CA - Ovintiv Maintains Enhanced Prospects With Strong Assets And Core Midland Acquisition

2023-07-24 18:22:52 ET

Summary

- Ovintiv, formerly Encana, is currently undervalued by ~22%, according to a weighted average between my projected NPV and Alpha Spread's relative valuation.

- Despite superior growth metrics, the company has experienced poor price action, likely due to a drop in natural gas spot prices and lower oil prices; however, a potential commodities upswing and the firm's scalability could drive growth.

- With scalable investments across the core midland Permian Basin and margin-expanding efficiencies built-in, I seek to rate Ovintiv a 'buy'

Ovintiv ( OVV ), known before its restructuring as Encana, is a multinational independent petroleum and gas company with assets spread across Canada and the Southwest US. The firm currently operates through three principal verticals; Oil & Condensates, Natural Gas Liquids, and Natural Gas.

{kind=link}

Through its activities, Ovintiv has achieved Q1 revenues of $2.61bn- a 23.82% YoY decline- alongside a net income of $487.00mn- a 302.07% increase- and a free cash flow of $446.00mn- a 90.60% increase driven by rising operational and financing free cash flow.

Introduction

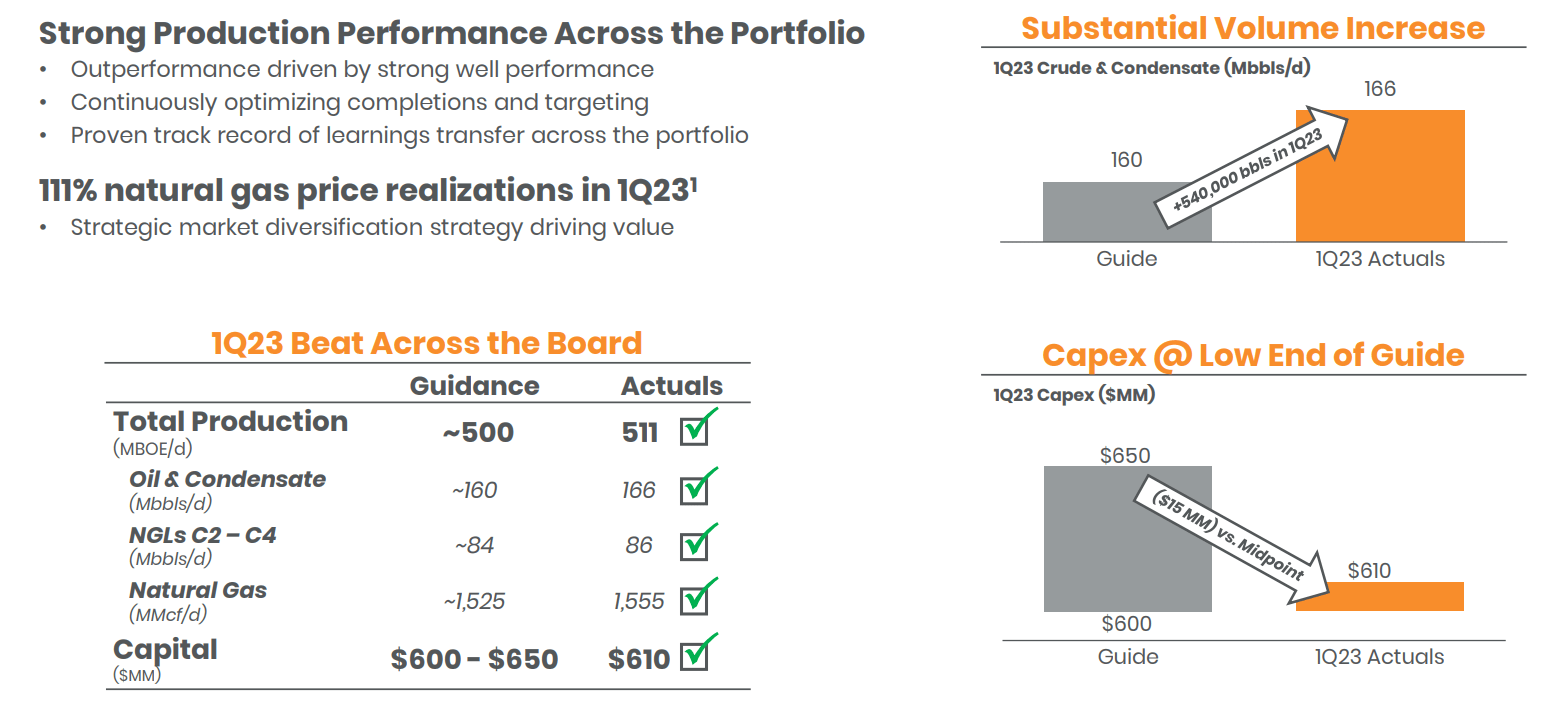

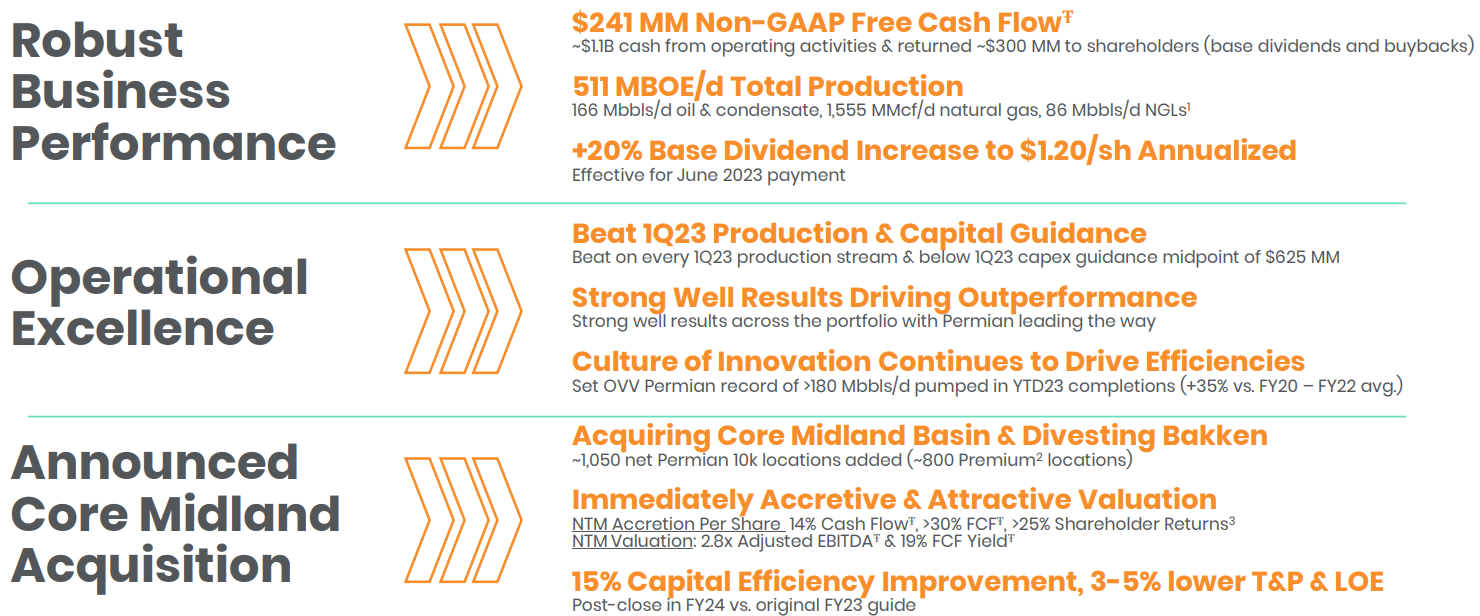

At the core of Ovintiv's operations remains its three primary objectives; persistently robust financial and business performance, operational and capital deployment excellence, and aggressive, synergistic scale expansion, through organic and inorganic modes. In Q1'23, Ovintiv has worked towards these goals through record free cash flows and >$300mn in shareholder returns, alongside Q1'23 production beats and the landmark acquisition of core midland basin assets.

{kind=link}

These broad-based objectives are supported by Ovintiv's strategic objectives, encompassing a diversified, high-quality asset portfolio, efficient and low-cost operations, multi-product commodity exposure as a yield-enhancing and resilience measure, and a superior premium inventory expansion.

{kind=link}

The combined accretive effects of Ovintiv's compelling portfolio, as well as its expansion efforts work alongside macro tailwinds and the firm's moderate undervaluation, leading me to rate Ovintiv a 'buy'.

