RTX - Palantir May Beat Consensus Again

2023-08-01 07:25:27 ET

Summary

- Today I'm previewing PLTR's forthcoming earnings report.

- What are the odds that Palantir will beat the current earnings estimates? My model says that the odds are very high - Read on.

- But what really confuses me about PLTR in the long term is its valuation in light of the specifics of its business model.

Intro & Thesis

If you have been following my articles, you are likely aware that I have previously covered Palantir Technologies Inc (PLTR) stock at length . I have analyzed different valuation models, discussed the company's business model and prospects, and assessed the probability of Palantir surpassing analysts' expectations on its earnings dates based on the latest quarterly reports from its peers. As you read this, I will preview PLTR's forthcoming earnings report and explain why it's probable to exceed current consensus estimates again.

Updated model: Palantir Can Beat The Consensus Revenue Estimate Again

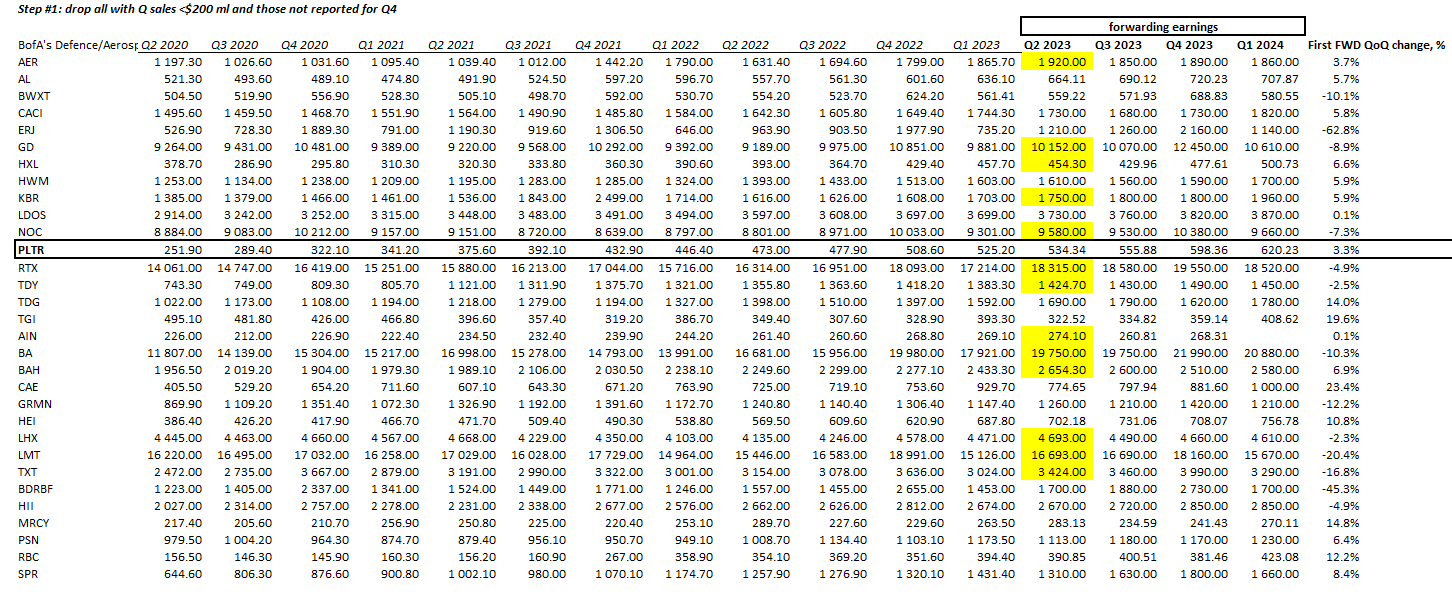

To begin, I would like to briefly describe the nature of my model. I took BofA's coverage sheet of the Aerospace and Defense sector [proprietary source], of which Palantir is a part because ~52% share of the company's revenues still depends on government contracts. Of the 31 companies on that list, only 13 were able to report for the second quarter of 2023. But that's enough for the analysis - the sample is relatively complete, and there's no point in waiting for the rest (there's a risk that we won't have time to present the analysis in a written form; besides, 1-3 new observations wouldn't change anything). So here are the companies and their sales figures:

Author's work, Seeking Alpha Premium data

{kind=link}

Above, I have highlighted in yellow the companies that have already reported for Q2 FY2023.

