MSFT - Oracle: An Underappreciated Cloud Giant Worth Buying

Summary

- Oracle has seen a terrible decade with almost no revenue growth at all, despite 11 acquisitions over the last 5 years.

- Yet, I expect this to change in the decade ahead, with Oracle finally accelerating its cloud efforts and showing solid growth rates as a result.

- Oracle has an excellent cloud offering, and its already large customer base give it plenty of opportunities to cross-sell its cloud products.

- Increased security and a focus on multi-cloud are just two factors that give Oracle an advantage versus the competition.

- I can see Oracle grow EPS at between 15% to 18% a year and believe it is currently undervalued as I calculate a target price of $106 at the midpoint.

Introduction

Cloud computing has been a talking point across all sorts of industries for a couple of years now. Businesses and individuals are moving their computing resources and data from local, on-premises hardware to remote servers and services that are accessible over the internet - to cloud servers.

In the past, businesses saved and hosted their data and systems on on-premises storage locations. This resulted in high maintenance costs for the servers while requiring a lot of space, on top of it being quite expensive as well. Cloud services offer a way to shift some of the IT infrastructure costs from capital expenditures to operating expenses, providing cost savings and flexibility. In addition to this, having your systems and data in the cloud means you can access it whenever and however you want by simply logging in. Also, cloud providers typically offer better security measures than many businesses can implement on their own, making the cloud an attractive option for businesses looking to improve their security posture.

The Covid-19 pandemic and the lockdown following as a result, caused an acceleration of this shift to the cloud. With many people being forced to work from home, many businesses were forced to accelerate their cloud plans to enable their employees to continue their everyday jobs from home. Cloud made it easier for employees to access company resources and collaborate with colleagues from home without many problems. Cloud-based tools for communication, project management, and file sharing became essential for maintaining productivity and keeping businesses running. Savings costs in tough economic times and increasing cybersecurity were other drivers following the covid pandemic.

And the shift is far from over with businesses expected to significantly increase their cloud budgets over the next decade as it increases in importance. About ¾ of businesses are now using cloud services, with 57% of organizations moving their workloads to the cloud in 2022. This drives significant growth for this market, resulting in an expected growth CAGR of 19.9% until 2029, resulting in a market value of $1.7 billion. AI could very well be the latest driver of cloud computing adoption.

Many investors have made solid profits by riding the cloud wave already, but it is not too late to step in on this secular trend today as illustrated by the expected growth rates shown above. Yet, while many focus on the big tech cloud leaders Microsoft ( MSFT ), Google ( GOOGL ), and Amazon ( AMZN ), I believe ERP leader Oracle ( ORCL ) can show a performance that is at least as strong, if not better. The company is often overlooked when considering the large cloud vendors, but the company has rapidly been gaining market share in this market and looks well positioned to continue on this trajectory with it quickly growing its solid offering and large existing customer base waiting to also make the shift.

I have had my eye on Oracle Corporation for some years now, but I kept on having some doubts about its prospects. The last 5 years have not been particularly great for the company with it seeing disappointing organic growth, resulting in a large number of acquisitions that often did not contribute as much to top-line growth as anticipated. As a result of this acquisition spree in desperation for top-line growth, the debt burden has increased quite a bit, making the company even less attractive to investors. Yet, over the last several quarters, Oracle has shown an impressive (out)performance with its cloud computing segments and products taking off, and easily outperforming competitors, resulting in market share gains.

Therefore, within this article, I will take a deep dive into Oracle to see if it is a good buy at its current share price based on business fundamentals and growth prospects & expectations.

So now, after this very long introduction, let’s dive in!

Oracle Corporation

Oracle is a company that might not be as well-known as other large software companies like Microsoft or Google but is an incredibly large company with a market cap of $239 billion and has an impressive presence in enterprise software.

Oracle Corporation was founded in 1977 and is one of the survivors of the dot-com bubble in 2000. The company originally focused on developing a relational database management system (RDBMS) called Oracle Database, which quickly became a popular choice for enterprise applications. In the 1980s and 1990s, Oracle expanded its product portfolio to include enterprise software systems for managing business operations such as enterprise resource planning ((ERP)), customer relationship management ((CRM)), and supply chain management ((SCM)).

