CA - Park Lawn: Temporary Headwinds Signal A Buy For The Deathcare Provider

2023-12-13 13:48:32 ET

Summary

- Park Lawn engages in various services in the deathcare industry and has attractive business characteristics with the potential for steady growth.

- The company's stock has experienced a sharp decline since 2022, presenting an opportunity for investors to buy at a lower valuation and higher dividend yield.

- Park Lawn is the second-largest listed company in its industry and has a sharpened focus on returns on capital, acquisitions, and organic growth.

Canadian company Park Lawn Corporation (PLC:CA) (PRRWF) engages in different services for the afterlife. The company has attractive and stable business characteristics with a long pathway for steady growth. Since the beginning of 2022 Park Lawn's stock has experienced a sharp 60% decline from its highs, when the company was benefiting from the pandemic.

The decline could represent an opportunity to invest in a company that suffers from temporary headwinds, appears to have a sharpened focus on returns on capital, is lower valued and indebted than its listed competitors and pays a decent dividend.

Park Lawn mixes the deck

Park Lawn is a Canadian company operating cemeteries, funeral homes and crematoriums. It's a collection of different local brands and operational companies. A majority of its over 300 locations are in the United States and the rest are located in Canada. In 2022 its annual revenue was $326 million and it had approximately 2500 employees. Approximately 90% of the revenues were generated in the U.S.

According to Park Lawn a majority (80%) of the death care industry is privately owned. This means that there are plenty of opportunities for inorganic growth for various consolidators. Although Park Lawn itself claims that it's not a consolidator but an operating company, 60% of its businesses have joined the company in the past 5 years. It is important to appear an acquirer with integrity as demonstrated in the recent movie The Burial and the true story behind it, which I believe led to the downfall of the Loewen Group and its sale to Service Corporation.

At the moment Park Lawn is the second-biggest listed company in its business. Service Corporation International ( SCI ) is by far the largest with nearly 2000 locations and revenues over 10 times more than Park Lawn. Carriage Services, Inc. ( CSV ) has a little over 200 locations but a similar level of revenue. In June Park Lawn pursued an all-cash offer for Carriage Services but later in October withdrew its offer.

Opportunity for a longer horizon

Temporary headwinds for a stable business

The shares of Park Lawn have gone through a major correction. This is likely a result of the sell-off of levered companies, the decline of earnings after the peak caused by the pandemic and consumers currently reducing their discretionary spending combined with rising costs - visible in the revenue and net income figures. The company expects the mortality rate to fall down further by low to mid-single-digit next year, which is a continuation of the normalization of the death rates after the pandemic.

Share price development. (YCharts)