Valuation & Financials

General Overview

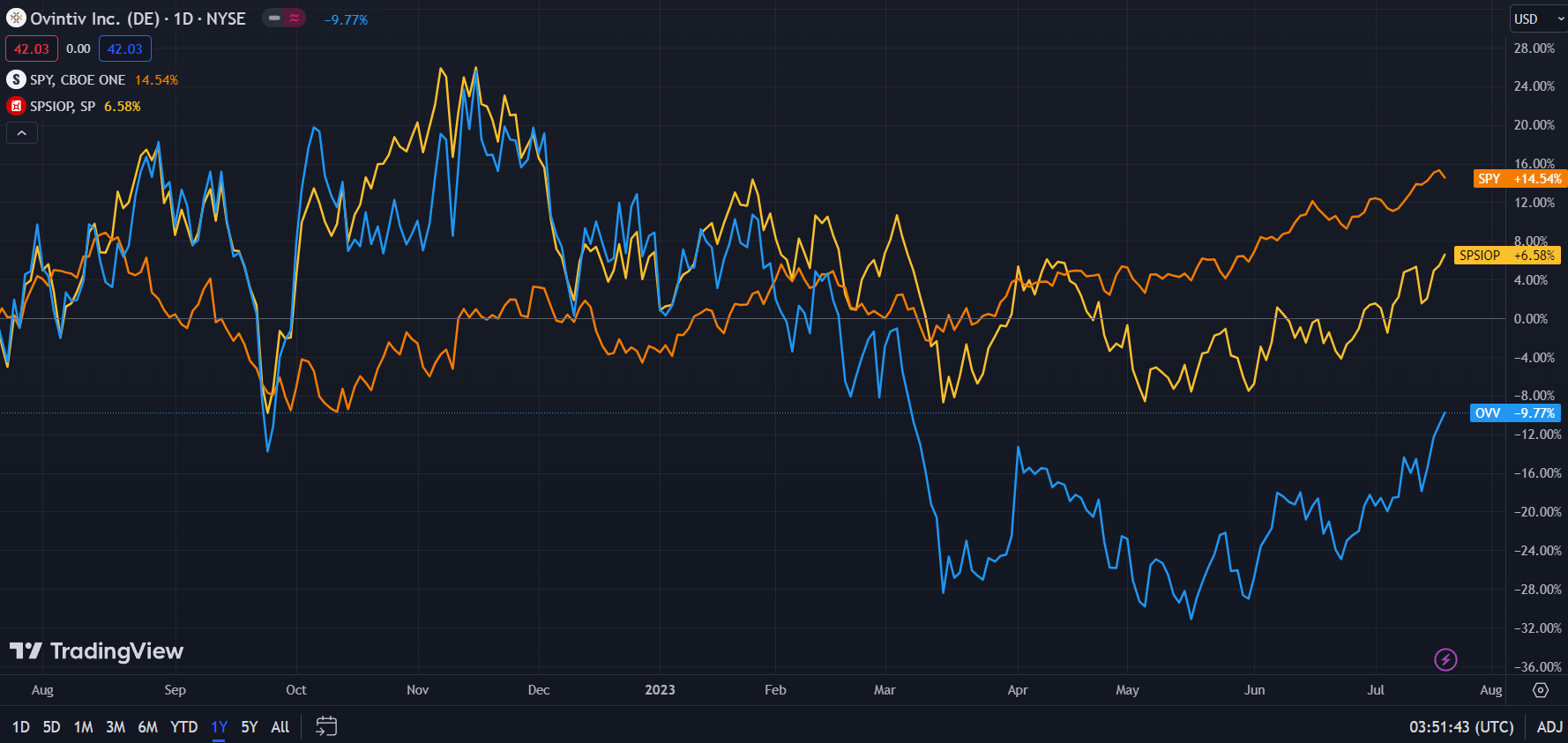

In the TTM period, Ovintiv- down 9.77%- has experienced poorer price action to both the oil and gas industry (SPIOP)- up 6.58%- and the broad market as represented by the S&P500 ( SPY )- up 14.54%.

Ovintiv (Dark Blue) vs Industry & Market (TradingView)

{kind=link}

Ovintiv's general underperformance is likely due to a drop in natural gas spot prices, with a milder winter and warmer spring priced in, alongside lower oil prices. Unlike the oil and gas industry, Ovintiv, as an upstream component, was not as insulated against fossil fuel prices, especially with a lack of hedge trading activity.

However, I believe, with a potential commodities upswing in the cards, and Ovintiv's scalability, the firm has growth built in.

Comparable Companies

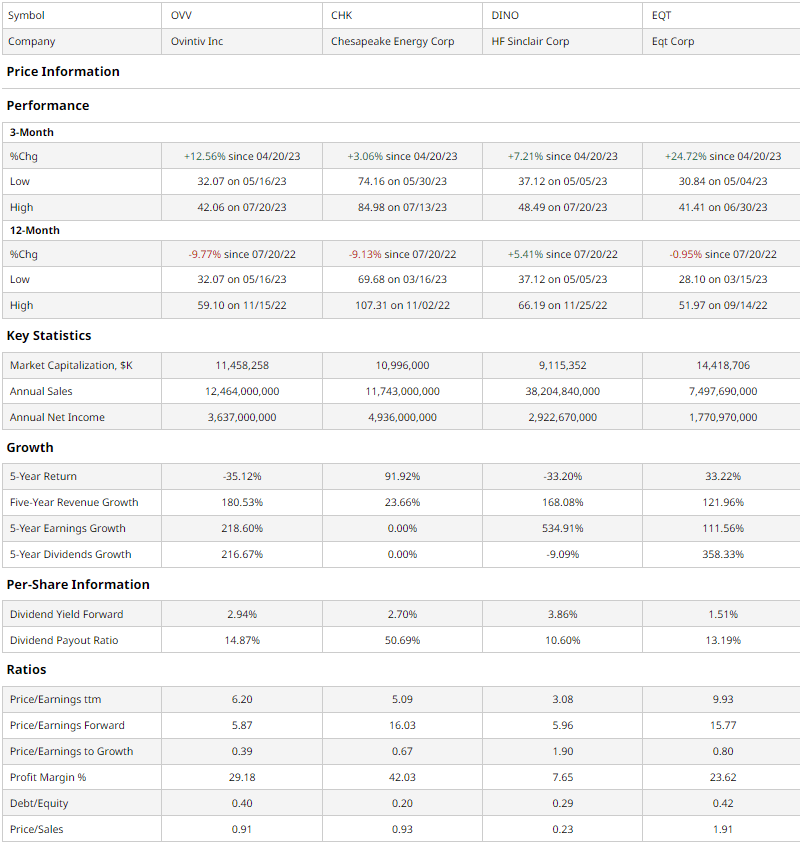

The upstream oil and gas industry remains highly fragmented, with a range of actors, from vertically integrated oil majors like ExxonMobil ( XOM ) and Chevron ( CVX ), to junior explorers, to mid-cap firms like Ovintiv. As such, I sought to compare Ovintiv with similarly sized oil and gas firms in the upstream and midstream segments, including fracking pioneer, Oklahoma-based Chesapeake Energy ( CHK ), oil refiner and oil-product manufacturer, HF Sinclair ( DINO ), and hydrocarbon explorer and pipeline transportation firm, EQT Corporation ( EQT ).

