CA - Paramount Resources: Inflation Beating Dividend And Growth

Summary

- Finances are conservative with a debt ratio way under 1.

- Production growth rate for the fiscal year is near the top of the industry.

- Long-term production growth will be likely in the high single digits.

- Dividend growth has been rapid as well. The dividend remains a very small part of cash flow.

- Insiders own nearly half the stock while continuing to turn around the acquisition of Apache Canada.

(Note: This article was in the newsletter September 22, 2022, and has been updated as needed.)

(Note: This is a Canadian company that reports in Canadian dollars unless otherwise noted.)

Paramount Resources (PRMRF) is one of the few companies that got through fiscal year 2021 basically ready to grow. Some of this is due to the ownership structure that allows management to balance market demands with long-term goals. Another is that this company has some darn good acreage that will allow for both production growth and dividend growth.

There are a lot of companies in the industry that are bowing to market demands to give back the excess cash generated while prices are high. This has created an opening for companies like this one to take advantage of strong commodity prices to sell even more product. That means growing production which will enable the dividend to grow even more in the future.

I have long been an advocate of finding companies that both grow (hopefully rapidly) while growing their dividend at a similar pace. Many times, this provides the investor with growing income and increasing wealth. Growing companies are often at far less risk of dividend cuts as well. During times of inflation, this is an inflation proof way to maintain purchasing power.

Back in 2017, Paramount Resources acquired Apache Canada . This acquired division had long been ignored by Apache ( APA ) and finally dumped at what turned out to be a bargain price.

Long-term followers know that Paramount took an unusual route to improve operations in this relatively giant project. Management borrowed money time and again and then sold the improvements, while keeping some production, to finance the next leg of improvements. Now, finally there's enough cash flow for management to continue to develop and improve the remaining part of the original purchase.

That means that finances are unlikely to be stretched in the future (followed by an asset sale to bring things back into line). This change in financial strategy will take a while for the market to "catch-on." In the meantime, until Mr. Market notices, investors can enjoy growing production as well as a rapidly growing dividend.

