CA - Orla Mining: Another Blowout Quarter In Q1

2023-06-08 00:49:26 ET

Summary

- Orla Mining released its Q1 results last month, reporting quarterly production of ~25,900 ounces, an improvement from the year-ago period when it was ramping up to commercial production.

- The company also reported what look to be the highest margins sector-wide despite headwinds from a strengthening Peso, and the company could beat its cost guidance midpoint again in 2023.

- That said, even with solid exploration results and continued delivery on its promises, I don't see enough margin of safety in the stock yet at US$4.55.

The Q1 Earnings Season for the Gold Miners Index ( GDX ) was mixed at best, with limited free cash flow generation, rising costs for most producers a year-over-year basis, and flat to lower revenue on balance. This was related to inflationary pressures that have persisted even if the rate of change has slowed. Fortunately, investors in Orla Mining ( ORLA ) were surprised with another major beat, with production tracking in line with guidance and costs below the low end of the range, an exceptional performance given the strength in the MXN/USD exchange rate called out by many of Orla's peers operating in Mexico. Let's take a closer look at the results below and whether the stock is worth buying ahead of its Q2 results:

Camino Rojo Operations (Company Website)

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q1 Production & Sales

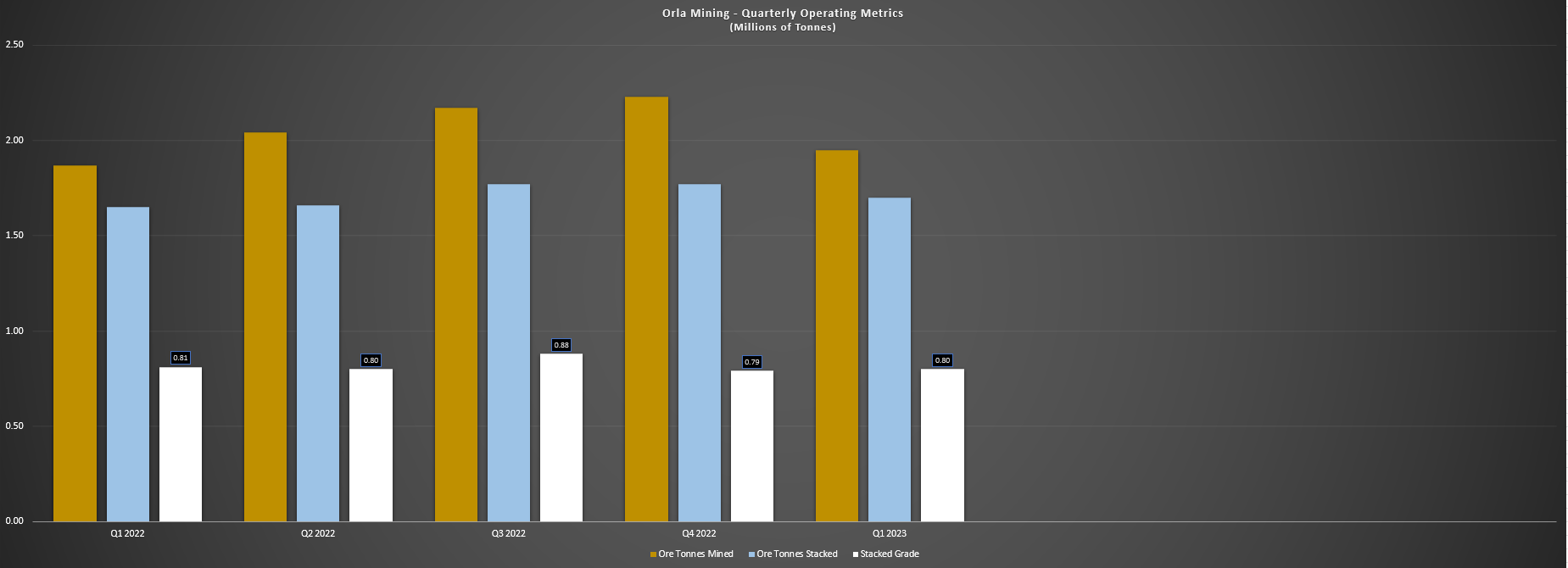

Orla Mining released its Q1 results last month, reporting quarterly production of ~25,900 ounces of gold, a 13% increase from the year-ago period, with production slightly lower in Q1 2022 as commercial production was not declared until April 1st, 2022. This has placed the company well on track to meet its guidance midpoint of 105,000 ounces this year (24.6% of total), and while this is a relatively small production profile, Orla makes up for its current scale with outsized margins. In fact, Orla reported the lowest all-in sustaining costs sector-wide among producers I track at $693/oz, and this was despite the Mexican Peso diving 10% vs. the year-ago period, a headwind for a relatively high-volume miner (low-grade, heap-leach) operating solely out of Mexico.