Nowadays, Oracle still largely offers these same services and products to businesses. These products are designed to help organizations manage their operations more efficiently and effectively, and Oracle, due to its many decades of experience, is one of the largest players for these enterprise software packages. This results in over 340,000 customers in 175 countries.

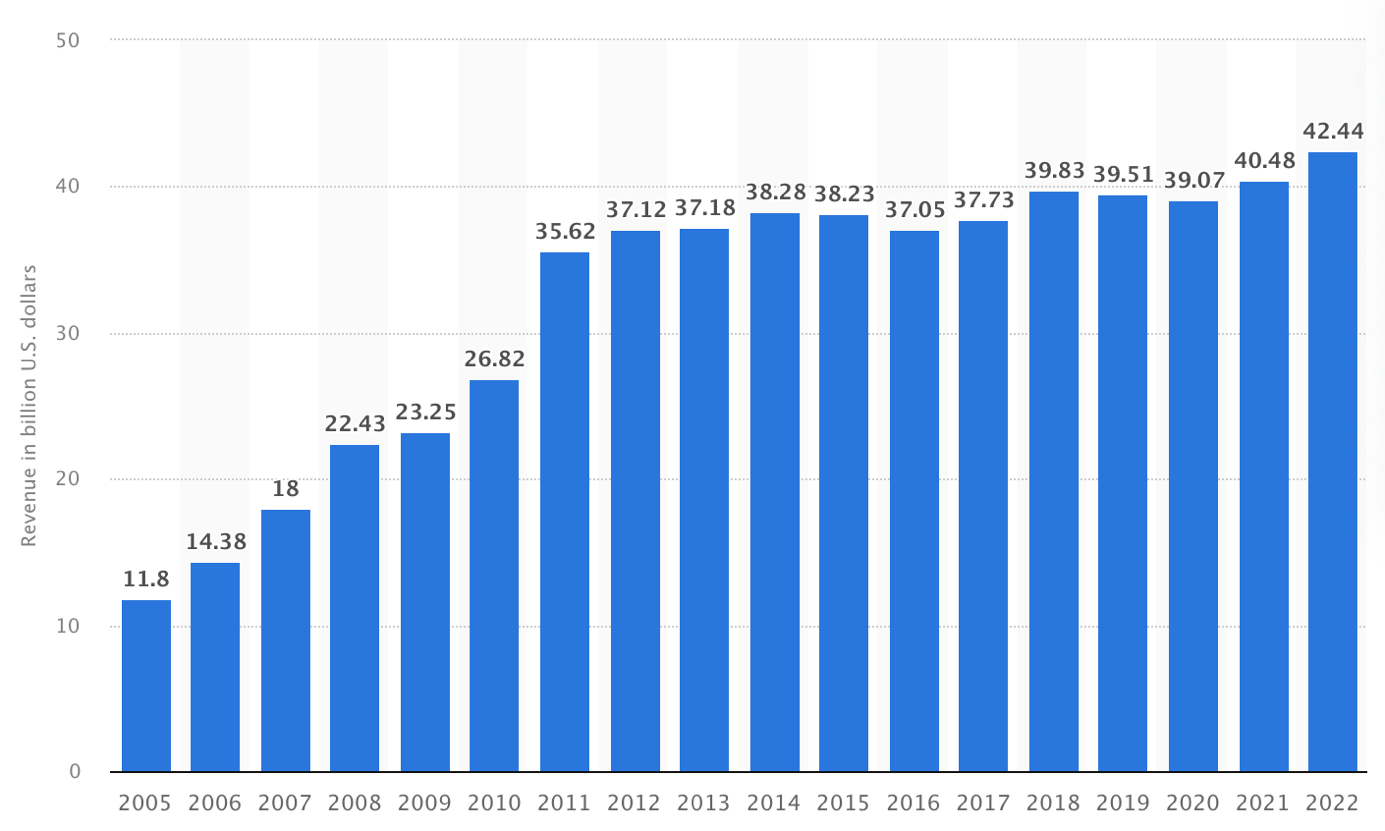

Yet, while its market position is very strong, the markets are not the fastest growing ones as they have matured, and new software entrants are taking away market share. This has resulted in somewhat disappointing revenue growth over the last decade and had the company desperately searching for new revenue streams, most often through M&A. Oracle has acquired over 150 companies, including 11 over the past 5 years. The largest one to date was Cerner back in 2022 for a total of $28.3 billion and the company has in total spent over $110 billion in M&A. This has massively increased the debt burden of the company and has not yet resulted in the growth the company has been looking for as can be seen below. Oracle has seen a very disappointing revenue growth CAGR of just 1.35% since 2012.

