PLTR - Palantir: Fundamentals Versus Narrative

2023-05-25 09:27:23 ET

Summary

- Palantir's business continues to grow at a moderate rate and margins are steadily improving. In the current macro environment, this type of stable performance should be seen as a win.

- PLTR stock has moved significantly higher in recent weeks, driven by growing excitement around the potential of generative AI.

- Palantir's current performance does not justify the move in the stock price and it is unlikely that growth will accelerate sufficiently to support the stock in a deteriorating macro environment.

Palantir ( PLTR ) continues to face a difficult macro environment, but management is extremely optimistic on the opportunity provided by generative AI. Rising expectations are setting investors up for disappointment though and creating downside risk. This may not matter in the near term as a bubble appears to be forming, with investors chasing price across a range of stocks, regardless of fundamentals. This could be spurred further by NVIDIA's ( NVDA ) recent forward guidance, which suggests a surge in data center demand for GPUs.

Palantir expects AI to be transformational for its business and for its customers, and is rebalancing its investments to capitalize on the opportunity provided by LLMs. Palantir’s view of the opportunity is quite pragmatic, and while recent management discussion seems overly promotional, generative AI can likely provide Palantir with genuine benefits.

Palantir appears to be basing its approach around Google’s ( GOOG ) purportedly leaked memo . Proprietary models hold a slight quality edge, but open-source models can iterate faster. As a result, Palantir believes that value is likely to accrue at the application and workflow layer, with vendors that can address skills shortages likely to do particularly well. Generative AI could also increase competition at the application layer, meaning that applications will need a source of advantage to benefit. Infrastructure providers are also well positioned due to the likely increase in activity.

Palantir believes that its platform has the framework, infrastructure, and software needed to capitalize on the opportunity provided by LLMs. It is leveraging this opportunity through the introduction of its Artificial Intelligence Platform ((AIP)). AIP empowers organizations to activate large language models safely and securely. It appears to be something of a coordination layer, connecting users with Foundry services and data. Palantir is focused on rapidly gaining mindshare with AIP, making it difficult for others to enter the market.

While Palantir may benefit from this in the long run, many of its customers are relatively conservative and the decision to standardize on Palantir's platform is a strategic one with a relatively long sales cycle, meaning that any benefit from generative AI is likely to be modest in the near term.

Microsoft ( MSFT ) is taking a similar approach in this area, and its distribution footprint makes it a formidable competitor. Palantir, Alteryx ( AYX ) and Microsoft have solutions that target different use cases and users though. Microsoft’s Fabric product is far more of a competitive threat to Alteryx than Palantir.

Fabric is an end-to-end analytics platform that integrates data and tools. At this stage it is not really clear to what extent Fabric represents genuine product innovation versus a marketing rebrand though, as it appears to be largely based on the integration of existing tools, like Azure Data Factory, Azure Synapse Analytics, and Power BI.

{kind=link}

Figure 1: Microsoft Fabric (source: Microsoft)

Microsoft plans on leveraging generative AI to help business users extract insights from data. This includes integrating Copilot into the service so that users can create data pipelines, generate code, build machine learning models, and visualize results using conversational language.

Palantir also recently launched:

- Process mining & automation suite

- Scheduling primitives

- Foundry marketplace developer suite

The Process Mining & Automation Suite enables customers to visualize their business processes and find inefficiencies. This moves Palantir in the direction of robotic process automation and it will be interesting to see if the company begins to add automation features in the future. Scheduling Primitives allow dynamically responsive resource allocation and scheduling. The Foundry Marketplace Developer Suite allows customers to create their own application marketplaces, where users can find both apps and assets.

Palantir’s Foundry Ontology Software Development Kit helps customers to build applications and integrate ontology into existing applications. These SDKs will also eventually support AIP. Palantir has stated that the market response to Foundry Ontology SDKs has been positive so far.

Process mining and SDKs extend Palantir beyond being a data and decision making platform, which is supported by infrastructure tools like Apollo. While it is still early days for Apollo, Palantir recently announced that it has closed its first 1 million USD Apollo deal.

