CA - Orla Mining: A Beat And Raise For This Junior Producer

2023-10-17 05:50:17 ET

Summary

- Orla Mining reported record gold production in Q3, driven by strong grades and throughput rates.

- The company was one of the few producers to date to increase its annual guidance, continuing a flawless track record of over-delivering on promises.

- In this update, we'll dig into the Q3 results, recent developments, and whether ORLA stock has entered a low-risk buy zone after its recent correction.

The Q3 Earnings Season for the Gold Miners Index ( GDX ) is just around the corner and one of the first companies to report its Q3 production results is Orla Mining ( ORLA ). True to form, the company has reported another exceptional quarter with record gold production, and Camino Rojo continues to be an asset that keeps on giving, with the company practically stealing the asset from Goldcorp in 2017, paying just ~$35 million (~31.9 million shares) plus a 2.0% NSR on the oxides. This is evidenced by the oxide portion of the asset alone having generated upwards of $130 million in operating cash flow since Q1 2022, with eight years of mine life still left (and significant long-term upside with the sulphide opportunity at depth). Just as impressively, the company waited for fire-sale prices in the market to parlay this initial transaction into a second transaction, adding a similar project (open-pit, heap leach with sulphide optionality) in a superior jurisdiction, Nevada.

And while Camino Rojo may not boast the same size of assets added in the period by other producers, this is one of the better deals among its peer group, with many deals lacking discipline (over-paying), and many buying projects that didn't turn out as planned, with some disappointments including Relief Canyon, Revenue-Virginius, and Tucano to name a few. While these companies bought counter-cyclically like Orla, the difference was that Orla paid the right price for an asset with low technical risk, with the difference being massive outperformance vs. its peers and the ability to build a larger portfolio with strong currency and cash flow from this asset. In this update, we'll dig into the Q3 results and see whether the stock is becoming more attractively valued following its recent pullback.

All figures are in United States Dollars unless otherwise.