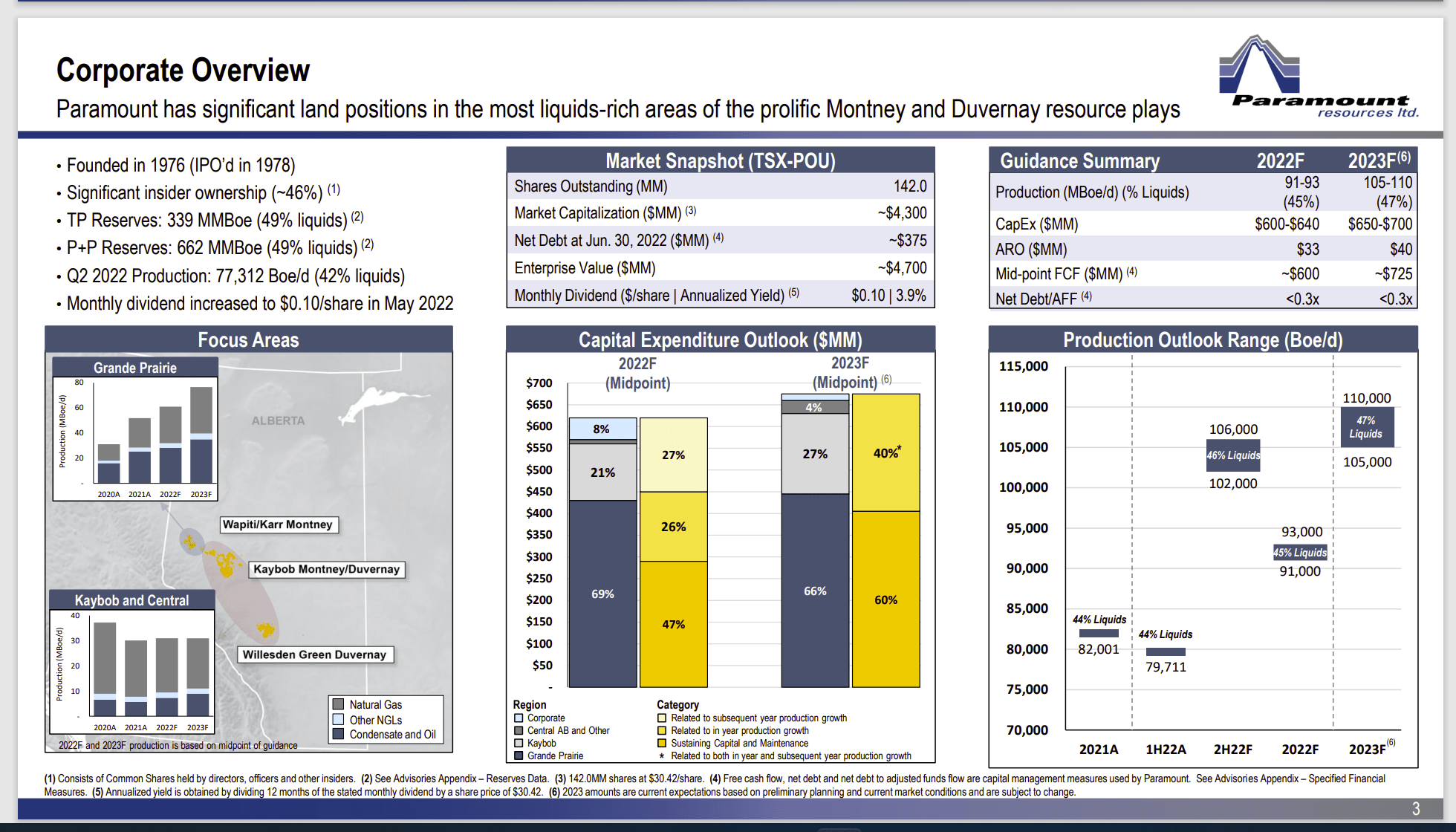

Management reported 77,312 BOE/D during the second quarter of fiscal year 2022. That same management is guiding to an eventual production of more than 100,000 BOE/D. Growth like that protects the dividend during an eventual cyclical downturn. The reason is that management bases the dividend on current cash flow and then raises it along with cash flow increases. Growth like the amount shown above is going to be allowing for some significant dividend increases from the current C$.10 per share per month. That makes this issue a suitable income consideration for a wide variety of investors.

Management also announced an acquisition of about 90,000 acres with a little bit of production as well as a divestiture. Management then participated in a private placement to acquire more securities of another company. This management has been known to acquire the whole company when it has ownership interest like that. It also may sell that interest depending upon market conditions.

Financial Safety

This management no longer needs to finance continuing operational improvements with debt. The currently robust commodity price environment has taken care of that need.

