CA - Paramount Resources: Cashing In On Condensate

2023-11-24 07:31:23 ET

Summary

- Paramount Resources has transitioned from a dry gas producer to a rich gas producer focusing on condensate production, which is a premium product in Canada.

- The company's emphasis on condensate production gives it a significant advantage over competitors, leading to superior profitability and cash flow.

- PRMRF has a debt-free balance sheet, allowing it to pay a dividend while continuing to grow production and manage through cyclical downturns.

- Paramount Resources is also in a position to benefit from rising natural gas prices.

- The condensate production raises the recycle ratio to demonstrate above-average profitability.

Paramount Resources (PRMRF) (POU:CA) long ago sold most of its dry gas production and then used the proceeds to purchase Apache Canada. This was a division of Apache ( APA ). In the roughly six years since that purchase, long-time readers know that this company has gotten that purchase price back several times over as I followed the progress through the years. Now, the balance sheet is debt-free.

Management has changed from a dry gas producer to a rich gas producer and now to a rich gas producer focusing on producing condensate which is a premium product to oil in Canada.

That means this company can cash in on the premium production of condensate in Canada while rewarding shareholders with a decent dividend that will likely continue to grow. Condensate is one of the few premium products to oil in Canada (where this company is located and hence reports in Canadian dollars ).

Canada is often short of the condensate it needs and, therefore, must import condensate that is used to mix with thermal oil and heavy oil to make the products flow through pipelines to their destination.

Therefore, a company like this one that has material condensate production often has superior profitability and generous cash flow.

Returning To Growth

I had previously mentioned that the hard Canadian winter followed by summer wildfires interrupted the growth plans of the company in fiscal year 2022. Now with another winter on the way when many Canadian companies get a lot of "work done", this company can get back to business.

Production Profile

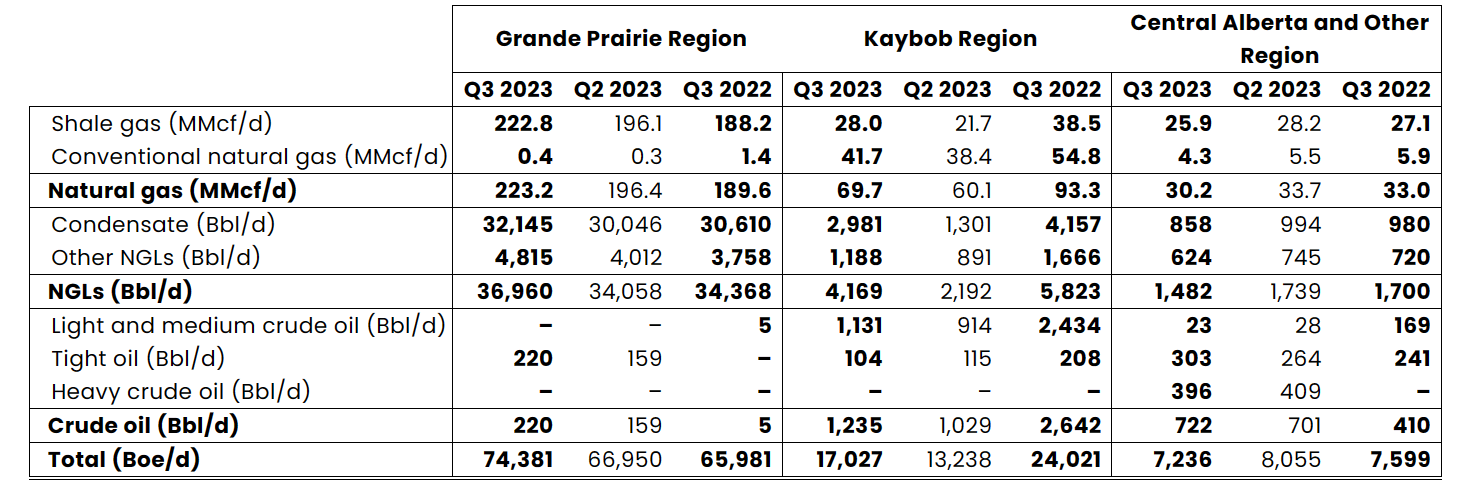

The company has moved to rich gas production. As noted above, the rich gas in many ways "specializes" in having mostly condensate for that "rich gas" classification. That is an "ace in the hole". Just look at the relative volume of condensate below. It makes competitors drool because this rich gas production is far more valuable in Canada.