Q3 Production & Sales

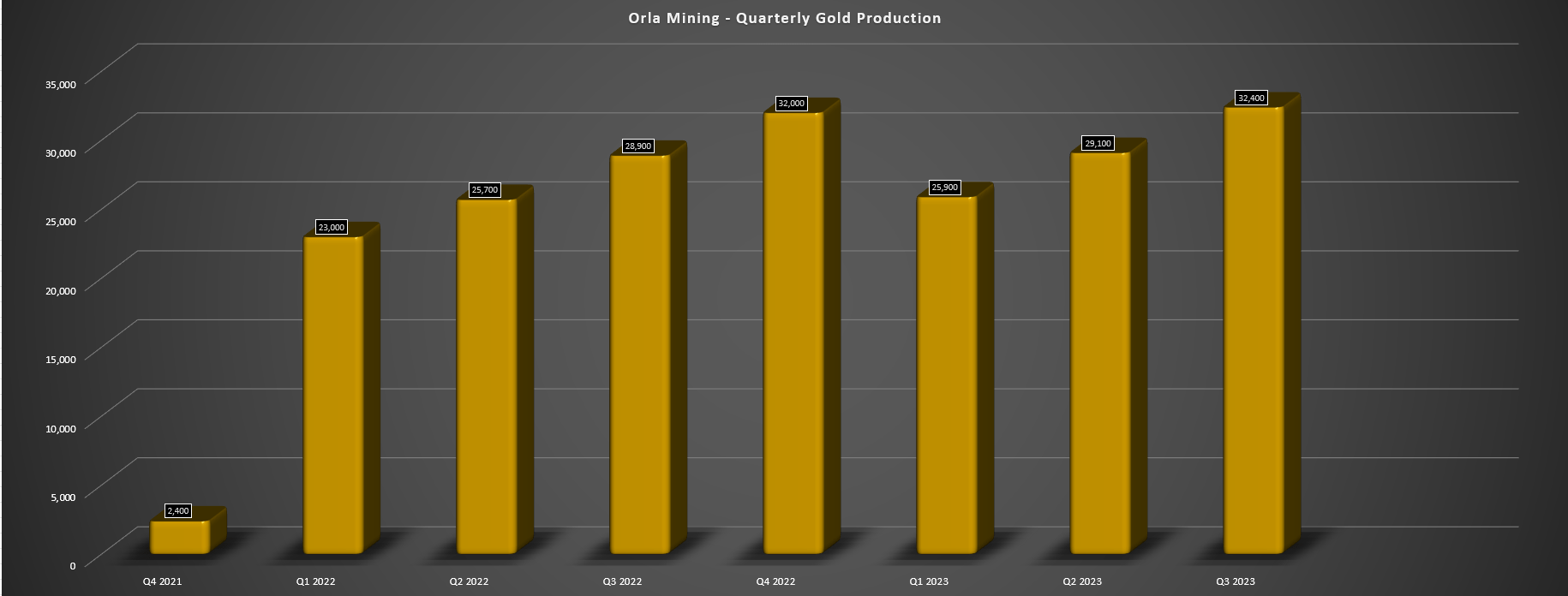

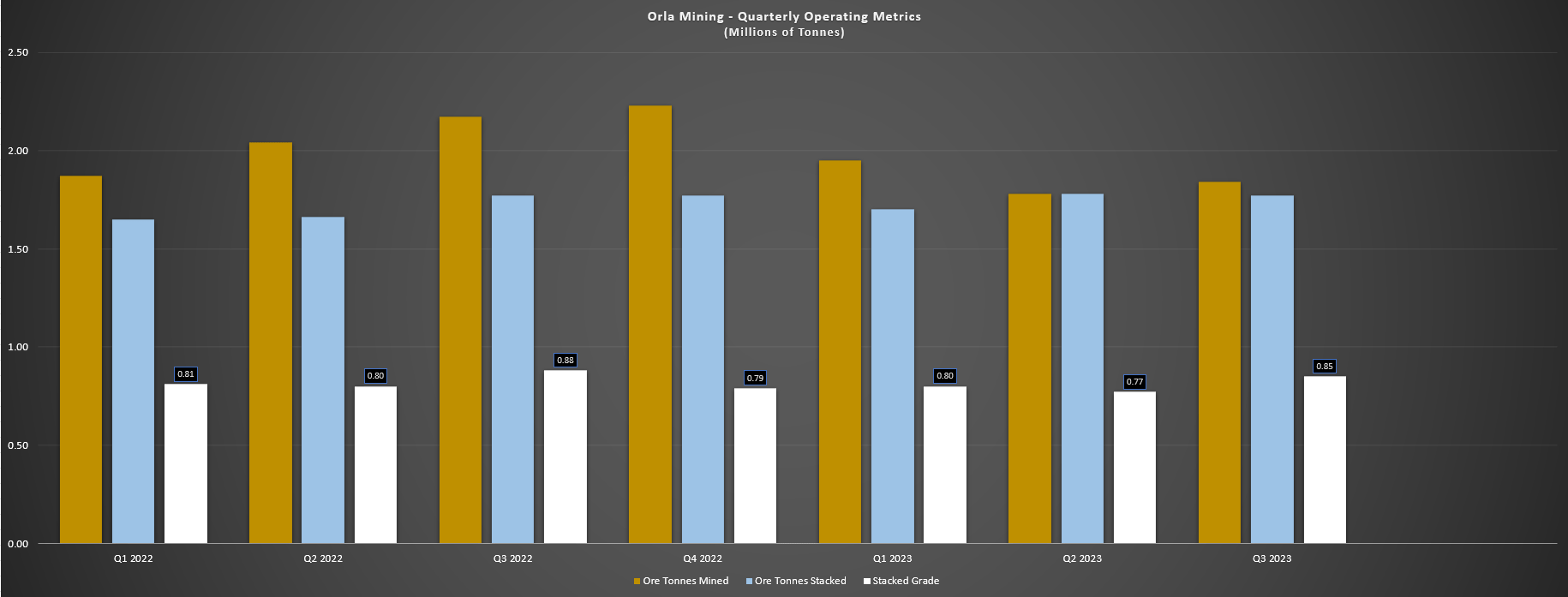

Orla Mining released its preliminary Q3 results this week, reporting quarterly output of ~32,400 ounces of gold, a record for the company that slightly edged out its previous record of 32,000 ounces in Q4 2022. This was driven by one of the best quarters for stacked grades to date at 0.85 grams per tonne of gold while daily average throughput rates continued to outperform nameplate capacity at ~19,200 tonnes per day. Meanwhile, the company mined ~2.93 million tonnes at an ultra-low strip ratio of 0.59, well below the life of mine strip of 0.92. And given the exceptional Q3 report that left Orla tracking at ~83% of its initial annual guidance mid-point, this has prompted Orla to increase its guidance by ~10% at the mid-point to 115,000 ounces, implying a solid finish to the year assuming it delivers at or above the mid-point.