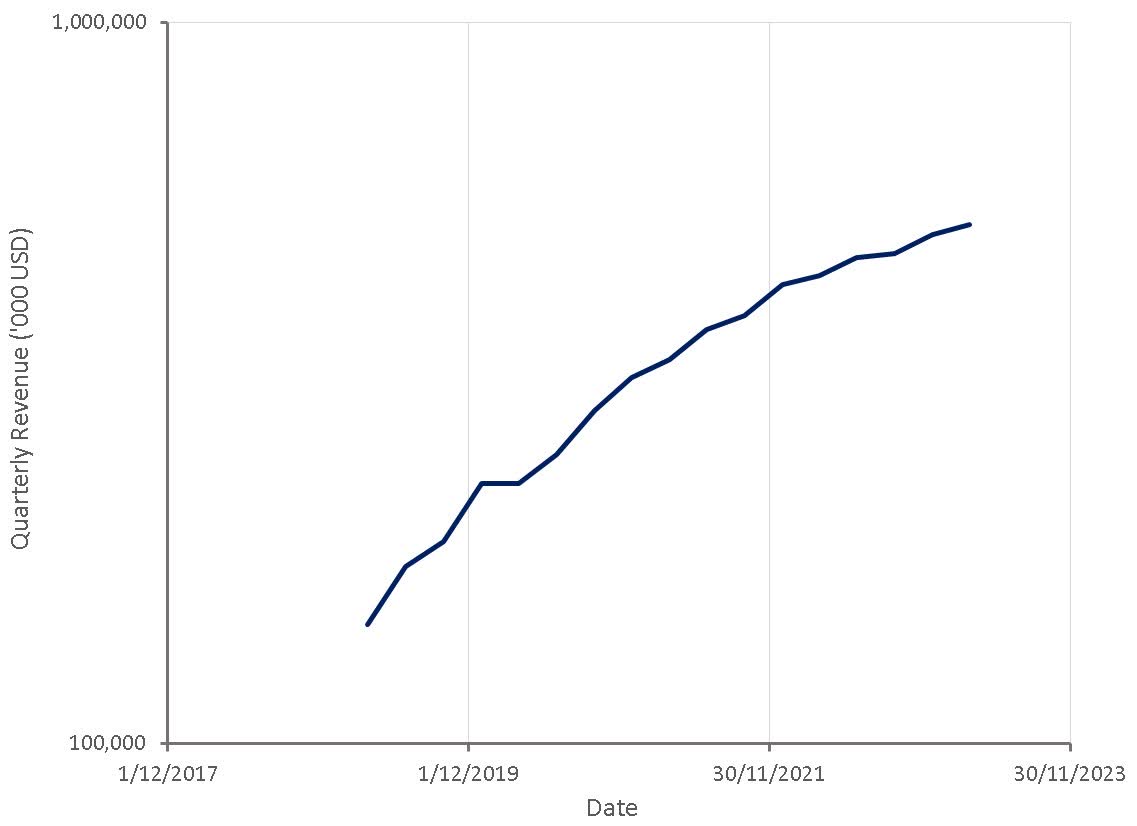

The first quarter tends to be Palantir's slowest quarter, but YoY growth did stabilize after six consecutive quarters of deceleration. Palantir's US commercial business reaccelerated and pilot starts and conversions were robust. Palantir also has a strong pipeline of US government opportunities, but there is uncertainty associated with this in respect to timing.

Palantir is currently guiding for 2.185-2.235 billion USD revenue in 2023, representing roughly 16% growth over 2022.

{kind=link}

Figure 2: Palantir Revenue (source: Created by author using data from Palantir)

Palantir's revenue tends to be lumpy, which is likely reflective of typical contract sizes and the nature of the company's services. This makes extrapolating performance difficult, but the last two quarters look constructive for the commercial business.

