CA - Organigram Is The Best Cannabis Stock

2023-05-15 17:58:24 ET

Summary

- I have followed Organigram closely since it went public in 2014.

- I find the valuation currently to be extremely cheap, and OGI is the largest position in my model portfolio.

- The company is rich in cash and free of debt, and its business is doing alright.

It seems like I'm the only analyst of the cannabis sector that likes Canadian LPs. I have written positively this year about Cronos Group ( CRON ) and Village Farms ( VFF ), both of which have declined since I wrote bullishly. I don't like all Canadian LPs! I have written very negatively about Canopy Growth ( CGC ), for which I later reduced my outlook as I shared a year-end 2023 target of C$0.59, which is currently equivalent to US$0.435, more than 50% lower.

I shared publicly my suggestion that owners of Canopy Growth sell it and replace it with either Cronos Group, Organigram ( OGI ), or Village Farms. Since then, Canopy Growth has plunged, but so have my replacement ideas, especially Organigram.

YCharts

Today, I want to explain why I like OGI so much. It's my favorite cannabis stock.

FY2023-H1

Organigram just reported its fiscal Q2, with sales falling a bit shy of expectations but adjusted EBITDA slightly ahead of them. Revenue of C$39.5 million grew 24% from a year ago but was down 9% from its Q1. Adjusted gross margin improved from 26% to 34%. Adjusted EBITDA of C$5.6 million increased 263% from a year ago. The key issue during the quarter was the extreme price decline of large formats of flower. I think Organigram is right to step aside, a move that caused revenue to be hit but helped its margins.

For the first half of the fiscal year, revenue has increased 33.1% to C$82.8 million. The gross margin before changes in the fair value of biological assets has improved from 15.0% to 26.0%. Adjusted EBITDA has been C$11.2 million, up from a slight loss a year earlier. A negative has been the cash flow from operations, which, at -C$16.2 million, has declined from a year ago.

One of the things that stands out for the company is its balance sheet, which used to be very pressured before the British American Tobacco ( BTI ) investment in early 2021. As of 2/28, the company reported almost no debt (C$198K) and cash and investments of C$72 million.

In terms of its operations, the company continues to successfully integrate the acquisition of Tremblant in Quebec and grow its international business. The bulk of revenue is from adult-use sales in Canada, which have been C$63.2 million year-to-date, which is 76% of reported revenue and up 27.4% from a year earlier. Its international business has more than doubled to C$16.6 million, 20% of sales. Canadian medical cannabis has declined by almost 50% to C$2.3 million, which is just 3% of sales. Wholesale, at less than 1%, remains a very small amount of the business.

Outlook

The company shared an outlook that falls short of very specific guidance. It projected that revenue will increase in FY23, that its adjusted gross margins will exceed 30% for the year, that it will have positive adjusted EBITDA and that capital spending will be approximately C$32 million. Finally, it expects positive free cash flow (operating cash flow less capital expenditures) by the end of 2023 (so during FY24).

For FY23, analysts project revenue will grow 18% to C$172 million. Adjusted EBITDA is expected to increase to $23 million. For FY24, the company is expected to grow revenue 16% to C$200 million. Analysts project adjusted EBITDA will grow 26% to C$28 million. I'm assuming an 18% margin, which works out now to be C$36 million.

For FY25, 2 analysts project revenue will grow 35% to C$269 million with adjusted EBITDA of C$57 million. I'm currently using the same margin of 21% but also a slightly lower revenue of C$240 million (+20%), which is C$51 million.

Valuation

Despite its growth and improving profitability and the elimination of debt and securing of cash, Organigram trades at a big discount to its tangible book value. At just 0.44X, it's very low. The stock more than doubled to get to its tangible book value, a valuation that would still be too low, in my view.

I think this is a very conservative target price, but I'm using 2.5X calendar 2024 projected revenue (C$213 million) for the end-of-year target, which works out to be an enterprise value of C$533 million. This implies a stock price of C$1.84, which is up 202% from the closing price of C$0.61 on 5/12. It also works out to be 13.X projected adjusted EBITDA for CY24 of about C$41 million. I think cannabis investors looking at MSOs, which trade a bit cheaper than this, need to remember that Organigram operates legally on a federal basis. My target in USD is $1.36 currently.