Orla Mining Quarterly Gold Production - Company Filings, Author's Chart Orla Mining Key Operating Metrics - Company Filings, Author's Chart

{kind=link}

{kind=link}

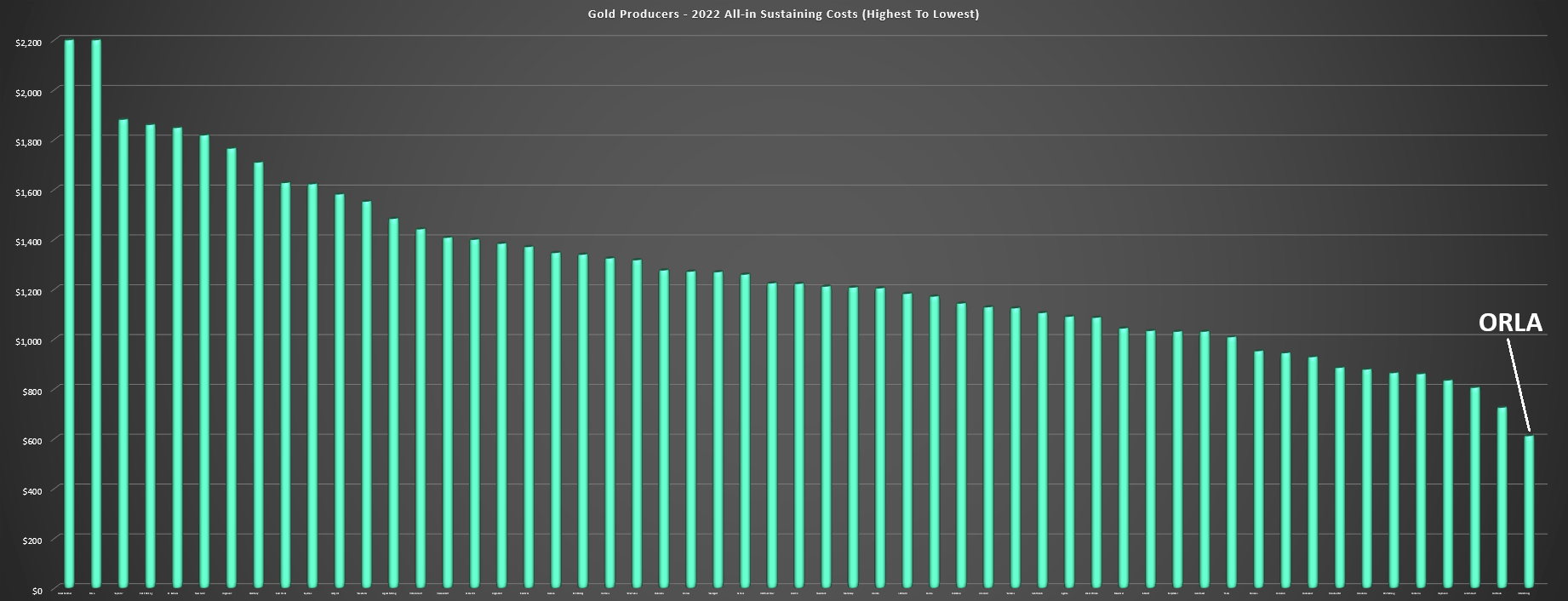

From a sales standpoint, Orla sold ~31,100 ounces in the period, suggesting that it should report revenue of $58.0+ million in the period, which would come in just shy of its previous record of $59.3 million depending on the timing of its sales. And despite the likely dip in margins sequentially (Q3 vs. Q2) given the pullback in the gold price, Orla should still maintain its industry-leading AISC margins of $1,200/oz plus, giving it 60% plus AISC margins and help the stock to maintain its premium multiple relative to its peer group. Finally, from a full-year standpoint, the exceptional production performance suggests that Orla should be able to deliver at the low end of its cost guidance range, with the potential to report FY2023 AISC of ~$700/oz (updated guidance: $700-$800/oz), making it the lowest-cost gold producer sector-wide for a second consecutive year.