Oracle revenue growth (Statista)

{kind=link}

This does compare quite badly to software peers like Microsoft which has seen much faster growth over the same period, and this is in part due to the late shift of Oracle towards cloud solutions. Oracle has been slow to transition to a cloud-based revenue model, which has put it at a disadvantage relative to some of its competitors who were early adopters of cloud technology. This has resulted in slower revenue growth in areas such as infrastructure as a service (IaaS), platform as a service (PaaS), and software as a service (SaaS), which are becoming increasingly important revenue streams for technology companies.

Yet, the narrative is shifting, and Oracle is rapidly taking market share in cloud computing today. One of Oracle's primary cloud offerings is its Oracle Cloud Infrastructure ((OCI)), which provides a range of cloud computing services, including compute, storage, networking, and databases. OCI is designed to be highly secure, reliable, and scalable, and it is aimed at enterprise customers who are looking to move their mission-critical workloads to the cloud.

Oracle has also been expanding its cloud applications portfolio, with offerings such as Oracle Fusion Cloud Applications, which include ERP, human capital management ((HCM)), SCM, and customer experience ((CX)) applications. These cloud applications are designed to help customers modernize their IT environments, improve efficiency, and reduce costs.

And while Oracle was initially slow to adopt cloud technology, the company has since made significant investments in cloud infrastructure and applications and has been increasing its efforts in cloud computing in recent years, positioning it much better to take back market share and see increased growth.

{kind=link}

So, now that we have a better idea of the company and its offerings, let’s dive deeper into the company’s competitive advantage, growth drivers, and additional reasons to invest before we move on to the recent financial results.

Competitive advantage & growth drivers

As said before, the cloud industry is a highly competitive one, making it quite hard to distinguish yourself from the competition. The three cloud giants offer a very complete package of solutions and are perceived as the best cloud platforms, so why go with the “outsider”, in this case being Oracle? One thing that jumps out right away once you start researching the cloud offerings and enthusiasm among customers, is that Oracle services companies across all industries, showing very broad acceptance of its offerings. Also, almost all customers point out that Oracle is able to offer significantly more business value for those customers, giving them no reason to shift to other cloud vendors. The more large customers Oracle acquires that are enthusiastic about the value it offers, the more it will be talked about. And in the end, there is not much stronger than word of mouth across industries, and so I expect this to bode well for customer additions for Oracle.

And another significant factor that helps Oracle gain more customers at a faster pace compared to competitors is the fact that it already has a huge customer base of over 430,000 that all need to make the shift to the cloud at some point as well. Despite the loss of market share over the last couple of years to cloud-native companies offering enterprise software solutions, Oracle remains one of the leaders worldwide. With a great number of its clients already using the Oracle software solutions for many years or even decades, these will most likely prefer to keep using Oracle to also move those workloads to the cloud with Oracle Fusion. Oracle has excellent cross- and upsell opportunities to increase value per customer by upgrading its existing customer base to more lucrative cloud products.

Why would a customer with a decade-long relationship with Oracle through enterprise software not also choose to use Oracle Cloud ((OCI)) with it shifting the software it is already using, to Oracle Fusion? If a company already uses Oracle's on-premises software, then Oracle's cloud offering can be a natural extension of that infrastructure.

Another factor that could make Oracle cloud look more attractive compared to many competitors is the acceptance of multi-cloud. While Oracle believes its cloud offerings are better than competitors, they know few customers go all-in on a specific environment and prefer to use multiple cloud vendors. Instead of relying on a single cloud provider, a multi-cloud strategy allows an organization to leverage the strengths and capabilities of multiple providers, while also mitigating the risks associated with relying on a single provider. This is what CTO Ellison said back in September regarding multi-cloud:

Our job is to give our customers the ability to choose application and infrastructure technology from multiple cloud providers, and then have those different clouds coexist and interoperate. Multi-cloud interoperability is an important step in the evolution of cloud computing.

