CA - Orla Mining: Limited Margin Of Safety At Current Levels

2023-08-17 05:21:55 ET

Summary

- Orla Mining reported Q2 production of 29,100 ounces of gold, a 13% increase from the previous year at industry-leading AISC of $698/oz.

- This helped the company to improve its balance sheet further with it having net debt of just ~$20 million less than 18 months after it began commercial production.

- Unfortunately, we did see the delayed receipt of permits related to the Camino Rojo layback and Railroad South could take longer to head into production than I originally expected.

- However, while remains a solid growth story with room for a re-rating long-term once Railroad South comes online, its outperformance has made it less attractive from a relative value standpoint vs. peers.

The Q2 Earnings Season for the Gold Miners Index ( GDX ) is coming to a close and while several producers reported flat to lower production and weaker margins year-over-year, Orla Mining ( ORLA ) was one clear exception. Not only did the company report the highest margins sector-wide at $1,277/oz (~65%), it also reported another quarter of strong free cash flow generation and meaningful sales growth year-over-year. This has placed it on track to potentially beat its FY2023 guidance mid-point and, although related to permitting delays, the company has lowered its cost guidance due to fewer waste tonnes mined than planned, setting the company up to be the sector's lowest-cost gold producer for a second consecutive year. Let's take a closer look at the results and recent developments below:

Q2 Production & Sales

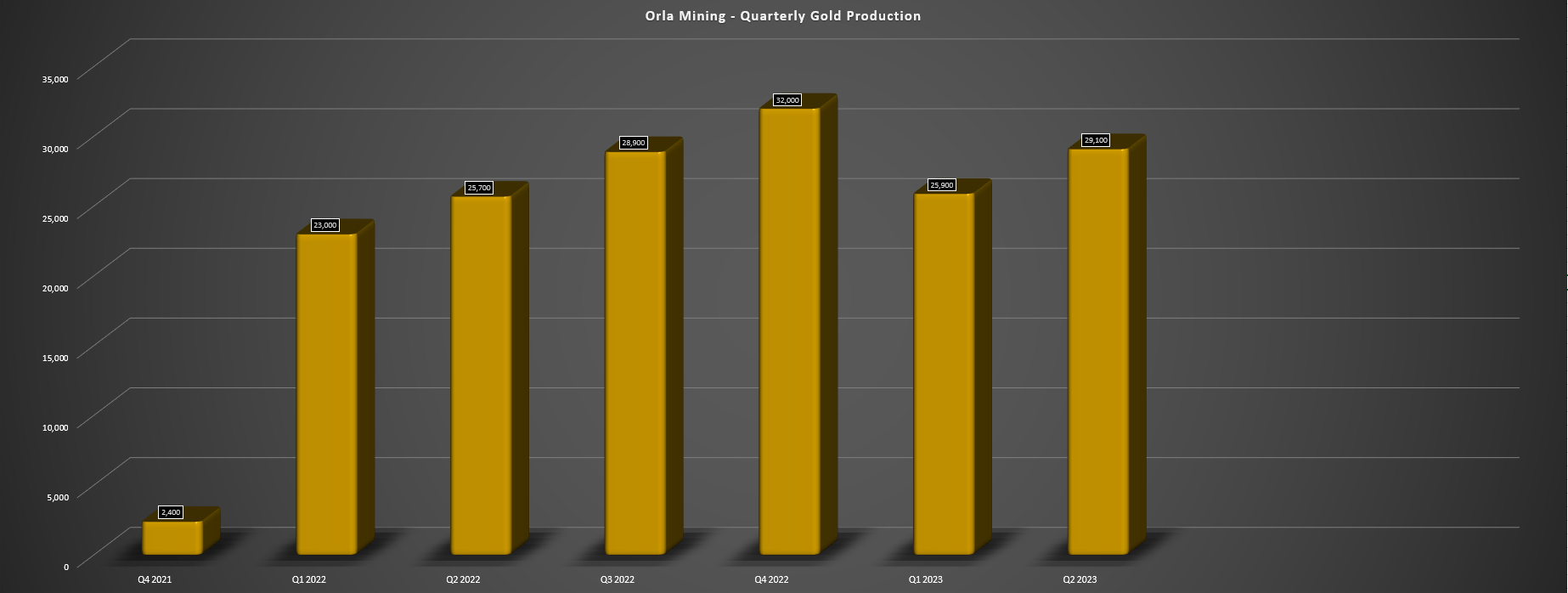

Orla Mining released its Q2 results last year earlier this month, reporting quarterly production of ~29,100 ounces of gold, a 13% increase from the year-ago period, and its second best quarter to date since it began commercial production at Camino Rojo Oxides last year. The solid performance was driven by stacking rates that continue to sit well above design capacity (~19,700 tonnes per day), grades that continue to sit well above the industry average for heap-leach operations and ore tonnes and process recoveries that continue to reconcile well with expectations. This exceptional performance has left the company tracking at 50% of the top end of its FY2023 guidance (~55,000 ounces produced year-to-date), and the company has shown impressive cost controls despite the backdrop of a rising Mexican Peso.

Orla - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

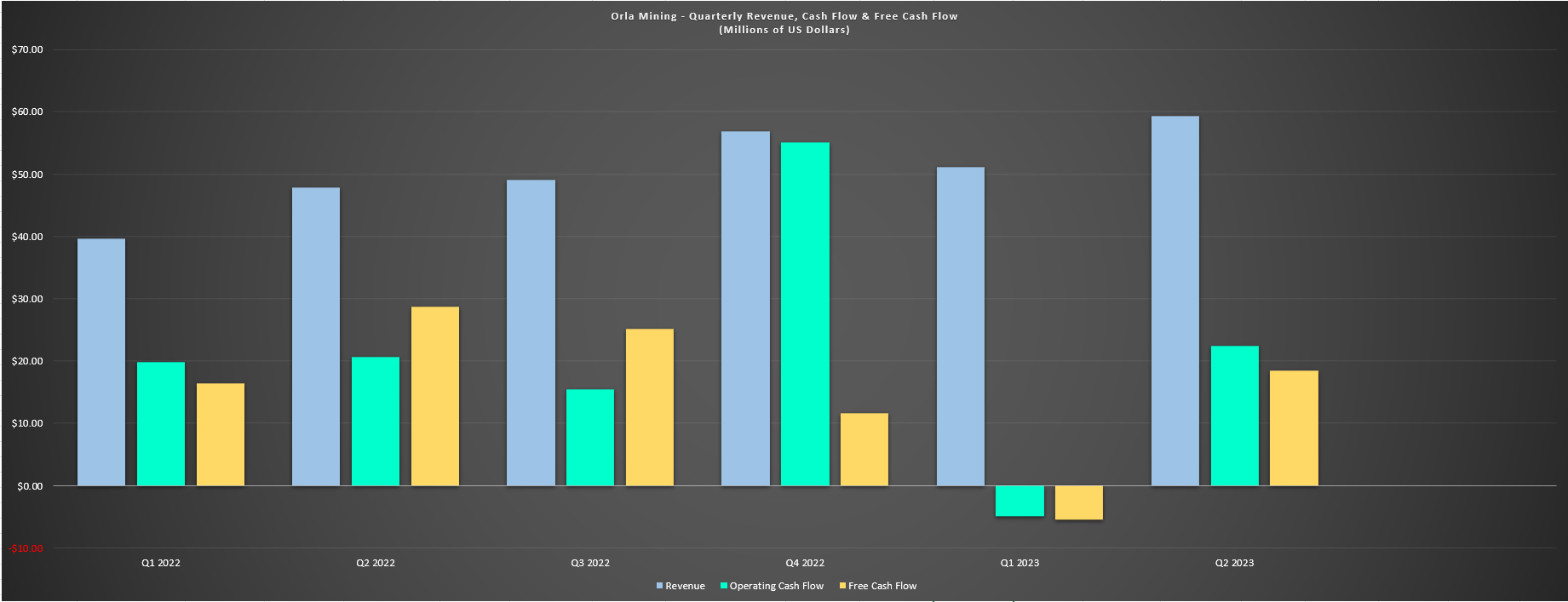

Moving over to Orla's financial results, the company reported revenue of $59.3 million (+24% year-over-year), benefiting from increased ounces sold and a record average realized gold price of $1,975/oz. This was above the industry average for the average realized price reported in the period, and helped the company to generate $18.5 million in free cash flow in the period, with Orla ending the period with ~$115 million in cash and barely $20 million in net debt, a solid balance sheet for a company that began commercial production less than 18 months ago. That said, we will see some cash outflows towards year-end for Orla from the final Fresnillo ( OTCPK:FNLPF ) payment of $22.8 million as part of the ~$63 million payment for the Layback Agreement (expanding its CR Pit onto part of Fresnillo's mineral concessions).