Orla - Quarterly Production Metrics (Company Filings, Author's Chart)

{kind=link}

Digging into the results a little closer, Orla's costs benefited from fewer waste tonnes mined, and lower blasting, maintenance, and reagent costs in the period. Meanwhile, the higher production was a result of a slightly higher processed grade (0.80 grams per tonne of gold), increased tonnes crushed and stacked, and daily stacking rates that continue to exceed nameplate capacity of 18,000 tonnes per day, with stacking rates of 18,902 tonnes in Q1 2023. The solid performance has left Orla with a ~2.5 million tonne stockpile of crushed ore (~114,100 tonnes) at 0.87 grams per tonne of gold and predominantly run of mine ore at 0.34 grams per tonne of gold, and the company is working to build a dome for its ore stockpile to improve dust control, making up part of its $6.0 million in planned sustaining capital this year.

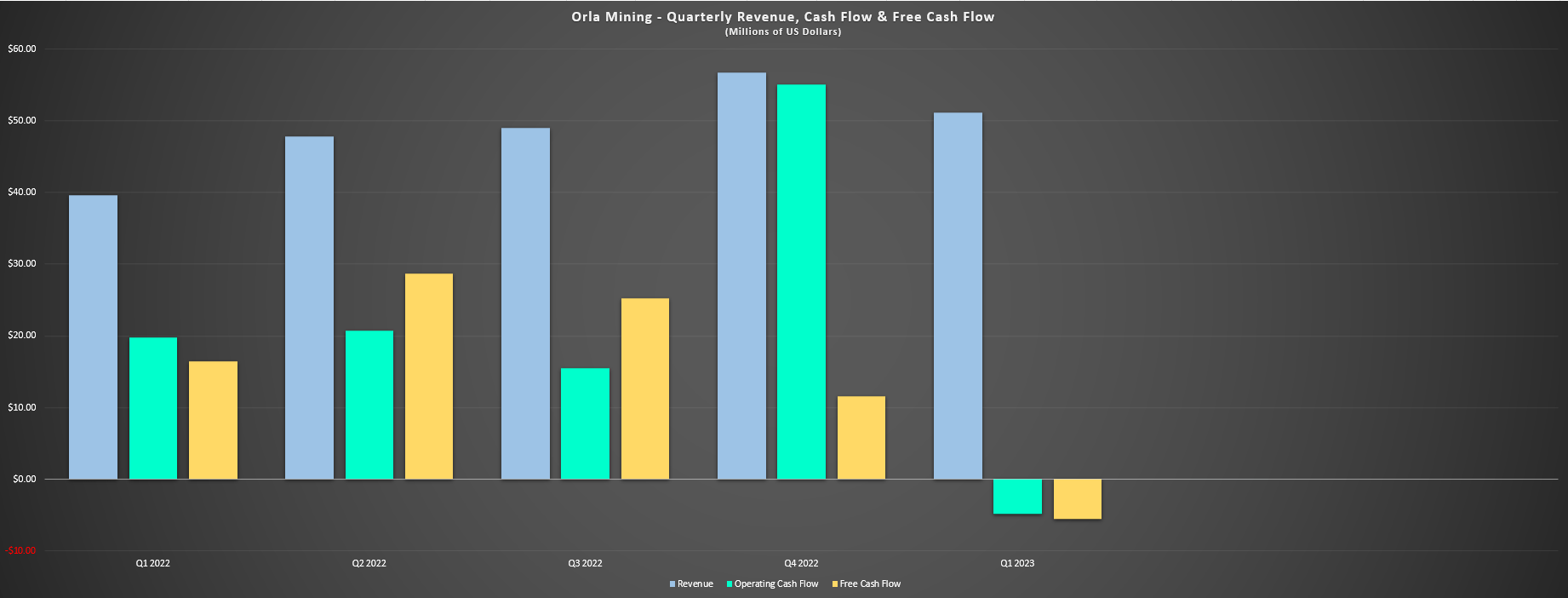

As for sales, Orla reported a flat average realized gold price of $1,888/oz in the period, but revenue surged to $51.1 million (Q1 2022: $39.6 million) due to the increased volume sold. This helped the company to finish the quarter with $83.8 million in cash and just $56.6 million in net debt, an enviable position for a company that began commercial production barely a year ago. In fact, there are some producers that have still barely put a dent in their net debt positions despite reporting commercial production in 2020, such as larger Yukon producer Victoria Gold ( OTCPK:VITFF ). And while a small investment for Agnico Eagle ( AEM ), the company certainly seems to like what Orla is doing at its Camino Rojo Mine, choosing to top up its investment in the company (8.9% ownership on an un-diluted basis) with ~4.0 million shares purchased at US$4.70 per share as part of its top-up right under the amended and restated investor rights agreement.