{kind=link}

As demonstrated above, despite superior growth metrics, multiples-based value, and shareholder return capabilities, Ovintiv has experienced the poorest 12-month price action, although the stock has rallied in the past quarter, with the second-best price performance of the group, likely reflecting the company's strong earnings and production beat.

For instance, Ovintiv maintains the lowest forward P/E ratio, alongside the second-lowest P/S. Moreover, with the lowest PEG of the group, Ovintiv demonstrates outsized growth potential.

This theme of operational outperformance and stock-price underperformance is manifested by Ovintiv's historic movements, with best-in-class revenue growth and the second-best earnings growth coupled with the poorest price movements of the group.

In conjunction with the second-highest dividend of the group and second-highest dividend growth rate, investors can expect value-centric growth alongside stable income returns.

Valuation

According to my discounted cash flow analysis, at its base case, the net present value of Ovintiv is $48.66, meaning, at its current price of $42.20, the stock is undervalued by 13%.

Calculated over 5 years without built-in perpetual growth, my model assumes a discount rate of 9%, accounting for the company's low-debt levels but assigning a greater ERP in the face of commodity price volatility. To maintain a more conservative approach, despite an average 5Y revenue growth rate of 34.27%, I estimated a slowdown in scale growth, owing to greater financing costs and reduced potential demand growth, and calculated a revenue growth rate of 18%. However, I additionally priced in a reduction in net margins, with greater capex costs to maintain the pace of scale growth.

{kind=link}

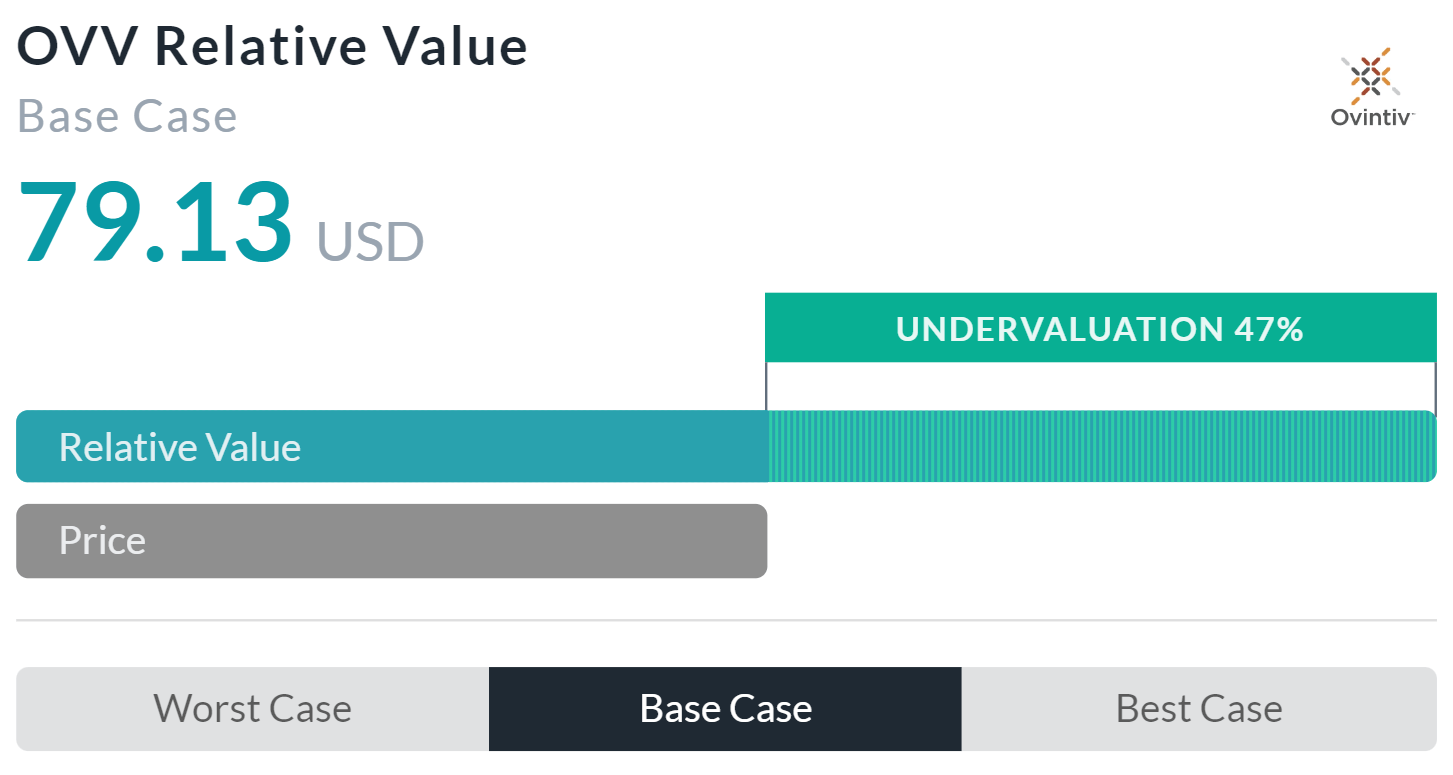

Alpha Spread's multiples-based relative valuation tool more than corroborates my thesis on undervaluation, estimating the stock remains underpriced by 47%, with a true relative value of $79.13.

