CA - Orla Mining: Patience Required

2023-05-03 05:36:17 ET

Summary

- Orla Mining was one of the best-performing precious metals names in 2022, eking out a 6% return vs. a 15% decline in the Gold Juniors Index.

- This outperformance was not surprising, given that it was one of the few miners to beat production/cost guidance in a year plagued by inflationary pressures and supply chain headwinds.

- However, Orla is not cheap after doubling off its 2022 lows & while mining law reforms shouldn't affect CR Oxides, it's unclear if they will impede growth at the project.

- Given the recent mining law reforms, that Orla continues to look close to fully valued short term, and its difficult comps on deck, I continue to see more attractive bets elsewhere in the sector.

The Q1 Earnings Season for the Gold Miners Index ( GDX ) has finally begun and the results have been mixed, with solid reports out of Alamos Gold ( AGI ) and Agnico Eagle ( AEM ) offset by a mediocre report and tough start to the year for Newmont ( NEM ). One name that's yet to report but released its preliminary Q1 results is Orla Mining ( ORLA ), a junior producer with a high-margin heap-leach operation in Zacatecas, Mexico and several development projects, including its newly acquired South Railroad Project in Nevada and Cerro Quema in Panama. In this update, we'll look at the company's preliminary Q1 results and how the recent gold price strength has impacted its FY2023 margin outlook.