Since I collected all the data manually, I had the opportunity to qualitatively assess the latest earnings results. What stood out to me was that almost all the companies that reported Q2 sales and earnings figures beat forecasts [by a margin] that had previously been lowered by analysts in anticipation of stagnant growth.

Defense spending is on the rise, and therefore the risks of an economic slowdown did not affect companies or their forwarding earnings. However, there have been situations where stocks have fallen sharply even on a very good report and surprises in earnings per share and sales.

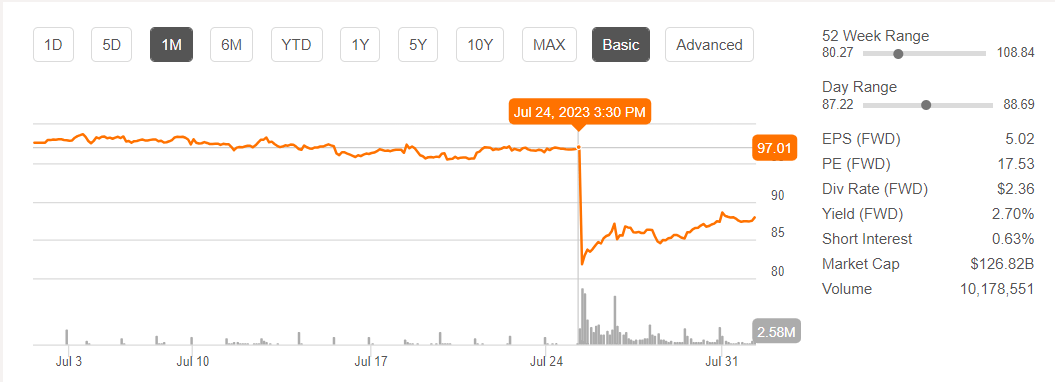

Take Raytheon Technologies (RTX) as an example. The firm reported impressive financials for Q2 , with an EPS of $1.29 (beating estimates by $0.11) and revenue of $18.32 billion (beating estimates by $620 million). However, its stock was downgraded by Morgan Stanley due to concerns over mechanical defects in Pratt & Whitney's jet engine. The company aimed to address the issue and said it would provide more information in September 2023, but it didn't help the stock price stay sustainable:

{kind=link}

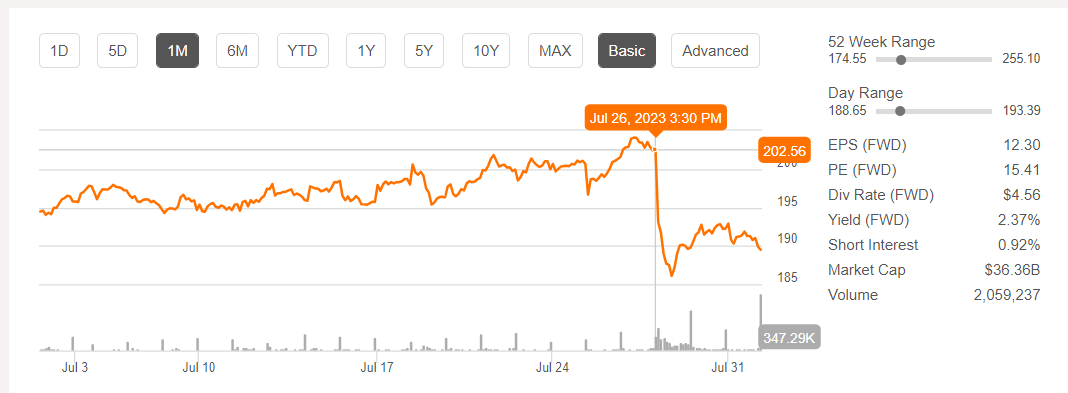

Another example: L3Harris Technologies ( LHX ) reported strong earnings , with a Non-GAAP EPS of $2.97, beating expectations by $0.02, and revenue of $4.69 billion, surpassing estimates by $320 million. Despite these positive figures, LHX's stock experienced a significant decline after the company announced that antitrust authorities at the U.S. Federal Trade Commission have given their approval for the proposed acquisition of Aerojet Rocketdyne (AJRD).