{kind=link}

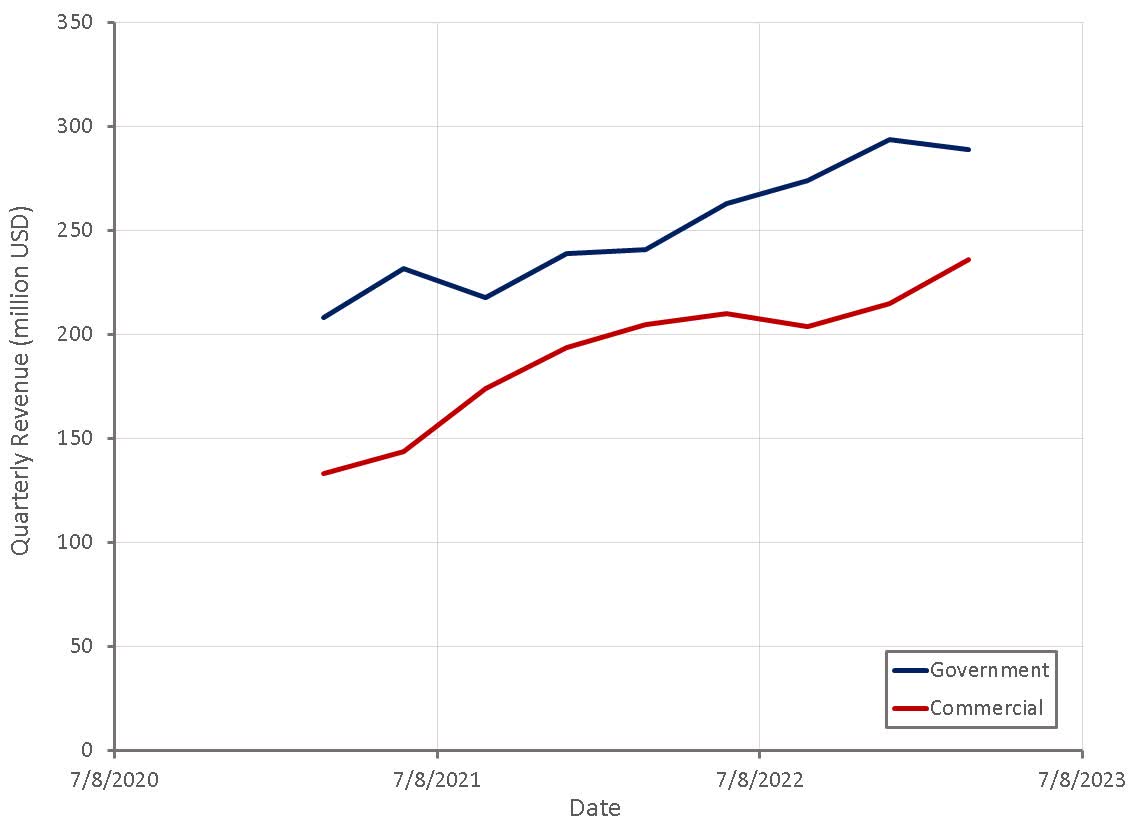

Figure 3: Palantir Revenue Segmented by Customer Type (source: Created by author using data from Palantir)

