CA - Orla Mining: Valuable Mexico Mine And Nevada Project With Little Net Debt

2024-01-17 09:12:06 ET

Summary

- Orla Mining operates a low-cost gold mine in Mexico and is focused on bringing its Nevada project into production soon.

- The Cerro Quema development asset in Panama is facing challenges, but its value has been written down close to zero by investors, potentially creating an opportunity for new share buyers.

- Orla is backed by powerhouse shareholders, including Newmont and Agnico Eagle, with an experienced A+ rated board of directors.

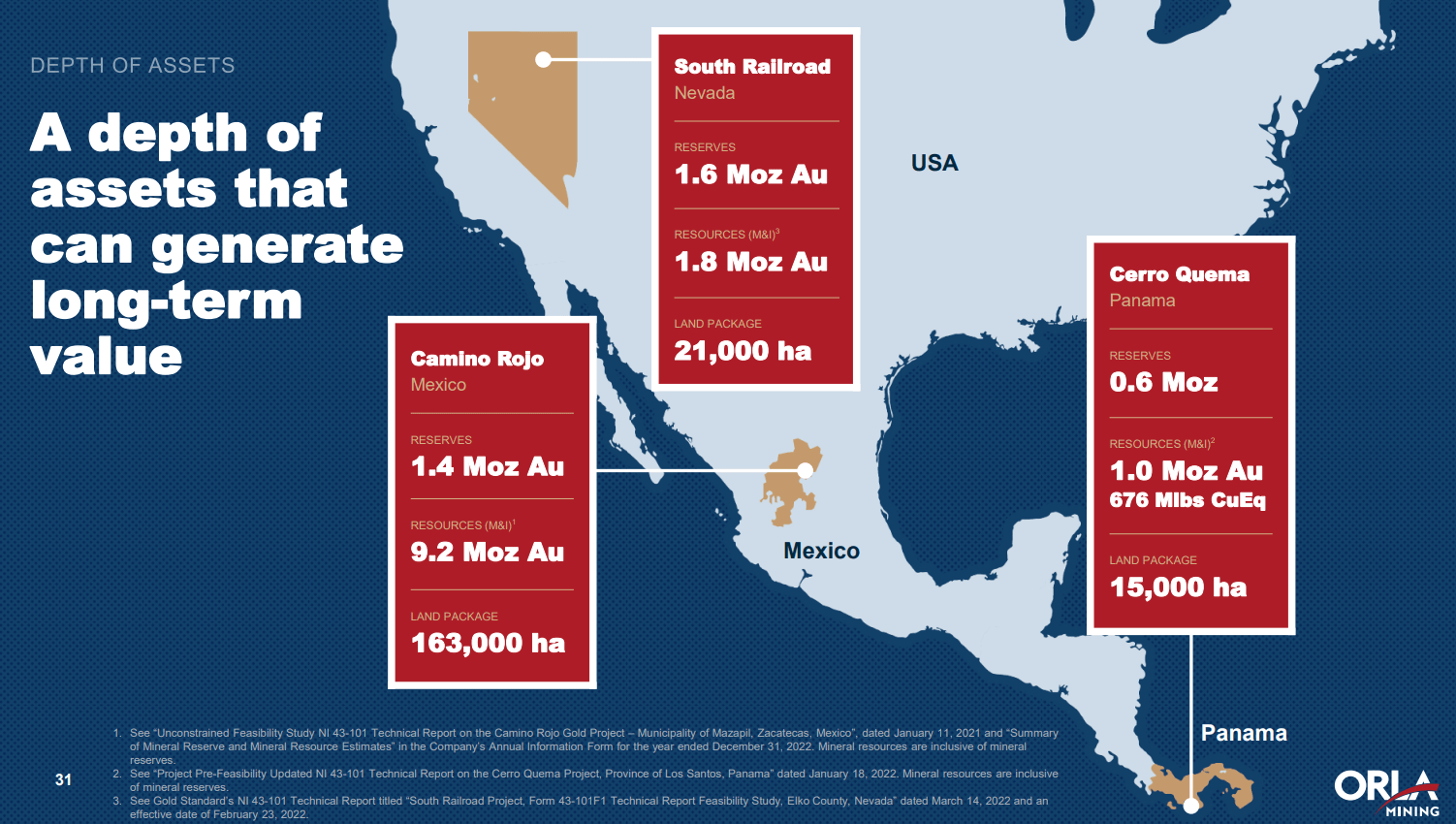

Orla Mining (ORLA) is one of the lowest-cost gold miners you can buy today, with an operating mine in Mexico ( Camino Rojo ) and another project in Nevada ( South Railroad ) finishing the permitting process, before a mine is built. My investment thesis is rising gold prices during 2024-25, alongside increasing production over time, will attract considerable bullish attention to this name.

