SHO - Our Pick Of The REITs Blackstone Is Buying

2023-10-28 09:00:00 ET

Summary

- The REIT market presents a historic opportunity.

- Even private equity players like Blackstone are buying REITs.

- We discuss some of Blackstone's current REIT holdings and choose the one we like best.

Recently, I was checking the latest 13F filing of Blackstone Inc. ( BX ) to see what they have been buying lately in the public capital markets.

In case you are not familiar with Blackstone, it is the world's biggest private equity group, managing over $1 trillion of capital, and nearly 60% of that is invested in real estate.

That makes them the biggest landlord in the world. They got to this position by achieving exceptional results for their investors.

Blackstone

So when they talk, we listen, and lately, they have talked a lot about opportunities in the public real estate investment trust ("REIT") market. Last year, they said that:

"The best opportunities today are clearly in the public markets on the screen and that's where we're spending a lot of time."

This isn't surprising given that REITs have been priced at 30-50% discounts relative to the fair value of their assets ever since they crashed in 2022.

Janus & Henderson

Blackstone has since then proceeded to buy out $30+ billion worth of REITs, and earlier this year, they acquired yet another REIT and made the following statement:

"We have nearly $200 billion of dry powder to take advantage of dislocation. With stock markets under pressure, we did agree to privatize two public companies in an otherwise muted deployment quarter... including a logistics REIT in the UK."

These buyouts were executed with funds that Blackstone manages for other investors in exchange for fees.

But the interesting thing is that Blackstone has also bought shares of quite a few REITs with its own capital.

Its biggest recent purchase was Mid-America Apartment Communities, Inc. ( MAA ) .

But Blackstone also owns positions in four other REITs:

- First Industrial Realty Trust ( FR )

- Sunstone Hotel Investors ( SHO )

- Apple Hospitality REIT ( APLE )

- Chatham Lodging Trust ( CLDT )

The investment theses for MAA and FR are already familiar to us. We are invested in Camden Property Trust ( CPT ) and EastGroup Properties ( EGP ), which are fairly similar.

However, I was surprised to see that 3 of their 5 positions are hotel REITs, especially since these are very small REITs with limited liquidity. Typically, Blackstone favors larger REITs because of its liquidity requirements, and so the fact it still went ahead with these investments tells me that they must be really bullish to sacrifice liquidity. CLDT only has a $480 million market cap!

But which one is the most compelling of the three?

- Sunstone Hotel Investors

- Apple Hospitality

- Chatham Lodging Trust

After doing some work on all three companies, I am leaning towards Chatham Lodging Trust and I am now considering including it in our Core Portfolio.

There are two main things that cause it to stand out.

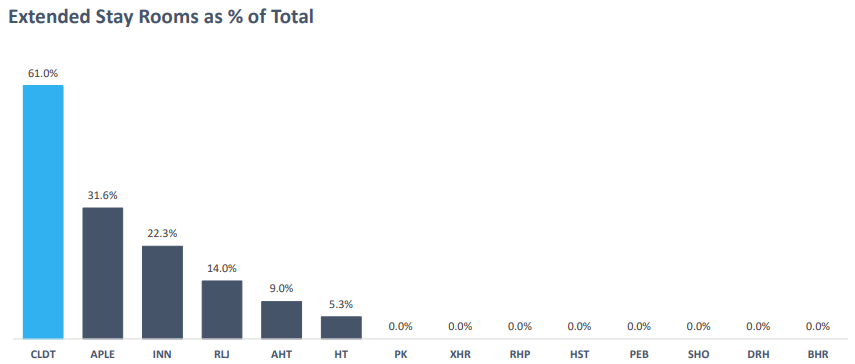

Firstly, it is heavily invested in extended-stay properties, now representing nearly 2/3 of its portfolio:

{kind=link}

{kind=link}

{kind=link}

Blackstone acquired Extended Stay America in a $6 billion deal in 2021, and then later, it also acquired another $1.5 billion worth of extended-stay facilities under the WoodSpring Suites brand in 2022.

So clearly, they have a high conviction in the extended-stay model and it is betting big on it.

Why is that?

Well, extended stay is a bit of a hybrid between traditional hotels and apartments. People stay longer, there are fewer services, and it is a lot cheaper for longer durations. The rooms are also typically larger and include a kitchen to accommodate longer stays.

And over the long run, extended-stay properties should benefit from three major trends:

- The growth of remote work. If you can travel and work remotely, for at least a few weeks or months in a year, then extended-stay properties are the ideal place for you. It is a lot cheaper, you get a kitchen, and a larger room.

- The growth of price-conscious travelers. Extended stay properties are cheaper than regular hotels because there are fewer services (housekeeping once a week), require less staff, and the properties are built very cost-efficiency.

- The huge investments into infrastructure will lead to a lot of demand for extended stay facilities from construction workers. The Infrastructure Investment and Jobs Act, the Inflation Reduction Act, and the CHIPS and Science Act will all bolster new demand for extended stay properties.

So, Blackstone is betting that this property sector will enjoy strong long-term NOI growth, which is today underappreciated by the market, allowing them to buy assets at relatively attractive cap rates of 6-7%.