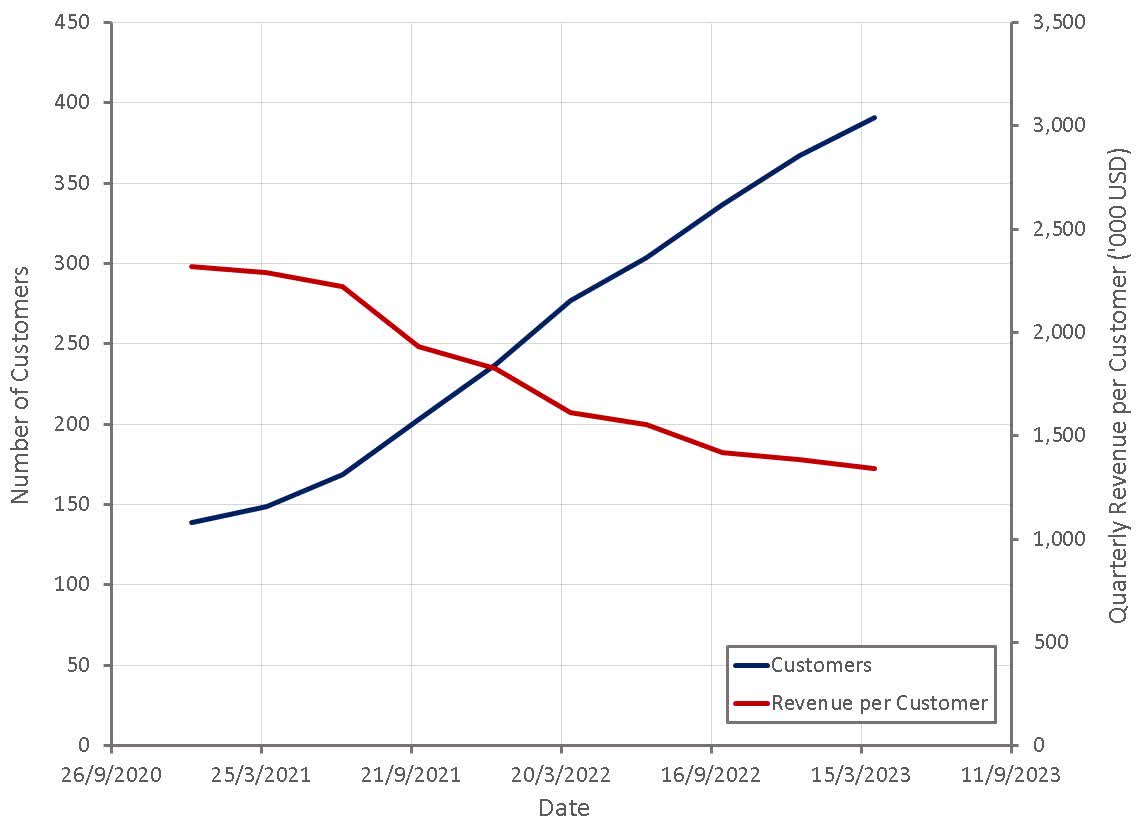

Palantir's business continues to be characterized by a relatively small number of extremely large customers. In the first quarter Palantir closed 64 deals worth at least 1 million USD. Of those, 22 were worth at least 5 million USD and eight were worth at least 10 million USD. First quarter, trailing 12-month revenue per customer from the top 20 customers increased by 14% YoY . New customer acquisition also remains relatively robust, although may be beginning to decelerate.

{kind=link}

Figure 4: Palantir Customers (source: Created by author using data from Palantir)

