OUST - Ouster Is The Best Lidar Pick - 2023 Edition

2023-05-15 20:46:07 ET

Summary

- Velodyne's acquisition synergies are on the way, Motional agreement extension.

- $33M in bookings, company beats on estimates of revenue, guides the highest revenue in history for Q2.

- Ouster's valuation warrants a strong buy recommendation.

Q1 Results

A few positive developments occurred in Ouster ( OUST ) communications during Q1. Firstly, the company exceeded its guidance, surpassing the lower range of expectations. Secondly, the news release regarding the Motional extension before the results for the quarter were announced was a pleasant surprise. It would have been even better if the news had been published before the market opening, allowing investors the time to appreciate its value entirely. Nevertheless, Ouster has done an excellent job of changing the narrative from the muted conclusion of the previous quarter (Q4).

With revenues of $17.3M, Ouster delivered the highest revenue among Western-based lidar companies. It is projected to generate $18 to $20M in revenue for the second quarter. Furthermore, Ouster closed the quarter with $257M in cash.

Estimating the company's burn rate is still challenging. However, excluding the apparent charges from $53M spent on operations, namely restructuring and merger fees, the confirmed annual reduction of $50M suggests a cash burn of approximately $33.7M or possibly less per quarter. Moreover, the company recognized additional opportunities, leading to a total synergy benefit of $85M or a further reduction of $30 to $35M annually. Based on my estimation, this would bring the yearly cash burn down to $100M to $105M. The confirmation and final run rate will be provided in the third quarter.

A negative gross margin of 2%, including one-time charges totaling $3.6M in that calculation, masked the potential for a 25% gross margin if these charges were excluded. Looking ahead to the second quarter, it is anticipated that there will be additional charges, estimated to be at least $3M. However, by the third quarter, the company expects a comprehensive understanding of its costs, benefiting from healthy revenue opportunities unaffected by the merger costs and taking full advantage of synergies.

In terms of overall performance, the company announced $33M in bookings for the quarter, marking the highest figure in its history. A significant improvement compared to the Q4 announcement of $70M for 2022. The second part of the year is expected to achieve strong results.

The company experienced a significant decline in its valuation following the completion of the merger and the subsequent reverse split process. After the reverse split, the company's stock reached $3.21 per share, resulting in a market capitalization of $124M, a significant decrease compared to the $19 per share valuation observed in February.

Valuation

Following the quarterly update, OUST stock responded positively, leading to a market capitalization of $192M or $4.94 per share. Despite this reaction, the company remains significantly undervalued compared to other lidar companies that generate similar revenue.

Using the current market capitalization, I calculated a few metrics to illustrate that situation. The consensus on Ouster's revenue sees an estimate for 2023 of approximately $87M. It implies around $50M in revenue for the latter part of the year, with a projected gross margin of 25% to produce a gross profit of $12.5M.

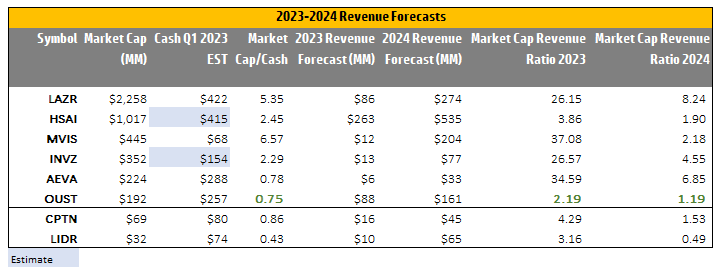

Among companies with comparable or higher revenues than Ouster, only two can be a basis for comparison: Luminar ( LAZR ) and Hesai ( HSAI ). According to Yahoo's analysis, Luminar is expected to bring in an average of $86M in revenue for 2023, while Hesai is projected to generate $263.9M. The table below provides an overview of market capitalization, cash levels, and revenue expectations for 2023 and 2024 for the entire sector.

Based on the revenue expectations for 2024, Ouster ranks slightly above AEye ( LIDR ).

AEye, based on its quarterly results, has gone into hibernation, waiting for Continental ( OTCPK:CTTAF ) to start selling its licensed lidar to OEMs sometime in 2024. Therefore, AEye is not considered an investable option at this or any other stage. Ouster ranking just above AEye is a significant market error and presents an excellent investment opportunity.