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q1 Production & Sales

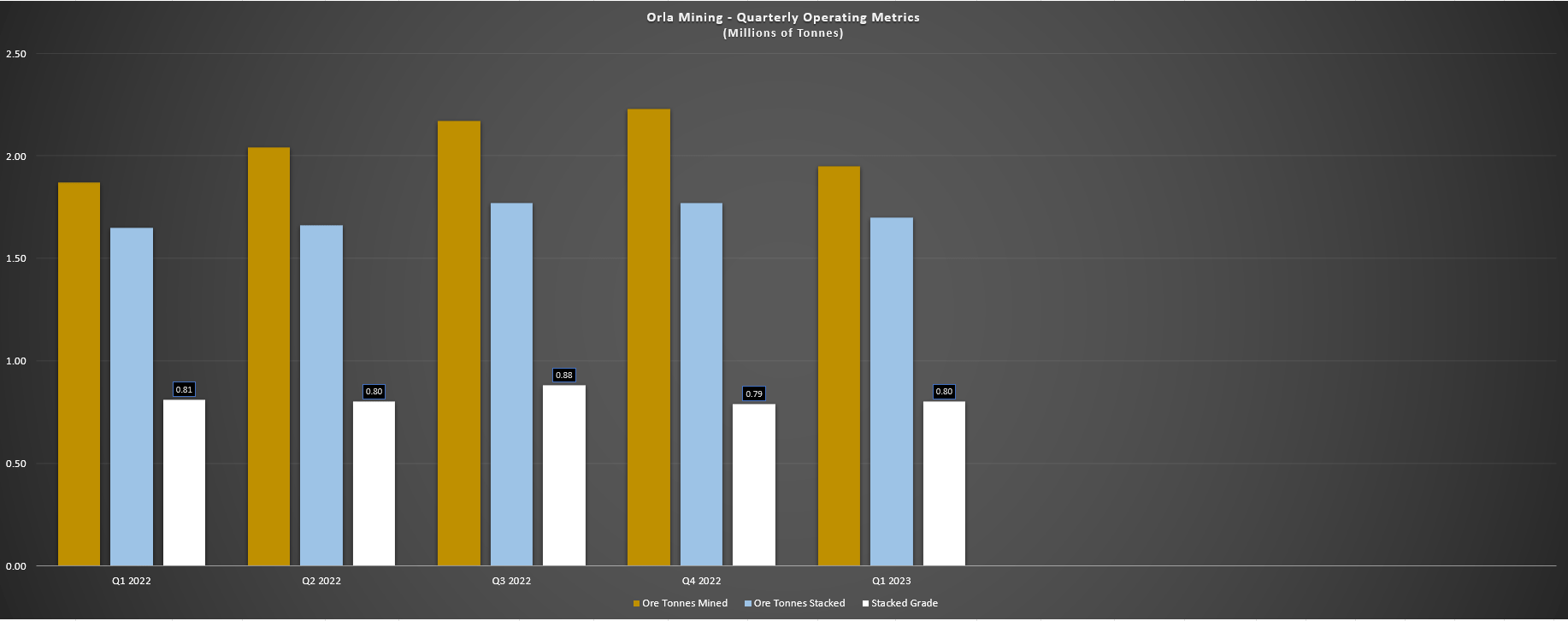

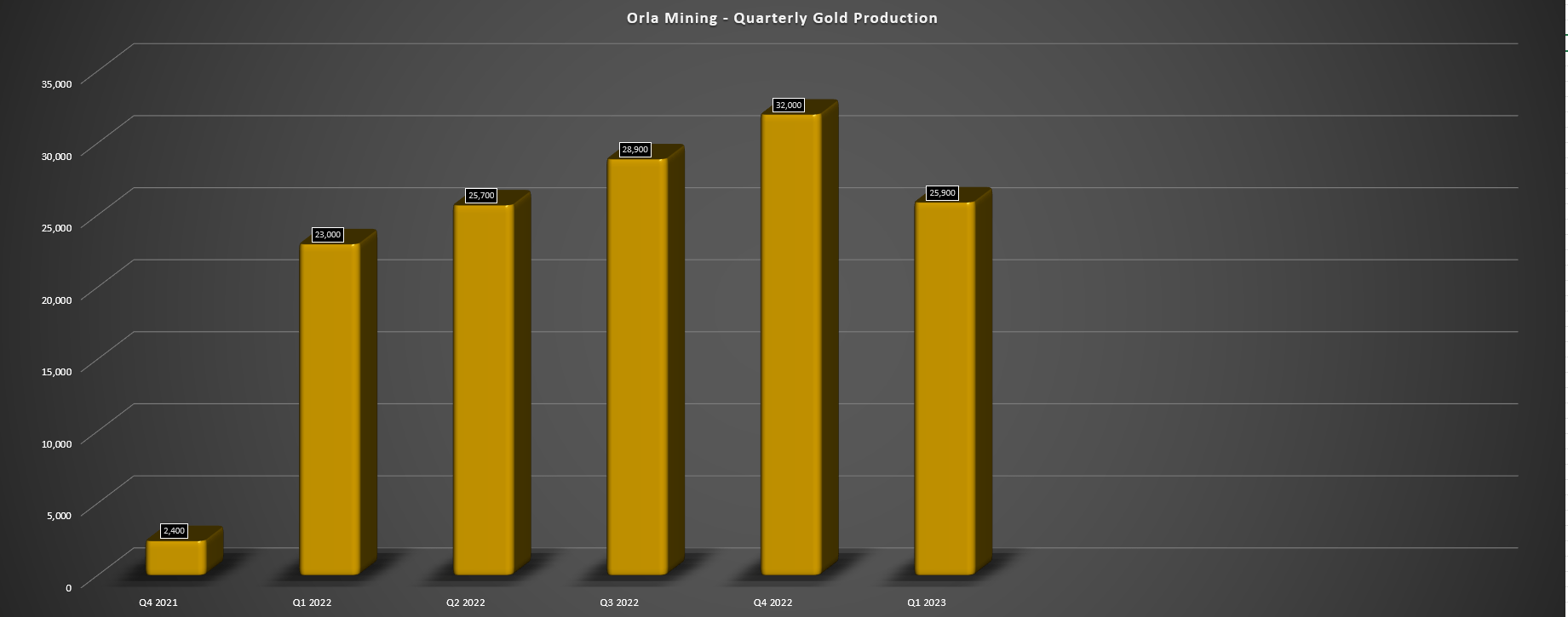

Orla Mining released its preliminary Q1 results last month, reporting quarterly production of ~25,900 ounces of gold in the period that it lapped the start of commercial production last year. This is tracking in line with the company's guidance midpoint of ~105,000 ounces this year, and Orla sold ~26,800 ounces in the quarter, setting the company up for a strong quarter of revenue with its average realized price likely to come in above $1,890oz. The company noted that it mined ~1.95 million tonnes of ore and stacked ~1.70 million tonnes at an average grade of 0.80 grams per tonne of gold. Notably, its daily throughput rate consistently coming in above design capacity at ~18,900 tonnes per day in Q1, up from ~15,100 tonnes in Q1 2022.