Paramount Resources Production Profile By Key Area (Paramount Resources Third Quarter 2023, Earnings Press Release)

{kind=link}

Long term, the company will be in a position to benefit from rising natural gas prices as North America increases the ability to export natural gas to the rest of the world.

But, in the immediate term, the company benefits far more than many rich gas producers through its production of condensate which sells at a premium to light oil. Therefore, when oil prices are as strong as they are now, this company has an unusually profitable production selection of products.

Most companies I follow that have rich gas production usually have a fair amount of natural gas liquids like ethane and propane that likewise will usually benefit from rising oil prices. But these products typically sell for a fraction of the light oil price (as opposed to the premium condensate commands).

Having such a product like condensate is even more valuable than oil production. As long as condensate is a significant part of the production, the advantage over competitors in terms of profitability and a shorter payback period as well as cash flow compared to competitors that do not produce as much condensate or produce no condensate. For a company like Paramount, cash flows under some extreme industry conditions.

The result of this is a cash flow bonanza that allows the company to pay a dividend while growing production. Most companies I follow do one or the other. Best of all, this situation is enhanced with a long-term debt-free balance sheet.

Relatively Large Netback Percentage

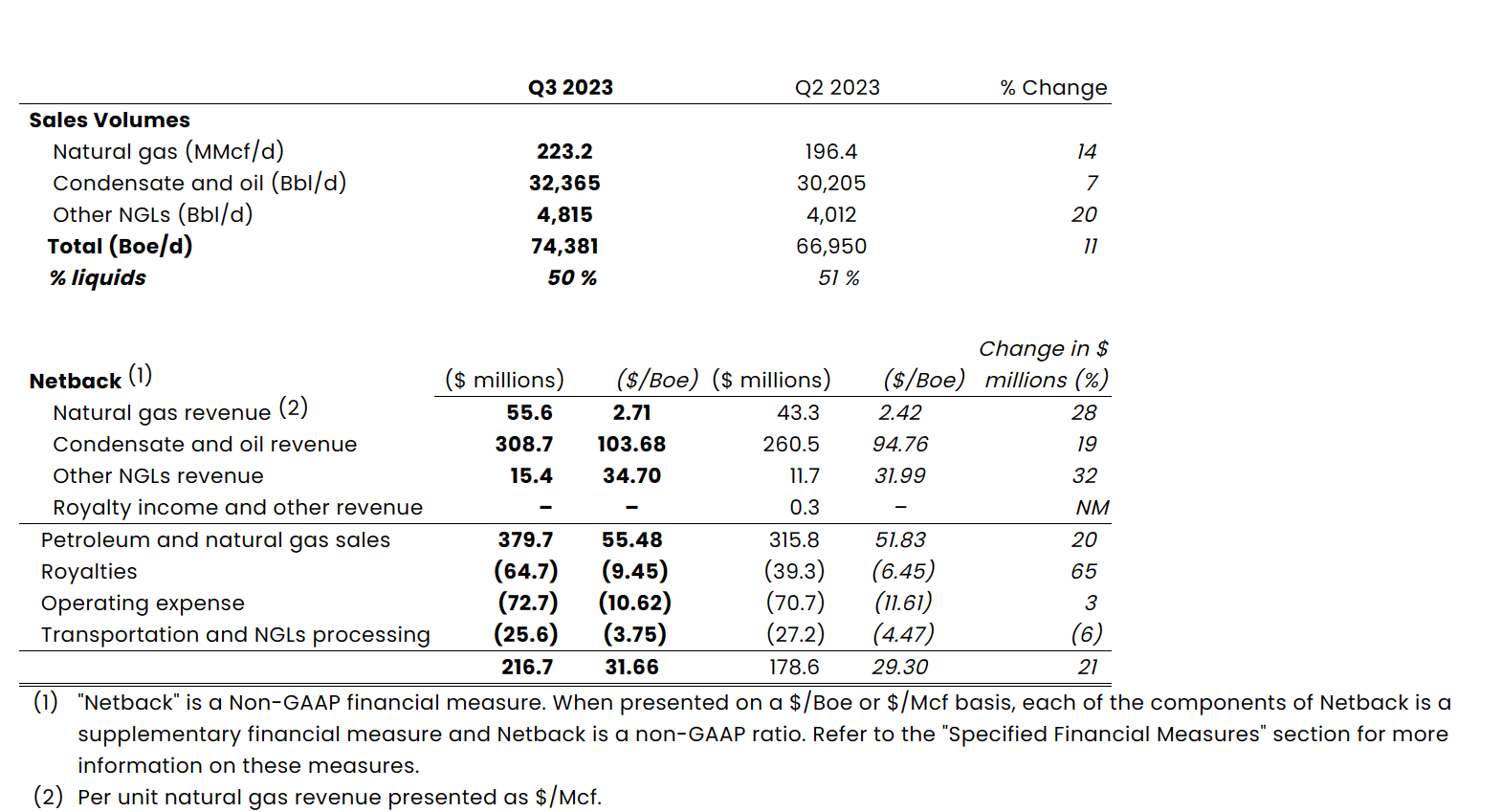

It will, however, take some time for the market to get used to this cash flow generator. Notice the effect of condensate in the production mix as shown in the overall netback calculation below:

Paramount Resources Netback Comparison Of Third Quarter To Second Quarter 2023 (Paramount Resources Earnings Press Release Third Quarter 2023)

{kind=link}

The result of this emphasis on finding some condensate as part of the rich gas production is the unusually large percentage of the revenue as netback. Notice that the per barrel netback is more than half the beginning average selling price per barrel. That is an extraordinary margin.

That margin can make for a very profitable company with extremely low breakeven points as long as the wells are not too expensive to drill and complete. Given the long-term debt-free balance sheet, those wells likely have a high profitability.