Nonetheless, due to Alpha Spread's inability to incorporate the potential for commodity price decline and the supply-demand disconnect particularly prominent in natural gas, alongside the model's inability to discount dividends, leads me to believe Alpha Spread is overvaluing Ovintiv.

As such, using a weighted average heavier towards my DCF and lighter towards Alpha Spread's relative valuation, the fair value of Ovintiv should be $53.86, with the stock currently undervalued by ~22%.

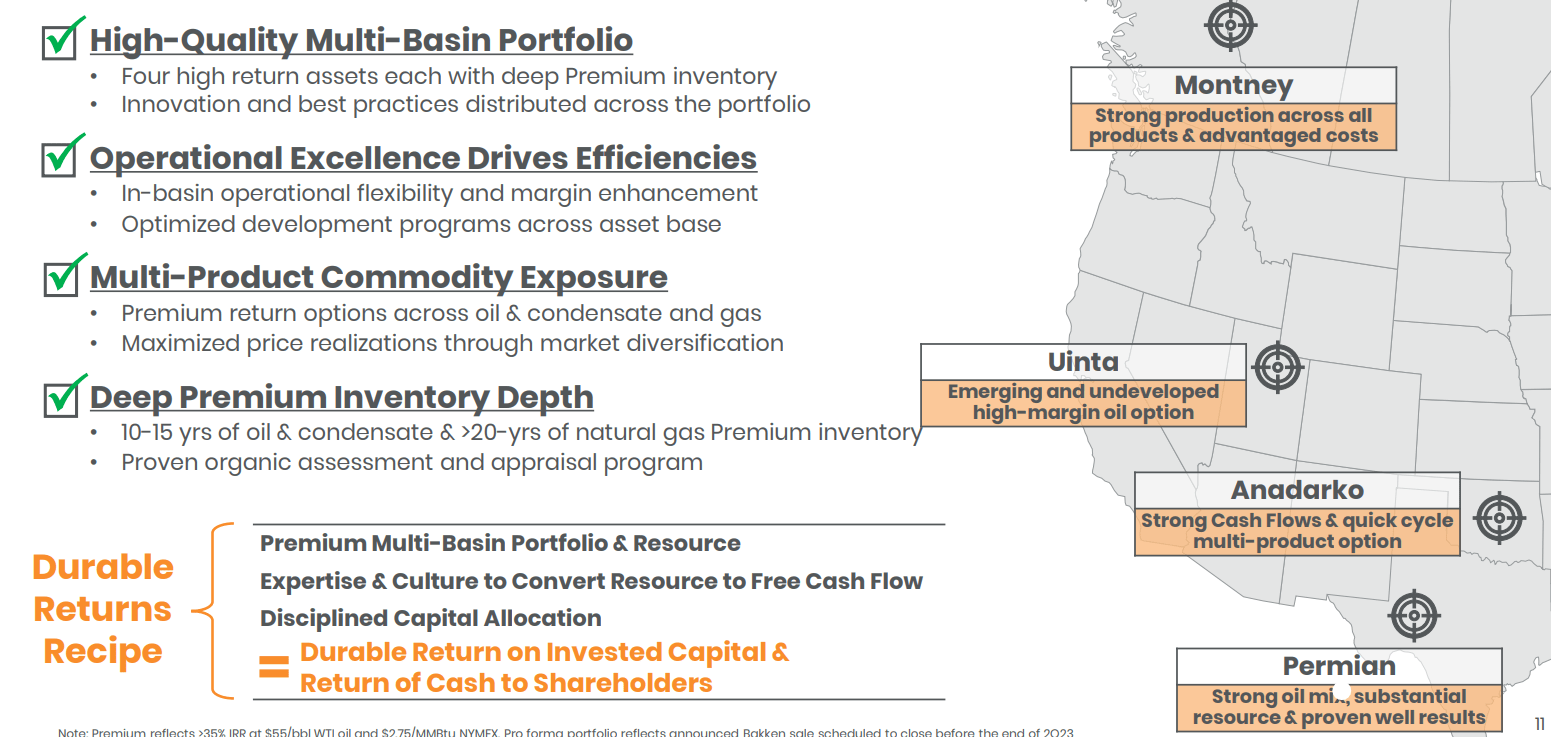

Ovintiv's Portfolio Remains Diversified & Well-Positioned For Long-Run Growth

