TSCO - Panic Never Pays: Avoid These 5 Dividend Stocks And Buy These 5 Instead

2023-03-31 07:00:00 ET

Summary

- Panic never pays.

- It seems the market could go up just as well as it could go down.

- How to invest in these situations?

- Here are 5 high quality dividend stocks to avoid, and 5 to buy.

Written by Sam Kovacs

Introduction

It is curious that Vladimir Lenin, the early 20th century Russian revolutionary, coined a saying which is extremely pertinent to capitalism and the stock market:

"There are decades where nothing happens, and there are weeks where decades happen."

The past few weeks have certainly felt this way.

The Silicon Valley Bank fallout, which led to the failure of Signature and Credit Suisse, have shook the markets.

This has led to a migration in deposits from regional banks to "too big to fail" banks.

Yet while many said this was a "Lehman moment" for the markets, so far the stock market has been holding up quite well throughout March, with the exception of regional banks which are directly impacted by the flow of funds.

Bloomberg

What's more, is that nobody seems to agree on the direction of the market, with the spread between the highest and lowest year-end S&P 500 targets being the biggest in two decades.

Bloomberg

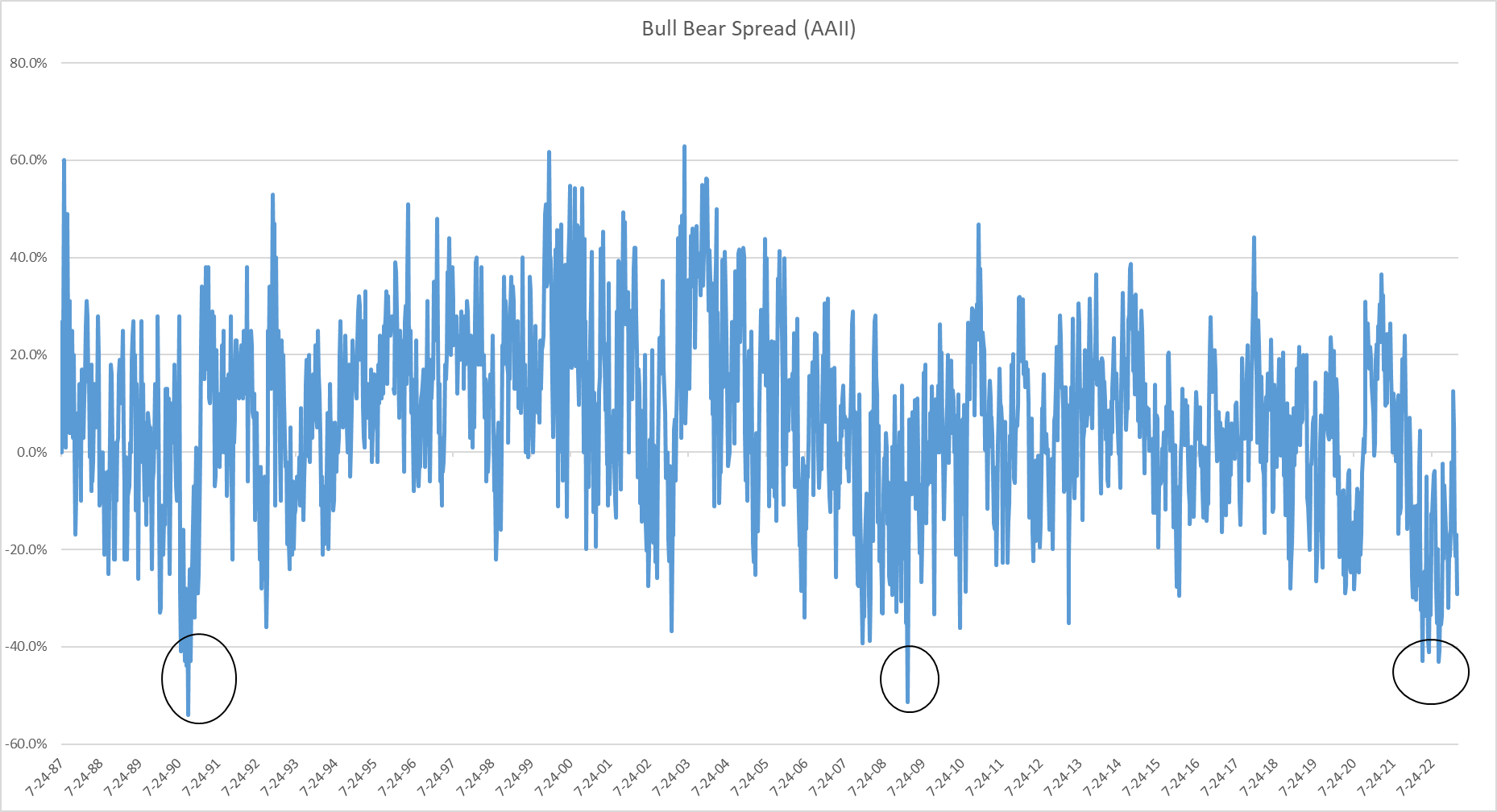

What is interesting to note, however, is that whenever these spreads were so high historically (at least in the past 20 years) they predated bull runs.

Since the AAII started tracking investor sentiment in 1987, every time the bull bear spread was less than negative 40%, it predated large bull market runs.

{kind=link}

The recent movements in bond yields indicate that traders are betting on yield cuts this year, despite Powell saying this won't happen.

The market doesn't trust the Fed anymore, and why should it? Powell spent all of 2021 repeating that inflation would be "transitory", only to capitulate in 2022.

Unfortunately, Powell is often tricked by thinking that he can force his will onto markets and the economy. But he can't, we can't, nobody can.

If the market tips into a recession, and the markets knee jerk, then the Fed might once again flip the script and move to cuts, which in turn could fuel a frenzied bull market to cap off the mega bull market which started in 2009.

Talented technical analyst Avi Gilburt sees the potential for a large rally from here. From one of his recent articles :

First, I still have not seen absolute evidence that this degree of bear market has indeed begun. Rather, I still think there is some potential that we can rally over 5000SPX before that bear market begins in earnest. And, I am assuming the rest of 2023 will likely make this issue a settled matter. Should the market make it very clear later this year that the long-term bear market has indeed begun, then I think we will all have to change our mindsets as to what the future holds sooner rather than later.

