CA - Orla Mining: Another Record Quarter In Q4

2023-03-20 10:33:23 ET

Summary

- Orla Mining released its Q4 and FY2022 results last week, reporting record quarterly production of ~32,000 ounces of gold, and FY2022 production of ~109,600 ounces.

- This translated to a massive beat vs. its initial FY2022 guidance midpoint of 95,000 ounces and all-in sustaining costs came in at the lowest levels sector-wide at $611/oz.

- Looking ahead to this year, we'll see another year of industry-leading margins plus more clarity on the date for first production at Railroad South plus the CR Sulphides opportunity.

- That said, while Orla is one of the sector's best growth stories with an enviable development pipeline, I don't see nearly enough margin of safety to justify paying up for the stock here above US$4.55.

We're nearing the end of the Q4/FY2022 Earnings Season for the Gold Miners Index ( GDX ), and it was a disappointing year overall. While several companies delivered on production estimates, many missed cost guidance, and some by a country mile, like Equinox Gold ( EQX ) and SSR Mining ( SSRM ). In fairness, this was because of stickier than expected inflationary pressures exacerbated by COVID-19 related exclusions, supply chain headwinds, and labor tightness in prolific regions. The result was that sector-wide all-in-sustaining costs soared 15% to ~$1,300/oz, a few companies ceased operations as net losses piled up, and on a two-year basis (FY2022 vs. FY2020), AISC margins compressed by 30% to just ~$500/oz, their worst levels since 2019.

Fortunately, there were some exceptions, and Orla Mining ( ORLA ) was one company to over-deliver on its promises. Not only did the company beat its initial FY2022 guidance by 15%, but it also beat cost guidance and reported the lowest costs among its peer group by a wide margin. In fact, Camino Rojo was one of the top-10 lowest-cost gold mines sector-wide in 2022, with all-in sustaining costs [AISC] of $611/oz which are even more impressive given that the asset doesn't benefit from economies of scale as a ~100,000 ounce per annum operation. Looking ahead to this year, the company enters 2023 much stronger with an impressive development portfolio and one of the sector's best growth profiles. Let's dig into the company's Q4/FY2022 results below.