Orla Mining - Quarterly Revenue, Cash Flow & Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

Costs & Margins

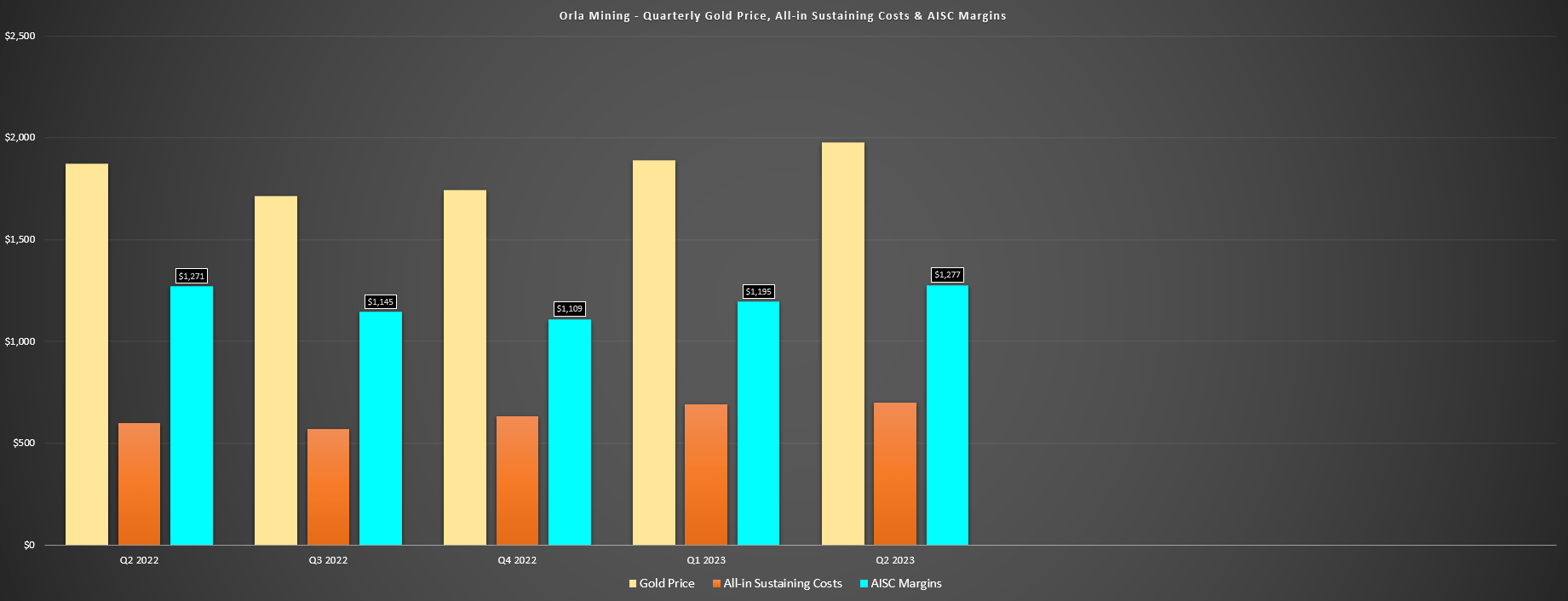

Moving over to costs and margins, Orla had another outstanding quarter, reporting all-in sustaining costs of $698/oz, nearly 50% below the estimated industry average of ~$1,360/oz in the period. This incredible cost performance was despite a foreign exchange headwind with the Mexican Peso hitting new multi-year highs against the US Dollar ( UUP ), allowing Orla to report AISC margins of $1,277/oz (~65% margins). However, Orla Mining noted that it benefited from fewer waste tonnes mined than initially expected, with this being attributed to the slower than planned receipt of permits from the Secretariat of Environmental & Natural Resources ["SEMARNAT"], with the Change of Land Use permit (related to the pit layback not included in the August 2019 CUS permit application) being declined for procedural reasons due to SEMARNAT's internal process timelines.