He made this comment following the news Oracle is expanding its software offering through the Amazon AWS platform. In fact, Oracle pays Amazon to have its databases available on the platform in order to offer its databases to as many clients as possible and give customers the flexibility to use multi-cloud solutions. He continued with the following:

Multi-cloud interoperability is one of the reasons our infrastructure business is booming, growing over 50% in U.S. dollars and almost 60% in constant dollars. We expect Oracle’s total cloud business to exceed a $20 billion annual run rate next year.

Ellison believes that protecting and preserving its database and enterprise software leadership is the most important factor in the long term and Oracle is willing to leverage the multi-cloud opportunity to achieve this. The next quote confirms this thought:

I know a lot of people for years have been concerned about whether Oracle can sustain its leading market share in the database business. And I think what is now clear is if our databases are available in multiple clouds, then the answer is clearly yes. If our database is not available in multiple clouds, then it’s an interesting question whether we can maintain our lead just on our own cloud.

So, we decided to make our best and greatest technology available in multiple clouds, and that gives customers choice. They can use it in OCI, they can use MySQL HeatWave at AWS.

These are interesting thoughts by Ellison, and I think he is on the right path here. If Oracle were to focus on a lock-in strategy and only build on its own cloud, it could lose its database and software enterprise leadership rather quickly, and with that also its cloud opportunity. The multi-cloud approach should position Oracle well to 1) keep its market share in its legacy business and 2) keep growing the cloud revenues through its existing moat. Ellison’s focus on the long-term is impressive and, in the end, Oracle cloud is optimized for Oracle workloads which could eventually drag customers back to the full Oracle cloud offering.