Q4 & FY2022 Results

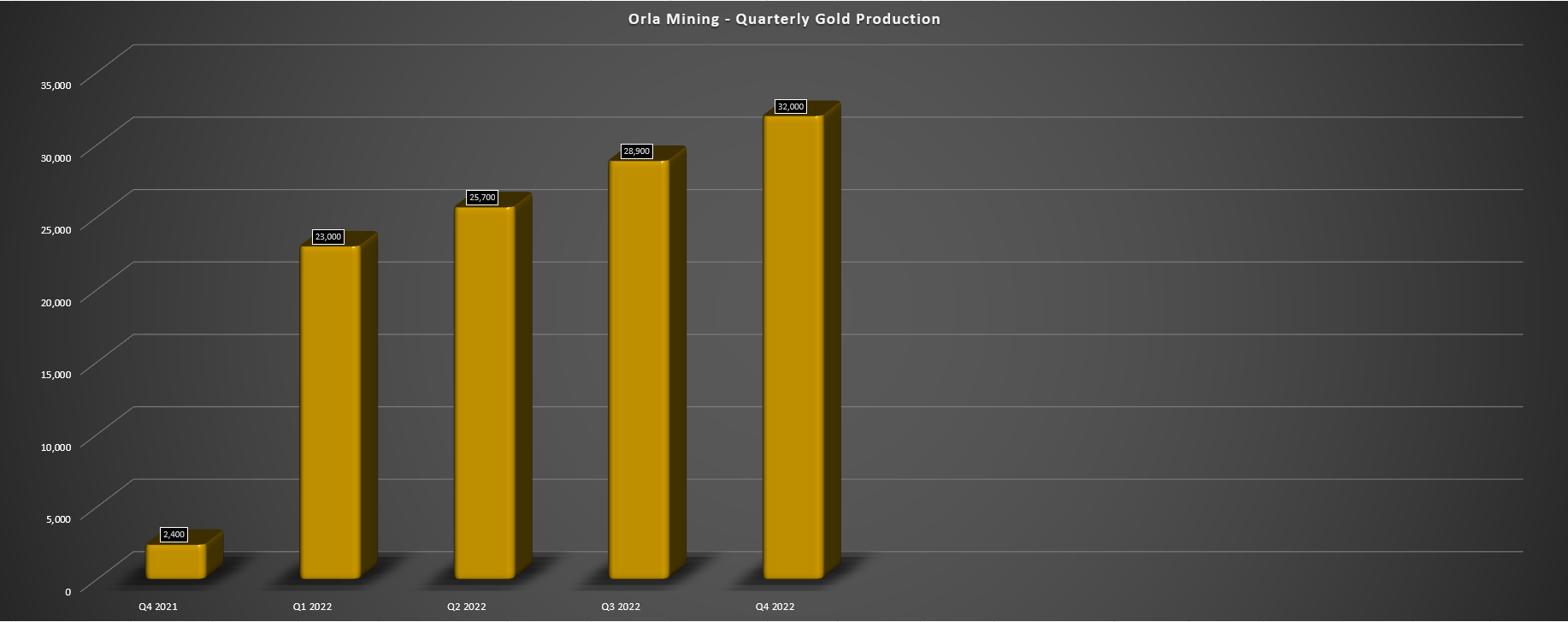

Orla Mining released its Q4 and FY2022 results last week, reporting yet another quarterly record with the production of over 32,000 ounces of gold, an 11% increase sequentially. The strong finish to 2022 catapulted Orla's full-year production well past its initial and upwardly revised guidance midpoints of 95,000 ounces and 105,000 ounces, respectively, with the company reporting a massive 15% beat vs. its initial guidance, an incredible feat for a mine in its first year of operation where we can sometimes see teething issues. Just as impressive, it built its Camino Rojo Oxides mine on schedule and under budget in an inflationary environment, over-delivering in both the construction and operations department in what was a tough year for the sector.