What is clear, is that in the next few months, it could go both ways.

How does one position for this?

How do you invest, knowing that either things will go very well, or very bad, with little room for a middle ground?

Dividend Investing will see you through it all

Here's the thing.

If we go into a long bear market, or if we go through another electric bull market, how does that affect your plans?

If you're planning your retirement based on the idea that you'll be withdrawing x% of your portfolio every year, then you're in a very precarious position.

A 20%, 30%, or even 40% decline in market value of your portfolio would set you back many years, or force you to compromise on your quality of life once retired.

Not optimal.

As dividend investors, we do not deal with this.

In fact, all of our dividend investing, buying as well as selling, is guided by our North Star:

" Does making this investment decision improve my income potential once retired?"

We buy stocks when they are priced at attractive valuations so that the combination of dividend yield & dividend growth will provide us with sufficient income in the future to retire on comfortably.

When people join the Dividend Freedom Tribe, we put them through a course which makes sure they've planned for all of these things.

We diversify our portfolios so that no single mistake can derail the plan.

We focus on high quality stocks, because why be owners of subpar businesses?

We then opportunistically sell when stocks are overvalued, and reinvest the proceeds in undervalued stocks, within our limited investment universe of just shy of 200 stocks.

Buy low, get paid to wait, sell high. Repeat.

In a bear market, you might go a long time without having opportunities to sell at objectively high prices. You'll have to accept selling at relatively overvalued prices, and rotate into relatively better value stocks.

But even if you didn't sell, but you owned all the right companies, which continued to pay growing dividends, you'd do alright, provided you bought them at the right price.

Now let's proceed to looking at stocks to avoid and stocks to buy in the current environment.

Stocks to avoid

So, if you're a dividend investor like us, you're probably already focusing on just high quality dividend stocks.

Many of the stocks we're going to suggest avoiding here, are stocks we've owned at some point.

It is not because anything is fundamentally wrong in their business that we're avoiding them.

It is because the price is too damn high.

Successful investing is always a function of price. Especially when it comes to dividends.