Last, from an exploration standpoint, Orla continues to report thick intercepts from Camino Rojo Sulphides, with highlight intercepts that include 22.9 meters at 4.02 grams per tonne of gold, 46.5 meters at 4.04 grams per tonne of gold, 21.0 meters at 6.12 grams per tonne of gold, and 55.5 meters at 3.08 grams per tonne of gold. These are Malartic-like intercepts that prompted Yamana Gold and Agnico to approve the Odyssey Underground Mine in Quebec, and the deep intercepts here that should grow the resource at improve grades are highly encouraging. Plus, from a regional standpoint, Orla continues to hit respectable grades, suggesting a high probability of mine life extension for Camino Rojo Oxides. For now, it's still early days regarding wrapping one's head around potential economics, but with a growing multi-million ounce resource base at Camino Rojo Sulphides, Orla arguably has one of the better development assets in small-cap/mid-cap gold producer space within in its portfolio which could easily sport a $1.2+ billion NPV (5%).

Costs & Margins

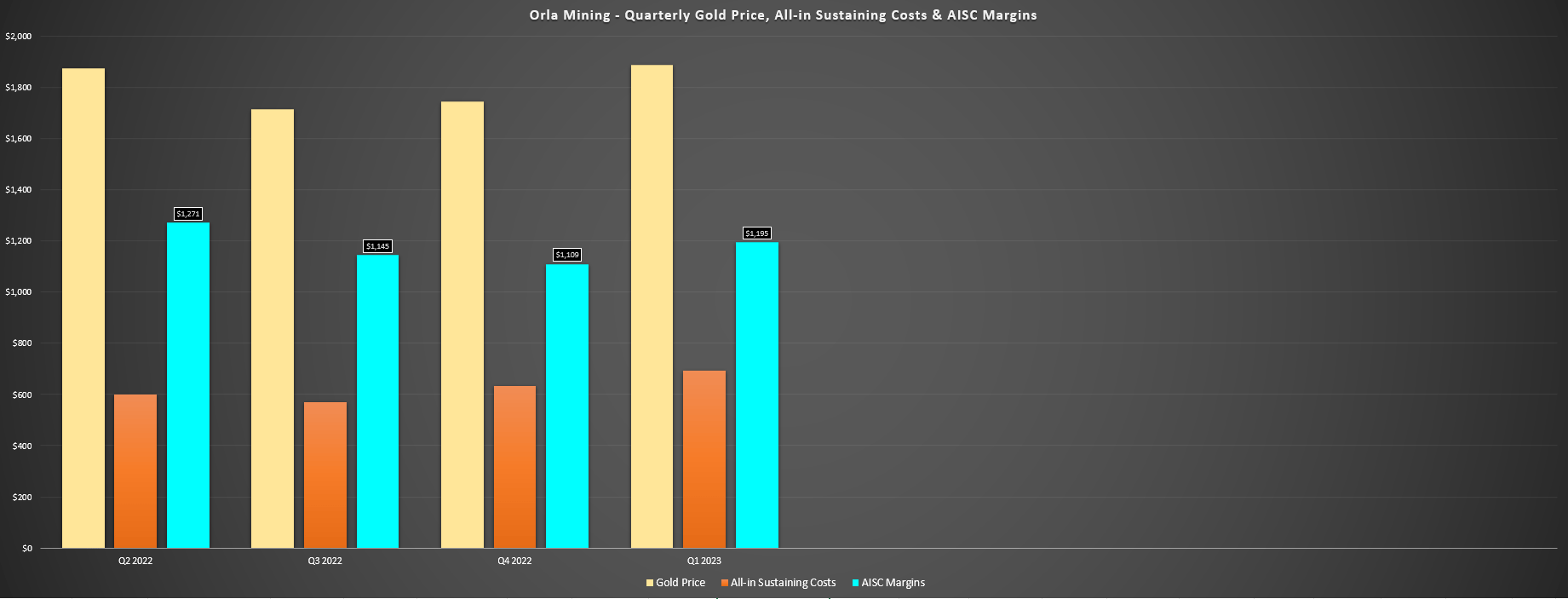

Moving over to costs and margins, Orla had another phenomenal quarter, reporting cash costs of $472/oz and all-in sustaining costs [AISC] of $693/oz, both over 40% below the industry average, respectively. In fact, Orla's AISC of $693/oz was over 47% below the estimated industry average of $1,310/oz in Q1, with the company boasting some of the highest AISC margins sector-wide at $1,195/oz (63.3% margin). However, while the gold price will be a tailwind in Q2 with a quarter-to-date average price of ~$1,970/oz, we should see some normalization in costs as the year progresses, with a pickup in waste tonnes mined during H2 and higher sustaining capital, with sustaining capital tracking at just ~18% of annual guidance. Therefore, with the market being forward-looking and the two strongest quarters of the year nearly over (Q1/Q2), I would expect a dip in margins during Q3/Q4 unless the gold price can remain above $1,950/oz, especially given the strength in the Mexican Peso.

Orla Mining - Gold Price, AISC, AISC Margins (Company Filings, Author's Chart)

{kind=link}

