WBD - Paramount: An Immensely Misunderstood Linear Networks Business

2023-09-22 09:12:01 ET

Summary

- CBS is a highly profitable, misunderstood, and overlooked asset that is a hidden diamond in the Linear Networks segment.

- Paramount offers immense upside with high downside protection based on a sum of the parts analysis.

- The article offers a deep dive into the Linear Networks business and provides an alternative view to the consensus that "Linear Networks is a dying business model".

"Please Not Another Article About Streaming!" Don't worry, this won't be yet another article mainly about whether streaming will work or not (and yet I won't come around to say a few words about it).

I find it very fascinating that I read dozens of articles about the streaming business and why it will fail or succeed, but to date I have not found a single article that goes into detail about the Linear Networks business, Paramount's (PARA) cash cow. The only thing I read about the Linear Networks business is that it is doomed, which seems to have general acceptance in the investment world and is not (or only marginally) questioned by investors. It literally screams of the phrase often cited by Howard Marks, "If something seems to be too bad to be true, it probably is" But is it? Or is it really as bad as it seems? My analysis is intended to provide a sober look at Paramount's Linear Networks business and describe why I think the company is a long-term investment á la "Heads I win, Tails I don't lose much". So let's start with a deep dive into the asset CBS.

Linear Networks Business

a. CBS

The asset falls under the "linear TV is dying" category on Wall Street and is, in my opinion, a very misunderstood asset, which is far more attractive than it appears. To begin with, here is a brief overview of the performance over the last few years:

Compiled by Author using data from annual reports

It is unfortunately very difficult to get an accurate picture of CBS because 1.) Paramount+ has had a significant negative impact on OIBDA over the entire period (please note that in 2018, the results of each division are skewed by the inclusion of Paramount+, at the time called CBS All Access), 2.) the profitability of each division is difficult to figure out, and 3.) CBS has been integrated into the results of the other Linear Networks since 2022, which means there is no accurate data available for the last year.

However, let's get into the three segments, Advertising, Affiliate and Licensing:

Advertising: The revenue mix consists mainly of advertising during sports programs, prime time/ non-sports programming and news, as well as political advertising. As can be seen historically, revenue in this area can fluctuate greatly, due on the one hand to the cyclical nature of the business tied to the economy, but also due to the rotating broadcasting rights of the Superbowl and NCAA Championship Games, as well as the political cycle.

To better understand the value of the advertising business, it makes sense to break down the revenue into its components:

Sports: According to media estimates , CBS generated around $1 billion in NFL advertising revenue in the 21/22 season. That year, CBS did not have the rights to broadcast the Super Bowl. It is important to note that the Super Bowl alone has an impact of around $550-600 million on the overall result. By my own estimate, the remaining advertising revenue from sports (primarily PGA Tour, NCAA and UEFA CL) accounts for another $700 million+. I assume here that these content rights like the NFL will also be amortized over the entire business and advertising revenue will therefore only account for around 75% of the future license fees (which will be sub $850 million, as will become more clear below). This means that in an off year without the Superbowl, around $1.7+ billion in advertising revenues are generated with sports, and in a year with the Superbowl around $2.3+ billion (excluding the other, smaller sports rights), or about 30-50% of the overall advertising business.

Political Ads: On top of that, there is political advertising. Here, too, the actual revenue is very difficult to estimate. Political ads are generally very high margin (according to our own estimates well above 50%+), which has the very simple reason that politicians do not think in terms of return on investment in the economic sense, but in electoral votes, which means that the financial incentives will always be to use the raised capital as extensively as possible. According to my own analysis, based on business reports from the big four broadcasters CBS, Fox, ABC and NBC, as well as owners of tv stations such as Gray Television, I estimate the bottomline impact to be around $350-450 million, so political ads revenue should be conservatively somewhere around $800 million+ in political years.

The remaining revenue is divided between news and other programming. I estimate that in 2022 advertising revenue was around 4.8-5 billion due to the lack of revenue from several sporting events, offset by political ads.