Orla Mining - December 2023 Investor Presentation Orla Mining - December 2023 Investor Presentation Orla Mining - December 2023 Investor Presentation Orla Mining - December 2023 Investor Presentation Orla Mining - December 2023 Investor Presentation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

A third development project and the original asset for the company is the Cerro Quema resource in Panama. This asset is smallest of the three projects for underlying value and giving investors the biggest headache. With the surprise government-ordered closure of the First Quantum (FQVLF) Cobre Panama copper mine, investors are questioning if Cerro Quema has any worth. So, investors in Orla have run for the exits, assuming Cerro Quema will never be built. The good news is 2023's share price markdown appears to be writing this project's value down to zero, potentially opening a great opportunity to acquire Orla's other assets at better pricing.

Orla Mining - December 2023 Investor Presentation

{kind=link}

And, if the Panama push to end all mining in the country proves a short-lived experiment (some 40,000 direct and indirect jobs may be lost at Cobre Panama), Orla's project might only be delayed a few years, not killed in the end.

Bullish Valuation

The most interesting part of the investment setup for me is 15.6 million ounces of gold have been listed as proven, measured or indicated on all three properties. So, today's $1.05 billion stock market worth and enterprise value (with almost zero in net debt) is backed by roughly $32 billion of inground gold resources, at $3.31 per share and $2040 gold quotes. If you will, Orla investors own gold resources in the ground at prices close to $67 per ounce.

Plus, additional ounces will undoubtedly be discovered on future drilling, given each asset owns/controls vast acreage positions.

Below are some 2023 financial highlights for the company from its December 2023 Investor Presentation . I dare you to find another junior producer with operating performance and balance sheet metrics the same or stronger than Orla.

Orla Mining - December 2023 Investor Presentation

{kind=link}

Below, you can review how the share price decline in 2023 has combined with growth in business fundamentals on expanding production to compress Orla's valuation setup. Price to trailing earnings of 20x, sales of 4.7x, cash flow of 14x, and book value of 2.3x are now well within the parameters of average valuations in the major mining sector, far more constructive than other junior miners.

YCharts - Orla Mining, Fundamental Valuation Stats, Since October 2022

The standout positive is Orla is now generating significant "free" cash flow, after production began in 2022. Most juniors are losing money today, while the majority of majors are reinvesting sliding cash flows into exploration. The 2021-present span of rising labor/energy costs has not mixed well with a relatively stagnant gold price for income and cash flow generation. Out the minor group of gold miners delivering free cash flow currently, Orla is one of the cheapest.

YCharts - Orla Mining vs. Peer Gold Miners/Streamers, Price to Trailing Annual FCF, 6 Months

Technical Trading Turnaround?

The selloff from $5 per share in March 2023 to $2.60 in December looks to be an overreaction to Panama news flow.

