CA - Parex Resources: Attractive But I'm Hoping For A Bigger Pullback

2023-12-12 10:30:00 ET

Summary

- Parex Resources has shown strong financial performance and overall health due to a strong oil price and good production results.

- The company reported a net profit of just under $120M and an EPS of US$1.13 in the third quarter.

- Parex has embarked on an investment program to increase reserves and average annual production rate, with a full-year capex of $450-$475M.

Introduction

Parex Resources ( PXT:CA ) (PARXF) was one of my favorite oil investments during the COVID crisis in 2020 when oil prices were exceptionally low. I argued the company's extremely healthy cash balance would protect the company's existence and allowed it to wait for better times. That indeed happened and although Parex has to be careful in navigating the sometimes volatile Colombian political waters, the company's financial performance and overall health is still very strong .

A strong oil price results in a strong cash flow result

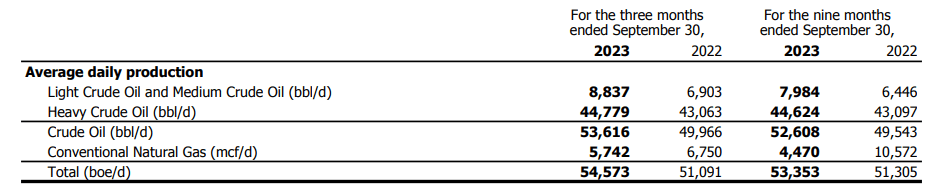

During the third quarter of this year, Parex produced almost 55,000 barrels of oil-equivalent per day. And as you can see below, the vast majority of the oil-equivalent output consisted of heavy oil with light and medium oil generating just over 15% of the total oil-equivalent output . The company also produces some natural gas, but this represents less than 2% of the oil-equivalent output.

{kind=link}

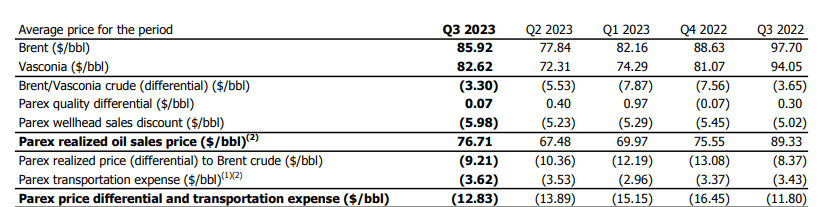

Thanks to the very strong oil price, the company's realized price also increased. As you can see below, the average price for Brent oil during the quarter (this is the benchmark for Parex' oil type) was almost $86/barrel while the local Vasconia oil price was $82.62 per barrel. After deducting the wellhead discount and the differential, the net realized price per barrel (excluding transportation costs) was $62.26/barrel after also taking the $13.72 in royalty payments into account.

{kind=link}

This resulted in an operating netback of almost $49/barrel, which is about 10% higher than the average operating netback generated in the entire first semester.

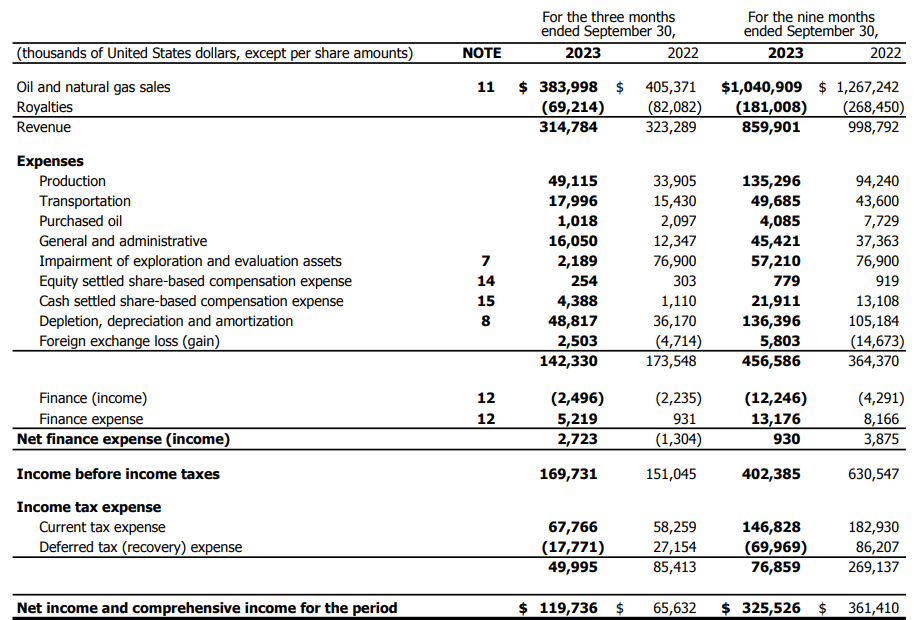

The good production results (compared to the same quarter as last year) and strong oil price helped the company to keep the net revenue pretty stable as it reported total revenue of just under $315M versus $323M in the third quarter of last year (the company reports its financial results in US Dollars).