We can "guesstimate" dividend growth over the next 10 years, and it's a very unprecise exercise because it involves both the economic reality of the company and the board and management's decision regarding their dividend policy.

But the dividend yield you're getting today is not up for debate. If you can conservatively invest in stocks which yield enough given your best estimate of dividend growth to reach your investment targets (the details of which I cannot explain here, a whole course is dedicated to it), then you're setting yourself up for success.

The following stocks, are not only relatively expensive relative to both their dividend growth potential and their historical yield range, but they have poor momentum.

Momentum is a factor which when you're uncertain about what is going on in the market, is a good failsafe.

Expensive stocks with poor momentum are in a particularly bad spot, because they are at extremely high risk of tanking a lot.

We calculate momentum by ranking all US stocks on 3 month performance, 6 month performance, and 12 month performance, then created a composite score of those rankings and rank the stocks on the composite score. This gives stocks a score from 0 to 100, with 100 meaning they have the strongest momentum.

Let's see a few examples of overvalued stocks with poor momentum.

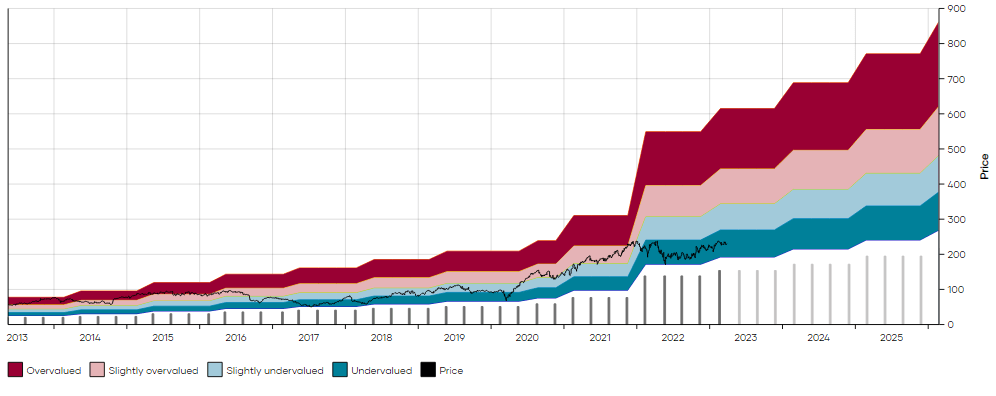

Northrop Grumman ( NOC ) currently yields 1.5%, which is a little less than its historical 10 year median yield of 1.5%. It ranks among the 38% of worst US companies on momentum.

{kind=link}

We exited the last of our NOC position at $485 , and missed the rally. This was fine by us, as nobody ever gets the top.

But a look at the MAD chart above shows that NOC can be a volatile stock.

While everything was looking good for it this year: revenue beats, EPS beats, macro tailwinds, we look at the stock's recent price action and can't help but think: I wouldn't risk the downside potential for a 1.5% yield and 10% annual dividend growth.

Based on historical movements, if NOC doesn't regroup, if defense stocks have topped for the cycle on the back of extreme war fears and security threats, then we could see NOC go down below $400, maybe below $380.

Note that nothing in the business is going wrong, but the market dynamics and income potential just aren't sufficient to justify being exposed here.

Let's look at another.

Caterpillar ( CAT ) currently yields 2.2%, which is below the median 2.68% for the past decade. Its momentum ranks somewhere in the middle of the pack, at the 56th percentile of US stocks (better than 56%), but its 3 month performance suggests that CAT might already have topped.

{kind=link}

With cyclicals like this, it's when things are looking too rosy that you want to be concerned. As you can see, CAT has clearly undergone multiple up and down cycles.

In a recent note, analysts at Baird downgraded the stock on fears that the backlog has maxed out.

This might be the case in North America and EMEA, but I believe this leaves out the China factor, which many seem to be underplaying right now.

A strong Chinese demand could extend CAT's cycle a little longer, but it is nonetheless apparent that if history rhymes within a year or two, the cycle can be expected to turn.

Declines in backlog usually then lead to declines in share price for CAT, and as you can see, they can be brutal.

The swings in stocks like CAT mean you really want to be careful buying when "everything is going great" because the cycles happen quite regularly.

