PACB - Pacific Biosciences: Looks Appealing In The Fast-Growing Long-Read Sequencing Market

2023-09-10 03:52:50 ET

Summary

- Pacific Biosciences has a leading position within the fast-growing long-read DNA sequencer market. Moreover, it is expanding its high-accuracy long-read portfolio to grab more market share from Illumina.

- My DCF model indicates significant upside potential. A sensitivity analysis shows that downside potential seems also limited.

- The complementary credit analysis I performed rules out any large need of capital increase for liquidity reason.

- I personally believe that the recent stock correction, correlated with other high Beta stocks, is a good opportunity to buy the stock.

Editor's note: Seeking Alpha is proud to welcome DZ Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

My thesis

Goals of this article are to assess the competitive landscape of Pacific Biosciences of California (PACB), set a company valuation and via a complementary credit analysis, assess if liquidity or solvency risks are present. I find out that the firm can outperform the long-read sequencing market for the coming years while exhibiting strong operating leverage. My calculations indicate a growing cash flow generation post 2026 allowing for significant potential upside for equity holders. Meanwhile, credit risk seems limited to me.

Investment overview

The technological advance of PACB within long-read sequencing was recognized by Illumina, trying to acquire the Californian company in 2019. Since then, the product update from Sequel II to Revio has been quite impressive. However, competition cannot be understated and will be intense. Main direct competitors are Illumina, Oxford Nanopore (ONTTF) and Beijing Genomics Institute ((BGI)). Illumina launched a product in March 2023 allowing for long-read sequencing but at a cost of $1,350 per full genome: higher than the $1,200 per sequencing of Oxford Nanopore and $1,000 per test of PACB. Note that PACB's strength not only consists of a lower cost per genome to sequence long-reads, but can also count on the highest read quality (Q33: >99.9%) vs. Q22 (>99%) for ONT. Meanwhile, Roche (RHHBY), while collaborating with Illumina, could enter into the NGS sequencing market thanks to its acquisition of Stratos Genomics made in May 2020.

PACB is also now present in the short-read sequencing, thanks to its acquisition of Omniome back in 2021. Its sequencer is called Enso and has started to be shipped in the second quarter of 2023, but revenues are expected by the management to be minimal this year and ramp up by 2024. It has a deep resolution (Q40, meaning 99.99% accuracy) allowing for less false positives. PACB just announced in August 2023 the acquisition of Apton for $110 million, a high throughput short-read sequencer firm, to enhance its portfolio against Illumina.

The main revenue driver is expected to be Revio, given its outstanding performances on long-read DNA sequencing. It integrates GPU chips (Nvidia) and, according to the Q1 conference call, allows for a large improvement with regard to previous Sequel II generation: " That's 400 gigabases per 24-hour run on Revio. To put that in perspective, Sequel IIe generates just 30 gigabases of sequence in 30 hours ."

I suspect that long-read sequencing will not only be a good complementary to short-read but also at some point a potential substitute, taking into the pie of Illumina NGS market. This could be achievable as the cost of sequencing of long-read falls way under the $1,000 level and can analyze much more information relevant to genomics. Revio product launch has exceeded expectations and reached new customers, as a third of new backlogs (>76 in Q1) came from new clients.

It will now be a question of execution (production, shipment) and controlling well the supply-chain to avoid any delays or cost inflation. Gross margins are expected to bottom this year as better production yields will be reached and a ramp-up of client throughput will fuel material uses (accretive effect). Financing needs will also be important, but we will see later on that the current cash level should be sufficient to cope with the 2023-2026 cash burn generation.

What valuation can we expect?

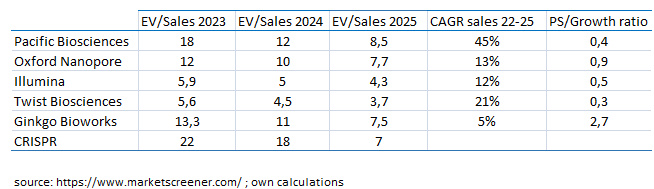

First, let's acknowledge that as the firm expects to be cash-flow breakeven after 2026, P/E and EV/EBITDA ratios can't really be employed until then, leaving EV/sales possible and long-term DCF model. Starting with multiples of revenues, we see that PACB is priced at 18X for FY23 but should converge toward 8X by 2026 thanks to its high growth profile. Compared relatively to peers in the DNA space, its EV/sales ratio to forward 3-year growth is actually quite good, as can be seen below:

{kind=link}

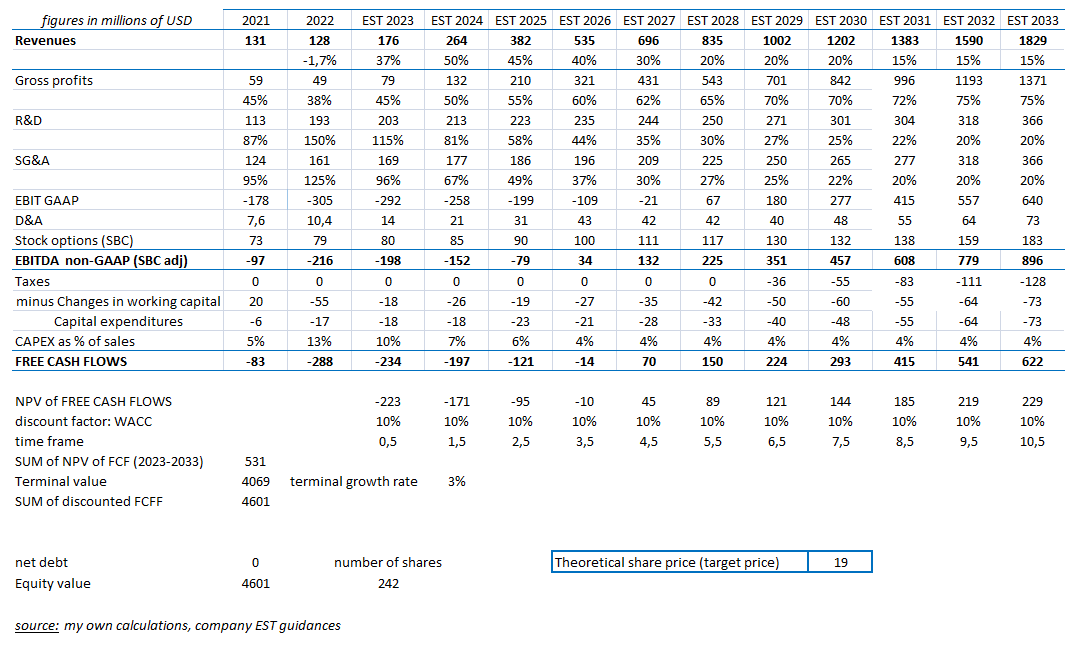

Trying to reach the intrinsic value of PACB, I set up a 2-stage DCF model (10 years, then infinity) in order to model different phases of the business (scaling /acceleration and durable growth).

I used as first hypothesis a revenue generation in line with the management estimate: with a 2022-2026 CAGR over +40% leading to revenues outpacing $500m by 2026. Meanwhile, its direct competitor ONT aims to grow more than 30% per year over the midterm.

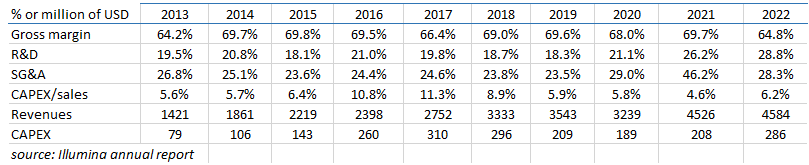

Then, concerning gross margins: I expect a gradual improvement toward 60% (high-end of management target) and long term, reaching 70%. In comparison, its competitor Oxford Nanopore should reach 60% this year and is targeting more than 65% by 2025. Illumina, while benefiting from a much larger scale, has generally benefited from a 65-70% gross margin level.

Going to operating expenses: I model the level of R&D/sales and SGA/sales to converge toward respectively 25% and 22% by 2030. In comparison, Illumina level of spending as a mature company and before Grail merger related extra spending was: 18.5% RD/sales and 23.5% SGA/sales, from 2018 to 2019. PACB management expects non-GAAP OPEX to grow only by +5%/year from 2022 to 2026 as most R&D and commercial workforce expansion are behind.

Finally, I used a 5% CAPEX to sales ratio, which has been the low-end level of Illumina.

{kind=link}

Using these inputs, and company data , I reach a FCF neutrality by 2027, so one year after the management expectation.

{kind=link}

I derive a target price of $19/share, representing 80% upside potential given current market prices. We understand there is a large spectrum of outcomes and forecast uncertainties in the model, due to the fast-growing profile of the company. Therefore, I implemented a sensitivity analysis:

Author's estimates

We can see that current stock price implies a revenue growth after 2026 of only 10% per year: this seems pessimistic to me.

Are we at the risk of a large capital raise?

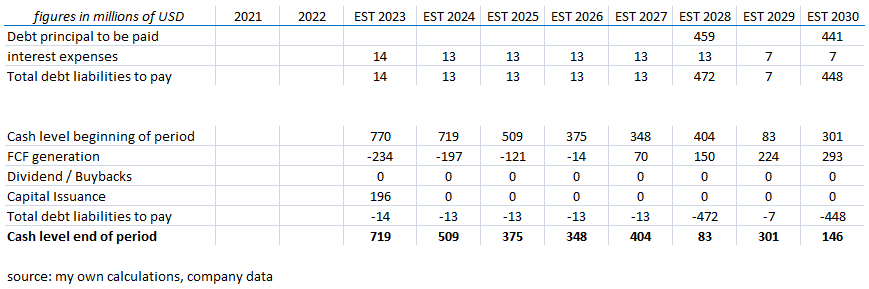

By implementing a credit analysis, we can see that: the debt profile exhibits two convertibles to be repaid by 2028 and 2030 respectively, which is far enough to prevent any liquidity issue. Until then, interest payments are quite low, as coupons were negotiated in 2020 during a low interest period. With regard to solvency issue, the projected free cash flow generation should be enough to repay both debt principals. If PACB had to miss my FCF projections, I still don't expect any large capital raise (apart from an M&A event) any time soon as the debt wall is not happening before 2028.

{kind=link}

Other risks

Several risks could impair my positive thesis. The first one which comes into my mind is related to the company competition. As discussed, Oxford Nanopore is a current serious competitor within long-read sequencers while Illumina , despite being a latecomer in this sub-market, dispose of formidable financial and technological resources to catch up. The second is related to the addressable market size: while 2026 revenues forecasts seems to be achievable given the strong dynamics of new backlogs, the mid-long term trend is uncertain: it is still possible that the short-read market will remain dominant, leaving the short-read as a niche market.

Conclusion

To sum up, I do believe PACB represents an appealing investment proposition. Its chances to grab a large market share of the fast-growing long-read sequencing market are real and, according to my estimates, it has sufficient financial resources to avoid any large capital increase. My fair value estimate is at $19/share, indicating 80% upside for the stock. Of course, risks associated with the business case are elevated, but the risk/reward ratio seems acceptable.

For further details see:

Pacific Biosciences: Looks Appealing In The Fast-Growing Long-Read Sequencing Market