{kind=link}

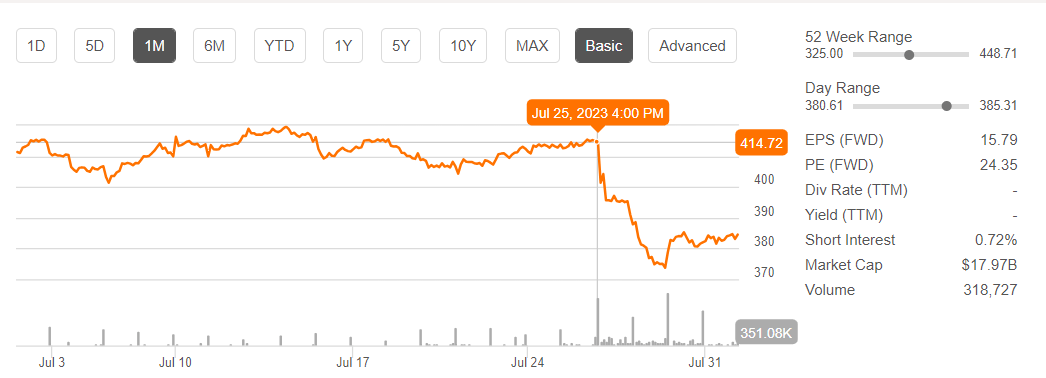

And another one: Teledyne ( TDY ) delivered a strong Q2 , with an EPS of $4.67 (beating by $0.03) and revenue of $1.42 billion (beating by $10 million). But it faced challenges in demonstrating substantial growth in the FLIR segment, and this fact led to a significant drop in the TDY stock following the earnings report:

{kind=link}

But in general, of course, most stocks have reacted positively - as in the case of Booz Allen Hamilton ( BAH ), Boeing ( BA ), Textron ( TXT ), and others. The most important thing is the absence of idiosyncratic risks and uncertainties from earnings calls - then the market will respond positively to earnings beats.

It was the perceived uncertainty in my mind regarding PLTR's Q1 earnings call that prevented me from being confident enough to issue a "Buy" recommendation before the Q1 earnings release in May 2023, even though my "earnings prediction model" indicated a high probability of a positive surprise that time. Also, the company seemed too overvalued to me at the time in light of future growth obstacles due to its labor-intensive business model [read my previous article to learn more about these points].

So if we assume that Alex Karp [the CEO] is optimistic as usual and there are no idiosyncratic risks, what are the odds that Palantir will beat the current earnings estimates , according to my model?

The model says that the odds are very high (at least when it comes to revenue) :