Gold Producers - Highest to Lowest AISC 2022 - Company Filings, Author's Chart

{kind=link}

Recent Developments

Digging into recent developments, Orla Mining upgraded its $100 million term facility (April 2027 maturity) and $50 million RCF (April 2025 maturity) into a $150 million RCF with room to increase this to $200 million subject to certain conditions. Not only has this extended maturity to August 2027, but it reduced the borrowing cost by 25 basis points and also reduced the standby fee for the undrawn portion of the facility to 250 basis points to 22.5% vs. 25.0% previously. As it stands, Orla has $88 million undrawn on its RCF, which gives it a total liquidity position of ~$170 million. This strong balance sheet, combined with consistent free cash flow generation can easily support upfront capex of ~$220 million (inflation-adjusted) at Railroad South, but could also allow for opportunistic M&A to potentially give the company a 600,000+ gold-equivalent ounce per annum production profile long-term (Railroad, Camino Rojo Oxides, Camino Rojo Sulphides, and a new project) if the right opportunity arises at an attractive price.

Normally, I might be concerned about the potential for M&A, but as Orla proved with its last deal, the company is focused on quality projects and proverbial low-hanging fruit and not projects with high technical risk, significant capex requirements, and or those that are up to a decade away from cash flow. So, given the company's disciplined capital allocation to date, I don't think there's any reason for investors to worry about potential M&A in the next 12-18 months given that like some of the other well-run producers in the sector like Alamos Gold ( AGI ), the company has done a great job of acquiring counter-cyclically and paying a fraction of NAV, suggesting that any deal the team does will benefit shareholders and be accretive.

Finally, on negative developments, the higher oil price isn't helping given that Orla is a high-volume and lower-grade operation, but the company certainly benefits from a much lower strip than other heap-leach projects, meaning it's moving considerably fewer tonnes per ounce produced than something like a Marigold or Paracatu. That said, there is also the risk of wage rates creeping up in Zacatecas and Mexico overall given that Newmont ( NEM ) just caved into an 8% raise to turn its Penasquito Mine back online in the state of Zacatecas. So, while there may be risk to the upside on labor rates at Mexican mines and higher fuel prices could put some pressure on Orla's margins, Camino Rojo is hardly a sensitive asset given its industry-leading cost profile, so I don't see the weaker gold price and higher oil price as all that material vs. a high-cost mine like a Round Mountain, which is producing at much higher costs in Nevada.