Orla Mining - Quarterly Operating Metrics (Orla Mining - Company Filings, Author's Chart)

{kind=link}

Looking at the chart below, we can see that production increased nearly 13% year-over-year, and continues to track well against expectations, a welcome surprise after we saw messy start-ups for a couple of mines that included Revenue-Virginius and Madsen. In addition, Orla brought its Camino Rojo Oxides Mine into production on time and under budget, another rarity given the inflationary pressures felt sector-wide. This is a testament to the strength of the management team, and it's encouraging to see that Orla isn't resting on its laurels, expecting to invest over $33 million across its projects this year for exploration, one of the largest budgets sub 200,000-ounce producers.

Orla Mining - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

Given the strong start to the year, Orla Mining is in a great position to beat production guidance again this year, and it should have a decent shot at beating its cost guidance of $800/oz. This is because we appear to be seeing a slight moderation in inflationary pressures sector-wide, and although it's still early in earnings season, Agnico Eagle noted that it's seeing some easing and a decline in steel and fuel costs, and "some" consumables. And it also noted in its Q1 Conference Call that logistics/supply chain is also improving. For a high-volume operator like Orla, this is certainly positive news, and we continue to see pressure on oil prices which should provide additional help to costs.

Recent Developments

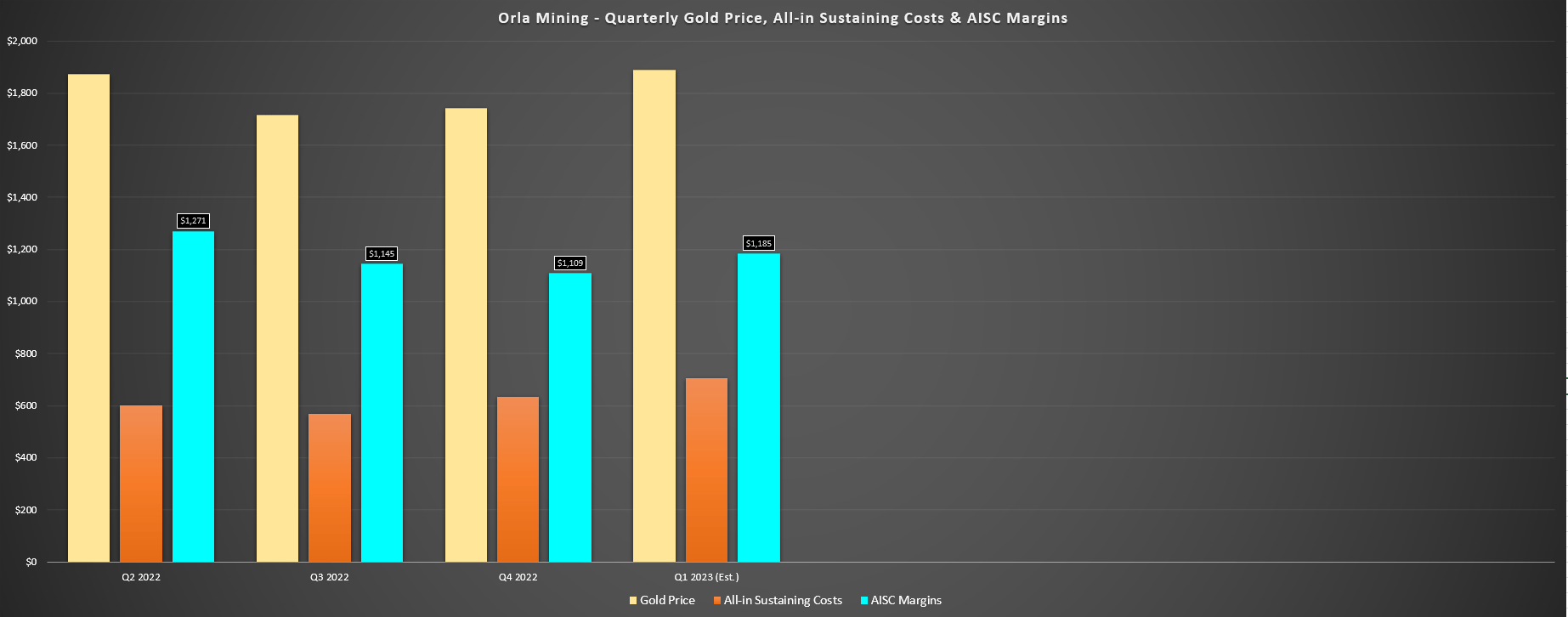

Apart from continued exploration across its portfolio (South Railroad, Camino Rojo Sulphides, and Cerro Quema) the most significant recent development is the gold price, which continues to knock on the door of $2,000/oz and continues to make higher lows. This is because I previously expected Orla Mining to see moderate margin compression on a year-over-year basis at an $1,850/oz gold price assumption, with AISC likely to increase from $611/oz in FY2022 to at least $770/oz in FY2023 even if the company beat its cost guidance midpoint. However, under an assumption of a $1,925/oz gold price for 2023, which looks quite possible, Orla would see minimal margin compression, with the gold price strength offsetting its higher costs this year.

Orla Mining - Quarterly AISC, Gold Price, AISC Margins vs. Q1 2023 Estimates (Company Filings, Author's Chart)

{kind=link}

Assuming costs come in at $770/oz, we would see a 2% decline in AISC margins ($1,155/oz vs. $1,179/oz), well below the 10% margin compression I expected at a more conservative gold price. And if Orla can deliver at the low end of cost guidance ($750/oz), AISC margins would be roughly flat year-over-year using a $1,925/oz gold price assumption. That said, without further upside from the gold price, it looks like Orla's best case is slight margin expansion this year, which certainly pales compared to peers that could see 40-50% increases in margins. And while this is partially because of poor operational performance for some peers relative to Orla's blowout 2022 performance, that could cause some share-price underperformance for Orla vs. more beaten-up names.