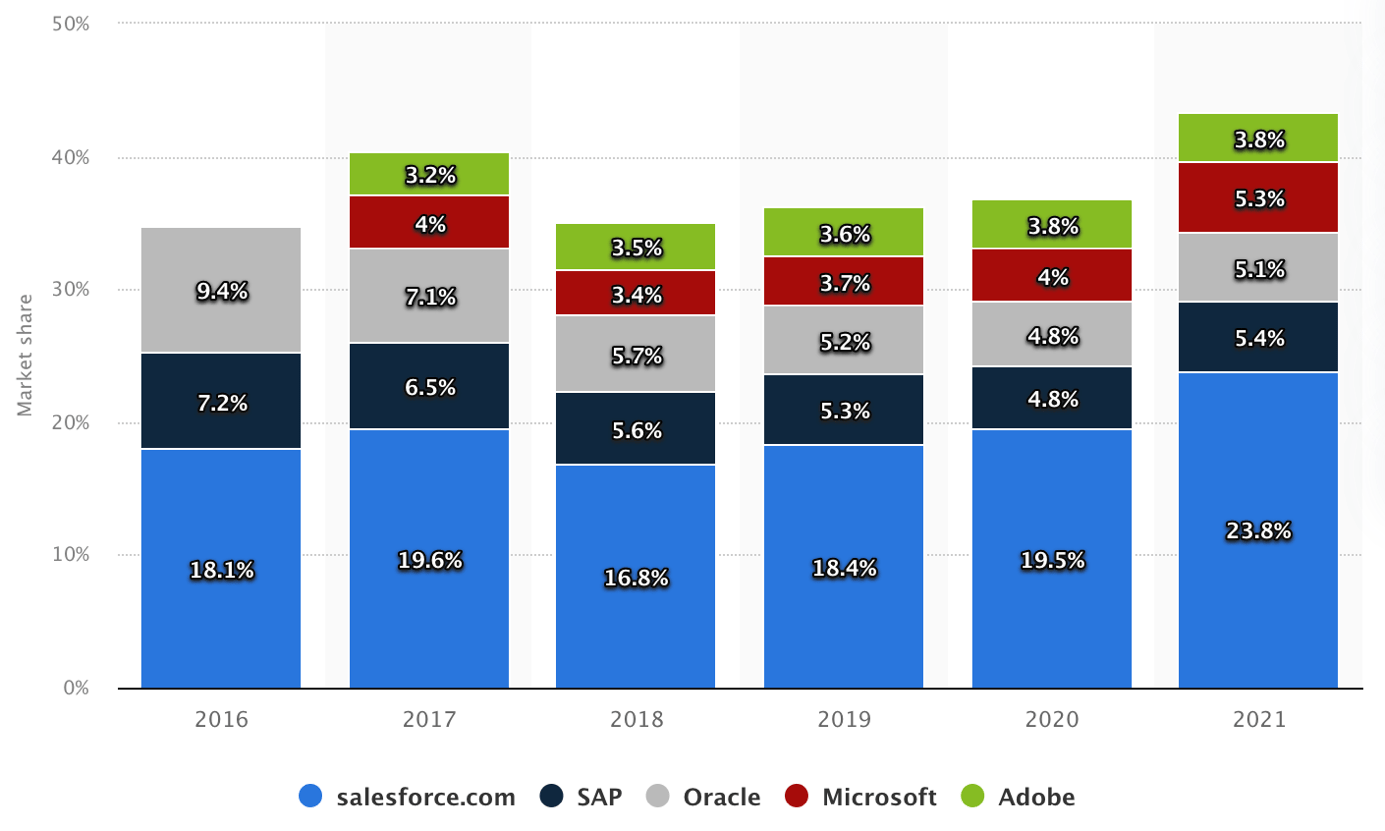

The focus on maintaining its legacy business within CRM and ERP makes a lot of sense as these products give Oracle its moat while being highly competitive as well. Oracle currently has a significant cloud ERP market share of close to 6%, much higher than the almost 3% for SAP ( SAP ). In CRM software solutions Oracle has to deal with industry giant Salesforce ( CRM ) that holds by far the largest part of this market as shown below. Still, the 5.1% market share from Oracle still positions them well to benefit from industry growth and since customer loyalty is generally quite strong in both these industries, in part due to high switching costs, these revenue streams are very reliable as well. That is why these products are crucial for Oracle and these generate significant cash flows that allow it to invest more into its cloud ecosystem. According to Grand View Research, the CRM market is expected to grow at a 13.9% CAGR until 2030, with the ERP market projected to grow at an 11% CAGR until 2030. This shows that both product segments should result in slid growth for Oracle as well, making these segments very crucial.

{kind=link}

Besides strong customer acquisition and a solid consumer-centric offering by Oracle, its cloud solutions are also technically of the highest quality. An important part of this is security. From day one, security has been a primary focus for Oracle in its cloud offering, with features such as virtual machine isolation and advanced threat detection. Oracle has also been awarded various security certifications and compliance standards. We should of course assume all cloud giants to see the highest security standards in their offering, but Oracle looks like it excels here, which could make it more attractive to highly regulated industries in particular.

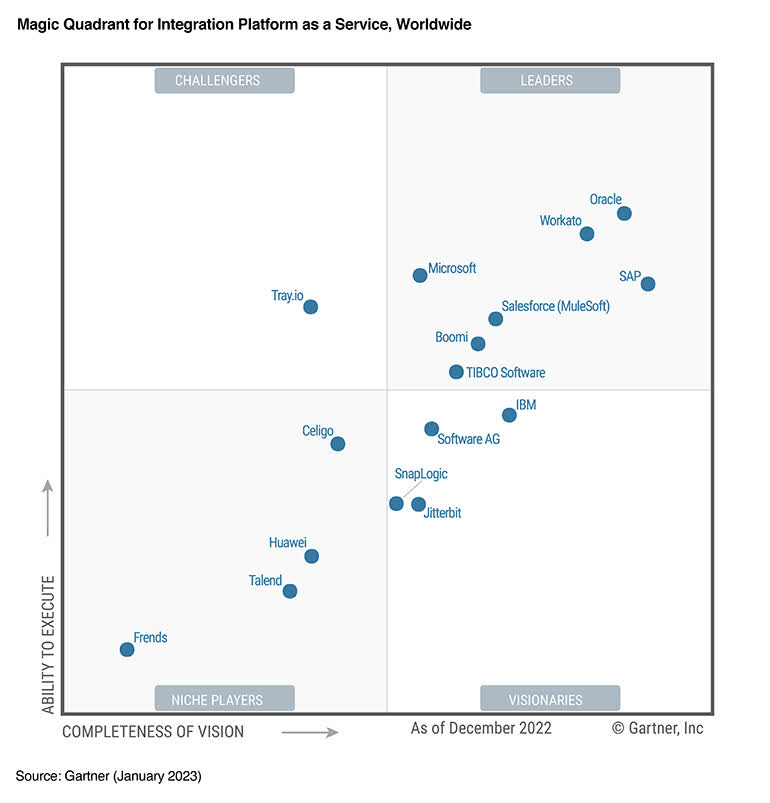

As a result of a very solid and secure platform, Oracle is being named a leader across several different products and services by Gartner’s magic quadrant. The image below shows Oracle being the leader in the integration of PaaS. But this is not all as Gartner’s magic quadrant also identifies Oracle as the leader in both cloud HCM suites and cloud ERP .