Valuation

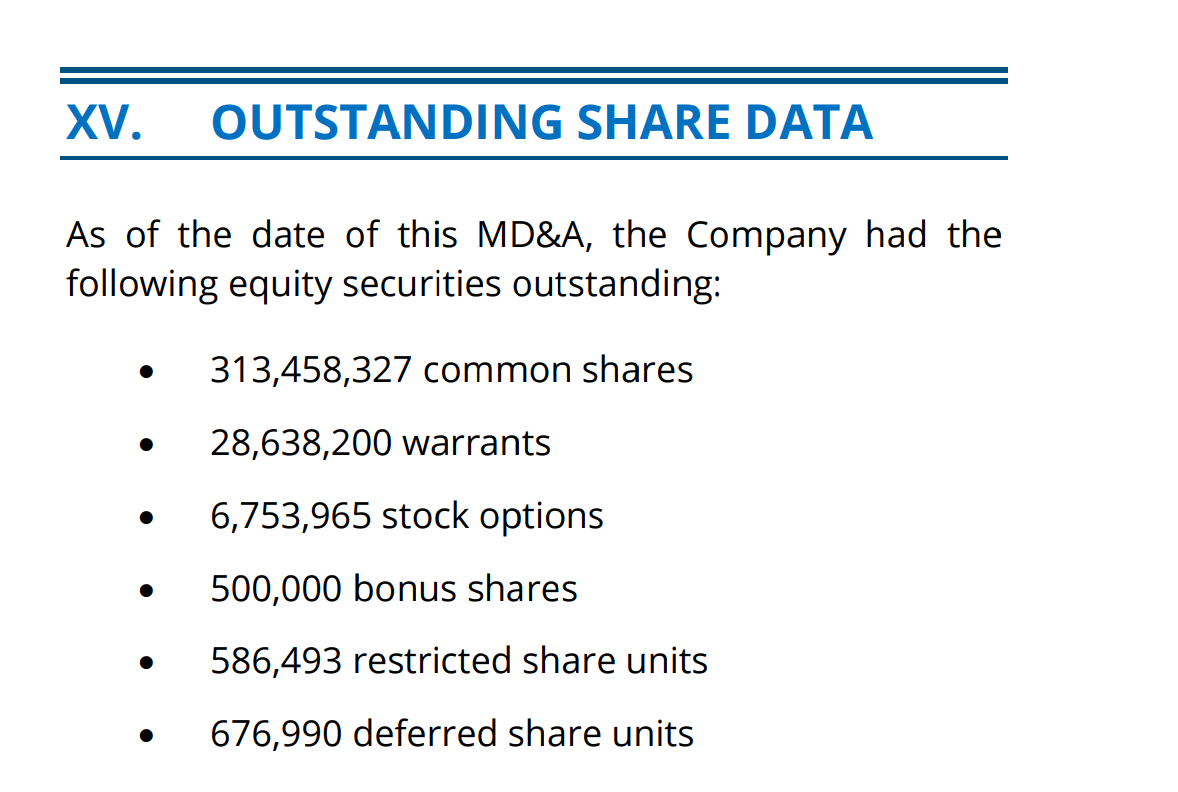

Based on ~351 million fully diluted shares and a share price of US$3.40, Orla trades at a market cap of ~$1.19 billion, a much more reasonable valuation following its recent correction. If we compare this to an estimated net asset value for the stock of ~$2.20 billion, Orla is back to trading at a steep discount, sitting at 0.55x P/NAV vs. closer to ~0.77x at its recent highs. That said, the company has the bulk of its NAV tied to Tier-2/Tier-3 ranked jurisdictions three out of four of its projects/mines in Mexico and Panama, which I believe justifies a lower P/NAV multiple of 0.90x vs. Tier-1 or primarily jurisdiction producers like Wesdome Mines ( WDOFF ), Alamos Gold ( AGI ) and others. And if we assign a 65%/35% weighting to P/NAV and P/CF (FY2024 estimates) with a fair multiple of 0.90x and 8.0x, respectively, I see a fair value for the stock of US$4.70.

Orla Mining - Fully Diluted Shares - Company Filings

{kind=link}

Although this points to a 37% upside to fair value, I am looking for a minimum 40% discount to fair value to justify starting new positions in small-cap names, and ideally closer to 50% for single-asset producers in Tier-2/Tier-3 ranked jurisdictions. So, although Orla has upside and it's certainly possible that this relief rally continues, the ideal buy zone for the stock comes in at US$2.85 or lower, suggesting that the stock would need to make new correction lows to head into a low-risk buy zone. Obviously, there's no guarantee that this will happen, and the strong Q3 report may help to put a floor under the stock near US$3.00. However, I prefer to buy with a deep discount to fair value or pass entirely, and with names elsewhere in the sector trading at steeper discounts to NAV and higher free cash flow yields, I continue to focus elsewhere for the time being.

Summary

Orla Mining put together another blowout quarter in Q3 and it is one of the few producers to raise its annual guidance, continuing its track of over-delivering on promises. Meanwhile, the stock has slid considerably from its highs following my previous update, leaving it back in value territory with it trading at less than 0.60x P/NAV. That said, even though the stock has played some catch-up to the downside with its peer group, there are other names that are still trading at more attractive multiples from a relative value standpoint. Plus, the stock has now moved into a new intermediate downtrend, suggesting that any sharp rallies have a higher probability of being sold. Hence, although I continue to see Orla as one of the better-run producers sector-wide, I would view any rallies above US$3.95 before February as profit-taking opportunities.

For further details see:

Orla Mining: A Beat And Raise For This Junior Producer