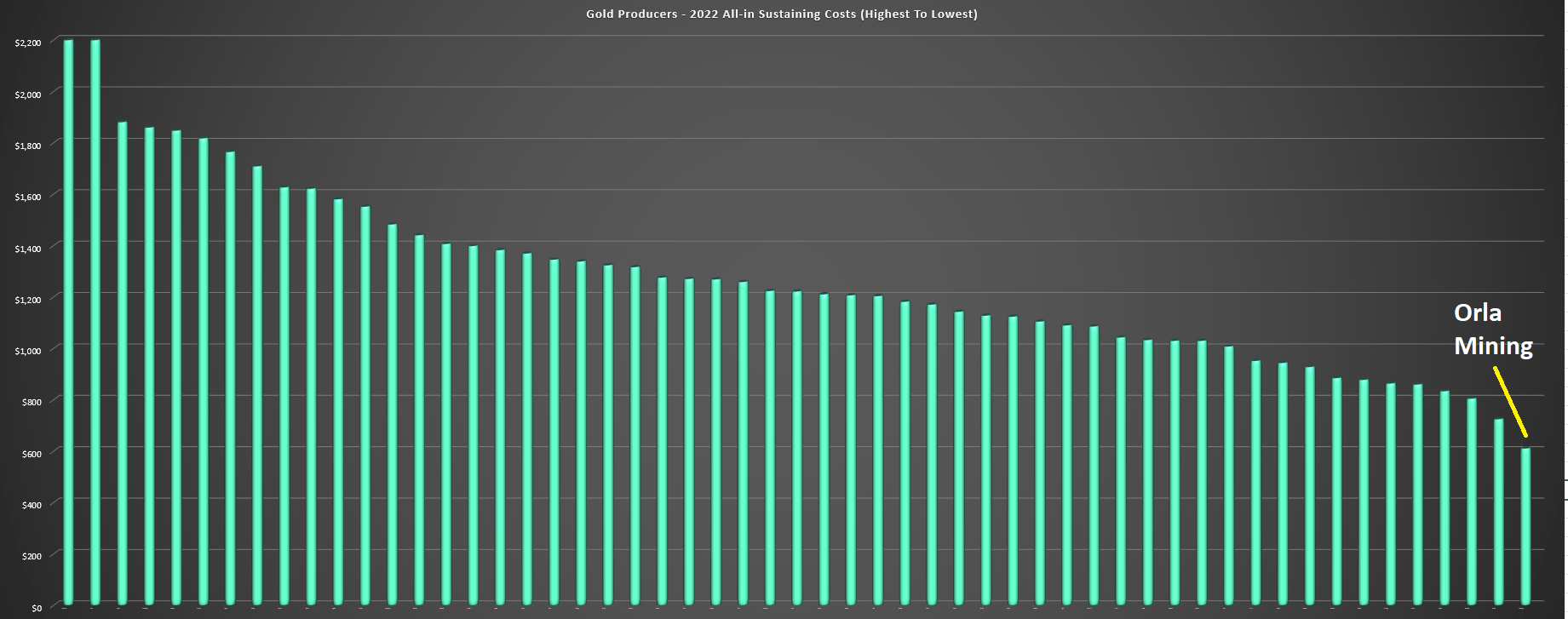

Gold Producers - 2022 AISC Ranked (Company Filings, Author's Chart)

{kind=link}

That said, Orla Mining was the lowest-cost producer in 2022 among the 60+ gold producers I track and should retain its spot as a top-3 producer from a cost standpoint even with higher costs. This is because Fortitude Gold ( FTCO ) has nearly chewed through high-grade Pearl ore, Lundin Gold ( LUGDF ) is also seeing a slight rise in costs, and Capricorn (CMM.ASX) and Evolution are also expected to see costs come in above $900/oz this year. Given Orla's position as being in the top 5% of all miners from a margin standpoint, it can certainly command a premium multiple. Let's see whether this is already priced in, though, by looking at Orla's valuation:

Valuation & Technical Picture

Based on ~347 million fully diluted shares and a share price of US$4.60, Orla trades at a market cap of ~$1.60 billion (enterprise value of ~$1.65 billion). At first glance, this might appear to leave Orla Mining significantly overvalued, with it having one of the steepest valuations compared to others in the 125,000-ounce to 250,000-ounce per annum gold producer space and comparing unfavorably to Victoria Gold ( VITFF ), Argonaut Gold ( ARNGF ), McEwen Mining ( MUX ) and Galiano Gold ( GAU ), with an average market cap of ~$400 million. That said, Orla outclasses these companies from a track record standpoint. Plus, its margins are near unrivaled sector-wide, and it has a portfolio capable of potentially more than tripling production this decade.

However, while Orla deserves a premium multiple for AISC margins well above the peer average (~$1,100/oz vs. ~$600/oz) using a $1,900/oz gold price assumption, the stock isn't cheap, especially when we compare its market cap to an estimated net asset value of ~$2.24 billion. Still, after subtracting out estimated corporate G&A and net debt and applying a P/NAV multiple of 0.90x to adjust for over 80% of NAV coming Tier-2 or Tier-3 jurisdictions (Mexico, Panama), its fair value comes in at ~$1.86 billion, pointing to a fair value of US$5.35. This suggests the potential for further upside from current levels, but the current share price doesn't offer much margin of safety, and certainly not what I'm looking for when starting new positions in small-cap producers.