But here's the thing:

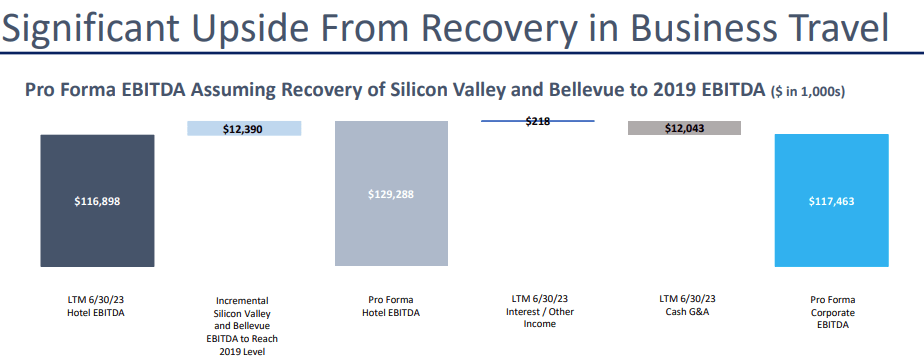

CLDT is priced at an implied cap rate of 9% based on trailing NOI and 10.1% based on proforma NOI assuming a full recovery of its Silicon Valley and Bellevue hotels, where demand is more driven by business travel.

{kind=link}

The management is confident that this recovery will occur as "companies slowly return to the office for at least several days a week, international travel recovers, and intern business returns in 2024 after most companies canceled in 2023."

CLDT's earns 15% of its cash flow from Silicon Valley so the recovery of Tech, the return to the office, and the huge investments into AI should benefit it in the coming years.

The management seems very optimistic, as stated in their Q2 2023 earnings call (emphasis added):

"The good news is we have substantial internal growth upside, as I said, inherent in our existing portfolio, with the ultimate recovery of Silicon Valley and Seattle, as well as the return of the intern business in Austin. If those hotels reached 2019 RevPAR in 2024, that would generate incremental portfolio RevPAR growth of approximately 7% and incremental FFO per share growth of $0.32. If you include the Austin intern business, that will add another 50 basis points to RevPAR and FFO per share of another $0.02.

So including all those hotels -- those seven, if you use current consensus estimates for 2023 adjusted FFO per share would increase almost $0.34 per share, which alone would represent an almost 30% increase. That certainly is substantial upside as you look at our company and look forward.

We continue to pursue external growth opportunities, though we must of course be mindful of our cost of capital while assessing in place cash flow yield and growth projections on potential acquisitions... With 39 hotels, we can acquire one or two hotels, and it significantly moves the needle with respect to EBITDA and FFO growth. "

But despite that, it is today priced at an exceptionally low valuation:

| CLDT |

| NAV discount |

| ~40% |

| Implied cap rate based on trailing NOI |

| 9% |

| Implied cap rate based on forward NOI |

| 10.1% |

| P/FFO |

| 8.4x |

| Pro-forma P/FFO |

| 7x |

Why is it then priced at such a low valuation if it owns such compelling assets?

There are 3 main reasons:

Firstly, its recovery recently got delayed after the intern business was mostly canceled in 2023 and interns are a big business for extended stay facilities. This is likely one of the main reasons why its share price has dropped a lot more than that of its peers this year:

YCHARTS

Secondly, CLDT is only paying a tiny dividend right now, and it is likely reducing the investor pool that would be interested in this REIT. It is intentionally retaining most of its cash flow to pay off debt and address maturities. Debt is expensive these days and so CLDT prefers to pay it off, despite only having a 4x Debt-to-EBITDA, which is quite reasonable.

Here is what they said in the most recent quarter:

"With good flow through, we were able to generate corporate level cash flow before CapEx and common dividends of $22.25 million up approximately 10% over last year. With the excess cash-flow we were able to repay a $20 million maturing mortgage. With only $70 million of maturity mortgages between now and June 2024 we're in an excellent position to address all remaining maturities this year and next year."

Finally, CLDT is a tiny REIT with a $450 million market cap, further reducing its potential investor pool. I am very surprised that Blackstone would even invest in this REIT given its tiny size, and this just goes to show that they must be very bullish on it.

Risks & Takeaway

We currently do not own any hotel REITs, but we have now placed Chatham Lodging Trust high on our watchlist. The fact that even Blackstone is buying it is very encouraging.

Even then, we are not yet ready to invest because we are not done studying the potential risk of increased competition coming from an Airbnb-like platform.

If you have any thoughts on this risk, please let us in the comment section.

Blackstone clearly does not seem to be concerned, but I know from my previous trips, that I tend to check on Airbnb for options whenever I am staying in a place for longer than 2 weeks.

Therefore, it would seem that extended-stay properties would face growing competition from Airbnb and other similar platforms.

At the same time, I recognize that extended stays are somewhat different as they are commonly rented for 1-6 months at a time - so quite a bit longer than typical offerings on Airbnb. Moreover, the customers of extended stays are often major companies that are temporarily housing some of their workforce. Finally, Airbnb is a bit of a hit-and-miss since the quality can vary significantly, the prices can be high, and expectations are not always met.

Even then, I am having a hard time figuring out how big of a risk this really is. As I finalize my due diligence, I will then decide if we want to initiate a position or not.

Also, note that I met the company's CEO earlier this year in Miami and there is a short video of it on YouTube (skip to 7:10 section). Already back then, he thought that the share price was way too low and it has dropped further since then. Insiders, including himself, have bought quite a bit of shares this year:

{kind=link}

For further details see:

Our Pick Of The REITs Blackstone Is Buying