This is not to say we don't get a last leg up before it plunges, but the risk-reward isn't satisfactory, and getting such a low yield and an expectation of 8% dividend growth means that you're not getting enough compensation if things go wrong early.

Let's look at another which could look attractive, but could be a trap.

W.P. Carey ( WPC ) currently yields 5.5%, a tad less than its 10 year median yield of 5.74%. It ranks among the worst 38% of stocks on momentum.

{kind=link}

WPC's high yield means that you're getting paid to wait, even if the dividend is growing at just 1% per year, while you're accumulating, the reinvestment of such a big dividend carries its weight as is.

The recent pullback in the stock might look like it's setting up an attractive entry point, but that would be acting to fast. As you can see WPC's stock has oscillated within a quite tight band. Buying the stock when it yields 6.2% or more (the deeper blue range on the MAD Chart above) sets investors up for success. Buying when it yields less than 5.3% sets investors up for a tough road ahead.

WPC still hasn't recovered its 2019 highs, which shows how long you can stay underwater when buying at the wrong price.

Note you can still be underwater when buying at the right price, but you have history on your side, and you're getting sufficiently compensated for it.

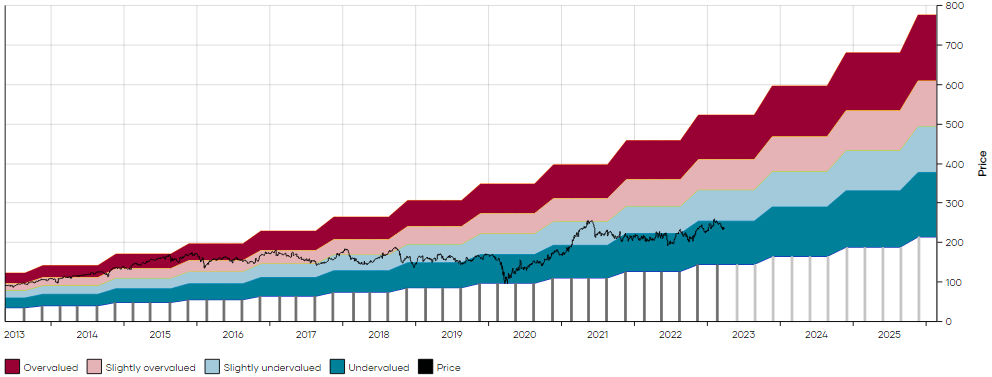

Archer-Daniels-Midland ( ADM ) currently yields 2.3%, which is less than its 10 year median yield of 2.69%. Its momentum ranks among the 20% worst US stocks, which means it is extremely at risk of doing bad in the next 3 to 6 months.

{kind=link}

Agricultural commodities might be just taking a small breather from what is looking to be a secular tailwind for the sector, amid worldwide population growth, global warming and what not. This doesn't mean that you should pile in at any price.

If you bought close to the top in 2014 to 2015, it would have taken until 2021 to break even. Not a fun proposition.

You're getting just over 2% to potentially be underwater for years.

Sure ADM could be a $120 stock 3 years from now, but it could just as well go back down to $50 before that.

The risk of tying up capital for so long in a stock that, while on the way down, is still expensive, is just too high.

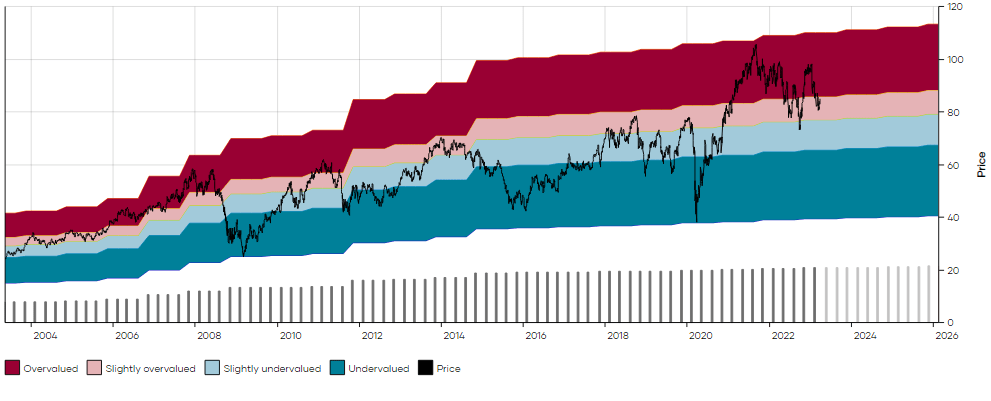

Emerson Electric ( EMR ) currently yields 2.5% which is less than its ten year median yield of 2.8%. It currently ranks among the worst 38% of stocks on momentum.