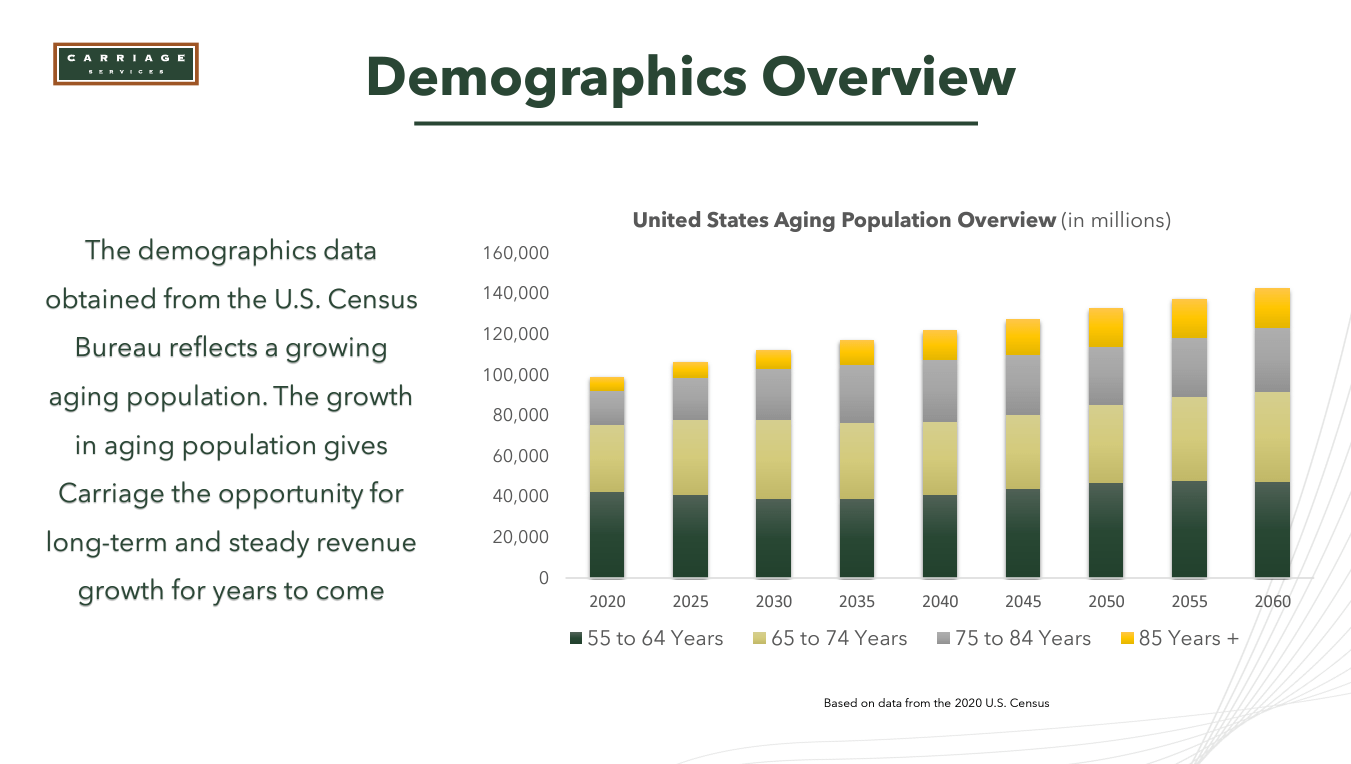

For a long-term income investor the correction could represent an opportunity to acquire shares in a stable business that has multiple drivers for growth. It has a major demographic trend supporting its underlying business, there's plenty of room for acquisitions and the company is investing in organic growth with a 20% IRR target.

Demographics overview. (Carriage Services.)

{kind=link}

Potentially sharper focus on returns on capital

Recently, Park Lawn announced the disposal of 72 cemeteries and 11 funeral homes in four different U.S. states as they "did not fit with long-term growth strategy" according to the latest earnings call. Park Lawn acquired these assets in 2018. The deal has not yet closed, which means that the current financials don't yet reflect its impact. The $70 million price had a valuation of 8x adjusted EBITDA. Park Lawn expects the divestiture to be dilutive to its earnings per share. The assets were sold to Everstory which has grown to be a bigger privately owned deathcare company.

The CEO of Park Lawn, James Bradley Green, has held the role since 2020. Now he and part of his team are facing normal or normalizing operating conditions for the first time. Previously Green worked for Carriage Services for over five years and was involved with acquisitions. Therefore, he should have a good understanding of how the competitor generates superior returns compared to Park Lawn.

The recent corporate actions and earnings calls suggest that the management has a sharpened focus on returns on capital and the quality of its portfolio. An increase in capital efficiency and margins would be required to justify aligned valuation compared to its peers. In addition to the asset disposal, Park Lawn has withdrawn from a cemetery development, which it deemed not meeting the investment requirements, and promising commentary from the management.

And those businesses are going to be higher growth potential, higher-margin businesses, things that we can really go in and improve, and that's what we're looking to do. And so when you see us looking, canceling projects that don't make sense on a capital basis and things of that nature, that's right. We're looking to make sure that we get to where we're extremely efficient and are operating, and then we can return more consistent numbers quarter-over-quarter. -James Green, Q3 earnings call

Returns on capital of PLC and its peers. (YCharts)

Navigating the key risks

The increasing share of cremations instead of archburying is one of the counterforces to the favorable demographic trend. According to Park Lawn, the cremation method has been a more popular method since 2016 and its popularity is increasing. Park Lawn is also engaged in cremation in several states and provinces and offers a Cremate Simply service in two locations.

Park Lawn carries a net debt of $200 million. With the rising interest rates the debt servicing has impacted the EPS negatively by $0.04. With the above-mentioned divestiture the company expects the net debt to adjusted EBITDA to decline to 2.8x, which is significantly lower than Carriage Services and Service Corporation.

The lower debt level compared to its competitors, likely also the private equity-backed companies, could enable Park Lawn to engage in acquisitions better when the others could be holding back. The stable business model allows the companies in the industry to carry relatively more debt. If and when the interest rates decline, the shares of indebted companies could benefit.

Since the company is in the process of disposing of a large chunk of its assets, redeployment of the proceeds poses a major question. It is yet unclear what the company intends to do with the money. It is likely that the proceeds were intended to be used to finance part of the acquisition of Carriage Services since the two announcements, disposal and withdrawal of the offer, came only two weeks apart from each other. Soon, the company will have a large pile of cash but, most likely, no predetermined target for an investment.

Valuation is below its competitors but fair

The decline in share price and lower multiples could be reasoned partly by Park Lawn's indebtedness. Its debt position might not support its acquisition-fueled growth strategy as interest rates have risen. As slower growth is expected and while more cash goes to interest and debt repayments, lower than historical multiples are justified.