{kind=link}

2023-2024 Revenue Forecasts (Yahoo Analysis - Financial Statements - Author)

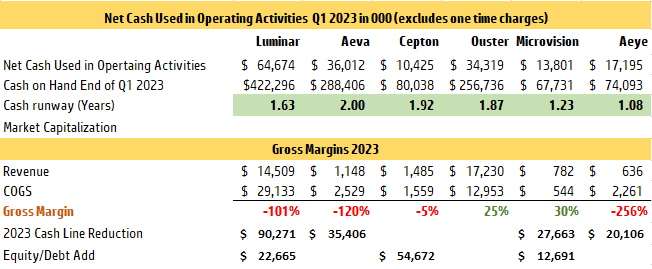

The cash level situation aligns similarly, which is crucial in determining the cash runway. I have excluded one-time costs related to restructuring and the merger to showcase the normalized burn rate. As mentioned earlier, management has indicated that there is an additional opportunity to further reduce the yearly burn rate by $30 to $35M. Additionally, as the company regains a 25% gross margin, it will improve its cash situation by leveraging gross profit to offset operating expenses. The table below shows that Ouster has a longer runway for cash than Luminar and has a better outcome with revenues and gross margins than Aeva ( AEVA ) and Cepton ( CPTN ), making it a strong candidate for survival.

{kind=link}

Net Cash Used in Operating Activities Q1 2023 (Companies' Financial Statements - Author)

In terms of financing or need for equity sale, both MicroVision ( MVIS ) and Luminar sold equity during Q1. Luminar utilized its dedicated acquisition filing, while MicroVision opted for an ATM (At-The-Market) offering. At this stage, it is evident that Ouster does not need to explore equity sales or resort to an ATM, particularly given the currently low price levels. In my opinion, even at $10 per share, which would result in a market capitalization of $388M, Ouster is potentially only aligning itself with the valuations of other companies. Still, in my view, that price remains a very conservative fraction of the potential.

Technology

During the call , the company provided updates on developing its two products. Specifically, the OS sensors operate as the REV7 version using the L3 chip. Plans are underway to tape the new chip, L4, by the end of this year. Additionally, the CEO mentioned the future generations of the spinning lidar product, REV8, and REV9, are being considered. The REV7 sensors have received positive reviews and excitement from customers and significantly contributed to the company's bottom line. Their average selling prices have driven Q1 results, with unit prices increasing by approximately 54% on average from Q4 for 3000 sensors sold in the current quarter.

Ouster intends to continue supporting Velodyne pucks, particularly the one selected for the long-range lidar exclusive to the Motional deal. These analog products will become a focus of manufacturing efficiency to fulfill contractual obligations rather than further development. At the same time, I expect Ouster to transition its business partners and customers from analog to digital technology.

The discussion then turned to DF (Digital Flash) and its potential. The early sample B, scheduled to be available later this year, will be equipped with a Chronos chip in early 2024; the B samples will offer the final form factor.

Like Aeva, Ouster's DF strategic partner has not yet been named. Such an announcement would have a beneficial outcome on the share price.

Conclusion

Ouster is deeply undervalued, making it an excellent opportunity for long-term investors to continue to average down or establish a long-term position. The lidar market is still in its infancy, and Ouster is well-positioned to benefit from its growth. Despite the high market capitalization and valuations of other lidar companies with minimal revenues and negative margins, Ouster's approach remains underrated by Wall Street.

Based on Ouster's strategy, I highly recommend it as a strong buy due to its revenue potential, cost reduction, and extended cash runway. Luminar is the closest company to offering similar revenue opportunities. Still, it operates at ten times the value of Ouster, has negative equity, significant convertible debt, and a lot of demand and gross margin risk. Luminar is fully valued at over $2.2B, making it less attractive.

On the other hand, Hesai, a Chinese entity, is not investable based on this condition and limited opportunity to match valuations offered to Western companies. Ouster also has an ongoing federal infringement case and investigation initiated by the ITC against Hesai. I certainly place my bet on the side of Ouster, expecting a positive outcome for the company in those proceedings.

For further details see:

Ouster Is The Best Lidar Pick - 2023 Edition