This means that on an adjusted basis >50% of Advertising revenue comes from revenue sources that a) are very acyclical and b) historically show an upward trend in Advertising spending. Only <50% of the Advertising business is thus affected strongly by secular decline. And CBS, as the broadcaster with the largest reach and the highest rated content, should be even less affected than its peers, as will become clearer later.

Affiliate: The second misunderstood part of CBS. In a nutshell, affiliate revenues represent revenues from MVPDs (cable, satellite, etc.) and vMVPDs (YouTube TV, etc.) as well as revenues from local TV stations (also called affiliate stations).

To specify this: MVPDs/vMVPDs compensate the TV stations owned by CBS (currently CBS owns 26 TV stations) for the right to retransmit the program, while local tv stations pay CBS as broadcaster for the right to broadcast the program.

Therefore, there are three relevant players in the distribution chain: Broadcasters (CBS, NBC, ABC, Fox), local TV Broadcasting Stations (Gray Television, Nexstar, etc.) and MVPDs/vMVPDs (e.g. Comcast, YouTube TV). Broadcasters charge fees to local TV broadcasting stations (reverse comp), which in turn charge fees to MVPDs/vMVPDs (retransmission revenue). Affiliate fees thus represent a cost block for MVPDs/vMVPDs, while they generate revenues for local tv stations and broadcasters.

The distribution of power is easy to understand: Broadcasting programming is essential for MVPDs, because to put it bluntly, without sports programming there is almost no reason for the masses to still use cable TV. Not broadcasting sports programming is unthinkable for linear TV providers, as it would lead to churn being even higher than it already is. TV stations, on the other hand, serve only as an intermediary. Apart from broadcasting the programming they do not add any value to the supply chain and therefore do not have much of a say, but they do participate in the pie to a certain extent by passing on the affiliate fees they receive from the broadcasters (reverse comp) to MVPDs (retransmission revenue). The broadcasters as owners of the content rights have the clear position of power and therefore the dominant bargaining position. As Bill Gates likes to quote: "Content is king".

This is also historically reflected in P&L statements. MVPDs have increasing costs and decreasing margins, as it becomes more and more difficult for them to pass on the TV stations retrans fee increases to the end customers (especially under falling subscriber numbers). TV stations, on the other hand, are making increasing profits in absolute terms, but are making ever smaller margins, as they can only pass on the affiliate fee increases to a share of <1. Broadcasters (like CBS) are happy to renegotiate prices on average every three years and in the meantime benefit from annual price increases with high incremental margins (while this is not directly clear, the margins should be WELL above the 15% EBIT margin that CBS achieves, as affiliate fees require almost no incremental costs). CBS, acting as a broadcaster, generally charges fixed fees and, acting as a broadcasting TV stations owner, has built escalators into the contracts to counteract the loss of customers. This is different for ABC, for example, which uses variable contracts and is negatively affected by subscriber losses.

According to own estimates, reverse comp conservatively accounts for >70% of affiliate revenues, while retrans revenue accounts for <30%, which minimizes the downside risk from subscriber losses enormously.

The bull thesis vor Broadcasters and local TV stations owners is that broadcasting has around 30% of viewing time on pay TV providers, but only has a revenue share in the high teens. This gap has been attempted to be reduced in recent years and will probably continue to be closed in the future. Based on the historical development (CBS sales are skewed, but retrans fees of TV stations have grown with ca. 6% CAGR in the last 5 years and historically with well over 20%), I expect that the segment will GROW with 5-10% and high incremental margins in the long run, starting from ~$3 billion in 2023.

Licensing: In brief, CBS licenses the content it produces to any possible content provider. Unfortunately, there is very little information on this division. However, revenues can fluctuate greatly and are very lumpy, as IPs are licensed on an irregular basis, and are furthermore (apart from some productions) associated with very low margins. Based on historical development, I assume that licensing will neither grow nor decline.

