CA - Out-Of-Favor Enbridge Shares Are A Buy (Rating Upgrade)

2023-10-18 19:28:39 ET

Summary

- Enbridge Inc. shares have sold off his year even though fundamentals have not deteriorated.

- It recently announced an attractive acquisition of Dominion assets and has reined in leverage.

- The shares offer significant appreciation potential, a secure 8% yield, and the prospect of dividend increases.

Note to readers: Dollar references in the article are to Canadian dollars.

Enbridge Inc. ( ENB ) shares have finally fallen out of favor of late, along with the entire Canadian midstream cohort. They have steadily sold off throughout the year and are now down 17.0%. At their current level, ENB's EV/EBITDA valuation has fallen to the lows of 2020, when the future prospects of the North American oil patch were cast into doubt.

Investors previously granted ENB a halo due to its quasi-monopoly position in Western Canadian Sedimentary Basin egress via its Mainline system. However, the reality is that the regulated price-setting mechanism eliminates any sustainably high return on capital earned from its dominant market position. In fact, in recent years, ENB’s average return on capital has only slightly exceeded its cost of debt.

{kind=link}

ENB’s persistently low return on capital, its routine outspending of internally generated cash flow, and its stock's lofty valuation have been our primary reasons for disliking ENB equity. They’re the reasons why we’ve rated its shares as a Hold since initiating coverage in 2021. But since a stock's investment merits must be considered with reference to its market price, we believe ENB's selloff has gone far enough to create a buying opportunity. We're therefore upgrading ENB’s stock to a Buy.

The Positives: ENB's Cash Flow Stability and Recent Acquisition

ENB is the largest midstream operator in North America. Its operations are focused primarily on liquids and until recently the company has focused its expansion on its U.S. Gulf Coast facilities. These investments likely offer more attractive returns on capital than ENB's Canadian investments, so we viewed them as a smart use of capital.

More recently, however, new management under Greg Ebel has changed course. On September 5, ENB announced its deal to acquire three utility assets from Dominion Energy ( D ). The company's move away from liquid midstream operations initially caught observers by surprise, but the market’s reception turned more positive as analysts digested the deal. Despite the overwhelming support for the deal, however, ENB’s stock continued to fall after the announcement.

We like the deal. For one, it provides relatively attractive returns on capital, which ENB will need as it confronts a higher interest rate environment. The market values the acquired assets’ cash flows at a slightly higher multiple than ENB’s historical valuation. The company can therefore deploy large sums of capital at attractive returns relative to its legacy assets, and its investments are likely to be well-received by the market. U.S. utility assets will allow ENB to deploy large sums of capital, which will help it move the needle with regard to long-term EBITDA growth. While the deal has yet to close, we believe the Dominion assets are a net positive addition to ENB’s existing system.

ENB’s Constructive Fundamental Trends

Even though sentiment toward Canadian midstream is in the dumps, company fundamentals have been stable—and in some cases have improved—over the past few quarters. ENB offers a case in point.

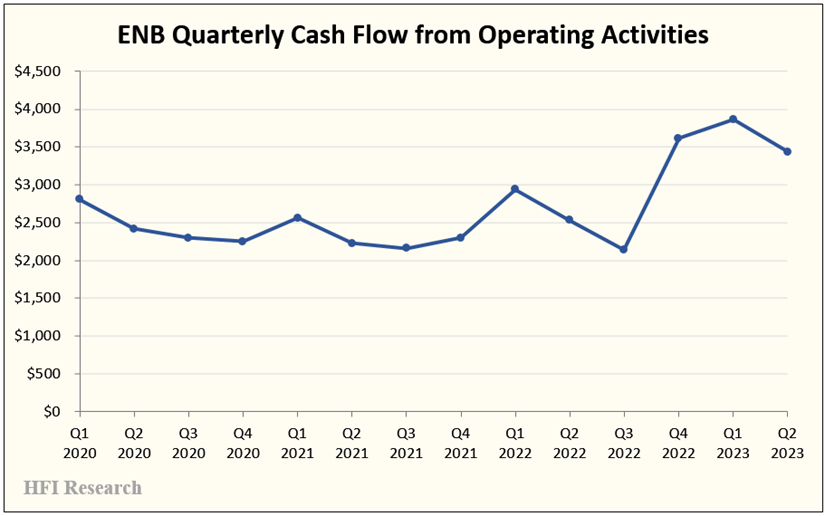

First off, its cash flow has been stable. What the company has sacrificed in terms of its return on capital, it has gained in terms of cash flow stability, as demonstrated by its operating cash flow below.