{kind=link}

For the fun of it, let's look at a 20 year chart for EMR.

{kind=link}

As you can see, there have been fantastic opportunities to profit from the stock over the past 2 decades.

There have also been many traps, where a slightly receding stock price preceded much larger drops. Buying in 2008, 2011, 2013, 2018, 2019, or 2021, would have been a bad idea and caused you a lot of pain, with a lackluster dividend growing way too slowly.

Buying EMR, or even keeping exposure to the stock here, sets you up for capital gain pains, which even if you hold until you eventually break even in the next cycle, will tie up capital without sufficient returns.

Stocks to buy

So if we want to avoid the trap of buying high quality stocks which are overvalued, don't provide sufficient income to wait in adverse scenarios, and are on the way down, which should we focus on?

You've probably guessed it: high quality stocks, which are historically undervalued, provide good income potential, and be on the way up.

Snap-on ( SNA ) currently yields 2.73%, more than its 10 year median yield of 1.94%. It ranks among the top 6% of US stocks on momentum.

The company increased the dividend yet again by 14% this year, which is a phenomenal level of growth.

{kind=link}

It is important to understand that the relationship between dividend yield and required dividend growth is extremely sensitive when yields get smaller.

While a 3% yielding stock might require a 10% dividend growth rate to provide satisfactory returns, a 2.5% yielding stock would require 12% growth, and a 2% stock require 15% growth. A 1.8% yielding stock would require 18% growth.

A smaller step down in yield requires a disproportionately higher growth rate as yields get smaller.

It's a mathematical relationship, and if you care about having enough money in retirement, one you shouldn't take lightly.

SNA is set up to do well at the company level, and the stock level, and provide you a brilliant dividend profile while you wait for these things to play out.