{kind=link}

All in all, the cloud offering by Oracle is very impressive and everything discussed above makes me believe that Oracle might be positioned for growth that is at least as strong, if not better than the current cloud leaders. Oracle might have been late to the party but is well positioned today to see solid growth through an excellent approach. AI might be the latest cloud adoption driver and Oracle has already acknowledged this as well as it is looking for AI and ML integrations into its software suite and cloud offering. This could position it well to ride the cloud and AI wave which is poised to continue for at least the rest of the decade.

And while, in all honesty, the growth story for Oracle is largely built around the cloud opportunity, there is more that might convince you to buy the shares. One such example is the acquisition of Cerner. While Oracle has acquired its fair share of companies over its lifetime, many have not turned out great as none of the acquisitions over the last 5 years have contributed to much growth. Though, I believe Cerner might be different.

Cerner is a global healthcare information technology company that specializes in developing and providing software solutions for healthcare providers. The company's products and services are designed to help healthcare organizations improve the quality of patient care, reduce costs, and increase efficiency. Cerner is one of the largest healthcare IT companies in the world, with more than 29,000 employees and a presence in over 35 countries. The company's clients include some of the largest healthcare providers in the United States, as well as numerous international clients.

Oracle paid $27 billion to acquire Cerner and get exposure to the massive healthcare sector. In the wake of covid, there is a worldwide shift going on into new digital and software solutions for healthcare providers ranging from digital forms to digital consultancy. The acquisition by Oracle, therefore, makes a lot of sense as it gets Oracle some great exposure to the healthcare industry, valued at $3.8 trillion in the US alone. In addition to this, Oracle plans to expand the Cerner business to international markets as well in order to grow its addressable market.

Oracle already has a strong cloud presence worldwide and expanding this into the highly lucrative healthcare market offers it plenty of cross-sell opportunities to existing Cerner customers. Ellison stated the following during the latest earnings call :

Our goals are ambitious: fully automate clinical trials to shorten the time it takes to deliver lifesaving new drugs to patients, enable doctors to easily access better information leading to better patient outcomes, and provide public health professionals with an early warning system that locates and identifies new pathogens in time to prevent the next pandemic. The scale of this opportunity is unprecedented—and so is the responsibility that goes along with it.

Cerner should see solid growth from its current offering as well as the global connected healthcare market is expected to grow at a CAGR of 27% until 2030 and should reach a market size of over $540 billion. Cerner is one of the leaders in this industry and is therefore extremely well positioned to see solid growth in addition to the synergy and cross-sell opportunities that appear for Oracle. This acquisition could turn out to contribute to solid growth for Oracle. During the latest quarter, Cerner added $1.5 billion in revenue to the top line of Oracle, boosting growth.

Latest financial results

Now that we have established the possible growth drivers and moat of Oracle, it is time to put these into perspective and take a look at the financials and at how the company performed over the latest quarter which it reported back in December.

Oracle reported its fiscal 2Q23 on December 12 and managed to beat both top and bottom-line estimates , as well as its own outlook. Total revenue for the quarter came in at $12.28 billion and was $200 million above the high-end of guidance by management and $260 million above the analyst consensus. This means Oracle managed to grow its top line by 25% in constant currency and 18% in USD, yet this does include the revenue boost coming from the Cerner acquisition that was not completed last year. Excluding the $1.5 billion generated by Cerner and we get a more realistic 9% growth rate which is still a very decent performance considering the tough economic times we are experiencing.

And this is in large part due to the cloud business that is performing excellently. Total cloud services and license support revenue, including Cerner, increased by 20% to $8.6 billion. Taking into consideration the volatile Dollar and growth was still 14% YoY which I believe is impressive. If we split this down further into product segments, we can see that total cloud revenue was up 43% and saw revenue come in at $3.8 billion. License support brought in an additional $4.8 billion.