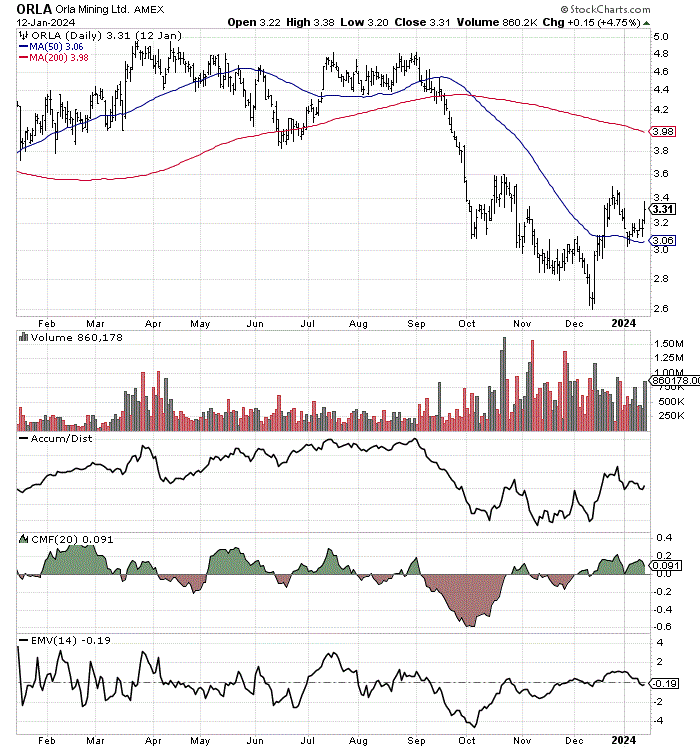

Over the last four weeks, the share price as recaptured its 50-day moving average. In the middle of January, buying appears to be overtaking selling pressure. The best technical momentum setup since July is expressed by action in the Accumulation/Distribution Line , 20-day Chaikin Money Flow and 14-day Ease of Movement calculations. Does this guarantee an advance is approaching for Orla? No, but the overwhelming selling pressure in October and November seems to have run its course.

StockCharts.com - Orla Mining, 12 Months of Daily Price & Volume Changes

{kind=link}

Final Thoughts

Orla is also an interesting choice because it is backed and advised by some powerhouse shareholders as partners. Newmont ( NEM ), the largest gold miner in the world, is Orla's top shareholder with a rough 14% stake. Angico Eagle ( AEM ), one the best-run and smartest gold miners in Canada, holds nearly 9%.

Fairfax Financial Holdings (TSX: FFH:CA ), a leading insurance company in Canada, upped its Orla stake just last week past 10%.

Pierre Lassonde is a 10% owner, perhaps one of the most recognized gold mining personalities alive today. Mr. Lassonde co-founded the first publicly traded gold royalty company, Franco-Nevada ( FNV ). He served as President of Newmont Mining Corp. , now Newmont between February 2002-07. Plus, he was Chairman of the World Gold Council between 2005-09.

Orla Mining - December 2023 Investor Presentation

{kind=link}

For sure, Orla now has an A+ rated (by me) board of directors and management team for industry experience and reputation, much better than the typical junior miner. A former CEO of top Canadian miner Goldcorp (before Newmont's acquisition in 2019), and current high-level employees of Agnico Eagle and Newmont are in place overseeing management decisions. The management team has extensive and successful experience building and running mines at companies such as Goldcorp and Alamos Gold ( AGI ).