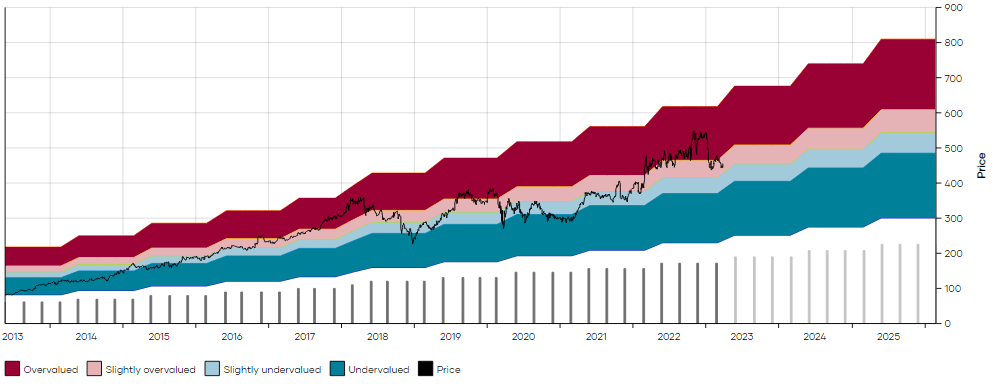

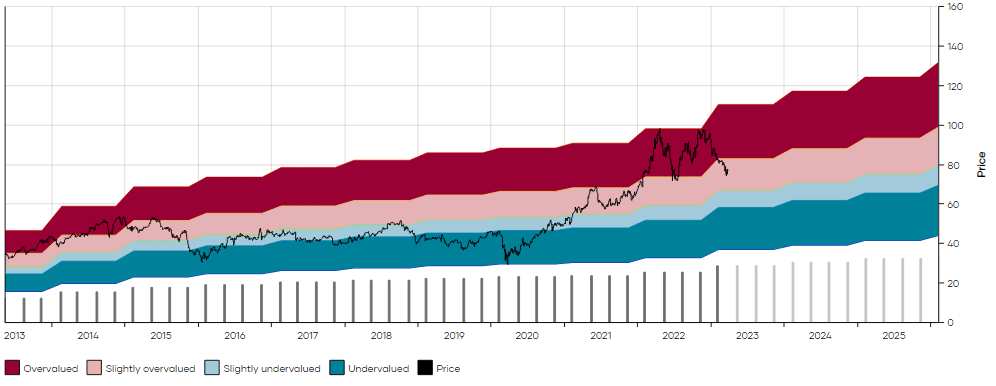

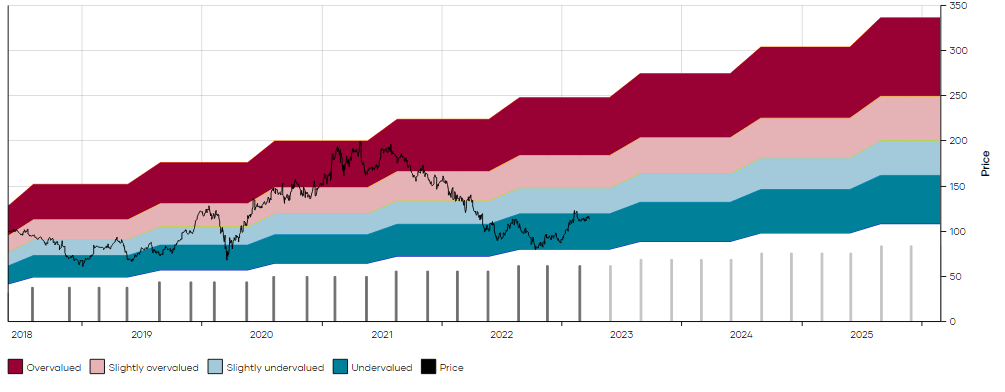

Tractor Supply ( TSCO ) currently yields 1.79%, more than its historical yield of 1.18%. It ranks among the top 11% of US stocks on momentum.

{kind=link}

The company has been doing very well. I explained this as follows to members of the Dividend Freedom Tribe :

Okay, so this is interesting. 65+ Y/Os are more and more present in rural areas.

This is a good data point, as they happen to be the wealthiest age group in the US. This means they will be more resilient through recessions, which is a great group to sell to.

I think that with an ageing population, and desire for more space in retirement, rural America has a glorious future ahead of it (as against the grain as that might sound).

The stock increased its dividend tremendously last year, and followed up with a generous 12% dividend hike this year.

As a discretionary company, its stock price is held back despite very good growth numbers last year, and good growth numbers projected for this year, on the back of its more resilient consumer base.

The discrepancy in historical yields could close, driving the share price up as much as 50% in coming years.

Skyworks Solutions ( SWKS ) currently yields 2.19%, which is significantly more than its 10 year median yield of 1.39%. It ranks among the top 14% of US stocks on momentum.

The 10 year MAD Chart doesn't show the ranges as well as SWKS migrated from being a very low yielding stock pre 2014 to one which oscillated between yielding more than 2% and less than 1%. So I'm displaying the 5 year chart which shows a more realistic view of the ranges since 2015.

{kind=link}

SWKS's revenue was down last year, and it seems that in late 2022, the market might have fully priced the decline in demand for smartphones.

On the upside, SWKS is a high margin, high growth business, which is investing in an impressive pipeline of verticals which will see secular growth (IoT, auto, infrastructure).

But SWKS' future dividend hikes have a lot going for them: The company is buying back as much as 10% of its shares this year, they only pay out 1/3rd of free cashflow, and are in a growth industry.

The strong momentum backed by good business fundamentals means that SWKS could be a $200 stock again within a year or two. You get paid a low dividend with double digit dividend growth to wait for that to happen.