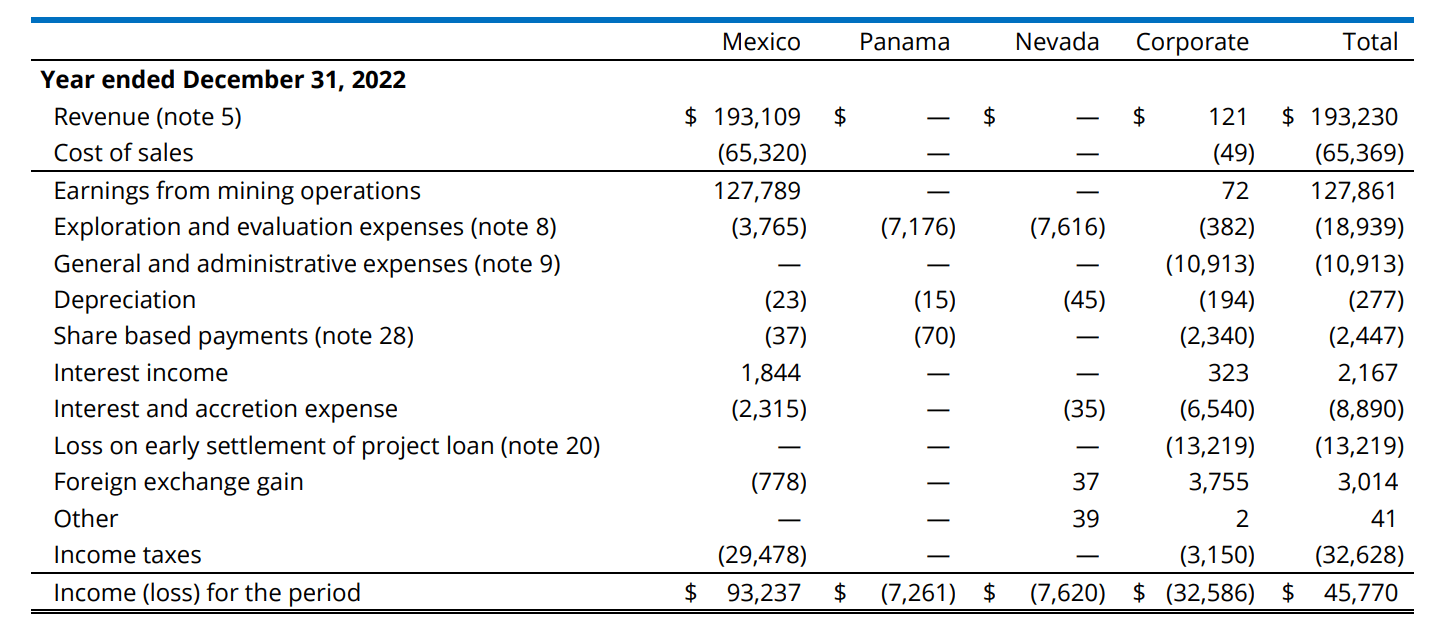

Orla Mining - Income by Segment & Corporate G&A (Company Filings)

{kind=link}

I prefer a minimum 40% discount to fair value for small-cap producers and perhaps a 45% discount is more applicable for companies with the bulk of net asset value tied to Tier-2/Tier-3 jurisdictions. However, even if we use the minimum discount of 40% and apply this to a fair value of US$5.35, Orla's ideal buy zone would come in at US$3.20 or lower, suggesting that the stock would need to decline over 25% to come close to offering a sufficient margin of safety. Obviously, there's no guarantee this occurs, but with the stock trading in the upper portion of its support/resistance range and several other names on sale elsewhere, I don't see the current setup as that interesting from a relative value standpoint.

{kind=link}

Summary

Orla Mining has been one of the best-performing precious metals names over the past year and is one of the few gold producers sitting just shy of all-time highs. And while this outperformance is justified given the company's ability to over-deliver on promises, it's in a uniquely negative setup for 2023 with limited margin expansion vs. a peer group that's set to enjoy significant margin recovery. This results from putting together a blowout year in 2022 and having to lap these tough comparisons, while some producers had kitchen sink years and missed and even those that didn't bomb guidance in 2022 are up against very favorable comparisons.