Orla Mining - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

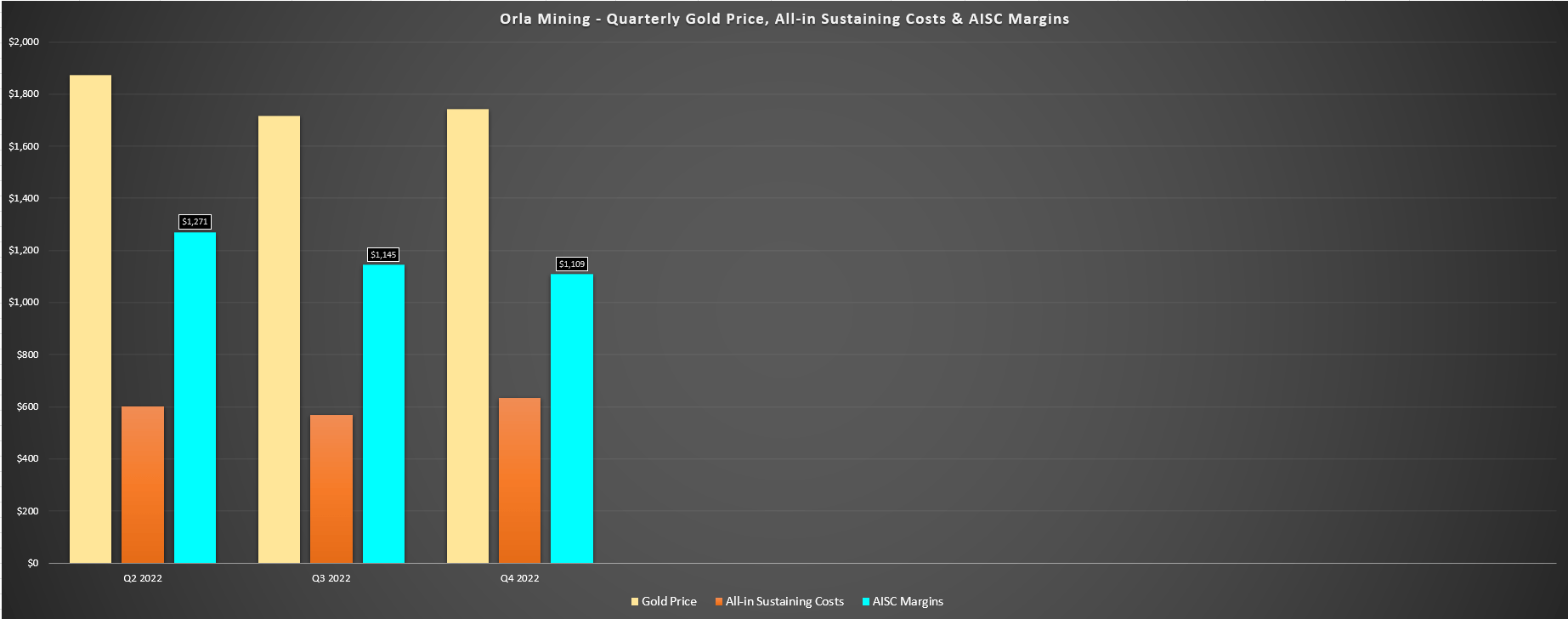

Regarding the impressive Q4 and FY2022 performance, Orla noted that stacking rates came in at ~19,600 tonnes per day in Q4 (9% above nameplate capacity), a quarterly record for the company. Orla noted that the strong year benefited from softer ore than planned in the upper benches of the mine, leading to reduced maintenance for its crushing, stacking, and conveying systems. It also saw lower consumption of electricity and reagents and sustaining capital for the year came in just shy of guidance ($3.53 million). The result was that Orla beat on production and costs, with the latter being especially impressive given that the average producer saw a high single-digit miss vs. its cost guidance. In fact, Q4 AISC came in at $634/oz with FY2022 AISC of $611/oz.

Orla - Quarterly Gold Price, AISC & AISC Margins (Company Filings, Author's Chart)

{kind=link}

As shown in the chart below and despite no help from the gold price in Q4 2022 ($1,743/oz), AISC margins came in at $1,109/oz, more than double the industry average of ~$470/oz. Meanwhile, FY2022 AISC margins came in at an impressive ~66% ($1,179/oz), also more than double the industry average of ~$500/oz. Given the solid cost performance and relatively low sustaining capital, Orla reduced its long-term debt to just ~$100 million. The result of the significant free cash flow generation (FY2022: $82.0 million vs. [-] $138 million in FY2021) was that it ended the year with a net debt position of just $49.5 million, a solid balance sheet for a company that's been in commercial production for less than a year, and certainly a better position than producers like Victoria Gold ( VITFF ) that continue to under-deliver on their promises.

The only negative for Orla Mining following these exceptional FY2022 results is that lapping this performance won't be easy, and the company has guided for production of 105,000 ounces at $800/oz AISC at the mid-point in FY2023. The expectation for increased operating costs is related to higher sustaining capital, and a full year of inflationary pressures (labor, reagents, consumables). Assuming the company over-delivers this year like it did in FY2022 and reports production of ~109,000 ounces at AISC of $790/oz, AISC with an average realized gold price of $1,870/oz, we would see annual AISC margins dip to $1,080/oz. That said, these would still be industry-leading margins. So while Orla has tough comps ahead, the recent gold price strength and another guidance beat could minimize the expected margin compression.