It's important to put things in context, and Orla will continue to be the highest-margin producer sector-wide even if costs climb closer to ~$800/oz in H2-2023. That said, like I warned on Lundin Gold ( OTCQX:LUGDF ), I would be careful not to extrapolate the strong Q1 results over the rest of the year, and while other producers may see a strong H2 vs. H1, Lundin and Orla are likely to be two producers with softer results that could lead to some underperformance. This is especially true given that they've massively outperformed their peer group over the past 12 months and some mean reversion would not be surprising. In summary, the ideal strategy would be to wait for lower prices into a softer back half of the year vs. chasing the stock with its best two quarters near completion.

Orla Mining - Quarterly Revenue, Cash Flow & Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

Finally, looking at the financial results, Orla reported cash flow of [-] $4.9 million in Q1 and a free cash outflow of $5.5 million, a significant deviation from the $20.5 million in cash flow reported last year. However, this was related to the $26.5 million payment of income taxes and while free cash flow was negative in Q1, we should see Orla report another strong year of free cash flow generation in 2023. And while up to $40 million in 2023 free cash flow may not seem significant, this is more free cash flow than many mid-tier producers are generating, let alone junior producers like Orla, helped by the impressive margins at Camino Rojo and the fact that the operation continues to operate at or above expectations (throughput above nameplate capacity and ore tonnes and recoveries in line with modeled assumptions). Let's dig into Orla's valuation:

Valuation

Based on ~351 million fully diluted shares and a share price of US$4.55, Orla Mining trades at a market cap of ~$1.60 billion and an enterprise value of ~$1.64 billion. And while the company boasts one of the highest estimated net asset values among the junior producer space with three key development assets (Cerro Quema, South Railroad, CR Sulphides), I still don't see enough margin of safety here based on its estimated net asset value of ~$2.24 billion. This is because I believe a 0.90x P/NAV multiple is more appropriate with the bulk of its NPV (5%) coming from Tier-2/Tier-3 jurisdictions (Mexico, Panama), which translates to a fair value of ~$1.86 billion or US$5.30. Plus, if we use a blended valuation of 70% weighting to P/NAV and 30% weighting to cash flow at a multiple of 9.0x FY2024 cash flow per share estimates ($0.28), Orla's estimated fair value comes in even lower at US$4.50.