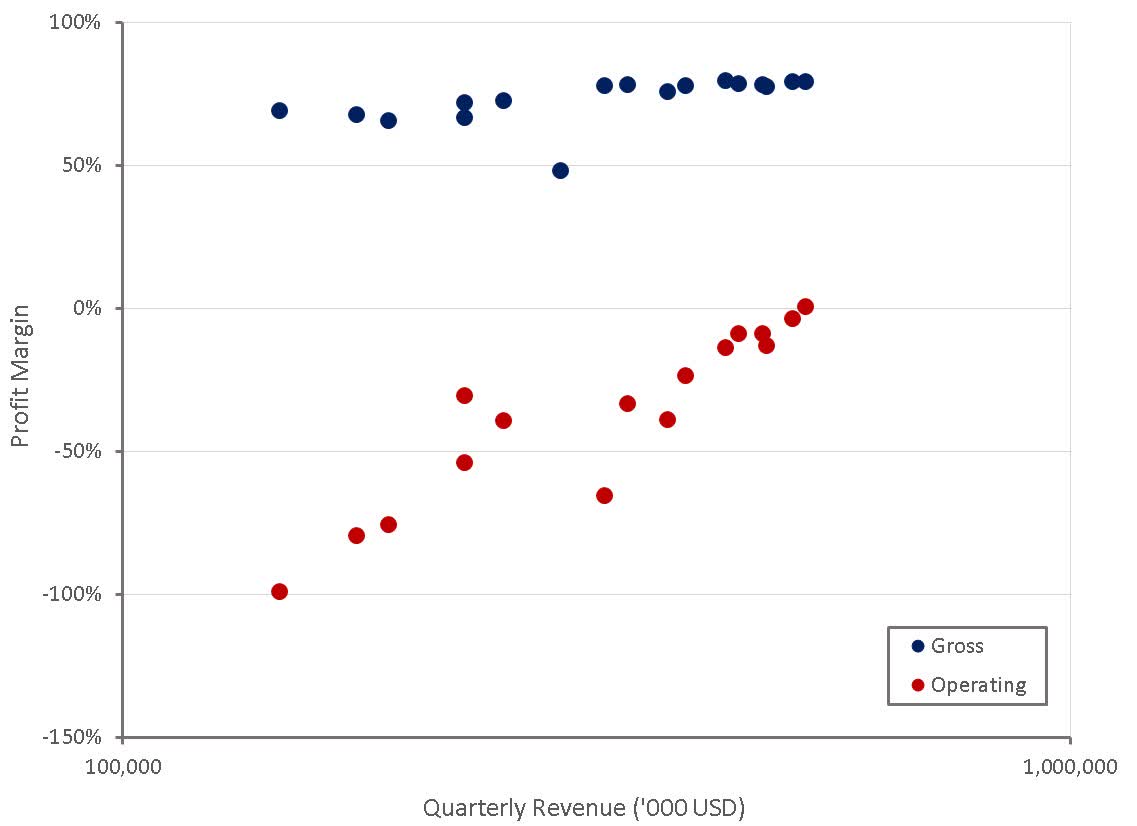

The most impressive aspect of Palantir's business at the moment is its consistent ability to improve operating profit margins with scale. This stands in stark contrast to many software companies that have struggled to improve margins, even with an increased focus on costs.

{kind=link}

Figure 5: Palantir Profit Margins (source: Created by author using data from Palantir)