Recent Developments

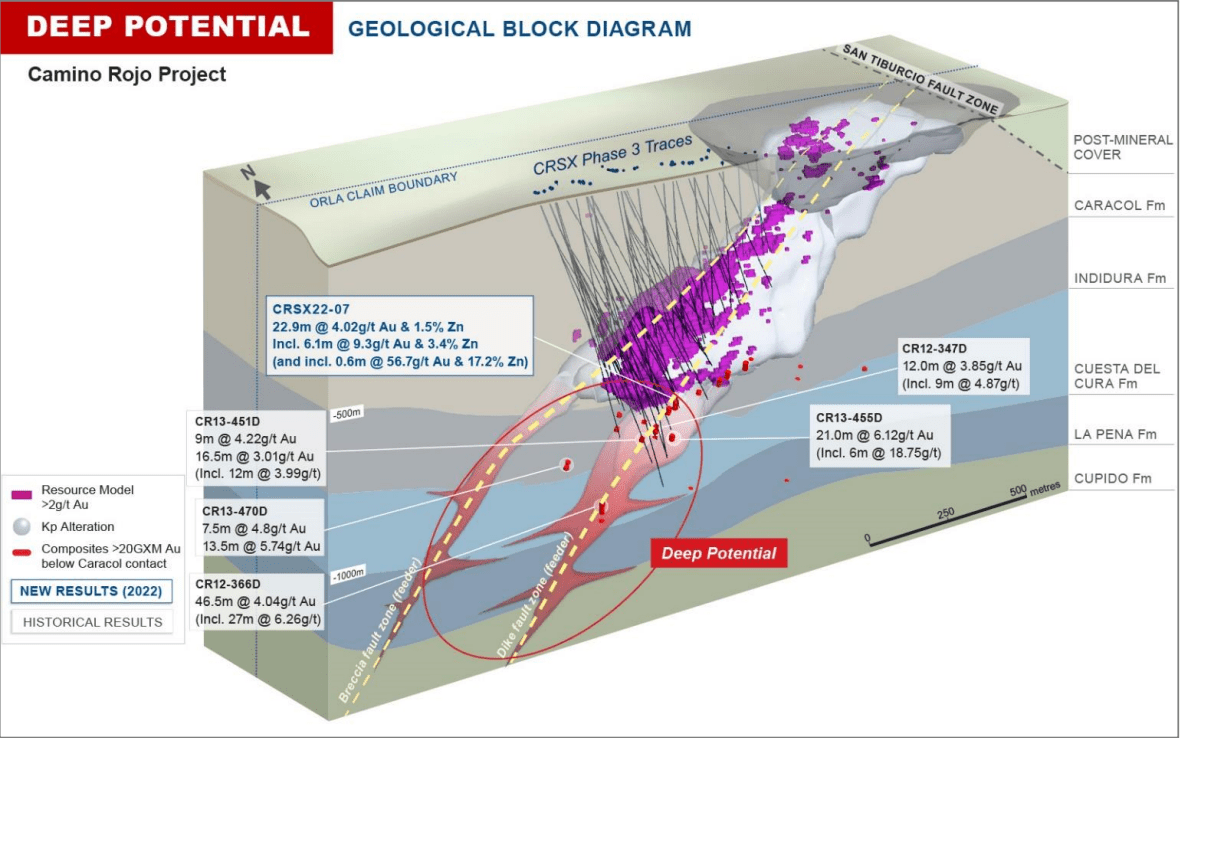

Moving over to recent developments, Orla had a phenomenal year from an exploration and development standpoint as well, adding a new Tier-1 jurisdiction (Nevada) with its acquisition of Gold Standard Ventures, and a massive land package southeast of the famous Carlin Complex. Meanwhile, at Camino Rojo Sulphides, the company continues to hit much higher grades at depth than what's in its current mineral inventory, with highlight intercepts at depth including:

- 22.9 meters at 4.02 grams per tonne of gold and 1.5% zinc

- 16.5 meters at 3.01 grams per tonne of gold

- 46.5 meters at 4.04 grams per tonne of gold

- 21.0 meters at 6.12 grams per tonne of gold

- 7.5 meters at 4.8 grams per tonne of gold and 13.5 meters at 5.74 grams per tonne of gold

Camino Rojo Project - Geological Block Diagram (Company Presentation)

{kind=link}

Not only are these intercepts over very mineable widths, but they are much higher grade than the ~7.3 million ounce measured & indicated [M&I] resource in place currently and suggest the potential for feeder zones down-plunge. These impressive results combined with positive early metallurgy work (two zones amenable to conventional CIL processing, and selective flotation could be used to produce a gold concentrate) suggest the possibility of a stand-alone facility to process sulphide material at Camino Rojo. 2023 work will include additional testing of mineralization at depth (20% of drilling on the deep extension target) and infill drilling to provide the basis for a Preliminary Economic Assessment that will finally give investors an idea of the possible economics of Camino Rojo Sulphides.

