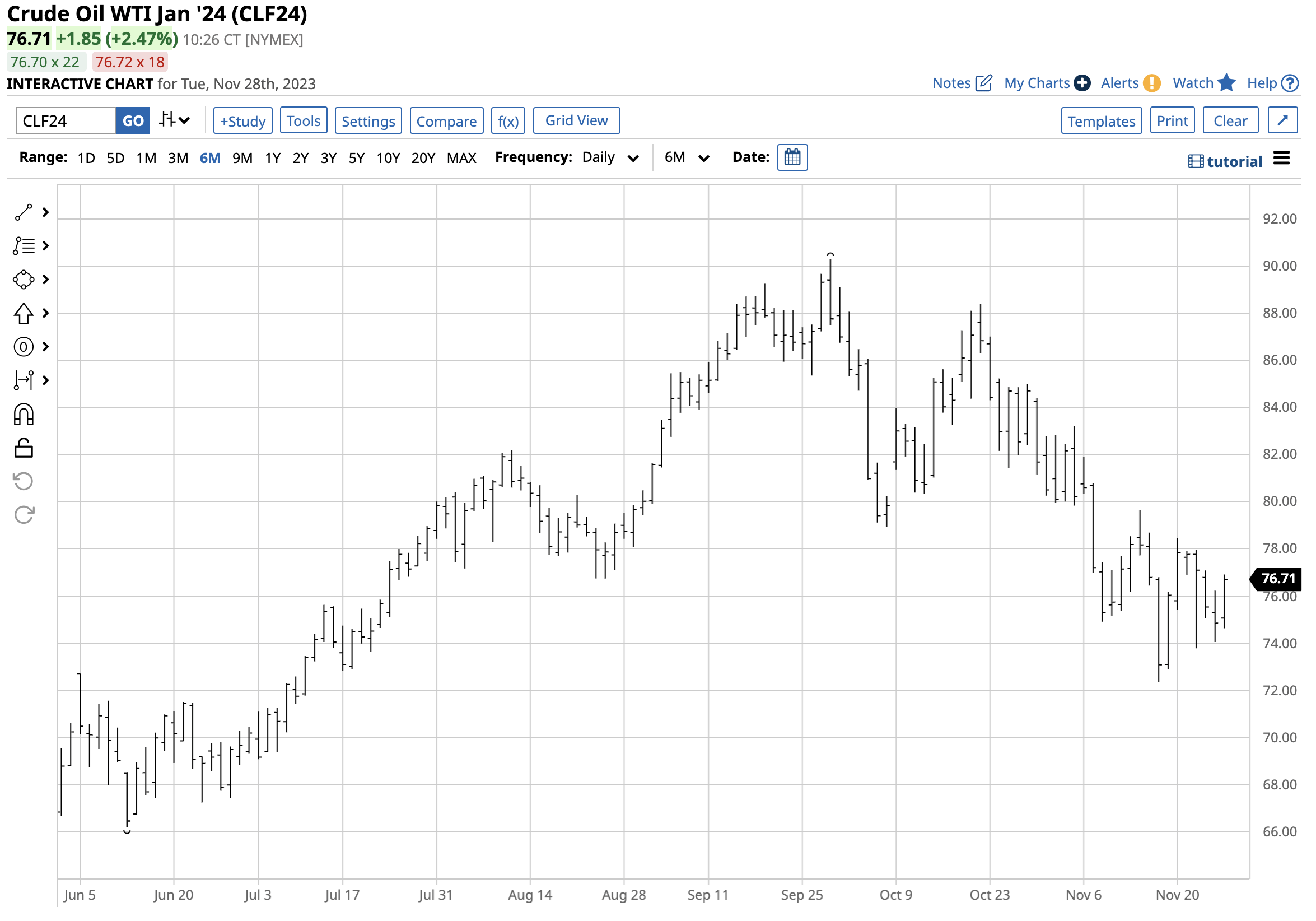

Six-Month Chart of January NYMEX Crude Oil Futures (Barchart)

{kind=link}

After the meeting’s delay, the chart highlights that selling on November 22 sent NYMEX WTI futures to a $73.79 low.