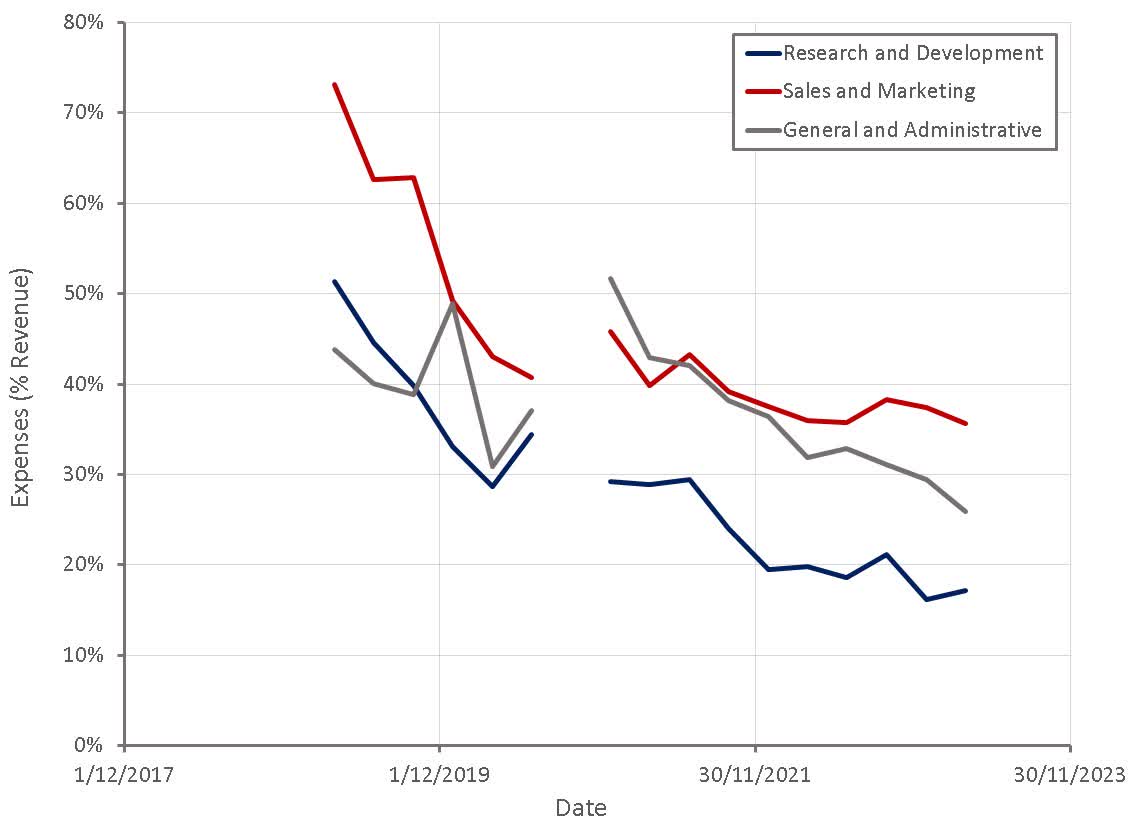

Palantir can also likely continue to drive margins higher as general and administrative costs still appear to be bloated. Management has stated that they are focusing on optimizing operations in G&A, capturing cloud efficiencies and focusing headcount investments in key strategic areas.

{kind=link}

Figure 6: Palantir Operating Expenses (source: Created by author using data from Palantir)

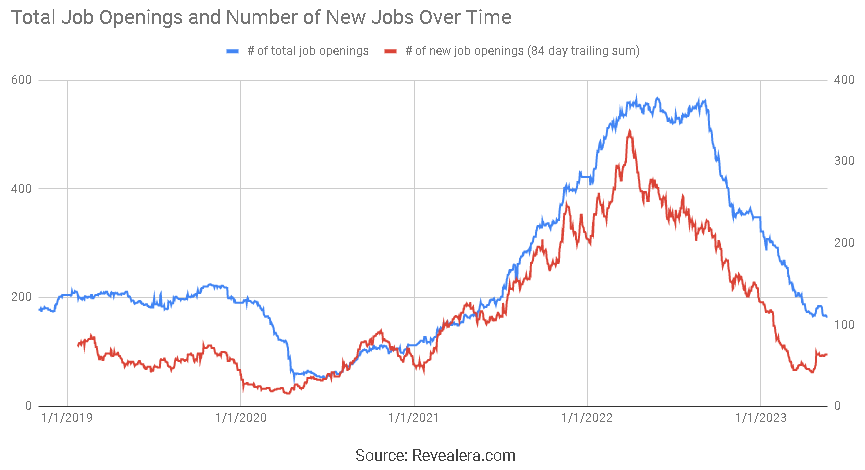

Job openings at Palantir suggest that growth in costs should be modest going forward, but there is also little to indicate support for the hype around AI. If generative AI is truly going to be transformational for Palantir, it would be reasonable to expect the company to be hiring ahead of a surge in demand.

{kind=link}

Figure 7: Palantir Job Openings (source: Revealera.com)

There is currently a lot of confusion surrounding AI and what it means for different companies. While LLMs are clearly a tailwind for some companies, others are naively being bid up when the actual impact is likely to be muted. Palantir may see some benefit in coming months, but a step change in growth, like NVIDIA is highly unlikely. This creates the potential for downside risk if growth doesn't accelerate in line with investor expectations.

While Palantir isn't necessarily overvalued on an absolute basis, there are now a range of SaaS companies with better prospects that are trading on similar or lower valuations. Profitability should provide Palantir's stock with some support going forward, but the market will likely want to see higher growth in order to justify the current valuation.

For further details see:

Palantir: Fundamentals Versus Narrative