Profitability

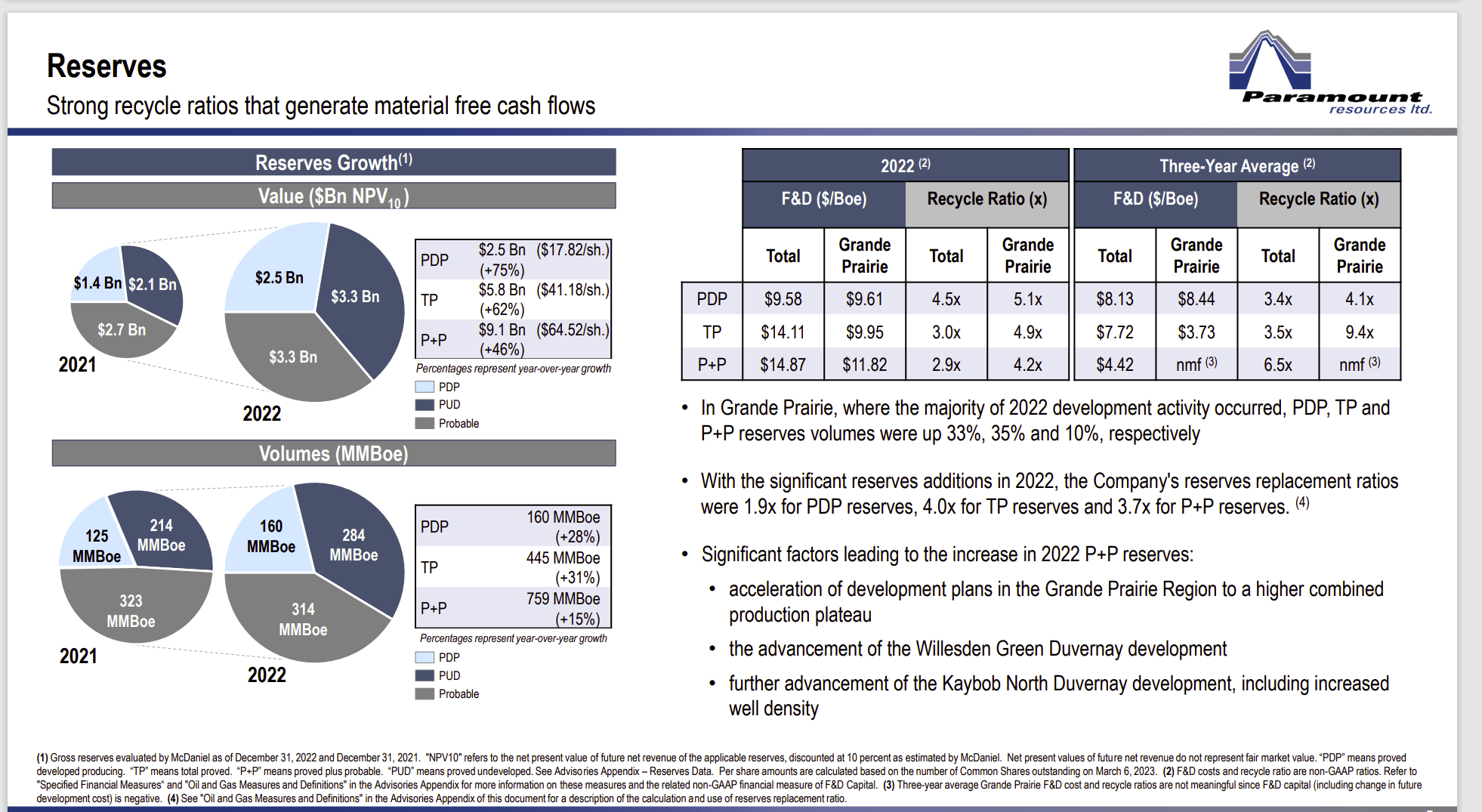

The company has an above-average profitability as measured by the recycle ratio. That should be expected given what we have seen so far.

Paramount Resources Business Overview And Profitability (Paramount Resources November 2023, Corporate Presentation)

{kind=link}

The recycle ratio is the profit (as in netback) per barrel of oil divided by the finding and development costs per barrel. The ratio needs to be at least one for the company to stay in business. As shown above, this company is quite a bit more profitable than that. In fact, a recycle ratio that high is not all that common.

The debt-free balance sheet allows the company considerable leeway to decide how to manage through the cyclical downturns that periodically affect the industry. This company does not have to worry about servicing debt. Therefore, management can cease all activities if the downturn is severe enough and just "cash checks" from existing production until the next cyclical recovery begins.

Project Lifecycle

This company is atypical in that it will sell whole projects if the costs of production climb too high. That is actually close to the Exxon Mobil ( XOM ) way of doing business. This management in the past has gotten darn good prices for anything it chooses to sell.

The other, this management has, is an investment portfolio of other public and private companies. Some are wholly owned by the company while others are a joint venture or a material presence in a public company.

Management will sell and purchase new investments from time to time. Or management may make an offer to acquire one or more of the portfolio companies. So, there is a mutual fund or BDC aspect to part of the company's business.

The Ghosts Of Years Past

This company used to develop acreage or otherwise maximize the value of the acreage while acquiring debt in the process. It was one of the few companies that succeeded in doing this after the large oil price decline of fiscal year 2015.

What has changed is the focus on liquids produced with natural gas. This company has moved from dry gas production to rich gas production. You now have rich gas production focusing on a relatively large amount of condensate and not much else. This is a profitability improvement that the market has not yet fully valued.

Combine that strategy change with a switch from the past strategy of selling the developed acreage while keeping some production to eliminate debt (and then start the process all over again).