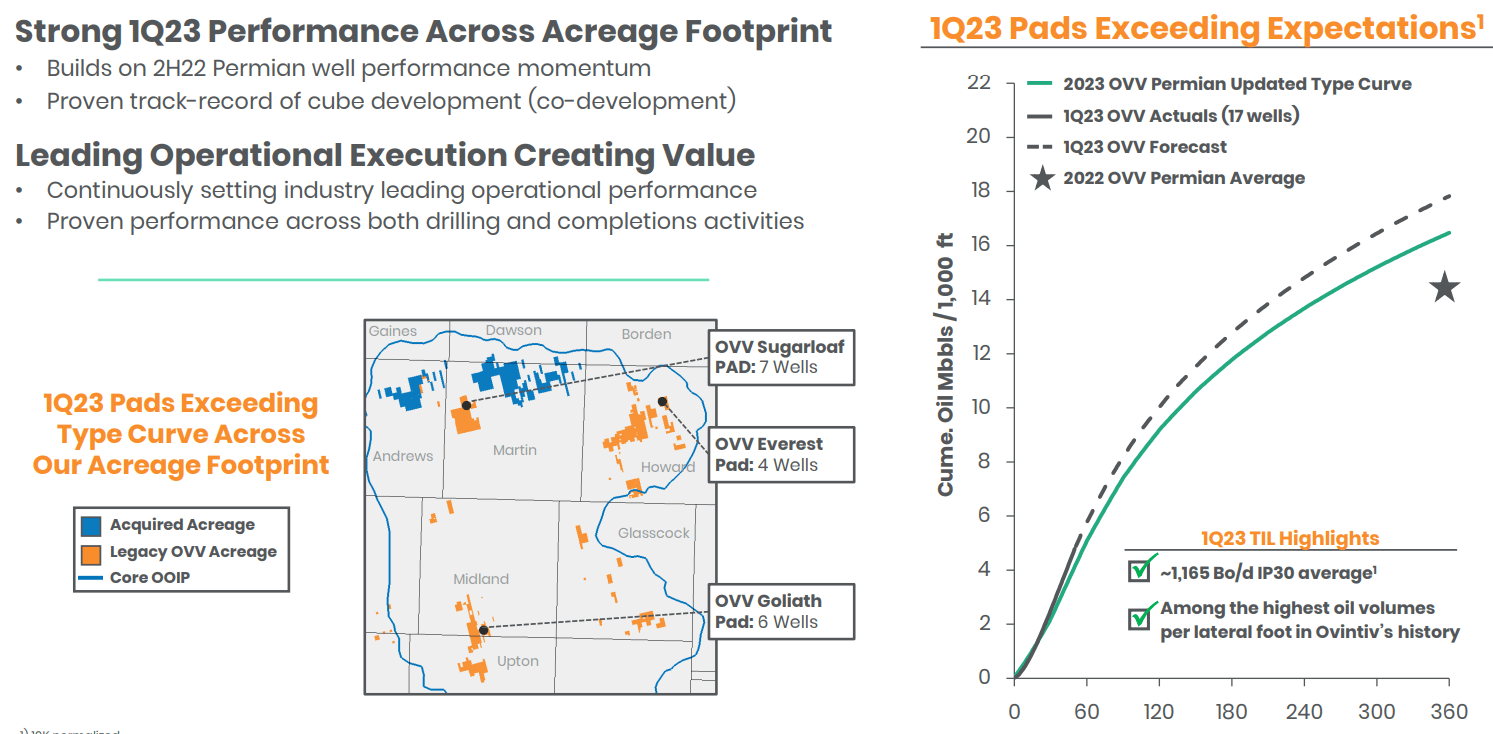

Ovintiv's growth strategy continues to hinge upon the scale expansion of high-quality assets. Most recently, Ovintiv has aggressively oriented its development towards the Permian Basin, wherein the firm has proven operational excellence. The said streamlined approach has seen a $4.275bn expansion in core basin assets alongside an $875mn divestment from less efficacious Bakken assets. Through this, Ovintiv has projected the rest of FY23 to see average oil and condensate output of ~192k bbl/day and FY24 expand said production to an average of >200k bbl/day, both being raised on guidance.