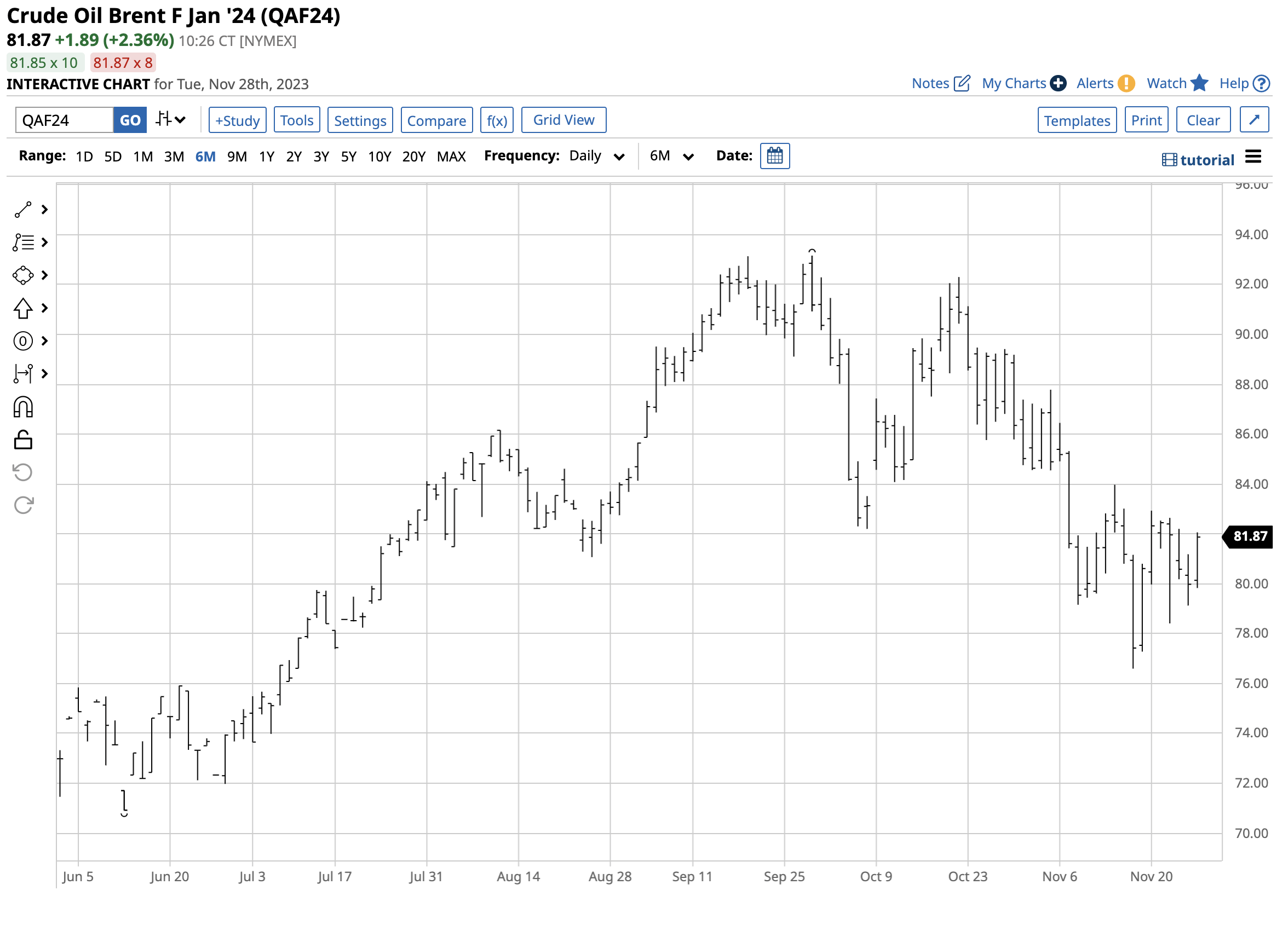

Six-Month Chart of January Brent Crude Oil Futures (Barchart)

{kind=link}

Brent futures declined to a $78.41 low on November 22. While the leading crude oil benchmark futures contracts dropped, they remained above the November 16 lows, which are the technical support levels.

On Tuesday, November 28, two days before the virtual OPEC meeting, January WTI futures were at the $77 level, with January Brent futures trading around $5 higher at $82 per barrel.