Author's work, Seeking Alpha Premium data

{kind=link}

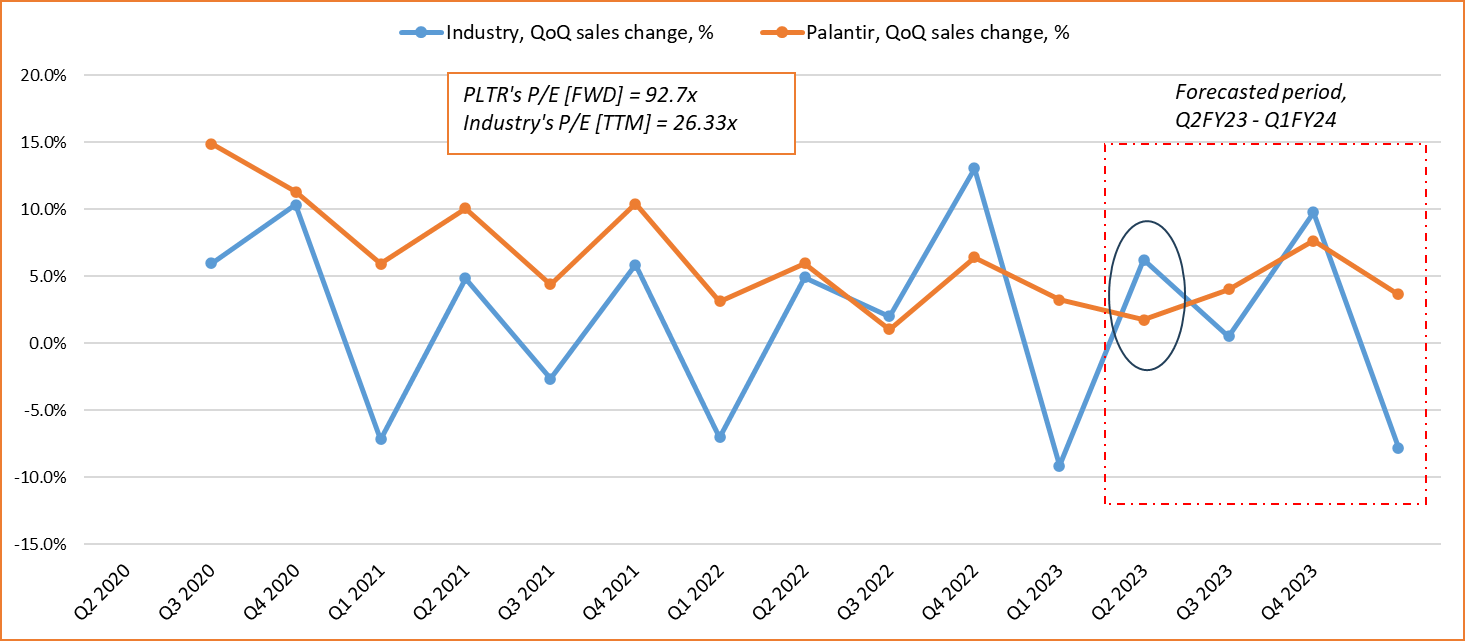

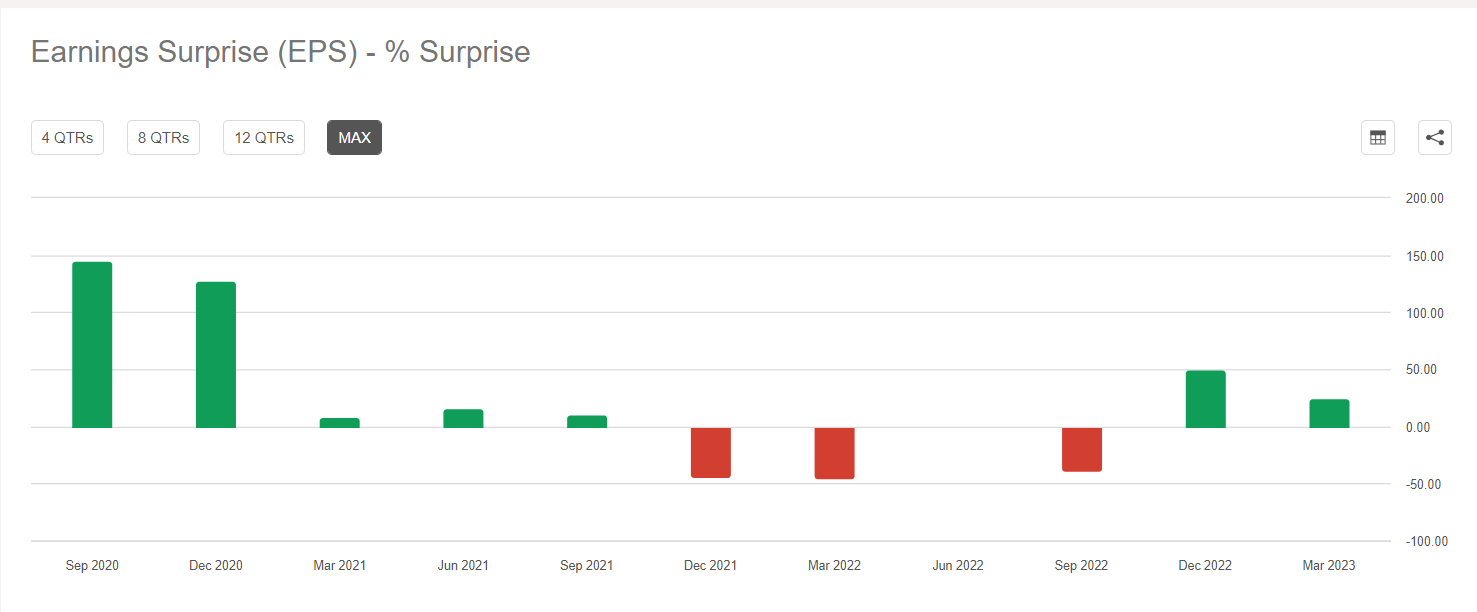

In the chart above, you can see the average QoQ change in industry sales compared to corresponding changes in PLTR's sales. I use both historical dynamics and the next 4 quarters of estimates. As you can see, PLTR's growth in 2020-21 outpaced the industry's growth - the company grew strongly and outperformed the average growth, which includes numbers from more mature companies with more "value-like" [non-tech] operations. But during 2022, Palantir's growth stagnated while the overall defense industry experienced a post-Covid upswing. Last 2 quarters, we saw PLTR return to a growth path, which let it beat the EPS estimate by a margin:

{kind=link}

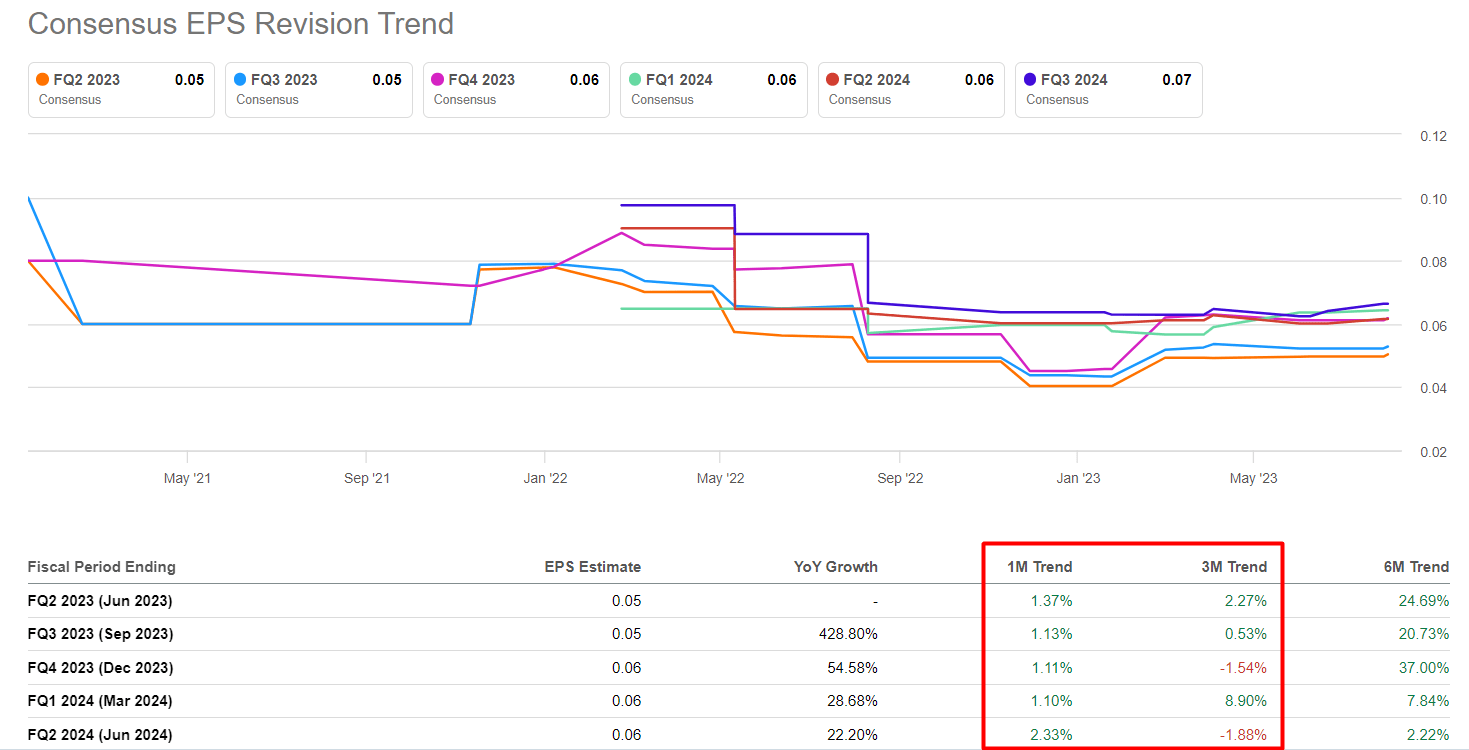

But analysts are in no hurry to adjust their estimates - at least not in recent months:

Seeking Alpha Premium, PLTR, author's notes

{kind=link}

This has led analysts to currently expect only a 1.7% quarter-on-quarter change in revenue from PLTR, compared to an average growth of 6.2% for the industry as a whole (taking into account QoQ results from the 42% of companies that have already reported). This is going to be a once-in-a-lifetime event in the company's history.

In my opinion, this event is not destined to come true. Given the hype surrounding the company and its role in applying AI to the U.S. defense sector (the Wedbush analyst even compared it to soccer superstar Lionel Messi, which sounds too bold and quite funny to me), the implied tailwind is not reflected in PLTR's sales growth consensus for Q2 at all, in my view. Another earnings beat is around the corner.