{kind=link}

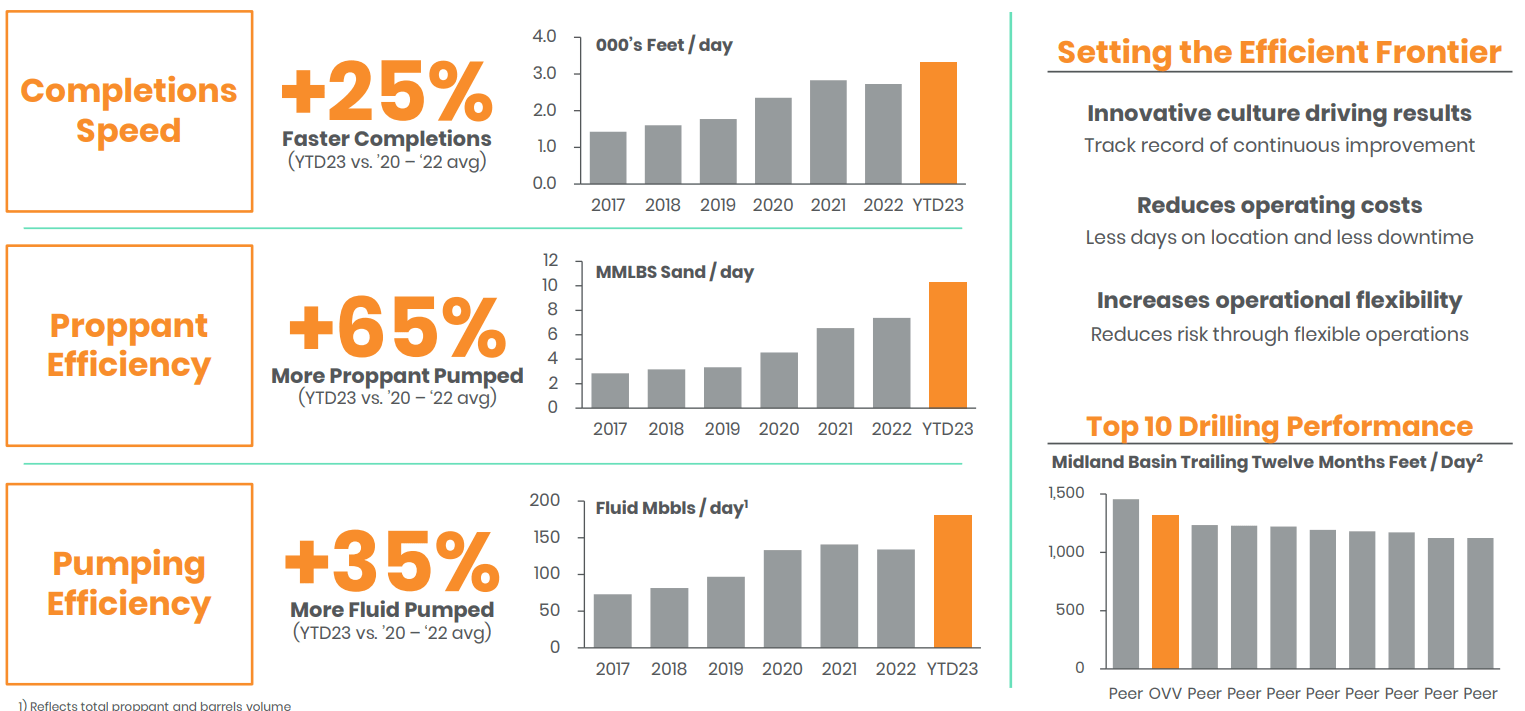

The latter operational growth feeds into Ovintiv's broader strategy of capital and operational efficiency, working towards superior production capabilities and margin expansion. Through this, Ovintiv has accelerated project completion velocity by a quarter, increase fracking output capabilities, and pump a greater volume of fluid with lower input levels, and overall maintained the second-best drilling performance among midland basin peers.

{kind=link}

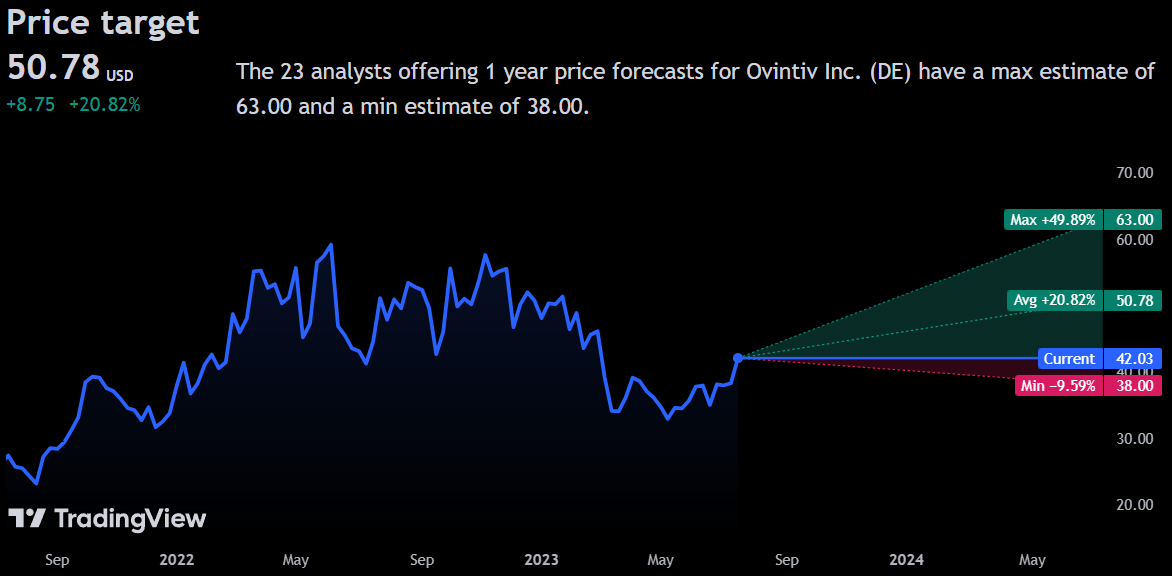

Wall Street Consensus

Analysts largely echo my positive view of Ovintiv, projecting an average 1Y price target of $50.78, a 20.82% increase from its current price.