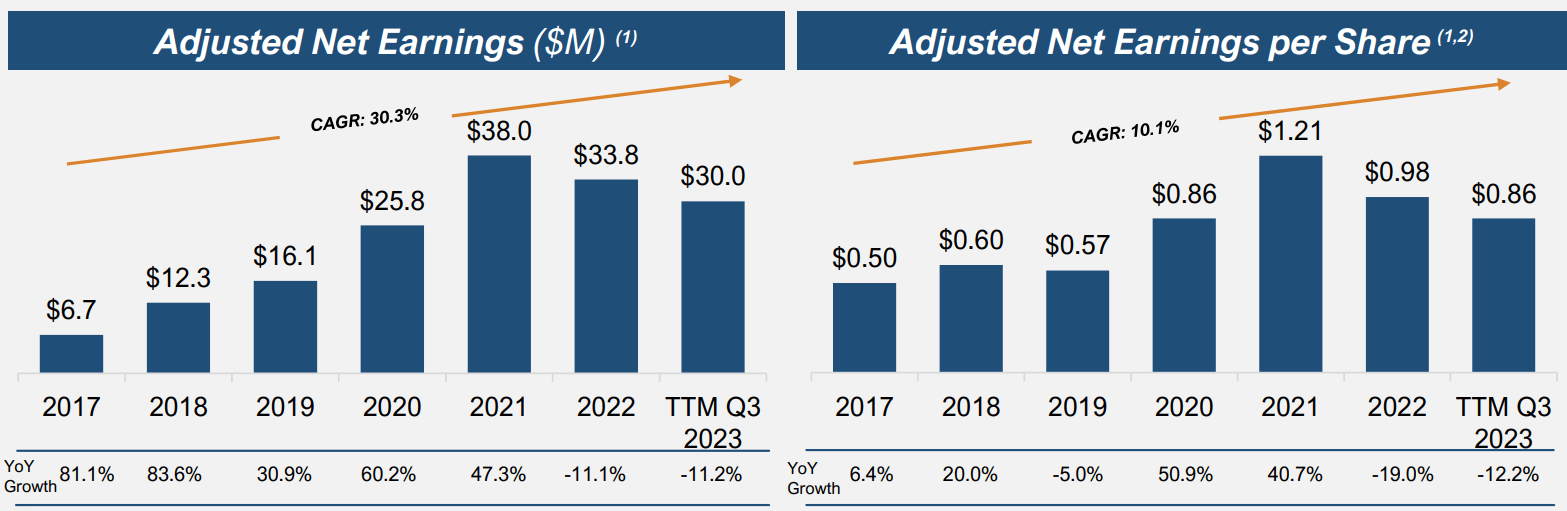

Earnings development. Figures in USD. (Park Lawn)

{kind=link}

Another major reason is the decline of net earnings margin, which has come down to 4.9% on a trailing twelve-month basis from 9.4% in 2021, when the company over-earned compared to its historical levels. Since 2017 the adjusted earnings per share have grown 10% per year. Analysts estimate the earnings to decline this year by 14%.

Earnings estimates. (Seeking Alpha)

Furthermore, it appears that the stock experienced further sell-offs in October when the company announced the withdrawal of the offer and disposal of the assets. From a positive perspective, both pieces of news can be perceived well. Withdrawal of the offer did not lead the company to a risky acquisition and now the company has an opportunity to potentially deploy the cash from the disposal in a more efficient way when the other consolidators might be holding back.

Compared to its two publicly listed peers Park Lawn stock is valued lower on several valuation multiples. Although Park Lawn has lower leverage, this can be explained by significantly lower margins and returns on capital. Service Corporation naturally has the benefits of a much larger scope and size. A full comparison is available here .

EV/EBITDA multiple of Park Lawn and its competitors. (Tikr)

Assuming an EPS of C$1.2 for 2024 and a current level of dividend, the stock is trading close to its fair value if the company can grow its earnings by 10% for the next 5 years and 5% thereafter. Here, a discount rate of 10% and a terminal multiple of 15x is applied. If a discount rate of 8% is applied the fair value would be C$20.5.

Estimation of the fair value based on earnings. (Author)

According to Seeking Alpha, there are seven analysts following the stock with an average target price of C$23.7 ranging from C$20 to C$28.8.

Historically high dividend and a hint about buybacks

For the past two years, Park Lawn has paid a quarterly dividend of C$0.114 resulting in a dividend yield of 2.5%. The yield has climbed up to a historically high level along with the decline of the share price. The four-year average yield is 1.6%. The current historical payout ratio stands at around 50%.

Dividend yield and payout ratio. (YCharts)

In the latest earnings call the CEO James Green also hinted about the possibility of buybacks due to the reason that the company made the sales at a higher multiple than the stock is trading at. The shares outstanding have moderately increased since mid-2021 after the company stopped financing acquisitions by issuing new shares.

Conclusion

Park Lawn is a company operating in a stable but structurally growing industry. It has the potential to grow through acquisitions and organic investments. Currently, it's facing temporary headwinds as the mortality rate normalizes and consumers are under pressure. Additionally, Park Lawn has placed itself in an unusual position with the pulled takeover offer and asset sales, which could have had an unjustified impact on the share price. When the temporary headwinds fade away the stock could have a good potential for upside.

For further details see:

Park Lawn: Temporary Headwinds Signal A Buy For The Deathcare Provider