CBS in the long term

Now that we have understood the drivers, let's move on to a way to think about the business in the long term.

CBS continues to own the rights of the NFL through 2033 (with average rights-costs of $2,1 billion per year), while being allowed to broadcast the Super Bowl for the 2023, 2027 and 2031 seasons, as well as the AFC in every year. CBS also owns the TV rights of the PGA Tour until 2030 (~$250 million), the rights of the Big Ten (football as well as basketball) from 23/24 onwards until the 29/30 season (~$350 million) and the rights of the UEFA Championsleague until 2030 ($250 million).

It is important to note that the market is afraid that CBS will experience a bottomline hit of around $1.5 billion in the worst case due to license renewals beginning 23/24, as the new contracts for NFL (+$1.1 billion), Big Ten (+$300 million) and UEFA (+$150 million) will be in effect. However, as contracts are usually based on annual price increases, I expect the hit to be significantly lower, as the published cost of rights only indicates the average over the period of the contract.

To highlight this point with the NFL as an example, because I think this is greatly misunderstood by investors and the media: When the media reports that NFL right costs are increasing from $1.1 billion to $2.1 billion, they are referring to the average for the period of the contract, since explicit contract terms are typically not communicated. This means that the cost this year for NFL rights will be WELL above the $1.1 billion average for the contract period ending 22/23 and then WELL below the $2.1 billion average for the contract period ending 32/33. There will likely be a one-time bump up in cost, but by no means the $1 billion implied by first level thinking!

So on the cost side, you have rising license costs in the long-term and in addition secular decline in the topline. But at the same time, you have immense tailwinds, both in 2024 and long-term. If you look at 2024, this is the first year CBS is going to air a Super Bowl, Big Ten Championship Games, more UEFA CL Games and the U.S. elections at the same time. Simultaneously, you're going to get higher affiliate revenues, which will come with very high incremental margins. According to my own estimate, this will more than compensate for the headwinds and lead to EBIT GROWTH instead of EBIT decline. So what does this mean in concrete numbers?

The bottom line of CBS next year overall is probably impossible to predict due to the many drivers that will impact the bottom line. An unsatisfactory answer, isn't it? Nevertheless, I would like to share a few thoughts.

I estimate that CBS' current EBIT, adjusted for Paramount+, to be around 1.8-2 billion. As I mentioned before, I see a high probability that EBIT will grow next year, because especially political ads and affiliate revenues are associated with very high margins/incremental margins and also mentioned sporting events are aired, which also have a significant impact on the bottom line. So you have tremendous tailwinds in 2024. The tailwinds will be largely non-existent in 2025, temporarily potentially leading to a significant cut in profitability. How much? No idea and I don't think anyone knows.

Still, it's worth pointing out that CBS has huge long-term benefits. People will always consume sports, while costs for sports ads will very likely rise steadily over the next decade. Sports as a commodity is still very valuable for companies, since due to scarcity and almost no vulnerability to disruption holders of the rights are in a very advantageous negotiation position with advertisers. CBS has (especially with the NFL) some of the most attractive sports rights for the next decade, with all licensing contracts already negotiated, which makes the business in sports overall predictable.

The same is true for spending on political ads, which has been rising for a decade and will likely continue to do so for the next decade. CBS, as the largest broadcaster with the largest national reach, will benefit greatly and is expected to continue to do so, making the political ads business more or less predictable. In addition, as described earlier, affiliate is also predictable.

The component that is least predictable is the secular headwind, primarily in the news and non-sports programming business, which accounts for <50% of the ads business. However, it bears repeating here that CBS is probably by far the most attractive of all broadcasters in this business.

So will CBS still be around in 10 years? The probability is more than very high. Even as CBS declines in viewing time in the linear networks model, viewing time elsewhere (vMVPDS and streaming services like Paramount) continues to increase, counteracting secular decline and therefore minimizing CBS's downside risks. So maybe CBS won't exist with the profitability of today (this is also debatable), but most likely the asset will hugely profitable for many years to come. According to my own estimates, it is realistic that the business will generate an average of >1.5 billion in EBIT in the coming years. This is below today's levels and is therefore conservative in my view. Why?