Meanwhile, although grades quite as strong as current head grades at Camino Rojo Oxides, Orla hit decent oxide grades in first-pass drilling at its Guanamero target that sits 7 kilometers northeast of current mining areas. This is one of several high mag targets on the property and the first hole [CRED22-01] hit 7.10 meters of 0.54 grams per tonne of gold and 2.35 grams at 1.35 grams per tonne of gold. Encouragingly, Orla noted in its prepared remarks that it hit similar geology to what it's encountered at Camino Rojo Deeps. Although it's early to look at this as a potential satellite target, exploration at Camino Rojo continues to surprise to the upside, both from a near-mine oxide standpoint (CRSX22-05 hit oxide and transitional material on the edge of the open pit), and a sulphide standpoint.

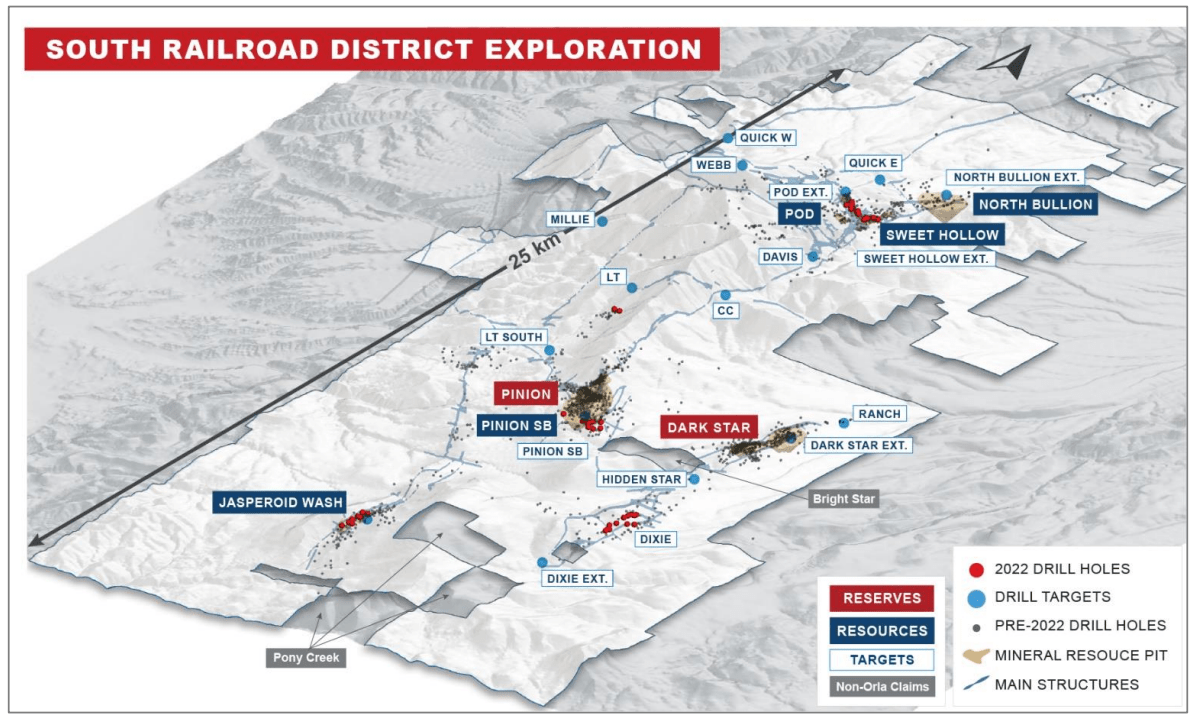

Finally, at the company's newest project, Railroad-South, Orla isn't wasting any time from an exploration standpoint, with plans to spend $10 million after what was already a busy 2022 drill season. Regarding 2022 drill results, several intercepts were quite encouraging, with 25.92 meters of 4.87 grams per tonne of gold at its POD target (transition material) which included 13.7 meters at 8.52 grams per tonne of gold in oxides, and 19.8 meters at 0.81 grams per tonne of gold in oxide at its Dixie target. Elsewhere and just southeast of its reserves at Pinion, Orla hit a thick intercept of solid grades (53.3 meters at 0.85 grams per tonne of gold) at its Pinion SB target.