{kind=link}

ENB’s cash flows will also remain largely insulated from the impact of inflation. ENB investors can rest assured that operating cash flow will remain supported in nearly any macro oil market or economic scenario.

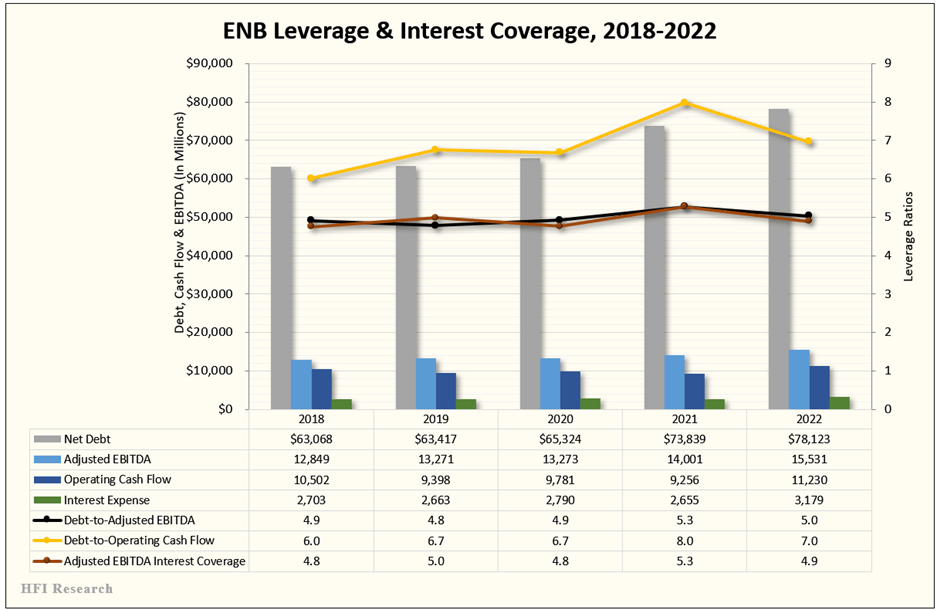

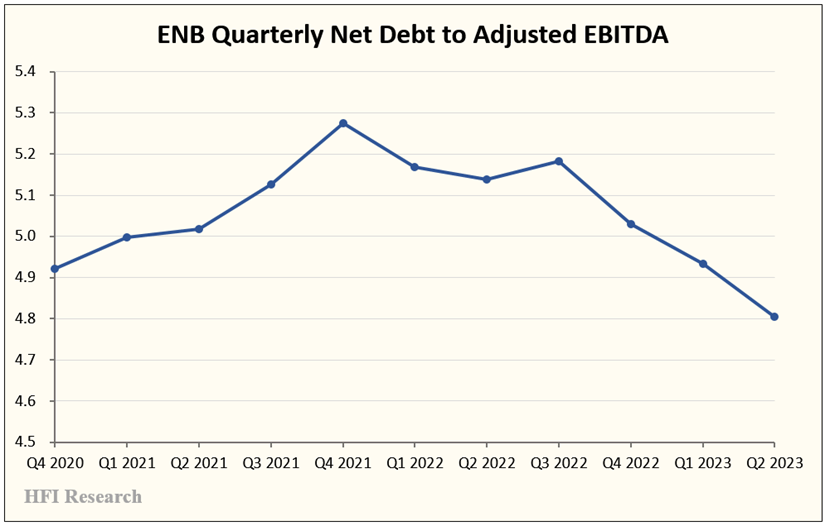

ENB’s stable cash flow can support a large debt level, which has caused debt to grow at a rapid clip. For the most part, EBITDA growth went hand-in-hand with growing debt balances, but by 2021, ENB’s leverage ratio increased significantly above 5-times, verging on an uncomfortably high level.