{kind=link}

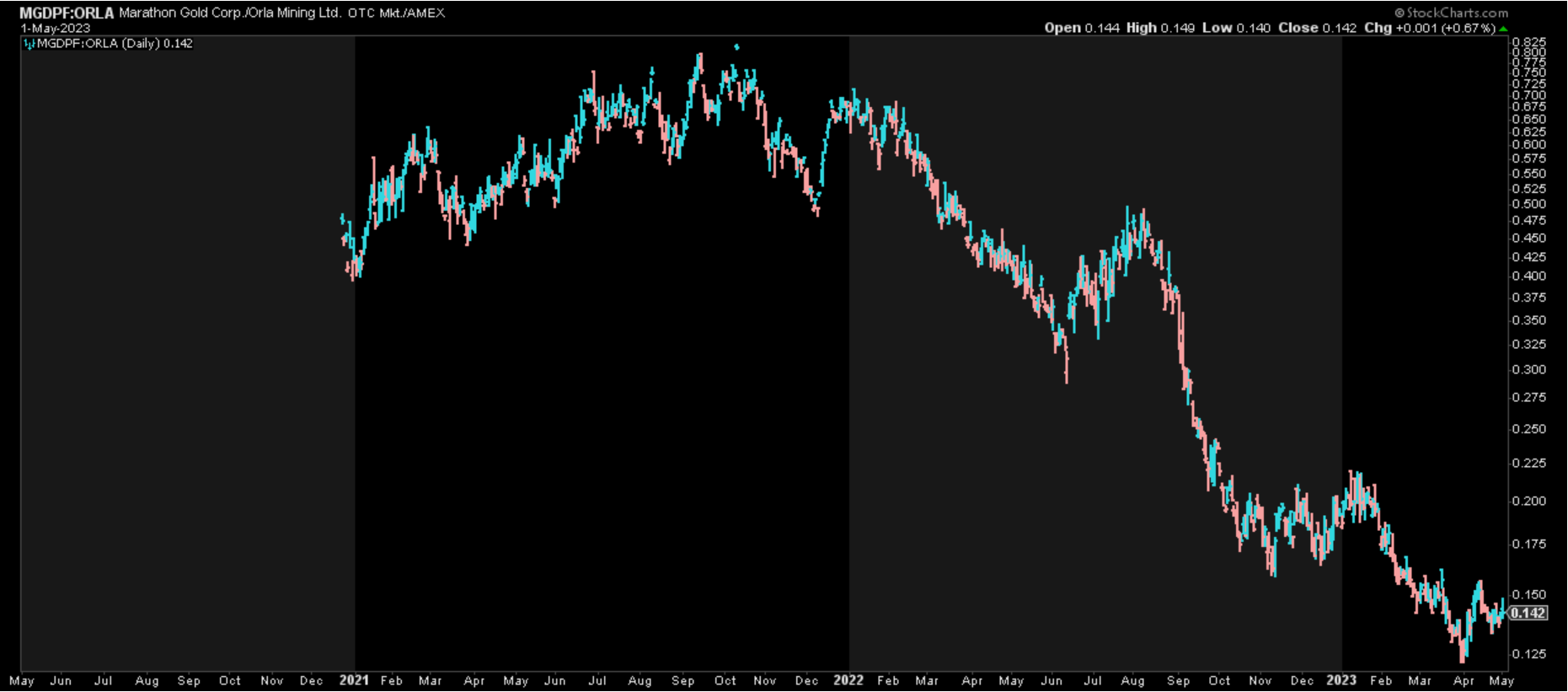

Assuming the gold price continues its ascent, Orla is likely to continue to trend higher, given that a rising tide lifts all boats. That said, with the stock trading up close to fair value, a slight downgrade in Mexico's investment attractiveness following a new set of mining reforms and an unfavorable setup from a margin standpoint relative to peers, I continue to see more attractive bets elsewhere. One name that stands out as being heavily undervalued with sentiment in the gutter is Marathon Gold ( MGDPF ), a company in a similar position to Orla three years ago with it set to graduate to producer status within 18 months and enjoy an upside re-rating if all goes to plan. Hence, if I were looking to put new capital to work, I see this as a more attractive bet.

For further details see:

Orla Mining: Patience Required