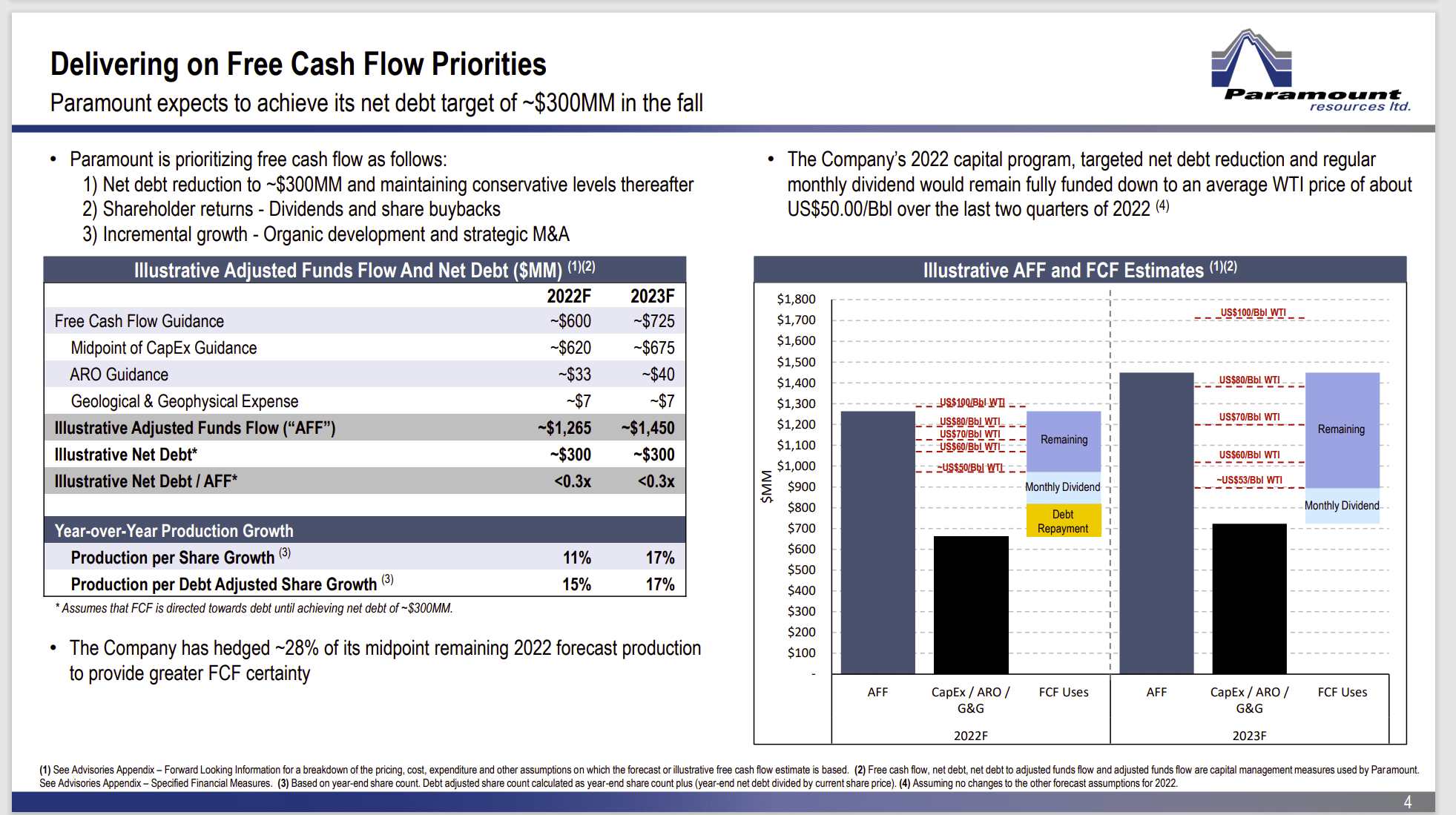

Paramount Resources Free Cash Flow And Debt Guidance (Paramount Resources August 2022, Investor Presentation)

{kind=link}

Debt is not only at conservative levels for the current environment. Those debt levels will be conservative at oil prices about half the current environment. That's more financial protection for the dividend and the finances than much of the industry currently offers. It's not going to take a lot of debt repayments for management to meet the goal shown above. So, a lot of dividend growth is likely to happen sooner rather than later.

More importantly, the balance sheet and production growth appear to have the priorities. That makes long term dividend growth (even in a cyclical industry) a viable proposition. Long term, management wants to grow production in the higher single digits. That makes for an attractive return in the teens long-term from the dividend and capital appreciation for a company this size.

Overall Considerations

The family of the founder (who passed away a few years back) has a significant interest in the company.

Paramount Resources Business Summary And Insider Ownership Percentage (Paramount Resources August 2022, Corporate Presentation)

{kind=link}

Insiders clearly have an interest in the success of this company. They also own enough stock to be firmly in control. There are a lot of studies that demonstrate that family-owned companies tend to out-perform the market with conservative financing. This company appears to fit that description very well.

Management has focused on getting a better price for the products produced. The result has been a lessening dependence upon some areas like AECO while increasing the exposure to some more lucrative markets. A future possibility is the ability to export and join the very strong pricing of the world market.

Similarly, when I first began following the company, this company was largely a dry gas producer. That strategy has switched to more liquids with an emphasis on condensate. Canada often must import condensate to meet the needs of the thermal and heavy oil producers. Condensate is often mixed with those products so that they flow through pipelines to refineries.

The result of this is that condensate often trades at a premium to WTI pricing for oil. That can result in superior well profitability. In the current environment, management can usually drill at least two wells with the same capital money in a fiscal year to provide rapid cash flow growth. That likewise implies a lot of future good news for the dividend.

A last consideration is that this company does have investments in other companies. That part of the company often functions like a mutual fund with one important difference. This company will from time to time offer to acquire shares it does not own of one of the companies in a business combination. It also can dispose of shares or sometimes acquire debt.

The Future

This Canadian producer took on a relatively huge project when management acquired Apache Canada. It has taken years to improve a lot of things and there is still a lot more room for improvement and development. Growth prospects for this company are relatively bright.

One of the few things that management does not do is road shows. Therefore, a lot of company promotion really does not occur with this company from that avenue. But the operational results are good enough and the company is now large enough to attract some decent institutional attention.

The introduction of a dividend combined with the production growth makes these shares suitable to a wide variety of long-term investors. A current investment in a situation like this is likely to provide a fairly generous income along with a more valuable investment by the time retirement is on the horizon.

Canadian companies tend to have a far more flexible view of dividends than US companies have. But the dividend is such a small part of cash flow that the company may take a view that is similar to the view of United States companies in that the dividend will likely be maintained during downturns (unless that downturn is really severe like 2020).

In any event, this is a company promising a combined return in the teens for the foreseeable future. Companies like this tend to become acquisition candidates at the right price. If that happens, it would be "icing on the cake." The conservative finances make the investment risk considerably lower than is the case for many upstream companies.

For further details see:

Paramount Resources: Inflation Beating Dividend And Growth