{kind=link}

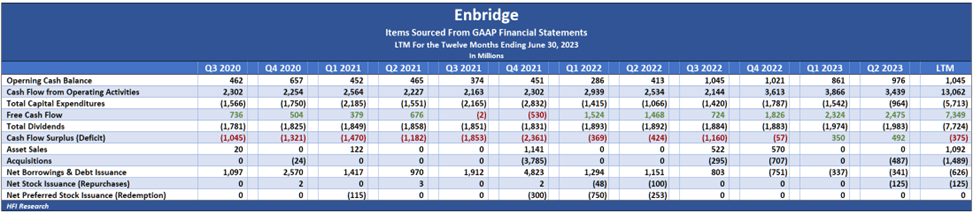

However, ENB’s leverage situation is changing for the better. By far, the most significant recent development for its shareholders over recent quarters has been the company’s inflection from net consumer of cash flow to generating a cash flow surplus. This means it has internally funded its expenses, growth capex, and dividends without the need to raise debt. The following table shows ENB’s cash flows since 2020 and how they’ve improved in 2023.

{kind=link}

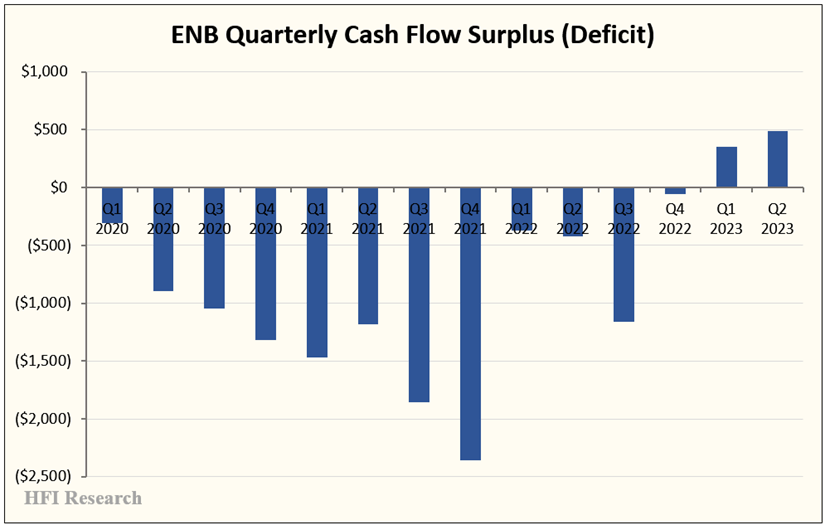

The chart below shows the company’s cash flow deficit inflecting to a surplus in the first and second quarters.

{kind=link}

If continued, this cash flow inflection should be a game changer for ENB shareholders. Companies like ENB, which generate low returns on capital, cannot continue to spend forever on new growth projects and fund those projects with long-term debt, particularly when the cost of debt is rising as it is today. Instead, they should pare back their growth capex—which in recent years has run at ludicrously high levels for ENB—and use excess cash flow to pay down debt. Without a growing debt balance, new projects set to come online over the coming quarters and years can increase Adjusted EBITDA and lower the leverage ratio to comfortable levels for shareholders.

ENB’s cash flow surplus demonstrates management’s commitment to reining in leverage. The chart below shows the recent progress in doing so and illustrates how swiftly leverage metrics can improve for a prodigious generator of cash flow like ENB.

{kind=link}

Management targets a leverage ratio of 4.5 to 5.0-times, so ENB is back in the clear with regard to leverage. What's clear is that ENB’s current leverage ratio should not have caused its stock’s recent selloff. Given how management plans to finance the Dominion asset acquisition, we don’t expect the deal to significantly add to ENB’s leverage.

The other positive development for ENB shareholders has been the new management’s tack toward returning excess cash flow to shareholders in the form of share repurchases. If the company is in fact inflecting to a sustainable cash flow surplus, shareholders will want to be sure that uninvested excess cash is delivered back to them in an intelligent manner. At the moment, with ENB shares being valued at multi-year lows amid stable or improving fundamentals, share repurchases offer a particularly attractive alternative.