{kind=link}

Even at the minimum calculated price target, analysts predict a decline of 9.59%, to a price of $38.00, with the net loss smaller due to Ovintiv's dividend. Still, in its worst case, analysts do not expect an extensive price decline, likely a product of existing undervaluation, with bear cases driven largely by extraneous factors.

Risks & Challenges

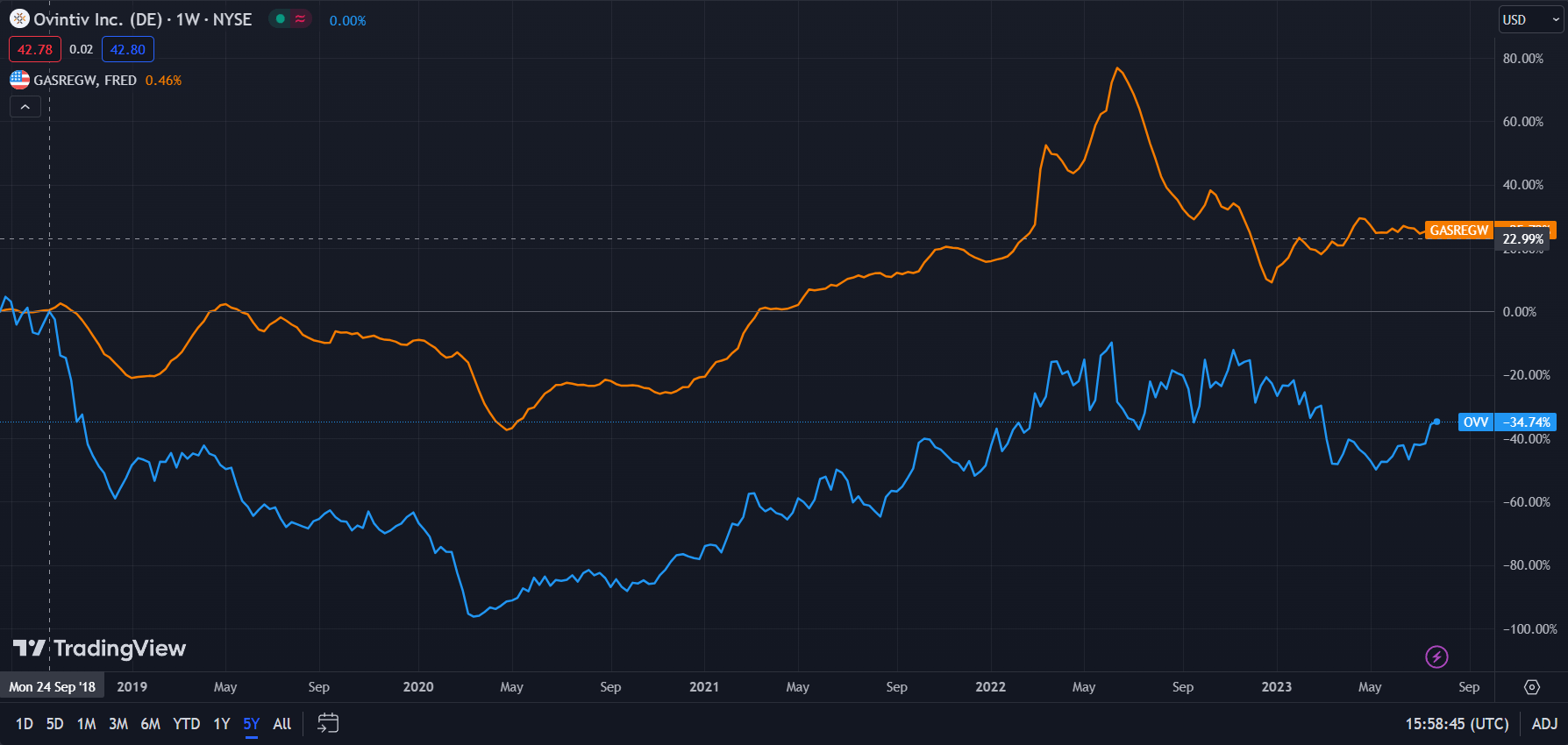

Ovintiv's Stock Price is Subject to Commodity Price Volatility

Although, within the confines of its operations, Ovintiv has put a premium on efficiency and a diverse range of assets, the firm nonetheless remains dependent on oil and gas price swings for operational success. As such, declines in fossil fuel prices driven by supply excess or diminished demand may lead to reduced revenues and scalability.

Although OVV has underperformed, its movements have largely been in line with gas spot prices (TradingView)

{kind=link}

Regulatory & Financing Pressures May Reduce the Viability of New Projects

Ovintiv's low debt ratios enable the firm to finance inorganic expansion judiciously. However, rising interest rates and greater cost of equity- especially when concerned with ESG-related funds- reduce the firm's capability to expand. Coupled with potential climate and environment-related federal and state regulations, Ovintiv's growth capabilities remain compressed.

Conclusion

In the long run, Ovintiv's combined scale capabilities and margin-expanding efficiency will support strong shareholder returns and share price reversion.

For further details see:

Ovintiv Maintains Enhanced Prospects With Strong Assets And Core Midland Acquisition