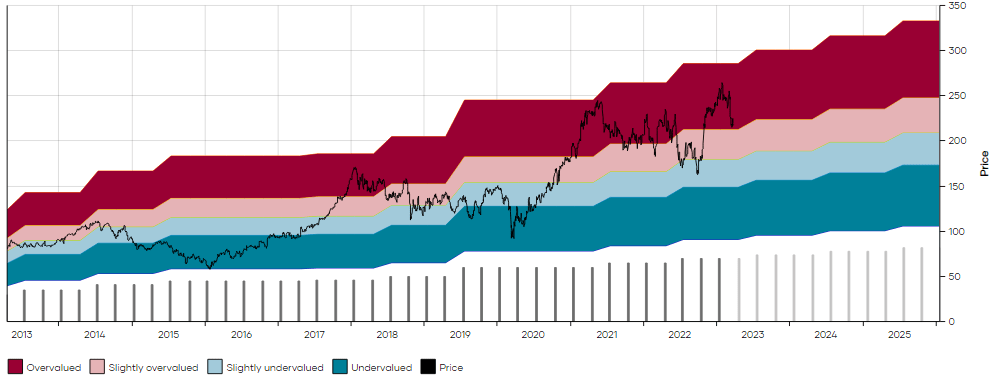

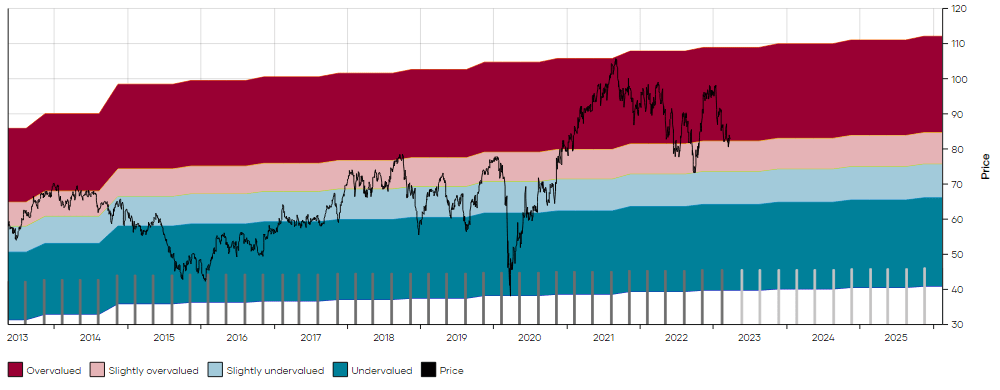

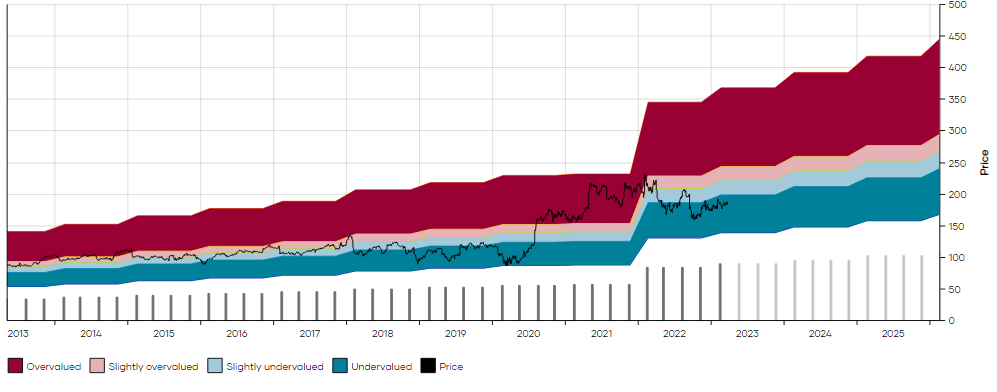

United Parcel Service ( UPS ) yields 3.46%, more than its median 10 year historical yield of 2.9%. It ranks among the top 20% of US stocks on momentum.

{kind=link}

As with TSCO, the market hasn't fully priced UPS's massive 2022 dividend increase.

2023 is expected to be a challenging year for UPS, but once again it seems that this is priced in and the bottom which the stock marked in 2022 could be the transition out of sluggish price action.

The dividend increased by just 6.6% this year, off the back of a massive increase last year.

But a 3.4% yield means you should be adequately compensated when you're getting 6-8% dividend hikes, which would be more in line with UPS rate of growth in the past.

The secular trend of parcel deliveries worldwide is unlikely to slow down anytime soon, and UPS have done a grand job at streamlining their business, optimizing their cost structure, and growing massively during the pandemic.