{kind=link}

As the chart above highlights, Orla may have added a solid heap-leach operation with its acquisition of Gold Standard (~152,000 ounces in first four years at ~$1,000/oz AISC), but the bonus is that it added a massive land package with fifteen targets outside of reserves at Pinion (mid-grade) and Dark Star (high-grade) across a 25-kilometer strike length. So, in a perfect world and assuming it enjoys exploration success, this could potentially end up similar to what AngloGold ( AU ) appears to have in Nevada in the Beatty District after consolidating land here (Corvus acquisition and Sterling/Crown acquisition) which is a hub capable of producing well over 250,000 ounces of gold per annum long-term.

So, while investors can look forward to first production as early as H2 2025 at South Railroad that will shed Orla's single-asset producer status, investors should keep a close eye on exploration success here that could increase its long-term potential in Nevada, with a land package and enough targets that could easily support a 250,000-ounce plus production profile in one of the world's top mining jurisdictions. Let's dig into the stock's valuation following a year of outperformance (6% return last year vs. an 11% decline in the GDX).

Valuation & Technical Picture

Based on ~347 million fully diluted shares and a share price of US$4.55, Orla Mining trades at a market cap of ~$1.58 billion and an enterprise value of ~$1.63 billion. This leaves Orla trading at ~0.76x P/NAV, which is not an unreasonable multiple for industry-leading margins and a development pipeline of this caliber (multiple high-margin assets, with one in Nevada). That said, I believe a fair multiple for the stock is 0.90x P/NAV given that while it has industry-leading margins and continues to enjoy exploration success, it will remain a single-asset producer until at least Q2 2025. After applying a 0.90x P/NAV multiple and subtracting net debt and estimated general & administrative expenses [G&A], I see a fair value for the stock of ~$1.86 billion or US$5.35 per share.

Although this fair value estimate points to an 18% upside for the stock (which suggests that we could see a move to new 52-week highs if it were to trade up towards fair value), I prefer to bake in a significant margin of safety when entering new positions in small-cap producers and especially single-asset producers. After applying a required a 40% discount to fair value to justify entering new positions and ensuring an adequate margin of safety, Orla Mining's ideal buy zone would come in at US$3.20 or lower, significantly below current levels. Obviously, there's no guarantee that the stock suffers a decline of this magnitude, especially when it continues to fire on all cylinders, but I prefer to go where the most value is, and while I see Orla as a solid buy-the-dip candidate, the valuation is less compelling after this rally.