Saudi Arabia and Russia control OPEC and need higher prices

Since Russia began cooperating with OPEC in 2016, the cartel’s production has been a function of negotiations between Riyadh, Saudi Arabia, and Moscow. Iran, another cartel member, is a Russian ally and an enemy of the Saudi Royal Family. The geopolitical interrelationships between the cartel’s members make any decision-making challenging. Consensus between oil-producing countries that are OPEC members is like herding feral cats.

Meanwhile, Saudi Arabia requires at least an $80 per barrel price to balance its domestic budget. Russians need the highest possible oil price that allows them to sell the maximum level of petroleum to fund its ongoing war in Ukraine. Iran favors a policy enabling it to sell as much crude oil as possible. Meanwhile, China has likely purchased Russian and Iranian oil at discount prices over the past months, sidestepping quotas and angering the Saudis who have trimmed output.

Climate change remains a policy path in the U.S. and Europe- Oil still powers the world

The 2020 U.S. election caused a 180-degree shift in energy policy. The drill-baby-drill and frack-baby-frack policies of the Trump administration gave way to addressing climate change under the Biden administration. The current U.S. administration encourages alternative and renewable fuel production and consumption and inhibits fossil fuel output. However, U.S. oil policy has been somewhat of an enigma for three reasons:

- The Biden administration sold crude oil from the U.S. Strategic Petroleum Reserve ("SPR"), causing a decline from over 600 million barrels in late 2021 to 351.3 million as of November 17. The U.S. SPR fell to the lowest level in four decades as the administration sold oil after Russia invaded Ukraine, and prices rose above the $130 per barrel level, the highest price since 2008. While the administration set a $67-$72 target for SPR repurchases, it has only bought around four million barrels even though the price fell into and below its target zone over the past months. The low SPR level reflects the U.S. desire to cap prices but could also be a plan to reduce stockpiles given the climate change initiatives.

- According to the U.S. Energy Information Administration, U.S. production has increased to 13.2 million barrels daily, matching the highest level during the previous administration. Rising production reflects the U.S. demand for crude oil.

- If President Biden loses the 2024 election, the U.S. energy policy path could take another 180-degree turn.

The bottom line is that the future of U.S. energy policy and a commitment to climate change initiatives are in the hands of voters in November 2024. The bottom line is crude oil continues to power the U.S. and the rest of the world.

Three reasons for higher oil prices and profits for the leading U.S. oil-related companies

The three factors that will support crude oil prices over the coming months and years are:

- Actions speak louder than words. While the U.S. administration favors less fossil fuel production and consumption, U.S. crude oil output is at a record 13.2 mbpd high. Moreover, the administration is a lurking buyer of crude oil to replace the SPR at $67-$72 per barrel.

- While the U.S. and Europe support climate change initiatives, China and India, the world’s most populous countries, will continue to consume increasing amounts of crude oil, coal, and natural gas. OPEC members will happily supply China and India, and when the economies improve, the oil demand will rise.

- Consolidation in the U.S. traditional energy-related sector has caused the leading companies to increase their market shares. Moreover, higher oil prices since the 2020 lows have increased profits after the top integrated U.S. oil companies, Exxon Mobil ( XOM ) and Chevron (CVX), trimmed expenses and increased profitability.

Even if oil prices remain around the $80 per barrel level, U.S. oil-related companies will profit. Higher prices will only turbocharge their earnings.