Get it while its down, yet on the way up.

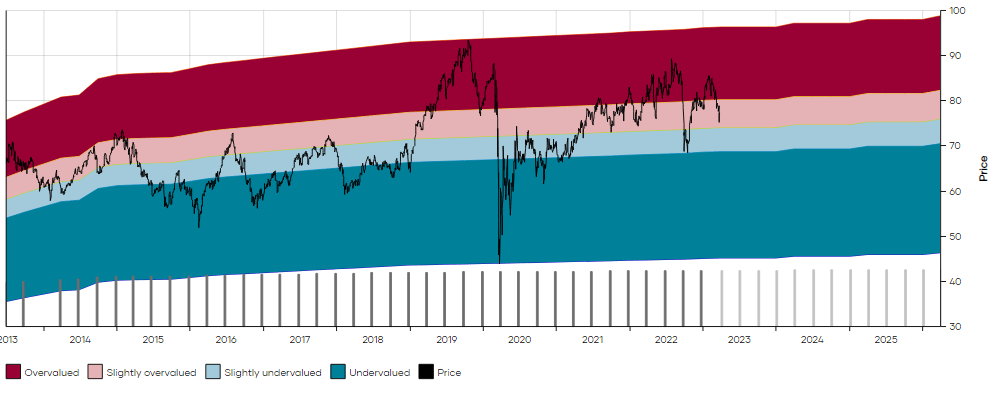

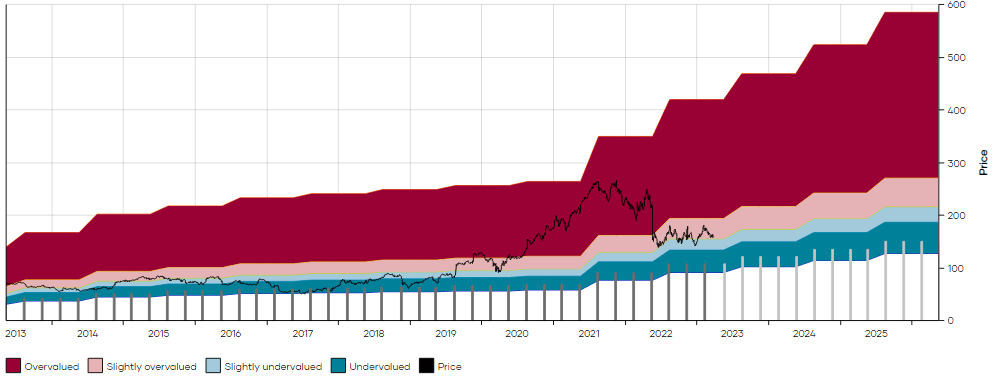

The final stock I'll present today is Target ( TGT ) which currently yields 2.7%, exactly its median historical yield. It ranks among the top 33% of US stocks on momentum. Which seems weird because it is doing awful on a 12 month basis, but its 3 month and 6 month results are vastly superior than most US stocks.

{kind=link}

As I said to members of the DFT recently:

"I continue to see TGT as a great stock to own in the current environment, as stated above, because of both the downside protection from the staples categories, and the upside possibilities if a positive scenario plays out."

TGT segment results (DFT Disclosure Explorer Tool)

The discretionary categories have come down in 2022, but TGT has reshuffled what customers put in their basket to focus more on staples, which has made up for the lost revenue.

Being able to gain market share in staples categories shows that TGT has created a superior experience for shoppers, and has managed to retain them throughout a cycle of shifting consumption habits.

This provides the business with downside protection.

Relative to history TGT is fairly valued. But this doesn't consider the fact that relatively to its history, TGT is a much better run business.

The transition which management underwent on the tail end of the past decade set TGT up for what it is today: A staples company with a discretionary side to it. This provides upside opportunity.

In the current "anything could happen" market, TGT is one of the names I'm most comfortable owning.

Conclusion

Keeping a cold head, and putting maximum chances on your side by combining quality, value, and momentum is a winning proposition.

If you can get paid a healthy dividend with good growth, even better!

Stay the course, and corporate America will take care of you long term.

For further details see:

Panic Never Pays: Avoid These 5 Dividend Stocks And Buy These 5 Instead