But I'd Avoid Palantir In The Longer Term

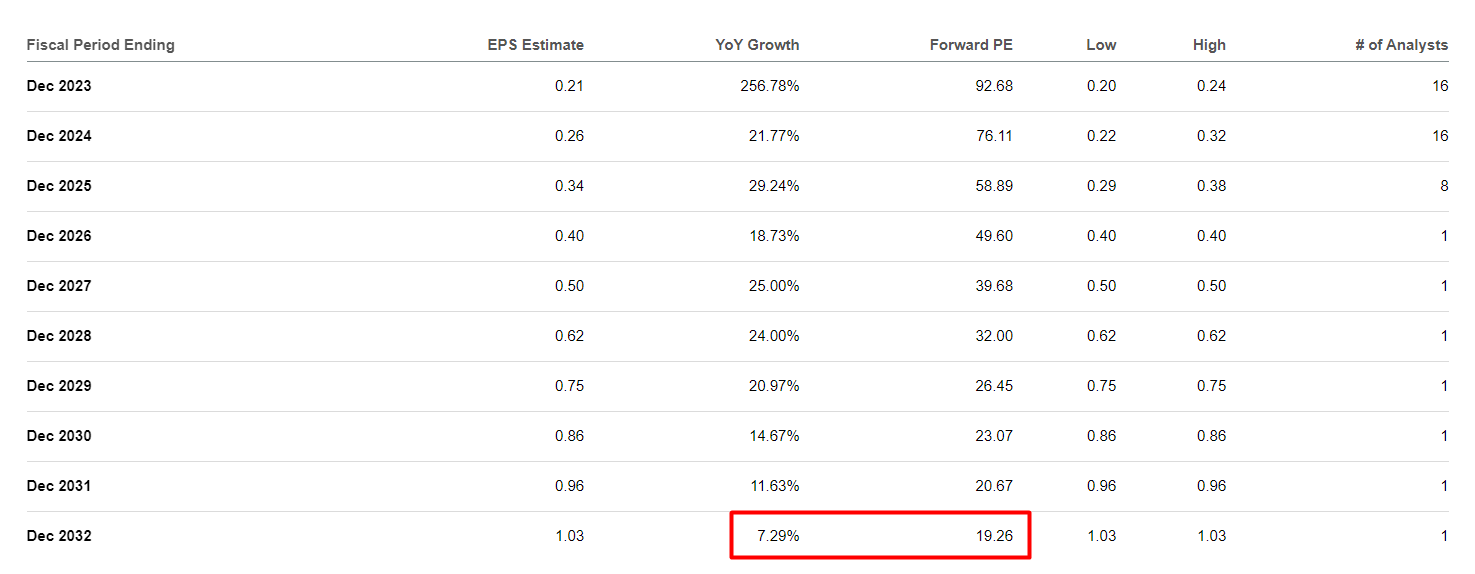

What really confuses me about this whole story is the valuation of the company in light of the specifics of its business model. Yes, I've written about this on numerous occasions, and my latest Sell thesis hasn't aged well, which I must admit to readers. Still, the fact remains that PLTR stock trades at 92.7 times next year's earnings per share, while the defense industry as a whole [the median of the 31 companies in the sample] trades at only 26.3 times the TTM P/E (I think the next year's value is even lower).

So it's fair to say that PLTR should grow much faster than the industry. According to the data I have on hand, PLTR's revenue growth over the next twelve months ((NTM)) should amount to 16.3%, while the corresponding industry figure (median) is only 8.8%. At the same time, however, PLTR's valuation is at least 3.5x higher than the industry's, based on its P/E ratio. The company's valuation includes a premium for AI, for longer-term EPS growth and market expansion. But even with an implied decline in the multiple, PLTR's P/E will be ~19x in 10 years [amid a 7.3% EPS YoY growth in FY2032], which I think is too expensive. Palantir will have to work hard to grow out of this valuation, and its business development in the Commercial segment is still questionable, as it's not the only AI company there.

Seeking Alpha Premium, author's notes

{kind=link}

The Verdict

Given all this, my article turns out to be neutral. On the one hand, PLTR's Q2 FY2023 revenue numbers (and assumingly EPS) seem too low to me, given how well the rest of the industry is reporting. And I haven't even talked about the tech sector, where there were even more beats this quarter. On the other hand, Palantir Technologies is too expensive to buy now to hold for the long term - most likely we are going to face a long consolidation at best after a possible strong earnings jump.

Be that as it may, the conclusions of my valuation and earnings prediction models are subjective and should not be used as the only decision-making tool for buying or selling PLTR before its upcoming earnings report. I strongly recommend you do your own due diligence before doing anything.

It would be interesting to know what you think of all this - let me know in the comments below! Thanks so much for reading!

For further details see:

Palantir May Beat Consensus Again