Contrary to the headwinds, primarily due to rising licensing costs and secular headwinds, there are long-term topline tailwinds due to 1) sports/political advertising, 2) affiliation fees and 3) secular TAILWINDS due to vMVPD/streaming, which makes CBS more valuable for advertisers also in news and non-sports programming. All in all, I think this will lead to a slightly declining to constant bottom line, conservatively estimated on a net basis.

Doesn't seem like a dying asset, does it?

For a premium asset with the quality of CBS, a valuation of 10-12x EBIT therefore is in my opinion accurate. This means that CBS should be valued at between $15-18 billion today. The valuation is a premium to ABC , however, this should be justified due to the higher scale and brand value of CBS.

In addition, there is the CBS Broadcast Building. The asset is a very attractive 860k sqf asset in Midwest Manhattan. Paramount sold a comparable building (Television City) in 2021 for $760m. I personally estimate the value to be between $750-1000 million, considering Manhattan real estate prices. The business is currently for sale and will generate additional cash, bringing the total value of CBS to $15.8-19 billion.

b. Linear Networks

I view this segment with a more pessimistic eye. First, to the numbers, which include BET, Showtime, Paramount, MTV, Nickelodeon, Comedy Central and all of the other networks:

Compiled by Author using data from annual reports

In this segment, too, the exact figures are difficult to determine because 1.) BET+, Pluto TV, Showtime+ and the other streaming businesses (excluding Para+) are included in the result until 2021 (here, as again, 2018 must be adjusted) and 2.) here, as well, the profitability of the individual businesses is difficult to work out.

Broken down, Linear Networks too consists of the Advertising, Affiliate and Licensing segments:

Advertising: Advertising is unfortunately less attractive than at CBS, as the linear networks unfortunately cannot compete with the sports assets that CBS has to offer. Linear TV is less and less attractive for advertisers (except in years of political elections, where a high reach is required) and I guess this trend will continue going forward. How powerful? No idea, and I don't think anyone knows.

Affiliate: This is no different for affiliates. Affiliate fees in this segment look a little different from CBS. In a nutshell, Linear Networks receive a variable fee from MVPDs that is tied to the subscriber count. The trend in this area is relatively simple to understand. Linear Networks increase fees while subscriber counts fall. Historically, however, fee increases have not been strong enough to offset subscriber losses, which equates to falling revenue and profitability for Linear Networks. Will this trend continue? Very likely. In any case, there is no reason to believe otherwise at this time. How powerful? No idea, and I think the answer is also written in the stars here.

Licensing: There is not too much to say about Licensing, but there has been a boost in recent years, driven in part by production for third parties. Revenues and thus profitability can fluctuate greatly and tend to be very lumpy. As an example, take South Park, which was licensed in 2019 for $500 million for 2020-2025, with an EBIT margin close to 100% (Paramount has a 51% JV share, so $250 Million in EBIT for Paramount). If Paramount licenses the IPO again in 2025, it can take a very strong impact on the EBIT margin of that year. My guess is that the licensing business will develop in a very lumpy way going forward.

So what will the segment return in the future? You probably don't want to hear it, but I don't have the slightest idea. Will the EBIT of the business and therefore the FCF decrease? I think in all likelihood the answer is yes. How much? I don't know and I guess probably nobody has a clue. But will the business still exist for the next five years? Of course, no transformation goes within a couple of years. Bulls would say (if there are any) that subscriber losses will slow as the older generation is not ready to switch to streaming, which would mean that linear networks will continue to generate cash flows for many years. Evidence shows that viewing time has actually even increased for people >65. Will it still exist in ten years? The question is more difficult to answer, but it is clear that the business will serve as an attractive cash cow for most of the way until then, as management will squeeze every penny it can out of the business.