Now, within cloud revenue, we can zoom in even further and can see that this exists of IaaS revenues and SaaS revenues. IaaS, or cloud infrastructure, saw revenue come in at $1.1 billion, increasing 53% YoY. Management commented the following on growth for this segment, pointing out the impressive growth of its cloud services:

Now excluding legacy hosting services, infrastructure cloud services revenue grew 69% with an annualized revenue of $3.8 billion, including OCI consumption revenue, which was up 88% and cloud and customer consumption revenue, up 83% and autonomous database up 50%.

During 2Q23, Oracle reported multiple contract wins with a value of over $1 billion, but these are simply added to the backlog or RPO. Several large customer deals were with FedEx ( FDX ), Deutsche Bank ( DB ), and the Tokyo Stock Exchange. This brings me to the following fascinating quote from the earnings call:

In fact, my favorite quote from a big phone company in the United States was the difference between Oracle’s Cloud and the other clouds are simply that Oracle Cloud doesn’t go down. I think that’s a very important issue when you have enterprise applications like a stock exchange where you can’t ever go down.

According to Oracle, companies with critical systems tend to choose Oracle cloud due to its reliability. These also include Vodafone ( VOD ), Deutsche Telekom ( DTEGY ), and Enbridge ( ENB ). Nvidia ( NVDA ) has also moved a bunch of its AI and machine learnings workloads to Oracle cloud and management states that is because of the following:

So we’re seeing a lot of machine learning and artificial intelligence workloads moving from other clouds to OCI because we’re faster. And again, in the cloud business faster -- when you charge by the minute, faster means cheaper.

Management announced a whole bunch of other large deals made over the last couple of months, illustrating the fast growth of the business. Oracle now has over 22,000 infrastructure customers across 55 regions and expects to keep growing its cloud infrastructure business at a very strong pace.

SaaS, or cloud application, saw revenue come in at $2.8 billion ($4.1 billion including license support) and increased by 40% YoY. This includes the Fusion ERP revenue of $0.6 billion and NetSuite cloud ERP revenue of $0.6 billion, up 23% and 25% YoY, respectively. I have not discussed NetSuite ERP products so far in this article, but these offer similar functionalities as the previously discussed Oracle Fusion products, but in a more basic way and aimed at small to medium businesses. Oracle has close to 30,000 NetSuite customers and 11,000 Oracle Fusion customers.

Moving on to the other business segments and we can see that software license revenues, including Cerner, were $1.4 billion, up 16% YoY. Revenue from hardware sales came in at $850 million which was an increase of 11% YoY. Finally, services revenue was $1.4 billion, up 74% YoY, bringing the total to $12.3 billion.

Moving to the bottom-line results and we can see that Oracle reported $5.1 billion in non-GAAP operating income, up 12% from a year ago. The gross margin for cloud services and license support dropped from the mid-90s one year ago, to 79% today as a result of much faster growth in the cloud segment, while license support has much higher margins. Of course, 79% is still incredibly strong, and even if these would drop to the 40% to 50% range over time, this would still result in very impressive operating income. Last quarter the overall operating margin stood at 41%.

Some tough tax effects caused a somewhat weaker net income of $3.3 billion, resulting in EPS of $1.21 which is down 1% from a year ago, yet up 7% in constant currency. Since the drop in EPS is not due to operating flaws, we should not focus on this overly much. EPS did still beat the consensus estimate by $0.04.

During the quarter, Oracle continued to see incredibly high demand for its cloud services. Even more, they are seeing an acceleration in demand, and this is reflected in the remaining performance obligation or RPO balance. At the end of the latest quarter, Oracle had an RPO of a whopping $61.2 billion, giving it a massive runway of growth ahead. RPO was up 68% in constant currency due to triple-digit cloud bookings and a strong contribution from Cerner. Even when we exclude RPO growth coming from the Cerner acquisition, this still shows an acceleration from last quarter with RPO growth of 28% compared to 22% last quarter. Oracle expects to turn 48% of its current RPO into revenue over the next 12 months.

To satisfy the high demand, Oracle realizes that it needs to continue investing heavily in its cloud ecosystem and hardware. Oracle now operated 40 public cloud regions around the world with another 9 underway. To realize all of these high investments, Oracle reported $2.4 billion in Capex during the last quarter and expects to see similar amounts invested over the next couple of quarters to keep up with demand.