{kind=link}

The total operating expenses were still very reasonable at $142M and as there are hardly any finance expenses, the total pre-tax income was a very reasonable $169.7M which ultimately resulted in a net profit of just under $120M which represents an EPS of US$1.13 (approximately C$1.53 at the current exchange rate).

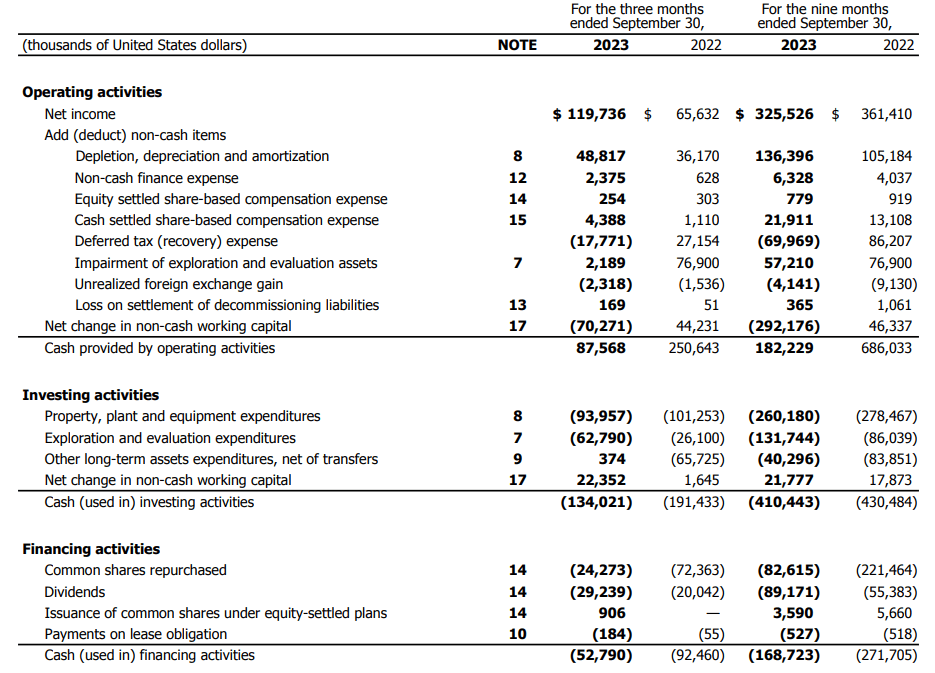

And from a cash flow perspective, Parex continues to put in a very strong performance as well. In the third quarter of the year, the company published an operating cash flow of $87.6M but this includes a $70.3M investment in the working capital and excludes a $0.2M lease payment.

{kind=link}

This means that on an adjusted basis, the operating cash flow was approximately $157.7M and considering the total capex was $157M, Parex was cash flow neutral. Then you wouldn't expect the company to pay dividends and to buy back stock, but keep in mind Parex has embarked on an investment program which should increase the reserves and the average annual production rate.

The company has guided for a full-year capex of $450-$475M which should initially push the average production rate to 57,000-63,000 barrels of oil-equivalent per day but this was later revised to 54,000-57,000/day. Given the average production rate in the first nine months of the year, I don't expect the company to get to the higher end of that guidance but it was very encouraging to see Parex reached an average production rate of 59,000 boe/day by the time it published its Q3 results.

This also indicates the fourth quarter should be pretty strong as well, despite the lower oil price. Parex will likely see a 6-9% increase in its production rate while the capex will likely decrease from the $150M+ in Q3 and the $130M average it recorded in the first three quarters of the year. Assuming a full-year capex of $475M, the Q4 net capex should be just around $85M. Parex will publish an updated outlook for 2024 in January, and it also aims to publish a three year outlook at the same time so it will be interesting to see if Parex will continue its focus on expanding and investing.

Investment thesis

I currently do not have a position in Parex Resources as I shifted my attention to some other oil names as the Parex share price remained much stronger than its peers. I was hoping for a bigger pullback in its share price as I am definitely still interested in re-initiating a long position in the company, but I am in no rush. And of course, the continuous share buybacks increase the residual value per share: in the past seven quarters, Parex has repurchased 16.2M shares and reduced its net share count by 15.2M shares.

Parex is still trading at an attractive level and I am definitely looking forward to the company's updated guidance for 2024 and the 2024-2026 era.

For further details see:

Parex Resources: Attractive, But I'm Hoping For A Bigger Pullback