Orla Mining - December 2023 Investor Presentation

{kind=link}

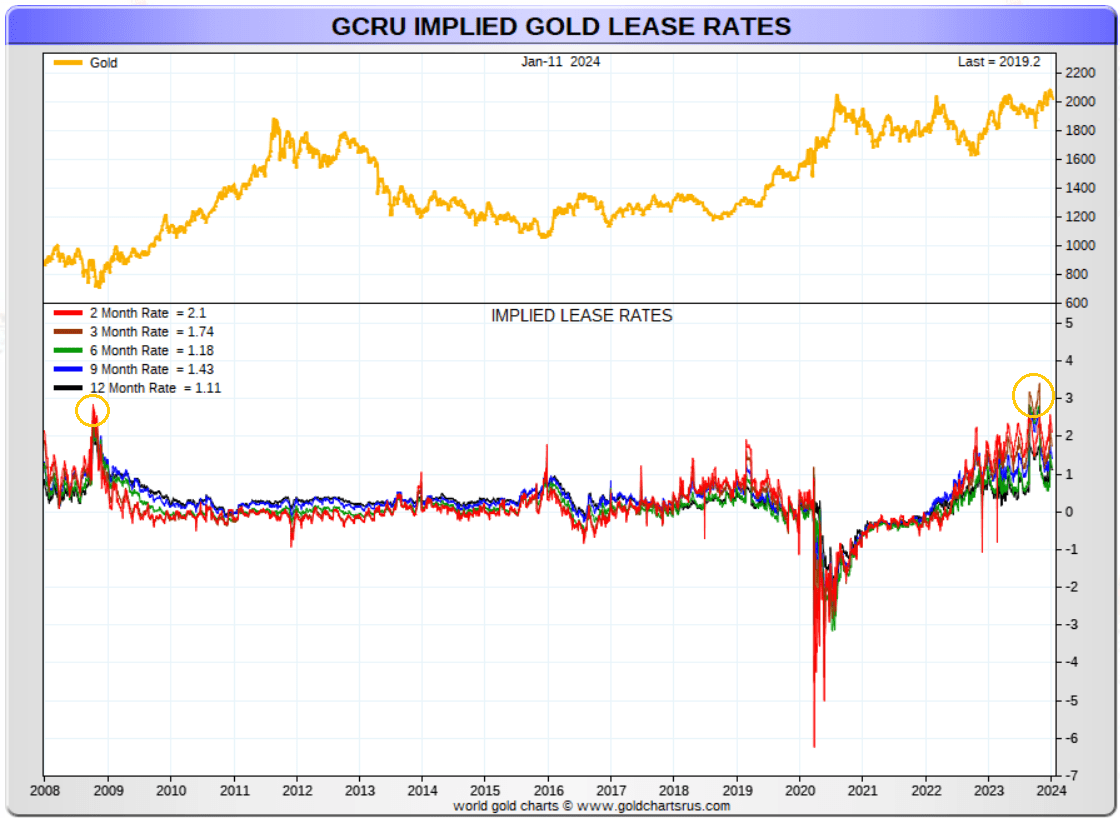

Really, I am finding it difficult to come up with a reason not to own Orla. If my expectation for rising gold/silver prices in 2024 proves correct, a nice drive higher in the share quote may be approaching. The spike in implied gold lease rates (from futures pricing) over the last six months is now screaming at precious metals investors to go long the whole sector. The last time a similarly bullish picture appeared was the important late-2008 bottoming pattern for gold bullion.

GoldChartsRUS.com - Gold, Implied Lease Rates, 16 Years, Author Reference Points

{kind=link}

What kind of upside is possible? That's where the buy argument gets interesting. If the Nevada property becomes a producing mine by 2027-28, I am projecting around 250,000 ounces of gold might become the new company production level yearly, roughly double current run rates. With low AISC of closer to $1,000 per ounce, a $2000 to $3000 price for gold will generate material earnings and cash flow.

$3000 is my current fair-value calculation for gold in early 2024, based on U.S. M2 money supply changes, Treasury debt growth, industry costs of gold production, plus relative pricing to commodities, land, and Wall Street worth readings over the decades (I go back to the late 1960s, just before we left a gold standard for U.S. dollars). As you can see on the graph below, gold's value discount to expanding rates in basic fiat money supply and sovereign debt is getting quite wide historically.

YCharts - Gold Price vs. U.S. M2 and Treasury Debt Growth Changes, Since 1986

Here is my thinking. $2000 gold would equal $500 million in annual Orla revenue and an estimated $150 million in after-tax earnings, on today's $1.05 billion equity market value for the company (2x sales and 7x EPS by 2028).

At $3000 gold, we are talking about $750 million in sales and as high as $300 million for after-tax profits each year in 3-5 years. (1.5x revenue and 3.5x EPS). Of course, this assumes little change in operating costs like labor wages and energy expense, which will undoubtedly climb a little.

Again, these assumptions include no help from its Panama asset. Plus, I am assuming no major new deposit discoveries are made on the large land packages owned at all three locations. If Cerro Quema is allowed to be built, and large "new" gold resources are discovered, Orla will be worth dramatically more than I am forecasting.

For share price targets by the end of 2027 (4 years in the future), given current precious metals quotes, Orla could trade up to $6 (assuming minor new resource discoveries) as currently configured (property acquisitions cannot be ruled out, which could help or hurt shareholder worth), good for investors gains of +15% annualized. I am using 250,000 ounce production numbers, with 4x sales and 12x earnings as appropriate valuation yardsticks, which are low historically for high-margin miners with large resource bases.

At $3000 gold, the reward argument becomes very compelling. Similar valuation ratios to my first target above gets Orla to $10 per share and potential upside of +30% or better annualized into early 2028.

What's the downside risk? Outside of massive changes in Mexico mining laws/regulation or a monster drop in gold under $1700 during 2024-25, I believe downside is very limited from $3 per share. Cash flow should be strong even at $1700 gold prices, the company is net debt-free, and its reserves/resources are not going anywhere. As long as management remains conservative and methodical in its operating decisions, I find it difficult to model the share quote falling below $2 on a sustainable basis. So, we have worst-case risk of a -40% loss vs. best-case upside of +200% over the coming years.

I rate Orla a Buy and own a small position. At this stage, any investment decision should primarily be a function of your bullish or bearish long-term outlook for gold.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Orla Mining: Valuable Mexico Mine And Nevada Project, With Little Net Debt