VDE could be a compelling ETF for 2024

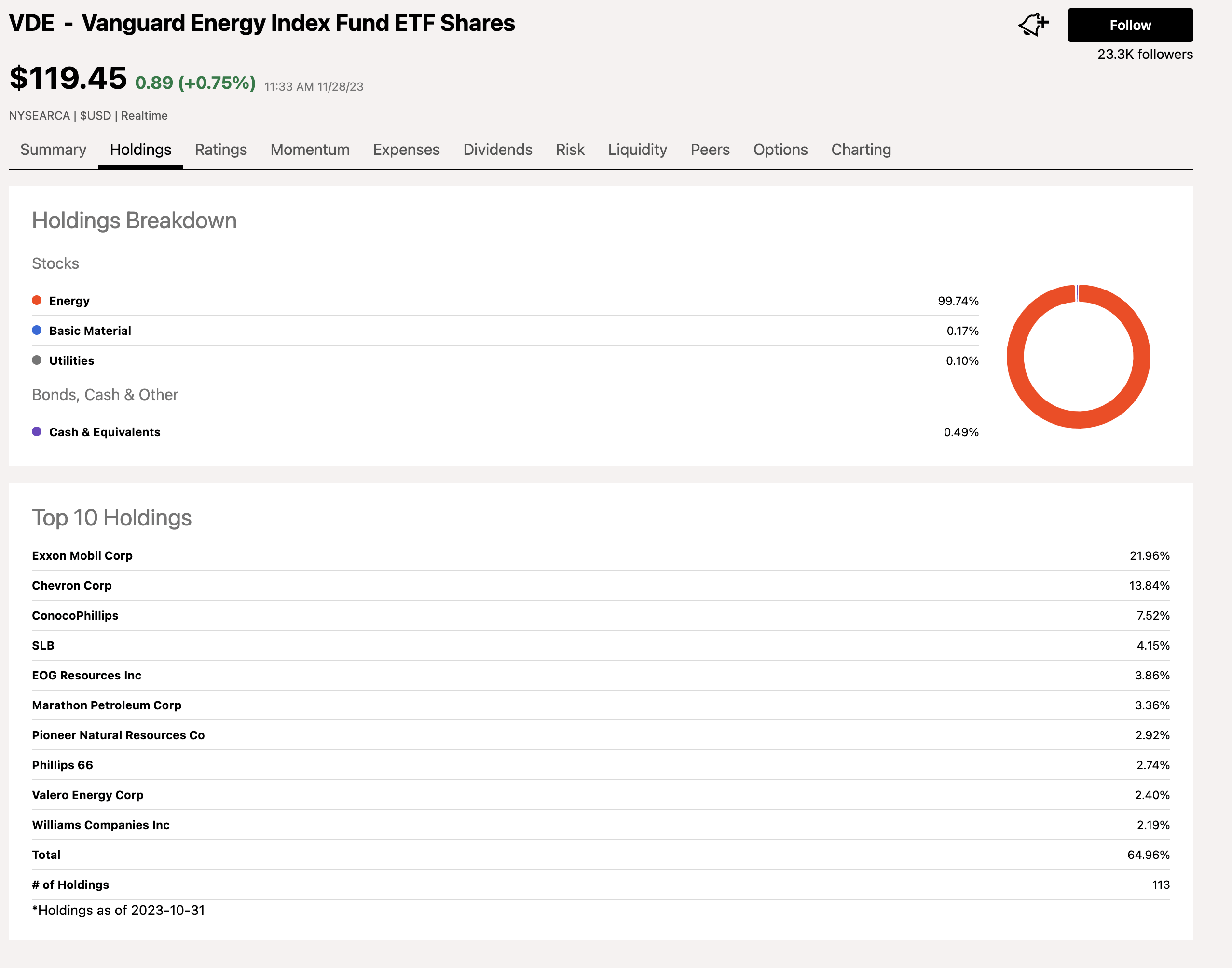

The top holdings of the Vanguard Energy ETF include:

{kind=link}

VDE invests over 35% of its $9.85 billion in assets under management in XOM and CVX. VDE is a highly liquid product that trades over 520,000 shares daily and charges a 0.10% management fee.

At $119.45 per share on November 28, VDE’s $4.22 dividend translates to a 3.53% yield. The dividend is well above the average 1.43% yield of the SPY that tracks the diversified S&P 500 index.

Further delays or conflicts within OPEC could lead to a short-term flood of crude oil onto the market during a seasonally weak time of the year. However, the cartel is not likely to cut off its nose despite its face and will eventually agree and compromise on production policies and output quotas for 2024. I view any selloffs as a buying opportunity for crude oil and the VDE ETF product. Moreover, the lower crude oil prices fall, the more likely the administration will purchase crude oil for the SPR, which remains at the lowest level in four decades. The wars in the Middle East and Ukraine increase the potential of 1970s-style oil embargos, and the U.S. cannot afford to leave the SPR at such a low level, given the state of the geopolitical landscape.

I am a buyer of Vanguard Energy Index Fund ETF Shares at the current price, leaving plenty of room to add on further declines. VDE’s all-time high was $145.97 in June 2014, and I expect the ETF to climb above that level in 2024.

For further details see:

OPEC+ Has Not Spoken: VDE Is In The Buy Zone