Chart

OGI has plunged 41.2% so far in 2023 to what is the lowest price since 2016. The New Cannabis Ventures Global Cannabis Stock Index has declined 19.2%. Over the last year, Organigram has declined 59.1%, while the index has dropped 57.2%.

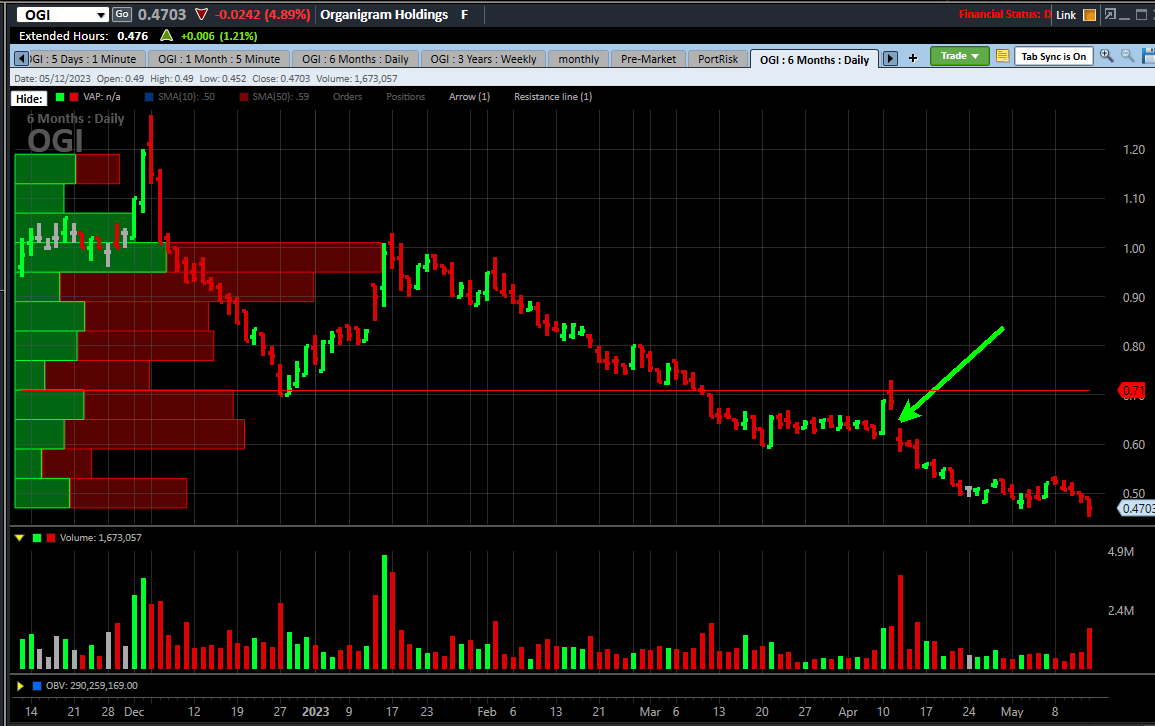

The chart over the past six months shows how precipitous the drop has been:

{kind=link}

When the company reported its fiscal Q2 in April, it gapped down. While I expect that gap to get filled, I do see technical resistance at $0.70, which was the low in December. Positively, a rule that I use regarding over-extension suggests a rally soon. In my experience, it's rare for a stock's 10-day moving average below the 50-day which is below the 150-day for 13 weeks or longer, and we are just past 13 weeks.

Conclusion

I like Organigram a lot for the reasons I have shared. It's now about 20% of my Beat the Global Cannabis Stock Index model portfolio, its largest position but very underwater. I believe that the weakness in the cannabis sector overall, the extreme weakness in Canopy Growth and slowing growth in the Canadian cannabis market are all factors impacting the stock. I think that British American Tobacco ( BTI ) ( BTAFF ), which is way down on its purchase from two years ago, could easily buy the company, but I have no idea if it will. It should!

For Organigram stock to do well, folks have to likely start buying cannabis stocks first. Buyers of cannabis stocks doing any sort of analysis on the sector will be hard-pressed to come up with a better idea.

One challenge for the company is that it faces potential delisting from the Nasdaq due to its low stock price. I expect the company to do a reverse-split to address this issue.

For further details see:

Organigram Is The Best Cannabis Stock