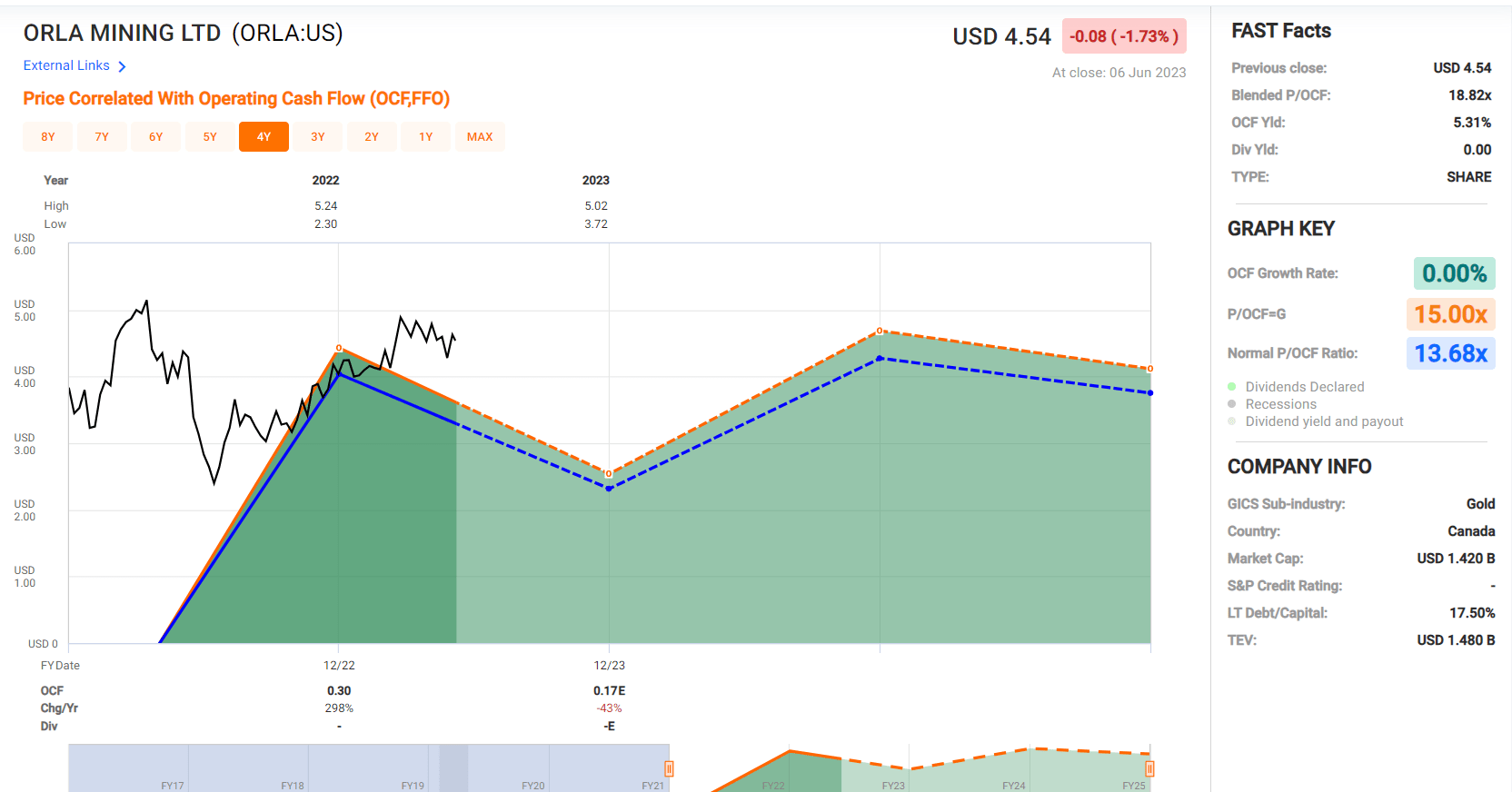

Orla Mining - Cash Flow Per Share (FASTGraphs.com)

{kind=link}

Given that my FY2024 cash flow per share estimates of $88 million severely understate Orla's long-term potential (which is the possibility of becoming a 400,000+ ounce gold-equivalent ounce producer by 2028), I would argue that valuing the stock on solely a P/NAV basis is appropriate (US$5.30 fair value). However, while this fair value estimate points to a 17% upside from current levels, I am looking for a minimum 40% discount to fair value for starting new positions in small-cap names to bake in an adequate margin of safety. After applying this required discount, Orla's low-risk buy zone comes in at US$3.20 or lower, suggesting that lower prices are needed to make the stock attractive from a valuation standpoint. Plus, the technical picture corroborates this view, with Orla sitting just shy of key resistance at US$4.80, and well above key support in the US$3.00 region.

ORLA - 3-Year Chart (StockCharts.com)

{kind=link}

Summary

Orla Mining continues to fire on all cylinders operationally and has been one of the few producers in the small-cap space to continuously over-deliver on promises, including constructing Camino Rojo on time and budget and exceeding guidance for its first year of commercial production. That said, and like Lundin Gold , much of this solid execution looks priced into the stock already, and from a relative value standpoint, there are larger producers trading at more attractive valuations, with some names trading at closer to 25% FY2025 free cash flow yields. This doesn't mean that Orla Mining can't continue its steady uptrend, but I prefer to buy only when there's a large margin of safety or pass entirely, and I don't see that present currently. So, while I continue to see Orla as a top-15 name sector-wide, I remain focused elsewhere for now.

For further details see:

Orla Mining: Another Blowout Quarter In Q1