The price of the stock has languished because of that debt-ridden past. Now that the balance sheet has a negative net debt position, I would expect the market to notice the strong balance sheet going forward as well as the ability to grow production and pay a dividend without acquiring debt. The company has far more and very profitable production than it did in the past.

Summary

This company kept changing production strategies for the better. But Mr. Market has to catch up to the latest strategy. The cash flow here is unusually large for the amount of production. Once the market figures that out, the stock price could revalue quite a bit.

This company will be far more financially conservative in the future. The production now generates decent cash flow to minimize the necessity of debt in the future. At some point, a well-run company like this one could become an acquisition candidate for the right price.

In the meantime, the Apache Canada assets that were acquired still have a lot of possibilities to keep this management busy for a very long time to come.

Therefore, continued growth as well as a growing dividend are likely in the future. It is a monthly dividend with a generous C$.125 per share dividend. The dividend was recently instituted and is growing rapidly. The condensate premium gives this dividend a survival edge in a cyclical downturn.

The severe Canadian winter this year followed by the fires impacted the company's production levels and cash flow. Next year could have a much better profitability as a result. Next year will also have to recover from the lost drilling days of the current fiscal year. It, therefore, may not be so easy to show production growth after a fiscal year like this one (but only for one year).

Still, natural gas production will be very profitable in the first and fourth quarters of the fiscal year. Therefore, the best may be yet to come.

This company can be considered a strong buy as family-owned companies like this one tend to be managed conservatively and outperform the market long term. Long-time readers know that the founder passed away some time back. However, the family is still actively involved in managing the company.

The conservative finances limit the typical upstream risk as does the unusual profitability of the wells. It will take time for the market to realize that the company is not going to leverage up anymore to develop the remaining properties. Waiting for that realization could prove very profitable once the stock is revalued for the now conservative management and likely more consistent future growth and dividend.

For further details see:

Paramount Resources: Cashing In On Condensate