Overall, it should be noted that the business today generates about $3 billion in EBIT. In my opinion, a valuation of 4-6x EBIT is an appropriate valuation for a declining asset, resulting in a valuation of $12-18 billion. Compared with other linear networks assets, which are mostly trading at high single digit EBITDA multiples, this valuation should be considered as very conservative.

Even if the business goes completely bust, you still have very valuable IPs, like Spongebob, South Park and co. that can be licensed for years and bring in cash flows per the Sony model. And this is just one of many creative ways to generate cash flows in a worst-case scenario. I think the market reaction is way too hyperbolic.

Streaming

My thesis on streaming is very unconventional and is very much based on the view of Warren Buffett and Charlie Munger, who discussed streaming at their Berkshire Annual Meeting . In a nutshell, I personally believe that streaming is a commodity product. Streamers serve a limited number of eyeballs with an infinite supply of series and movies, which makes the various streaming providers seem very undifferentiated overall, while converging over time to an even more undifferentiated supply as content spending remains very high. Fundamentally, streaming is thus not a good business given high competition in a saturated market, but can become a good business through 1) price increases or 2) consolidation. 1) implies an oligopoly, 2) the evolution towards one.

Price increases: For price increases to be successful, they must happen across the board because, assuming a commodity market, subscribers will otherwise switch to an alternative, cheaper streaming service. This will not happen, however, as there are short-term incentives to reduce the price in order to gain customers and achieve a higher benefit at the expense of the other streamers. Thus, in game theory terms, prices are kept low in anticipation of competitor decisions, which is rational for all competitors, but still disadvantageous (the result is paretoinefficient), since all competitors would be better off with higher prices. However, the less competition there is in the market, the easier indirect coordination becomes, and hence the more likely it is that players will collectively raise prices, as the risk of short-term profit maximization through price deviation at the expense of long-term profit sacrifice becomes smaller. I think two aspects are very interesting in this regard:

1) Gunnar Wiedenfels speaks openly about the issue since the beginning of the year and has the strong opinion that streaming providers offer too much value for too little price and ergo price increases would be rational.

2) Every streaming provider (excluding tech) has raised prices in the last 9 months. Disney with its recently announced second price increase continues the trend. It is not unlikely that tit-for-tat is currently being played to test oligopolistic tendencies. Overarching price increases mean that as a consumer, there is no incentive to switch streaming providers, as there is not much of a cost advantage.

So are we already in an oligopolistic market? I don't know, but there are a few reasons why not: Supply goes beyond the big 5 with tech players and smaller providers, high churn could lead to incentives to reduce prices again, lack of scale with small providers, etc. Overall, I think price trends are probably impossible to predict. Accordingly, it remains to be seen how the market will develop.

Consolidation: If price increases do not work, the only thing left to do is consolidation. Consolidation reduces competition and ergo increases the chance of being able to raise prices in the future. Paramount, along with Peacock, is an attractive takeover candidate as one of the two smaller suppliers, but any consolidation is beneficial to the industry and especially to Paramount. It can be seen that there is already a lot of consolidation going on (Showtime, Bundeling, etc..).

What happens if none of this materializes? This would be unfavorable for all competitors and streaming will remain the unattractive business it currently is. Will this happen? Of course, anything is possible, but I think it is unlikely, as there are almost no incentives to do so in the long run.

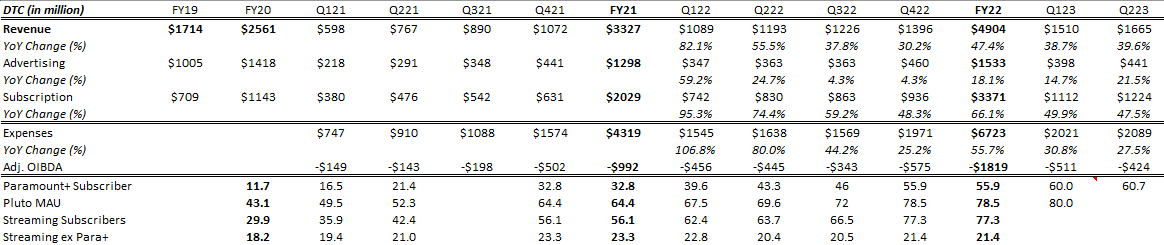

So will Paramount's DTC business become profitable? First, let's look at the numbers:

Compiled by Author using data from annual reports

{kind=link}

To give the answer: I don't think so. Personally, I think the probability of the business not becoming profitable is higher than it becoming profitable. Why? Lack of scale and little pricing power due to high competition.

For my valuation, I therefore assume a total negative value of $4 billion. The business will probably generate a loss of around $2 billion this year, of which >1 billion has already been taken into account. I assume that the loss will be strongly reduced in the next years by 1) the integration of Showtime (up to $700 million), 2) the announced less spending and 3) growing topline. Furthermore, I assume that management will act rationally and not finance a loss-making business ad infinitum. With the financial incentives set for Sheri Redstone and Bob Bakish and the involvement of Warren Buffet, anything else would be irrational in my opinion. Accordingly, I consider a negative value of $4 billion to be justified and conservative, and positive surprises are not priced into my valuation.

To give an example for a positive surprise: Not included in my valuation is PlutoTV, which could be enormously valuable for Paramount in the coming years. PlutoTV is a $1 billion+ advertising business that was acquired in early 2019 for $340 million. The business has since scaled from 12 million MAU to ~80 million MAU and is accordingly many times larger than it was a few years ago.

Filmed Entertainment:

Let's move on to the last part of Paramount, Filmed Entertainment. The business consists mainly of Paramount Studios and is responsible for Paramount's theatrical releases. Accordingly, the business is enormously volatile in both the top and bottom line:

Compiled by Author using data from annual reports

{kind=link}

What is the value of Paramount Studios?

To be conservative, I compare Paramount Studios to MGM, which was sold to Amazon for $8.5 billion in 2022, and value the asset at the same price. I do consider that as conservative, as Paramount Studios is significantly larger than MGM and, in my opinion, the IP is significantly more valuable.

Downside protection: In addition to the IP, the studio owns Paramount Pictures Studio in LA, which totals 62 acres at 1.85 billion sq ft. The building can be compared to CBS Studio Center (LA, 40 acres in size), which was sold in 2021 for about $1.85 billion. It can be assumed that as a premium asset, the asset is worth at least as much, if not significantly more. So PPS alone could potentially be worth $2.5-3 billion. So even if I am wrong with my estimate of $8.5 billion, there is a huge downside protection due to the real estate value underlying it.

Valuation

Let's get into the SOTP valuation:

Author´s calculations

Included in cash is the sale of Simon & Schuster for $1.3 billion (= Net Proceeds).

Based on my valuation, this provides an upside potential of 110%-260%, or 2x-3.5x. .

Risks

A Turning advertising cycle in addition to a strongly depressed market leads to declining cashflows in the short term. However, the advertising market is highly cyclical and should reach a higher level in the medium to long term.

A decreasing bargaining power in the affiliate business, especially at CBS, causes a significant cash flow driver to weaken, which would invalidate my thesis.

Long-term rising streaming costs combined with the absence of a decision to close the business will result in Paramount generating significantly less cash than expected and therefore invalidate my thesis.

National Amusements insolvency would cause short term selling pressure and therefore a declining share price. However, this would not impact the fundamentals of the business.

An ongoing writers strike involves the risk that Paramount's services will become less attractive to customers, which may in particular jeopardize the streaming services business.

Conclusion

I think CBS is an overlooked and misunderstood asset within Paramount that, in combination with the Linear Networks business, is going to generate significantly more cashflow than the market expects. At the same time, there is significant downside protection due to the asset value as described, which leads to an investment case a la "Heads I win, Tails I don't lose much".

For further details see:

Paramount: An Immensely Misunderstood Linear Networks Business