In the first half of 2023, ENB spent its excess cash on asset acquisitions, but the Dominion utility acquisition will likely be the last one for some time. ENB also spent on share repurchases, which is more constructive for shareholders. At the very least, it shows the new management’s intent to allocate capital intelligently for shareholders.

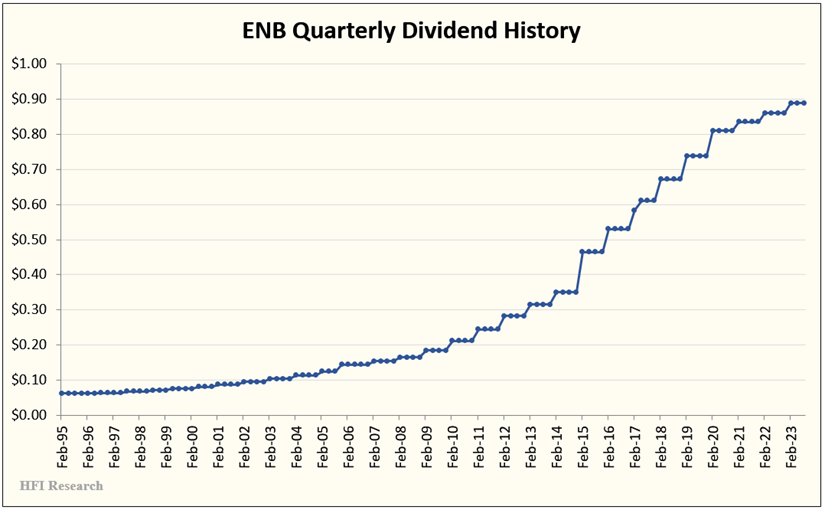

We also expect ENB’s excess cash flow to be delivered to shareholders through increased dividends, continuing ENB’s impressive long-term track record, as shown below.

{kind=link}

Valuation

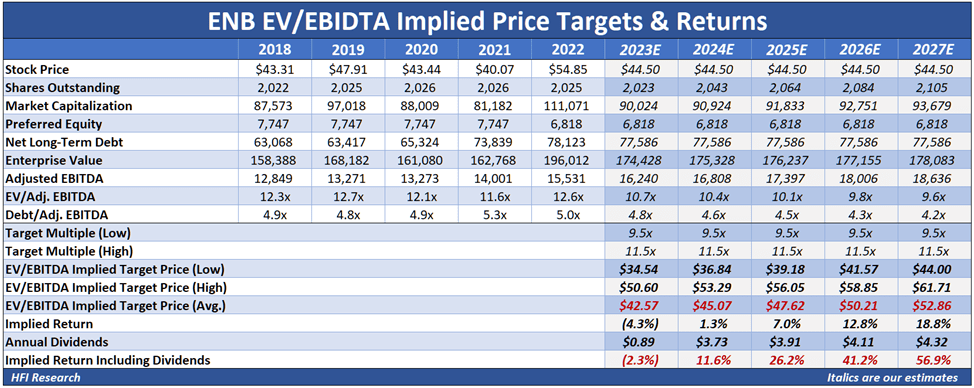

Our ENB valuation implies little downside risk and significant total return upside from the current price of $44.50. With regard to appreciation potential, the shares possess 21.3% upside to our price target of $54.00.

Our EV/EBITDA valuation implies that the shares offer 11.6% total return upside through next year, which increases to 56.9% by 2027.

{kind=link}

Dividends comprise a large portion of the total return, and we believe ENB’s safe and large 8.1% yield is particularly attractive.

Our valuation doesn’t account for the Dominion asset acquisition. We expect the transaction to add to ENB’s intrinsic value over time. As such, we believe our valuation excluding the assets is more conservative.

Our valuation is also conservative due to its 10.5-times EV/EBITDA multiple. ENB has traded at a multiple closer to 11.5 in recent years, so a reversion to a higher trading multiple would result in additional upside for the shares.

Conclusion

It’s taken a while for us to come around to Enbridge Inc. shares, but the recent selloff has done the trick. We recommend the shares for conservative investors, as the large dividend yield should be safe and substantially shielded from the impact of inflation. Income investors should make the contrarian move and buy out-of-favor ENB shares for the long term.

For further details see:

Out-Of-Favor Enbridge Shares Are A Buy (Rating Upgrade)