Balance sheet & Dividend

At the end of the latest quarter, Oracle held $7.4 billion in total cash on the balance sheet which is solid enough. The larger problem here is the debt load of the company which now stands at close to $91 billion. This is the result of large share buyback programs to make the stock more attractive to shareholders during years of flat growth and the many acquisitions by the company that has not resulted in the necessary cash flows to pay down the debt pile. As a result of the large amount of debt, Oracle has seen credit rating downgrades from both S&P Global and Fitch which downgraded the company from a BBB+ rating to BBB. For me, the current balance sheet is a big problem for a tech company that needs to invest large amounts of cash to build out its cloud network, and as a result, I don’t expect Oracle to be able to decrease the net debt position it currently holds in the near term. Yet, the company is capable of generating solid cash flows and profitability is absolutely no issue. Over the last 12 months, Oracle generated $8.4 billion in free cash flow, combined with $6.7 billion in Capex.

And despite the tricky balance sheet, Oracle keeps returning large amounts of cash to shareholders. During 2Q23, the company returned $448 million through share repurchases and $863 million through dividends. Oracle currently has a dividend yield of 1.46% and a payout ratio of just 26%. The company has been growing the dividend for 8 straight years now and has been increasing it at an 11% CAGR over the last 5 years. I believe Oracle could see very decent dividend growth on top of a safe and sustainable yield today, making it a nice dividend growth opportunity.

Overall, I would prefer Oracle to stop the buybacks and focus on strengthening its balance sheet and increasing its dividend, but this is a very personal preference.

Outlook & Valuation

So now, let’s turn to guidance for the next quarter for which Oracle will release results on March 16. Revenue is expected to grow 17% to 19% YoY in USD which should translate to revenue of between $12.29 and $12.51 billion. This will be driven by cloud growth of between 43% to 47% in USD. These top-line growth expectations should translate into EPS growth of between 4% to 8% and come in between $1.17 and $1.21 in USD. Overall, the outlook from management looks very decent and shows strong growth rates to continue from last quarter.

The current analyst estimates show expectations in line with management’s guidance as these project revenue of $12.42 billion and EPS of $1.20. I believe these estimates are fair, although an outperformance by Oracle also seems highly likely. For fiscal FY23, ending in May, analysts expect revenue of $49.87 billion, up 17.52%, and EPS of $4.91 which is flat YoY.

For the following years, analysts expect Oracle to grow EPS at mid-double digits until 2026, combined with revenue growth of high single digits as shown below.

EPS estimates (Seeking Alpha) Revenue estimates (Seeking Alpha)

{kind=link}

{kind=link}

I believe we could see growth come in slightly higher than currently projected by analysts and see EPS growth of between 15% to 18% and revenue growth of around 10%. This is based on the growth drivers and industry trends mentioned throughout this article.

Now, what does this mean for the valuation? Oracle is currently valued at an FY23 P/E ratio of close to 18x which is 17% above its 5-year average valuation of 15.35x. Yet, this was during a time with a much dimmer outlook and close to no growth. As a result, I believe that an 18x to 20x P/E would be fair for Oracle based on its growth expectations. Based on the current FY24 EPS consensus of $5.58, this would result in a target price of between $100 and $112 per share and leaves investors with an upside potential of between 14% and 28%, or 21% at the midpoint.

Conclusion

Oracle has seen a tough decade with flat growth and many failed acquisitions that have resulted in a debt pile of over $90 billion. Yet, despite this, the next decade should look much better due to a very solid cloud infrastructure and applications offering that can fight the cloud leaders and increase its market share.

I expect Oracle to see very solid growth over the next 4 years, driven by a strong product offering, large existing customer base and moat, and focus on growing its cloud infrastructure offering.

Based on the current EPS estimates for its fiscal FY24, I calculate a target price of $106 at the midpoint and this leaves investors with a 21% upside potential from its current share price of $87.58. Therefore, I rate Oracle a buy at prices below $95 as this leaves investors with plenty of downside protection to make an investment in this underappreciated cloud giant a relatively safe one.

For further details see:

Oracle: An Underappreciated Cloud Giant Worth Buying