{kind=link}

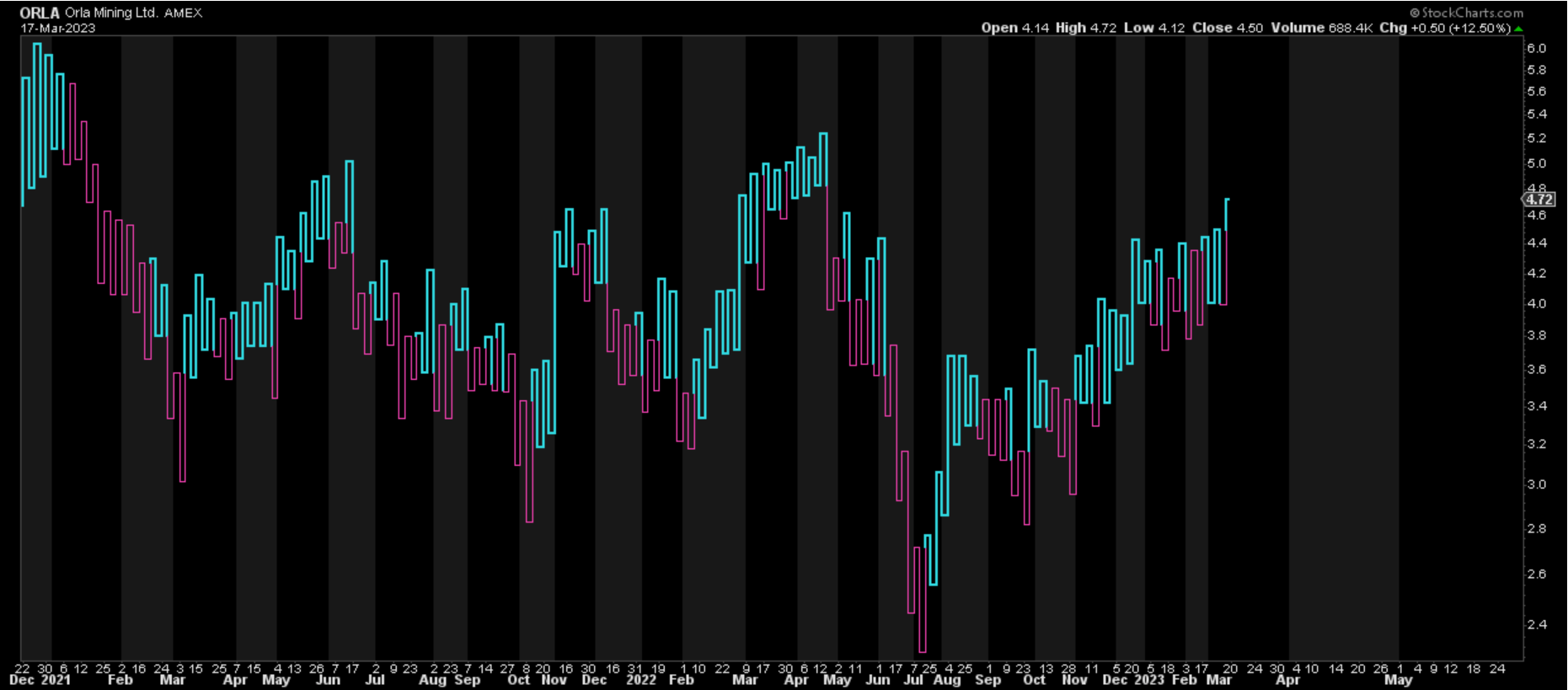

Finally, if we look at the technical picture, Orla Mining is hovering in the upper portion of its support/resistance range, with strong resistance US$4.65 - US$4.75 and no strong support levels in place until US$3.20 - US$3.30. This doesn't mean that the stock must fail here, and it could certainly continue its outperformance vs. its peer group. That said, the current reward/risk ratio even using the top end of the resistance range and top end of the support zone is 0.16 to 1.0, which is a very unfavorable reward/risk ratio compared to some other names out there currently. This corroborates the view that Orla is not in a low-risk buy zone, and suggests that a continuation of this rally could run into selling pressure.

Summary

Orla Mining continues to be a top-10 growth story sector wide and while it may look expensive on a market cap per ounce produced basis, this metric doesn't provide any value for its significant development portfolio that could add upwards of 300,000 ounces of gold production per annum by the end of the decade. This cap also doesn't give any value to satellite targets on its properties, which arguably should hold some value given the exploration success Orla is enjoying at all three properties.

That said, the stock is nowhere near a low-risk buy zone after its 100% plus rally since last July and I don't see nearly enough margin of safety at current levels. So, if we were to a see continuation of this rally, I would view any move above US$4.76 before April as an opportunity to book some profits. And while some investors might argue that Orla is a potential takeover target given its growing production profile in attractive mining jurisdictions (Zacatecas, Nevada), I see the likelihood of a suitor coming in at these prices and offering a premium as quite low.

For further details see:

Orla Mining: Another Record Quarter In Q4