Orla - All-in Sustaining Costs, Gold Price & AISC Margins - Company Filings, Author's Chart

{kind=link}

The good news is that the delayed receipt of this permit will not affect 2023 production and it is not expected to impact 2024 production either. And given the lower strip ratio, Orla has revised its cost guidance to $700/oz to $800/oz vs. its previous outlook of $750/oz to $850/oz because of the lower strip ratio. That said, if this permit is not received at some point next year, this could affect planned 2025 production levels given the time needed for waste stripping. Orla noted in its Q2 Conference Call that it could there are mitigations available if this is the case, but that it doesn't expect to have any issues, with Orla stating:

"We have a great relationship in the state of Zacatecas personally with the governor who's spoken on our behalf with the President. The President has appointed the Secretary of the Economy for the state of Zacatecas to be the liaison for Zacatecas-based mining companies and the federal SEMARNAT agencies."

- Orla Mining, Q2 2023 Conference Call

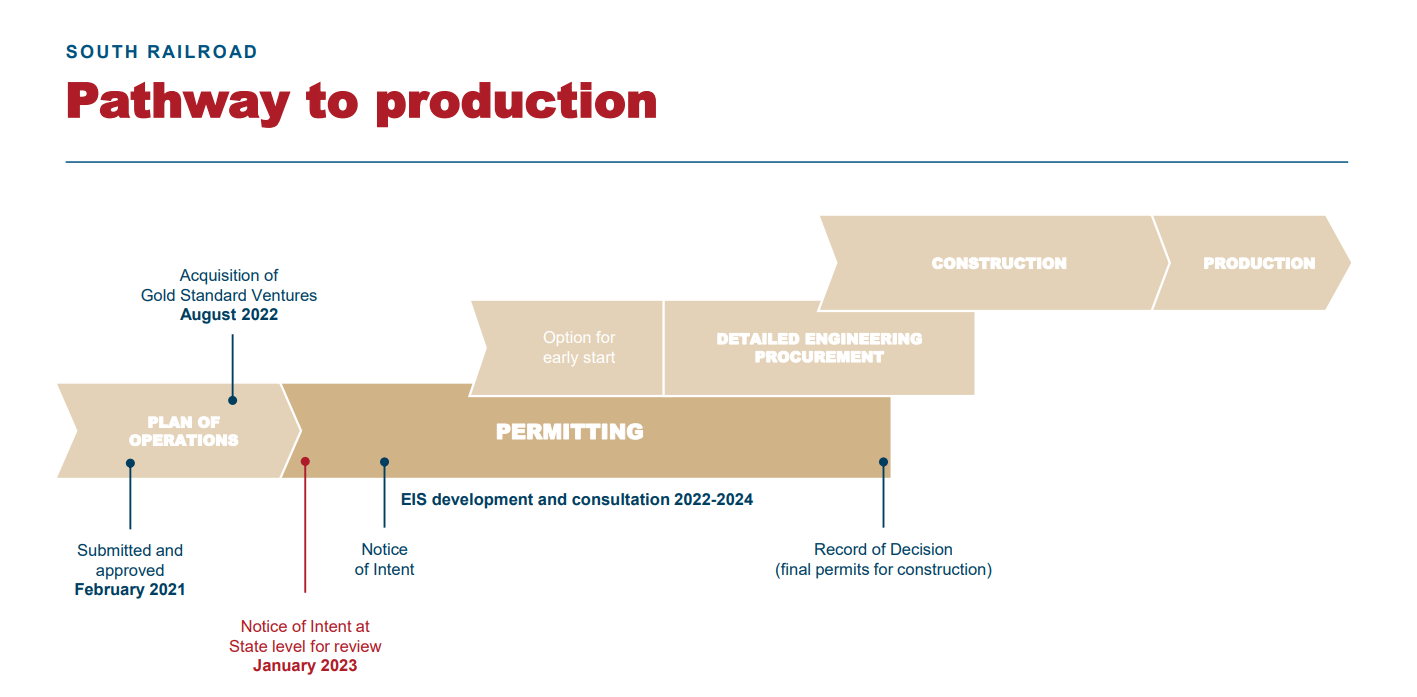

Overall, I see the risks to the operation here as low and don't see this as a reason to be overly concerned. That said, the South Railroad Project is moving a little slower than I expected through the permitting process. This is unfortunate given that it's impeding Orla's ability to graduate to dual-producer status and diversify its production profile, which I would expect to translate to a higher multiple when achieved. Let's take a closer look below:

Recent Developments

As discussed in the MD&A and news release, Orla Mining expects the Nevada Bureau of Land Management [BLM] to file its Notice of Intent [NOI] in the Federal Register later this year or in early 2024. Once filed, public scoping meetings can begin towards the granting of the Environmental Impact Statement [EIS] ahead of an eventual Record of Decision [ROD] which Barrick continues to wait for with unfortunate delays at Goldrush on the Battle Mountain Trend (South Railroad is on the Carlin Trend). As it stands, it would surprise me to see the ROD granted before Q2 2025, suggesting South Railroad will not start production until at least 2026. And with this being more advanced than Cerro Quema, Orla will remain a single-asset producer for another three years, longer than I initially expected, which was an H2 2025 first gold pour (placing some conservatism on Gold Standard's Q3 2024 estimate ).

This is not a big deal and I don't see any reason to believe that Orla won't get its permits at South Railroad, which will ultimately add ~150,000 ounces over the first four years at sub $1,150/oz all-in sustaining costs in its early years (adjusted for inflationary pressures), placing Orla on a path to becoming a ~250,000 ounce producer with peak production closer to 300,000 ounces in 2027 (~100,000 ounces Camino Rojo, ~190,000 ounces of peak production at South Railroad). However, with South Railroad continuing to await its permits and now additional (albeit minor) permitting uncertainty at Camino Rojo, I continue to believe that a 0.90x P/NAV multiple is more appropriate for Orla Mining, even if it the highest-margin producer in the sector by a wide margin for the time being.

The final development worth noting is that Orla continues to spend aggressively on exploration, with $10.5 million spent in Q2 2023 alone, one of the largest budgets among junior producers. This continues to pay off in spades with multiple impressive intercepts from Camino Rojo Sulphides (a growth project at its operating Camino Rojo Mine), and the company will likely release drill results from South Railroad later this year with drilling having begun in Q2. Its goal this year is to upgrade and grow its resource its satellite deposits (of which there are multiple outside of the main Dark Star and Pinion pits in the mine plan), with solid oxide grades reported earlier this year at Pinion SB and Dixie (south of Dark Star), and POD. So, with more drill results to come from Cerro Quema, Railroad South, and potentially Camino Rojo Sulphides, it should be a busy rest of the year, with an updated resource at CR Sulphides to follow this year's drill program.

Summary

Using what I believe to be a fair multiple of 0.90x P/NAV and 9.0x FY2024 cash flow given its industry-leading margin profile and a 65% weighting to P/NAV and 35% weighting to P/CF, I see a fair value for the stock of US$4.90. And although this points to a 9% upside from current levels, I am looking for a far greater upside to justify starting new positions in precious metals stocks, and especially single-asset producers in Tier-2 ranked jurisdictions. And while Zacatecas is one of the better states in Mexico, the jurisdiction has certainly had its challenges even among the better states, with a strike continuing at Newmont's ( NEM ) Penasquito, multiple illegal blockades over the years (San Jose, Los Filos), and now some uncertainty around mining law reforms.

South Railroad - Permitting Process & Path To Production - Company Presentation

{kind=link}

The above issues (history of blockades, nearby strike, potential mining law reforms) don't directly affect Orla's Camino Rojo Operations and while the strength in the Mexican Peso affects its costs, the company certainly has the margins as the sector's lowest-cost producer to absorb any cost pressures. Still, I prefer having a minimum 35% discount to fair value to justify starting a new position in a single-asset producer, and if we apply this discount, the stock would need to decline below US$3.20 to become more interesting. Hence, with more attractive relative value bets elsewhere in the sector and a slower path to first production than I initially expected at South Railroad (impeding it from attaining dual-asset producer status before 2026), I remain focused elsewhere currently.

For further details see:

Orla Mining: Limited Margin Of Safety At Current Levels